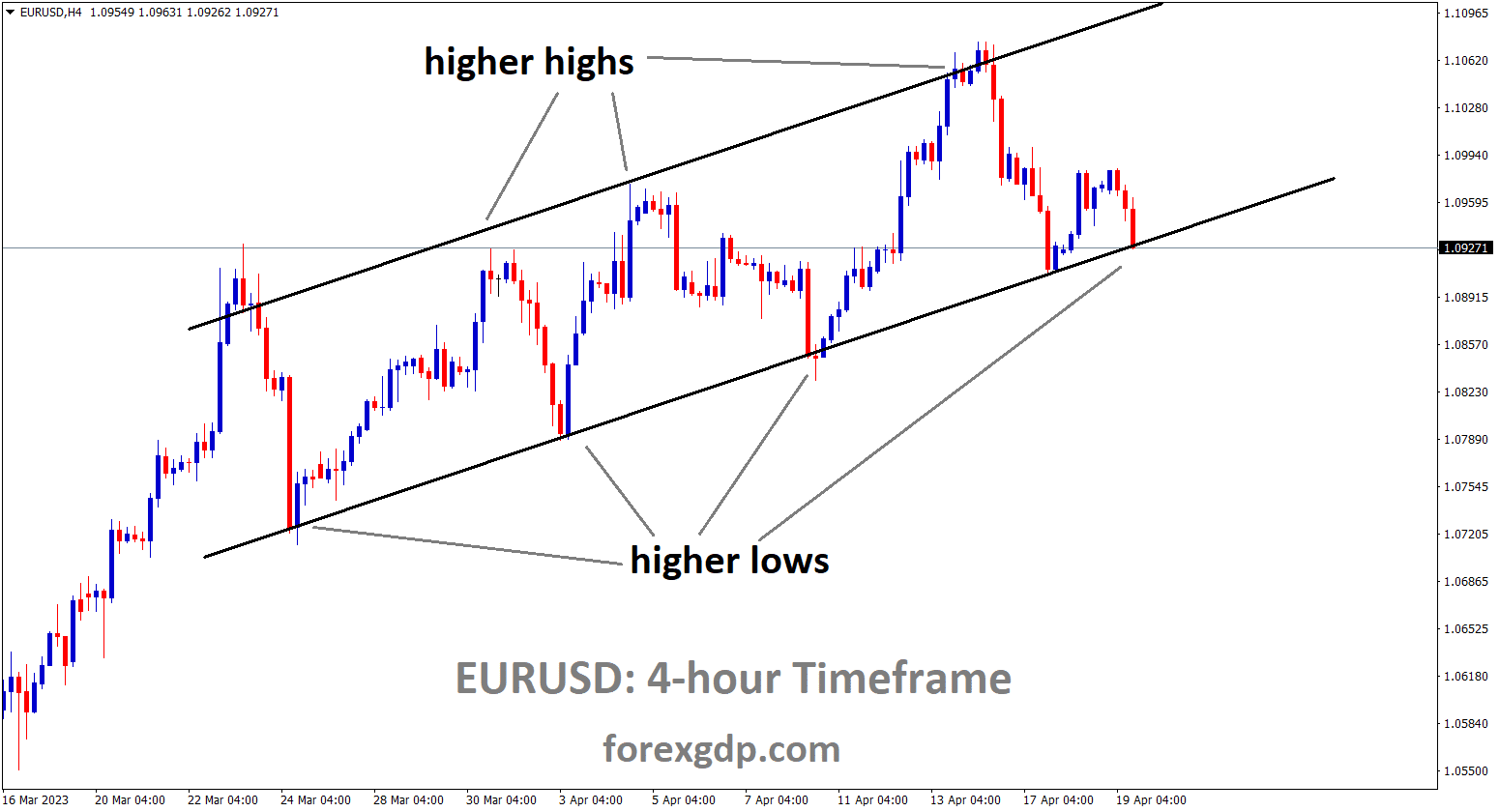

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

Gold prices continue to hold steady above the $2,060 mark, as the Middle East tensions show no signs of abating. Major shipping companies such as Maersk and CMACGM have been granted permission to conduct sea transportation in the Red Sea under the watchful presence of multinational military forces.

The rise in Gold prices can be attributed to traders taking into account the possibility of rate cuts by the Federal Reserve. Additionally, the WIRP indicates that the market has factored in a 15% probability of a rate cut on January 31 and has fully priced in rate cuts by March 20, with six rate cuts fully priced in by the end of 2024. Geopolitical tensions in the Middle East are contributing to a heightened risk-off sentiment, which is increasing demand for Gold as a safe-haven asset. Despite concerns, major shipping companies like Maersk and CMA CGM have begun to resume operations in the Red Sea, signaling a tentative return to normalcy with the deployment of a multinational task force in the region. We are eagerly awaiting Hapag-Lloyd’s decision on resuming shipments, which is expected on Wednesday. It’s important to note that while there are concerns about Iran potentially closing the Gibraltar Strait, many doubt the feasibility of such an action.

As of the current moment, the US Dollar Index remains below the 101.50 level. The DXY is facing downward pressure, influenced by subdued US Treasury yields. Both the 2-year and 10-year yields on US bonds are trading lower, with rates at 4.29% and 3.88%, respectively, as of the present time. This sentiment is further reinforced by former Dallas Federal Reserve President Robert Kaplan, who has highlighted the central bank’s past mistake of keeping interest rates excessively low for too long. Kaplan believes that the Federal Reserve is now proceeding cautiously to avoid repeating this error on the opposite end, ensuring that they do not become overly restrictive and potentially hamper economic growth. The US Dollar has also come under additional pressure due to the US Bureau of Economic Analysis reporting softer Core Personal Consumption Expenditures Index figures for November. US Core PCE Inflation has grown by 3.2%, falling short of the expected 3.3% and the previous 3.4%. Meanwhile, the Month-on-Month data has remained consistent at 0.1%, slightly below the market’s expected 0.2%. Looking ahead, Thursday is expected to bring the release of Initial Jobless Claims and Pending Home Sales data from the United States (US), providing further insights into the economic landscape.

SILVER Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has reached the support area of the Box pattern

Former Fed member Kaplan has expressed the view that the Federal Reserve is tardy in adjusting monetary policy settings. He believes that rate cuts should be implemented once both inflation and the economy show signs of weakening, as failing to do so could lead the economy into a recessionary phase.

On Tuesday, former Dallas Federal Reserve President Robert Kaplan expressed his anticipation that the central bank will initiate interest rate cuts in the near future to mitigate the potential risk of pushing the US economy into a recession. He highlighted the past mistake of the Federal Reserve, where it maintained an overly accommodative stance for an extended period even as the economy showed signs of improvement. Kaplan emphasized the central bank’s desire to avoid a similar error on the opposite end, where it becomes excessively restrictive. He noted that as the economy and inflation have softened, the Federal Reserve aims to strike a balance and not make the opposite mistake by staying too rigid in its monetary policy approach.

USDJPY Analysis:

USDPY is moving in the Descending channel and the market has reached the lower high area of the channel

The Bank of Japan has released a summary of its members opinions regarding policy settings in December 2023, affirming their commitment to maintaining ultra-easy monetary policy settings until inflation reaches the 2% target and wage increases become more evident in the months ahead.

The Bank of Japan has released the Summary of Opinions from its December monetary policy meeting, and here are the key points: One member emphasized the need to maintain monetary easing patiently. Another member stressed the importance of ensuring a sustainable and stable achievement of the price target before considering an end to negative rates and Yield Curve Control. A third member suggested closely monitoring wage and price movements under YCC, particularly in light of strong upward price pressures that are likely to stabilize. Yet another member expressed the view that even if wage hikes in the coming spring are significantly higher than expected, the risk of causing underlying inflation to significantly exceed 2% is minimal.

One member stated that the BoJ is not currently in a situation where they would be behind in raising rates, even if they decide to wait and assess wage negotiation outcomes next spring. Another member highlighted the importance of the BoJ providing clear communication regarding central bank balance sheet management to maintain confidence in its ability to conduct monetary policy during the exit phase. Lastly, one member noted that there is an increased momentum toward higher wage hikes compared to the previous year.

USDCAD Analysis:

USDCAD is moving in the Box pattern and the market has reached the Support area of the Box pattern

The Canadian Dollar is on the upswing due to the influence of heightened Middle East tensions and the Federal Reserve’s dovish stance on interest rates. Former Fed member Kaplan has stated that the Fed may need to reduce rates in the near future as the U.S. economy enters a recession.

Canadian economic data indicates a slowdown in the economy, with the month-over-month Canadian Gross Domestic Product (GDP) failing to register any growth for the fourth consecutive month in October, remaining flat at 0.0%. This follows a downward revision of September’s GDP figure from a modest 0.1% to flat. However, the US Dollar is facing downward pressure due to increasing speculations about potential monetary easing by the US Federal Reserve (Fed), which is constraining the upward movement of the USD/CAD currency pair. The ongoing weakening sentiment is further exacerbated by the decline in US Treasury yields, adding to the factors that are undermining the strength of the US Dollar. Furthermore, former Dallas Federal Reserve President Robert Kaplan shared his perspective with the media on Tuesday, emphasizing the Fed’s past mistake of maintaining prolonged excessive accommodation, even in the presence of positive economic indicators. He believes that the central bank is now proceeding with caution to avoid repeating this error on the opposite end, ensuring that they do not become overly restrictive and potentially hinder economic growth.

In addition to these factors, the US Bureau of Economic Analysis has reported a softer Core Personal Consumption Expenditures (PCE) Index for November, which has contributed to the pressure on the US Dollar. US Core PCE Inflation grew by 3.2%, falling short of the expected 3.3% and the previous 3.4%. Meanwhile, the month-on-month data remained consistent at 0.1%, slightly below the market’s anticipated 0.2%. Looking ahead, Thursday will see the release of Initial Jobless Claims and Pending Home Sales data from the United States. However, there are no scheduled economic data releases on the Canadian economic calendar for the week.

USDCHF Analysis:

USDCHF is moving in the Box pattern and the market has reached the Support area of the Box pattern

The Swiss Franc has surged against the USD to levels last seen in 2015, primarily because the Swiss National Bank has upheld its accommodative stance in its recent meeting. Additionally, heightened tensions in the Middle East have led to increased demand for the Swiss Franc as a safe-haven currency compared to the US Dollar. Increased risk aversion appears to be driving greater demand for safe-haven currencies such as the Swiss Franc. Concerns have arisen about the potential closure of the Gibraltar Strait by Iran, although many doubt the feasibility of such an action. Nevertheless, major shipping companies have begun returning to the Red Sea, suggesting a tentative return to normalcy with the presence of a multinational task force in the region. The Swiss National Bank (SNB) is positioned to take a proactive approach, as outlined in its recent Quarterly Bulletin. The SNB has communicated its preparedness to actively intervene in the foreign exchange market when necessary. This signals a hawkish stance, underscoring the bank’s commitment to managing currency dynamics and supporting the Swiss Franc.

The US Dollar Index has risen above 101.50, even as yields on US 2-year and 10-year bonds have declined to 4.29% and 3.87%, respectively, at the time of reporting. This decrease in yields contributes to the overall subdued performance of the US Dollar in the market. Former Dallas Federal Reserve President Robert Kaplan’s sentiments align with the notion that the central bank is proceeding cautiously. Kaplan emphasizes the Federal Reserve’s historical error of maintaining prolonged excessive accommodation, even as the economy improved. According to Kaplan, the central bank is now exercising caution to avoid a similar mistake on the opposite end, ensuring it does not become overly restrictive. Looking ahead to Thursday, significant insights into the economic landscape are expected as the United States is set to release data on Initial Jobless Claims and Pending Home Sales. These indicators play a crucial role in assessing the labor market’s health and the real estate sector’s condition, providing investors with essential information for evaluating the overall economic outlook.

GBPCHF Analysis

GBPCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

The GBP currency is gaining strength against the USD, driven by robust retail sales figures for November. With diminished expectations for a rate cut in the Bank of England’s outlook, it is anticipated that interest rates will remain accommodative in the upcoming meeting, further bolstering the GBP against the USD.

The Pound Sterling is exhibiting reduced volatility in a week characterized by thin trading. The GBPUSD pair maintains a generally positive outlook, with investors anticipating that the Bank of England will commence its rate-cutting measures later than the Federal Reserve. This optimism stems from the clear decline in inflationary pressures within the United States. Despite mounting concerns about a recession in the UK economy, investors are still directing funds into the Pound Sterling. Recent estimates indicate that the British economy contracted by 0.1% in the July-September period. According to the latest forecasts from the BoE, the economy is anticipated to remain stagnant in the final quarter of this year.

If the UK economy contracts again, it would officially enter a technical recession. Despite these challenges, the Pound Sterling continues to hold its ground against the US Dollar, benefiting from upbeat Retail Sales data for November, driven by robust sales at non-food retail stores. The boost in consumer spending resulted from higher discounts offered by non-food retail stores during Black Friday sales. Monthly Retail Sales saw a substantial increase of 1.3%, surpassing the consensus of 0.4% and the previous month’s stagnation. Surprisingly, annual sales at retail stores recorded a 0.1% increase, contrary to investor expectations of a 1.3% contraction.

GBPCAD Analysis:

GBPCAD is moving in the Descending channel and the market has reached the lower low area of the channel

The Pound Sterling maintains its strength despite deepening concerns about a recession in the UK economy. Revised estimates from the UK Office for National Statistics revealed a 0.1% contraction in the economy during the third quarter of 2023, contradicting earlier expectations of stagnation. Additionally, the Bank of England’s latest projections indicate an expected economic standstill in the final quarter of this year. Last week, the UK’s Finance Minister, Chancellor of the Exchequer Jeremy Hunt, mentioned a reasonable possibility that the central bank might decide to reduce interest rates if inflation continues to decrease. However, BoE policymakers have been cautious about implementing interest rate cuts, even with a significant decline in the price index. Stronger wage growth has cast doubt on whether inflation is clearly on a downward trajectory. Barclays recently suggested that the BoE might initiate its rate-cutting campaign as early as May, contrary to the previous expectation of August.

Early rate-cut expectations are driven by factors such as the anticipation of a recession in the UK economy and Chancellor Jeremy Hunt’s unusual suggestion that the central bank consider rate cuts to stimulate growth. Looking ahead, market sentiment is expected to remain subdued during this holiday-shortened week. The US Dollar Index is trading near a five-month low around 101.46, primarily due to a more significant than expected decline in the core Personal Consumption Expenditure price index for November. This has fueled expectations of early rate cuts by the Federal Reserve. The monthly US core PCE data grew by a mere 0.1%, falling short of the 0.2% growth rate recorded for October. On an annualized basis, underlying inflation has decelerated to 3.2%, below the consensus of 3.3% and the previous reading of 3.5%. It’s worth noting that the Federal Reserve, in its Summary of Projections released last week, forecasted core PCE to be at 3.2% by year-end.

EURJPY Analysis:

EURJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

ECB Vice President Luis De Guindos has emphasized that it is too early to consider easing monetary policy settings, suggesting that the Eurozone may not face a recession in 2024. He advocates for a data-dependent approach to rate cuts.

According to Bank of Japan Governor Ueda, any adjustments to monetary policy settings should only occur when wage increases match the 2% inflation target. Otherwise, there is a risk that the economy could transition into an inflationary state that is difficult to manage.

The Federal Reserve’s preferred measure of inflation, the Core Personal Consumption Expenditures Price Index, grew by 3.2% year-on-year, slightly below the expected 3.3%. On a monthly basis, the Core PCE saw a 0.1% increase, falling short of the consensus forecast of 0.2%. At its recent December meeting, the Federal Open Market Committee opted to maintain the current interest rate and hinted at the possibility of three rate cuts in 2024. Turning to the Eurozone, the European Central Bank chose to leave its benchmark interest rates unchanged during its final meeting of the year. ECB President Christine Lagarde emphasized that the ECB’s policy decisions are contingent on economic data rather than influenced by market expectations or rigid timelines.ECB Vice President Luis de Guindos stated that it is premature to consider easing monetary policy and expressed the central bank’s belief that a technical recession in the Eurozone is not anticipated. These more hawkish comments from the ECB could potentially bolster the Euro.

Bank of Japan Governor Kazuo Ueda addressed the Japan Business Federation meeting on Monday. Ueda expressed that the likelihood of attaining the central bank’s inflation target was gradually increasing, and they would contemplate adjusting their policy if the prospects of consistently achieving the 2% target improved substantially. He noted that service prices were gradually accelerating, although many firms found it challenging to pass on rising labor costs. Ueda stated that if a positive wage-inflation cycle strengthened and the outlook for achieving the price target on a sustainable basis improved sufficiently, they would consider altering their monetary policy. He emphasized that the timing of any future policy change couldn’t be predetermined but would be decided upon while closely monitoring economic developments and firms’ wage and pricing behaviors.

In an economy where sustained positive inflation prevails, nominal interest rates would be higher, allowing the central bank room to implement significant interest rate cuts when necessary. Ueda pointed out that effective monetary policy would reduce the risk of a sharp deterioration in the economy or a return to deflation. The Bank of Japan’s strategy is to patiently maintain monetary easing to ensure that any changes in firms’ wage and pricing behavior are enduring. Ueda reiterated that they would meticulously assess economic developments, including the potential strengthening of the positive wage-inflation cycle, and make appropriate decisions to achieve the price target sustainably. While it may take some time, the upward pressure from past increases in import prices is expected to gradually diminish. Ueda emphasized that their future monetary policy decisions would be made thoughtfully by examining economic developments and firms’ wage and pricing behaviors.

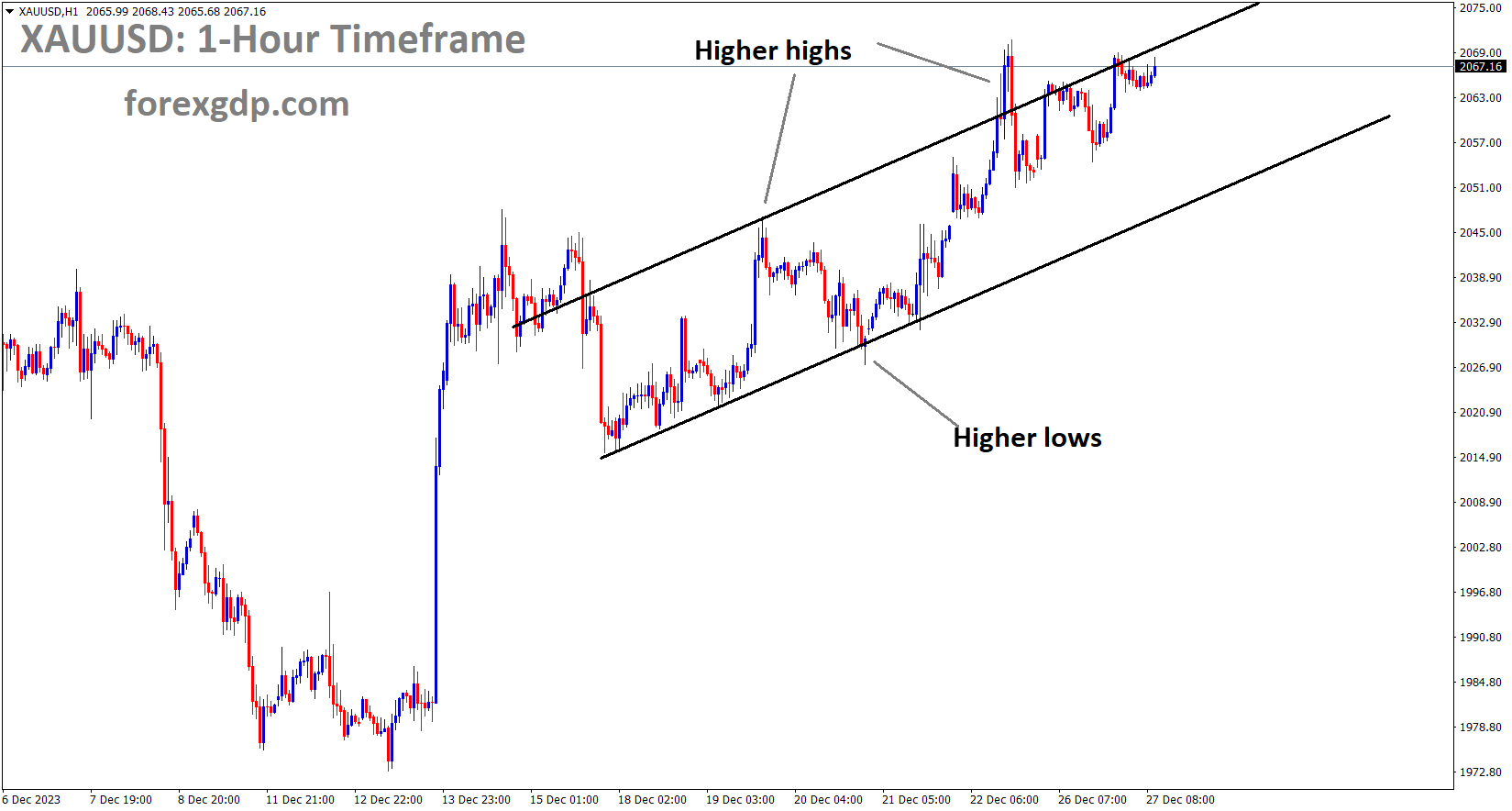

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The Australian Dollar is gaining strength following the release of the RBA statement, which indicates a positive sentiment regarding the upcoming monetary policy meeting. With the RBA aiming to reach its 2-3% target by 2025, it is likely that an interest rate hike will be considered in the forthcoming meeting.

On Wednesday, the Australian Dollar is on an upward trajectory, driven by improved risk appetite, while the US Dollar might exhibit signs of weakness due to speculation about the Federal Reserve adopting a dovish stance on interest rates. Australia’s central bank holds a hawkish outlook, fueled by strong inflation and stable housing prices, which is bolstering the Australian Dollar’s resilience. The upcoming year may witness a tug-of-war between expectations of rate cuts and the Reserve Bank of Australia’s resistance. With the latest RBA forecasts approaching the upper boundary of the 2-3% inflation target by the end of 2025, the RBA may remain open to further deliberation. China’s year-on-year Industrial Profits for January to November recorded a 4.4% decline, signaling a slowdown and underscoring the need for additional policy support from Beijing to stimulate growth in the world’s second-largest economy. China plays a central role in shaping the global economic landscape in 2024, characterized by stable inflation and low borrowing costs. The world is closely monitoring global economic momentum, especially with the potential for economic stimulus from China. Such developments could sway the Reserve Bank of Australia (RBA) to maintain its hawkish stance, influenced by trade relations between the two countries.

Meanwhile, the US Dollar Index is under downward pressure amid increasing speculation of potential easing by the US Federal Reserve. This sentiment is further compounded by the decline in US Treasury yields, contributing to the factors eroding the strength of the US Dollar. Former Dallas Federal Reserve President Robert Kaplan shared his insights with the media on Tuesday, emphasizing the Federal Reserve’s past mistake of maintaining excessive accommodation for an extended period, even as the economy showed signs of improvement. He believes that the central bank is being cautious to avoid repeating this mistake on the opposite end, ensuring that it doesn’t become overly restrictive. Regarding economic data, RBA Private Sector Credit showed a 0.4% increase in November, surpassing the previous rise of 0.3%. However, the Year-over-Year data indicated a decrease of 4.7%, compared to the previous 4.8% rise. The RBA highlighted the need to examine additional data to assess the balance of risks before making decisions on future interest rates in its recent Meeting Minutes. In the United States, the Housing Price Index contracted to 0.3% in October from the previous 0.7%, falling short of the expected 0.5%. The US Bureau of Economic Analysis reported that the Core Personal Consumption Expenditures – Price Index grew at 3.2% in November, missing the 3.3% expectations and the 3.4% previous figure. Meanwhile, the month-on-month data remained consistent at 0.1%, falling short of the market’s expected 0.2%. Lastly, US Gross Domestic Product Annualized grew at a rate of 4.9% in Q3, slightly below the expected 5.2%.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

As a result of the Christmas and New Year holidays, the Forex markets are experiencing reduced trading activity. The New Zealand Dollar has seen an increase in value against the USD, attributed to the Federal Reserve’s dovish stance and a series of unfavourable domestic data releases in recent weeks.

On Tuesday, the dollar index declined while the euro reached its highest level in over four months as investors awaited fresh signals regarding when the Federal Reserve might commence interest rate cuts, given that inflation is edging closer to the central bank’s annual target of 2%. Trading activity remained subdued on the day after Christmas, with several markets, including the UK, Australia, New Zealand, and Hong Kong, observing public holidays. Furthermore, many traders around the world are still on holiday until the New Year. The greenback is currently on track to register its weakest performance since 2020 against a basket of currencies, primarily due to expectations of Fed rate cuts, which have diminished the appeal of the US currency relative to its counterparts. Many analysts anticipate a notable slowdown in the US economy in 2024. However, the Fed is also expected to take action to ensure that the gap between the fed funds rate and realized inflation does not widen significantly. If inflation declines more rapidly than the Fed’s benchmark rate, it can inadvertently tighten monetary conditions beyond what Fed policymakers intend, thereby increasing the risk of a severe economic downturn. Analysts at Action Economics noted in a report on Tuesday that inflation is expected to continue cooling, providing policymakers with the flexibility to reduce rates by June to prevent inadvertent tightening in real interest rates. However, they disagree with the market’s expectation of a cut as early as March and the pricing of 154 basis points in easing by December. They believe such aggressive action is unlikely unless the economy were to slide into a recession in the coming months. Recent data revealed that US prices declined in November for the first time in over 3.5 years, further pushing down the annual inflation rate.

In contrast, annual home prices in October continued to rise, indicating the ongoing recovery of the housing market, according to data released on Tuesday. Additionally, a Mastercard report indicated that US retail sales increased by 3.1% between November 1 and December 24, as consumers sought last-minute Christmas bargains during significant promotions. As of the latest data, the dollar index was down 0.18% for the day, trading at 101.44. It has retreated from its 20-year high of 114.78 on September 28, 2022, and is heading for a yearly loss of 1.98%. The euro strengthened by 0.20% to $1.1045, its highest level since August 10. The single currency has rebounded from a 20-year low of $0.9528 on September 26, 2022, and is set for a 3.08% gain this year.

Against the yen, the dollar increased by 0.06% to 142.47. It previously reached a 32-year high of 151.94 yen on October 24, 2022, and came close to reaching that level again last month before the Japanese currency staged a recovery. The dollar is on track for an 8.68% gain this year. The yen has stabilized near a recent five-month peak, as there is a belief that the Bank of Japan may soon signal an end to its ultra-easy monetary policy. For most of 2022 and 2023, this policy has exerted downward pressure on the Japanese currency, as other major central banks embarked on aggressive rate-hiking cycles. BOJ Governor Kazuo Ueda mentioned on Monday that the likelihood of achieving the central bank’s inflation target was gradually increasing, and they would consider adjusting their policy if prospects for sustainably achieving the 2% target improved sufficiently.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/