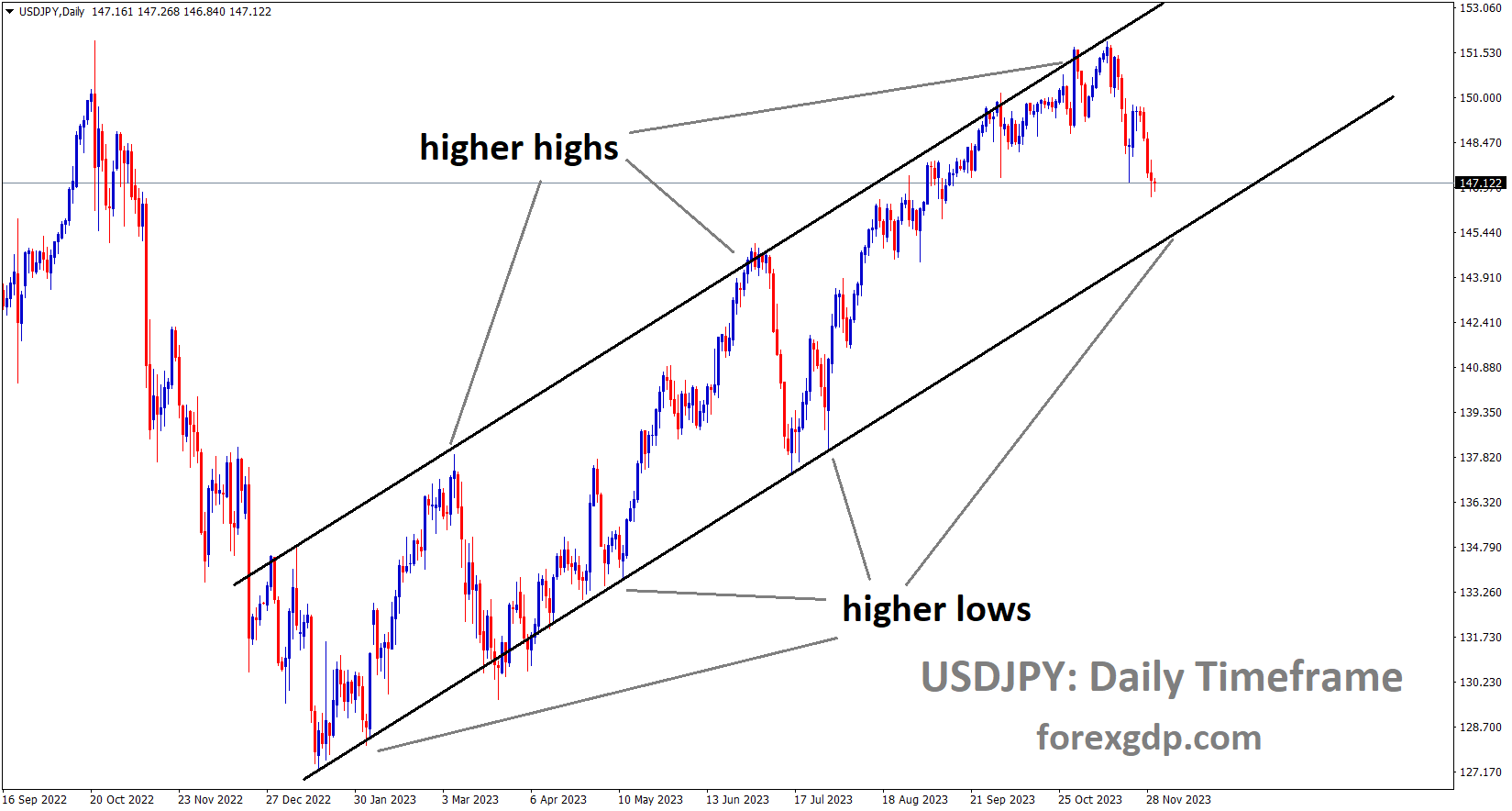

USDJPY Analysis:

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

Board member Toyoki Nakamura of the Bank of Japan emphasized that the policy shift requires additional time, and the convergence of wages and inflation is contingent on a specific event. This alignment is expected to persist as long as interest rates remain in the negative territory.

In October, Japanese industrial production recorded a growth of 1.0%, surpassing the previous month’s 0.50% and the expected 0.80%. On an annualized basis, there was a notable increase, with a reading of 0.90%, marking a positive shift from the previous year’s decline of -4.4%.

Bank of Japan Board member Toyoaki Nakamura, in his recent remarks on Thursday, shared insights regarding the potential departure from the central bank’s ultra-loose monetary policy. He indicated the difficulty in specifying the timing of such a policy shift at the moment. Nakamura emphasized the risk associated with altering the policy based on the assumption that future improvements in the Japanese economy are guaranteed.

He stressed that the current juncture is not suitable for contemplating a policy shift and highlighted the necessity to observe sustainable increases in wages and inflation before considering such a move. Additionally, Nakamura expressed the intention to assess firms’ profitability to determine the appropriate timing for a policy shift, mentioning the scrutiny of data, including the upcoming Ministry of Finance quarterly business sentiment survey, to gauge whether conditions are aligning for any potential policy adjustments.

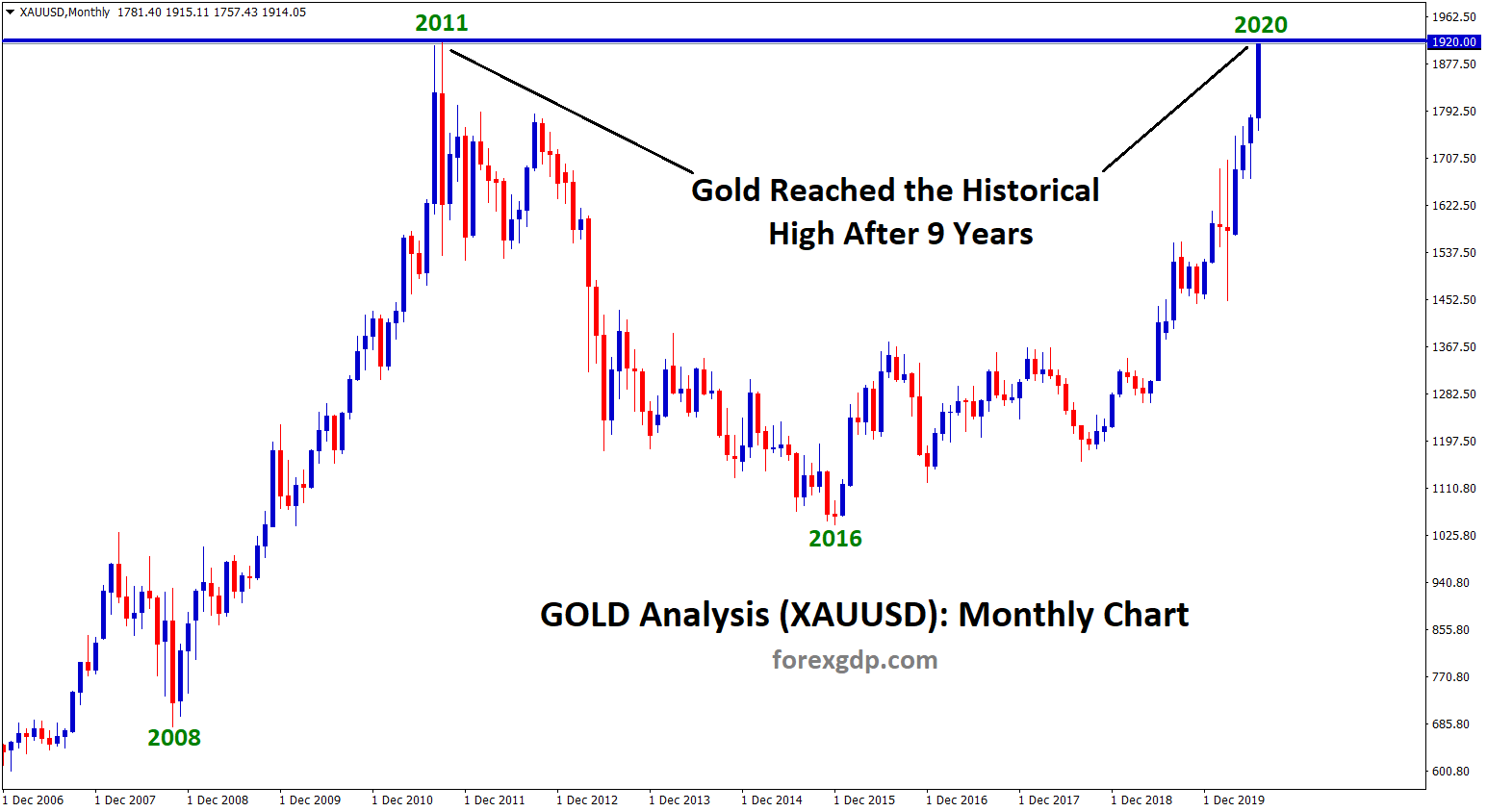

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

Despite the Q3 US GDP data surpassing expectations, gold prices continue to stay elevated in the market. The anticipation of a Federal Reserve rate cut in early 2024 provides strong support for an upward movement in gold prices. Gold prices continue their sideways movement as bullish investors choose to stay on the sidelines, awaiting the release of Personal Consumption Expenditures data from the United States before making new market entries. The core gauge of the Fed’s preferred benchmark, crucial for assessing longer-term inflation trends, is expected to significantly influence the next policy move and act as a driving force for the non-yielding yellow metal. Heading into this key data release, there is a growing consensus that the Federal Reserve (Fed) has concluded its policy tightening campaign, contributing to the weakening of the US Dollar and acting as a supportive factor for gold prices. Investors now appear convinced that interest rates in the US have peaked, with market expectations indicating a series of rate cuts by the Fed in 2024. The CME Group’s Fed Watch tool suggests a possibility of such a move as early as March 2024, with an almost 80% likelihood of a rate cut in May 2024. This sentiment is further reinforced by a continued decline in US Treasury bond yields, which fails to help the US Dollar build on its overnight bounce from its lowest level since August 11. China’s economic challenges also contribute to supporting the safe-haven appeal of gold.

Recent statements from various Federal Reserve officials, including Fed Governor Christopher Waller and Cleveland Fed President Loretta Mester, indicating the potential for future rate cuts, act as a tailwind for gold prices. Waller flagged the possibility of a rate cut in the coming months, while Mester expressed satisfaction with progress in achieving a 2% inflation target. Market expectations now incorporate a cumulative 100 basis points of rate cuts by the Fed in 2024, further evidenced by the sustained decline in US Treasury bond yields. The yield on the 10-year US government bond, which surpassed 5% in October for the first time in 16 years, remains near its lowest level since September 14. Additionally, the yield on the two-year US Treasury note, sensitive to rate changes, is at its lowest since July, contributing to the undermining of the US Dollar and providing support to XAUUSD. The second estimate of US GDP indicates that the largest global economy grew at a 5.2% annualized pace in the third quarter, exceeding the previously reported 4.9%. While this upbeat macroeconomic data provided a modest boost to the USD on Wednesday, dovish Fed expectations continue to limit any substantial recovery from its multi-month low. Recent data from the National Bureau of Statistics (NBS) reveals a slight decline in China’s Manufacturing PMI to 49.4 in November from 49.5 the previous month. The non-manufacturing PMI also dropped to 50.2 in November from 50.6, raising concerns about deteriorating conditions in the world’s second-largest economy.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

The third-quarter GDP data for the United States showed a growth rate of 5.2%, surpassing the previous quarter’s 2.9% and the anticipated 4.9%. Surprisingly, the US Dollar displayed minimal reaction following the release of this data yesterday. The Federal Reserve had initially projected a GDP growth of 1-2% for the fourth quarter, but the Q3 figures exceeded these expectations.In Q3 2023, the US economy demonstrated robust growth, expanding at an annualized rate of 5.2%. This figure, revised upward from the initial estimate of 4.9%, surpassed the anticipated 5%. The updated GDP estimate, released with more comprehensive source data than the previous “advance” estimate, revealed notable changes. Nonresidential fixed investment and state and local government spending saw upward revisions, contributing to the overall growth. However, this was partially offset by a downward revision in consumer spending. Remarkably, residential investment experienced a significant upturn, marking the first increase in nearly two years, surpassing initial expectations at 6.2% compared to the advance estimate of 3.9%. Private inventories played a pivotal role, adding 1.4 percentage points to growth. Government spending also increased at a faster pace, rising by 5.5% compared to the earlier estimate of 4.6%. Conversely, consumer spending slightly lagged behind expectations, increasing by 3.6%, but still marked the most substantial gain since Q4 2021.

Disposable personal income showed a notable increase of $144.0 billion or 2.9% in the third quarter, reflecting an upward revision of $48.2 billion from the previous estimate. Real disposable personal income experienced a 0.1% increase, revised upward by 1.1 percentage points. Surprisingly, the release had a limited impact on the US Dollar, which actually lost ground post-announcement. The outlook for 2024 suggests growing optimism for more assertive rate cuts, with influential figures like Bill Ackman speculating that the Fed might initiate rate cuts earlier than market expectations. Federal Reserve policymakers have notably adopted a dovish tone in recent comments, with some, like policymaker Bowman, maintaining a slightly hawkish stance. However, the pace of economic growth in Q4 is expected to slow, with Fed policymakers eyeing a range of 1-2%. Concerns linger about the service sector, which has faced heightened demand, keeping prices elevated. The end of 2023 and the start of 2024 will be pivotal in determining how the US economy navigates these challenges and whether the battle against inflation is firmly in the Federal Reserve’s rearview mirror.

USDCAD Analysis:

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

Today, the Canadian Q3 GDP is set to be unveiled, with an anticipated increase of 0.20% in the data. Concurrently, the OPEC+ Meeting is scheduled, and the outcome may influence oil prices. If the meeting hints at further rate cuts in 2024, it could support oil prices; however, if there is an indication of increased supply, it may lead to a decline in oil prices in the market. The Canadian Dollar is finding support from a weaker US Dollar and improved crude oil prices. The US Dollar Index appears poised to resume its downward trend after Wednesday’s gains, currently trading lower around 102.80. The USDCAD pair received a boost from stronger-than-expected US Gross Domestic Product Annualized data released by the US Bureau of Economic Analysis. Third-quarter US GDP annualized increased by 5.2%, surpassing the previous reading of 4.9% and exceeding the market consensus of 5.0%.

and its allies")

Western Texas Intermediate prices are on a three-day winning streak, trading near $77.90 per barrel at the moment. The momentum in crude oil prices is attributed to the upcoming meeting of the Organization of the Petroleum Exporting Countries (OPEC) and its allies. Anticipation surrounds the likelihood of Saudi Arabia and Russia proposing an extension of oil supply cuts into 2024. Concerns about oil demand have surfaced again following China’s economic data. The NBS Manufacturing PMI for November declined to 49.4 from the previous reading of 49.5, while the Non-Manufacturing PMI contracted to 50.02, falling below the expected 51.1. Canada’s Gross Domestic Product Annualized for the third quarter is set to be released on Thursday, with expectations of a 0.2% increase. Meanwhile, the United States will release crucial economic data, including Initial Jobless Claims for the week ending on November 24 and the Personal Consumption Expenditure Price Index data.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

The Swiss ZEW Survey results for November registered at -29.6, showing an improvement from October’s figure of -37.8. The third-quarter GDP data for the Swiss region is set to be released this upcoming Friday.

The recent decrease in US bond yields over the past three sessions is attributed to the prevailing positive sentiment suggesting that the Federal Reserve may conclude its interest rate hikes. However, as of the current press time on Thursday, the 10 and 2-year US Treasury yields have inched slightly higher to 4.27% and 4.65%, respectively. Furthermore, the US Dollar received support from stronger Gross Domestic Product Annualized data, which exhibited a 5.2% increase in the third quarter, surpassing the expected rise of 5.0%.

The focus will now shift to Initial Jobless Claims for the week ending on November 24 and Personal Consumption Expenditure Price Index data. Cleveland Federal Reserve President Loretta Mester emphasized that any decision to implement additional hikes would hinge on data-driven considerations. She highlighted that the current monetary policy is well-placed to assess forthcoming data on the economy and financial conditions.

GBPCHF Analysis:

GBPCHF is moving in the Box pattern and the market has fallen from the resistance area of the pattern

On the Swiss front, the Swiss Franc remains supported and strengthened by the hawkish comments from Swiss National Bank Chairman Thomas Jordan, who has not ruled out the possibility of future interest rate hikes. The ZEW Survey Expectations report indicated a decline to 29.6 figures in November compared to the previous contraction of 37.8. Additionally, attention will be on Swiss Real Retail Sales for October on Thursday and the Gross Domestic Product for the third quarter on Friday.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

Governor Bailey of the Bank of England emphasized that additional rate hikes in the market will continue until inflation is brought under control and aligned with our goals. The ongoing hawkish stance of the Bank of England’s rate hikes contributes to strengthening the GBP against its counterparts. Bank of England Governor Andrew Bailey has underscored the central bank’s dedication to taking necessary measures to bring inflation down to its 2.0% target. Despite the efforts made, Bailey noted a lack of sufficient progress, casting uncertainty on achieving the inflation goal. This hawkish stance may have contributed to the upward support for the Pound Sterling.

Meanwhile, the recent decrease in US bond yields over the past three sessions is attributed to the prevailing positive sentiment that the Federal Reserve might conclude its interest rate hikes. However, as of the current press time on Thursday, the 10 and 2-year US Treasury yields have slightly increased to 4.27% and 4.65%, respectively. The US Dollar Index hovers around 102.80 at the moment, exhibiting indecision likely influenced by mixed remarks from Federal Reserve members. Cleveland Federal Reserve President Loretta Mester has highlighted that any decision to implement additional interest rate hikes would rely on data-driven considerations. Governor Michelle Bowman’s expressed desire to maintain the possibility of more rate hikes raises concerns about the persistence of inflationary pressure. In contrast, Fed Governor Christopher Waller has suggested a more accommodative approach by not insisting on maintaining high-interest rates.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

In November, German inflation decreased to 3.2% from the October figure of 3.8%. The governing factor influencing Germany’s inflation is the European Central Bank’s policy of implementing rate hikes. In Germany, inflation eased to 3.2% compared to November 2022, marking a further decline from the 3.8% year-on-year figure recorded in October. Notably, there was a month-on-month decrease of 0.4%, surpassing the estimated -0.2%. Tomorrow, the EU is set to release inflation data, and consensus estimates suggest a continued drop in both headline and core measures of inflation.

The declining trend in inflation has led to market expectations of rate cuts in 2024, aligning with the anticipated pace of cuts from the Federal Reserve, amounting to just over 100 basis points. However, there is a concern that inflation might decrease further in the EU, given that the European economy has not exhibited the same resilience as the US. This divergence in economic performance could intensify existing economic challenges, posing a potential threat to the Euro. The impact of the inflation report was overshadowed when the US GDP growth for the third quarter received an upward revision, leading to a downward move on the 5-minute time frame within the same trading day.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Australian private capital expenditure data for Q3 showed a growth of 0.60%, a decrease from the 2.8% recorded in Q2. The inclination of private companies to increase capital spending is influenced by higher interest rates in the economy. This trend is expected to alleviate inflationary pressures, leading the Reserve Bank of Australia to consider maintaining current interest rates in upcoming meetings. The Aussie pair is facing downward pressure, largely attributed to the resurgent US Dollar. Australia’s Private Capital Expenditure contracted by 0.6% in Q3, a notable decrease from the previous growth of 2.8%, falling short of the anticipated 1.0% rise. The data, released by the Australian Bureau of Statistics, indicates a decline in both current and future capital expenditure intentions within the country’s private sector. This contraction is expected to alleviate inflationary pressures, reducing the likelihood of an interest rate hike by the Reserve Bank of Australia.China’s NBS Manufacturing PMI for November declined to 49.4 from the previous reading of 49.5, missing the market expectation of an increase to 49.7. Furthermore, the Non-Manufacturing PMI contracted to 50.02, below the expected 51.1 and the previous reading of 50.6. The disappointing PMI data has sparked discussions about the need for additional stimulus, benefitting the Australian Dollar.

Although the US Dollar Index halted its four-day losing streak supported by stronger-than-expected US Gross Domestic Product Annualized data, it struggles to maintain its position. The data, released by the US Bureau of Economic Analysis, indicated a third-quarter increase in the value of final goods and services produced in the United States. Notable economic data releases later in the North American session include the weekly Jobless Claims for the week ending on November 24, with an expected increase to 220K from the previous 209K. Additionally, the Core Personal Consumption Expenditure Price Index for October is anticipated to show a slowdown in consumer inflation, with the expected annual rate decreasing from 3.7% to 3.5%. Australia’s Monthly Consumer Price Index for October reveals a reading of 4.9%, a decrease from the previous 5.6% in September and slightly below the expected 5.2%. Meanwhile, Australia’s seasonally adjusted Retail Sales data for October declined by 0.2% against market expectations of a 0.1% rise and the prior 0.9%. Reserve Bank of Australia Governor Michele Bullock cautioned that the current monetary policy, characterized by rate hikes, may dampen demand, especially considering persistent services inflation. Governor Bullock stressed the need for caution in using high-interest rates to combat inflation without inadvertently increasing the unemployment rate. US Federal Reserve Governor Christopher Waller suggested that if inflation consistently declines, maintaining high-interest rates may not be necessary. US Gross Domestic Product Annualized increased by 5.2% during the third quarter, surpassing the market consensus of 5.0%. The US Housing Price Index remained steady at 0.6% in September, in line with the expected figure of 0.4%. The CB Consumer Confidence Index experienced an uptick in November, rising to 102.0, following a downward revision of October figures from 102.6 to 99.1.

NZDUSD Analysis:

NZDUSD has broken the Descending channel in upside

Governor Orr of the Reserve Bank of New Zealand stated that inflation is expected to persist for an extended duration, and any rate hikes in forthcoming meetings will be contingent on data. Several rate hikes have already been implemented as part of efforts to manage inflation within the economy. The New Zealand dollar surged, propelled by a weakening US dollar and the Reserve Bank of New Zealand’s interest rate decision. Despite the central bank opting to keep rates unchanged, Governor Orr conveyed a notably hawkish and authoritative tone. Several key statements underscore this stance, including the expression of nervousness about inflation persisting outside the prescribed band.

Governor Orr also highlighted the gradual rise in the 10-year inflation expectation, expressing concern about the upward trend in longer-term inflation expectations. Emphasizing the global context, he acknowledged the significance of global rates for New Zealand, emphasizing the need for current interest rates to be maintained for an extended period. Moreover, the central bank signaled flexibility by asserting its ability to respond to unforeseen shocks outside regular policy meeting schedules. While current expectations in money markets do not anticipate further rate hikes in 2024, the RBNZ emphasized its commitment to data dependency. Should inflation data continue on its upward trajectory, the Reserve Bank of New Zealand might decisively opt for tightening monetary policy once again.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/