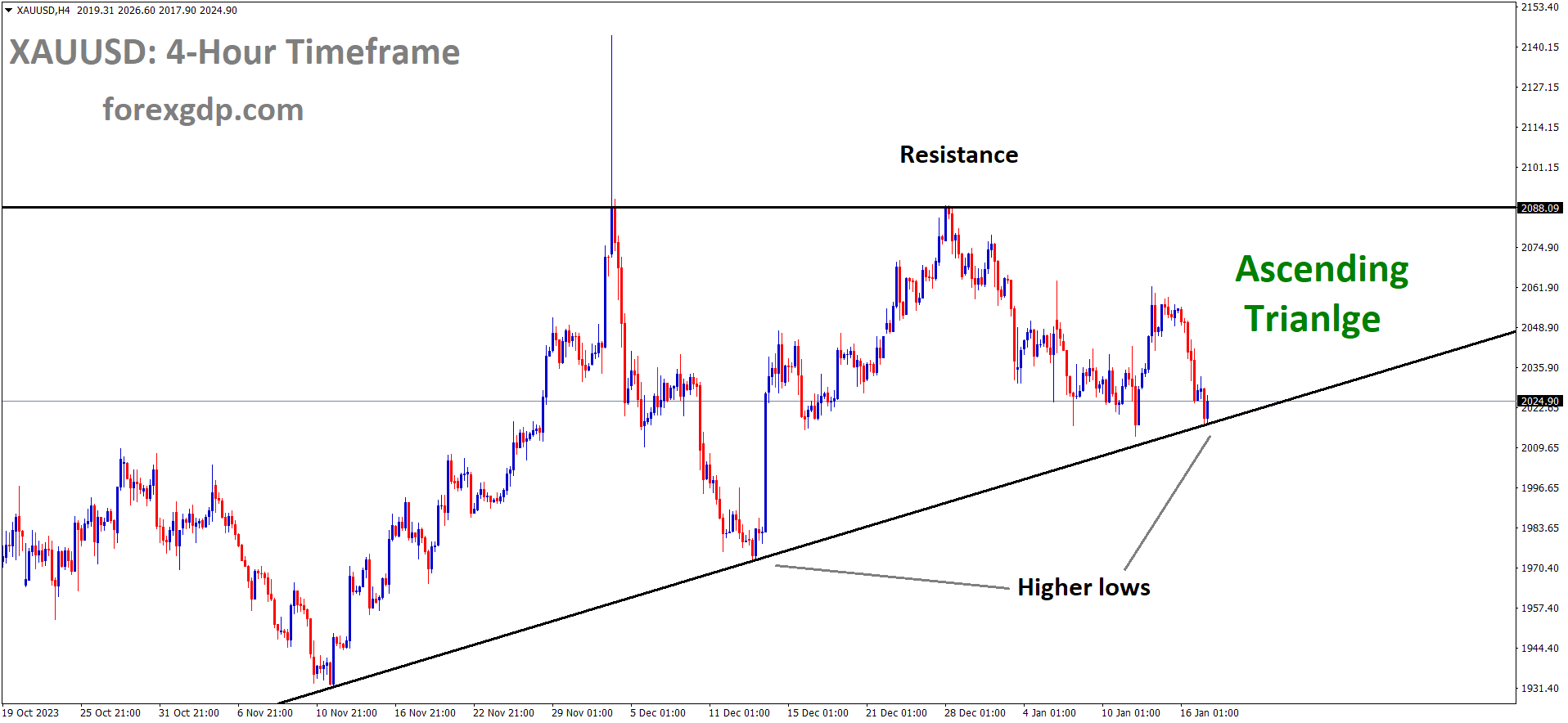

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending triangle pattern and the market has reached the higher low area of the pattern

Gold prices have declined as geopolitical tensions across the Red Sea have escalated. The anticipation of a rate cut by the Federal Reserve in the March meeting is waning in the wake of these conflicts in the Red Sea region.

Federal Reserve Governor Christopher Waller’s remarks on Tuesday prompted investors to further reduce their expectations of an imminent interest rate cut by the US central bank. This has bolstered US Treasury bond yields, pushing the US Dollar to a level not seen in over a month and diverting investment away from gold, which does not yield interest.

Simultaneously, the diminishing likelihood of a Fed rate cut in March, combined with geopolitical tensions and lackluster economic growth data from China, has tempered investors’ appetite for riskier assets. While this has resulted in a generally subdued sentiment in equity markets, it has not sparked renewed demand for the safe-haven gold price. Consequently, the prevailing trend for XAUUSD appears to be downward. Traders are now closely monitoring US macroeconomic data releases and speeches by influential FOMC members for short-term trading opportunities.

Federal Reserve Governor Christopher Waller’s recent statements have further eroded expectations of a rate cut in March, posing a challenge to gold, which does not generate yield. Waller emphasized the need for caution and avoiding hasty rate cuts, given the overall health of the economy. This stance has driven up US Treasury bond yields, which, in turn, have supported the US Dollar while capping gains for gold, a non-yielding asset. Despite the potential for increased Middle East tensions, gold has failed to find support, and bullish sentiment remains muted.

In the latest development, the US conducted another airstrike targeting a Houthi missile facility in Yemen, citing a threat to merchant vessels and US Navy ships. Official data from the National Bureau of Statistics revealed that China’s economy grew at an annual rate of 5.2% in the final quarter of 2023. On a quarterly basis, Chinese GDP expanded by 1.0% in Q3, matching expectations, while December Retail Sales and Industrial Production increased by 7.4% and 6.8% YoY, respectively. Following the release of this impactful data, the NBS acknowledged that China’s economy faces challenges due to a complex external environment and low consumer prices reflecting weak domestic demand. Despite these challenges, the combination of geopolitical risks and China’s economic uncertainties may prevent traders from aggressively betting against gold and could help limit further losses. Traders are now awaiting US macroeconomic data, with expectations of a 0.4% growth in monthly Retail Sales for December and flat Industrial Production. Scheduled speeches by Fed Governors Michael Barr and Michelle Bowman may also influence the USD and provide momentum to the commodity.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending triangle pattern and the market has reached the horizontal support area of the pattern

The US Dollar remains dominant across the global currency spectrum, fueled by lingering uncertainties related to China’s economic challenges and ongoing geopolitical tensions in the Middle East. China’s economic situation continues to raise concerns, with its fourth-quarter Gross Domestic Product growth coming in at 5.2% year-on-year, falling short of market expectations of a 5.3% expansion. Furthermore, on a quarterly basis, Chinese GDP exhibited signs of losing momentum by increasing 1.0% in Q4, in line with expectations. In December, China’s Retail Sales grew by 7.4% year-on-year, missing the anticipated 8.0% growth, while Industrial Production saw a 6.8% year-on-year increase for the same period, surpassing the expected 6.6%. On the geopolitical front, the situation escalated as Iran-backed Houthi rebels targeted a US-owned cargo vessel with an anti-ship ballistic missile near the Yemeni coast, adding to market jitters.

Additionally, the US Dollar is receiving support from recent comments by US Federal Reserve Governor Christopher Waller, who shifted away from his earlier dovish stance. Waller stated on Tuesday that, despite inflation nearing the central bank’s 2.0% target, the Fed should exercise caution and avoid rushing to cut interest rates until there is clear evidence of sustained lower inflation. Market sentiment is now pricing in a 62% probability of a Fed rate cut in March, as indicated by the CME Group’s Fed Watch tool. This is a notable decrease from the 81% likelihood at the beginning of the week. The US Dollar continues to capitalize on reduced expectations of aggressive Fed rate cuts, thanks to a more hawkish tone from various Fed officials. Nevertheless, the upcoming release of US Retail Sales data will play a pivotal role in shaping market expectations regarding Fed rate cuts for the rest of the year.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The US Central Command has reported a third airstrike targeting a Houthi missile facility in Yemen. The rationale behind this latest military action is the perceived imminent threat posed by four missiles to merchant vessels and US Navy ships in the Red Sea. This development has heightened risk aversion in the markets, leading to increased demand for the US Dollar. The US Dollar Index is trading higher, hovering around the 103.40 mark. The recovery in US Treasury yields is further bolstering the Greenback, coupled with assertive statements from Federal Reserve (Fed) officials. US Federal Reserve Governor Christopher Waller emphasized that despite positive developments in the inflation outlook, the central bank is in no rush to announce plans for interest rate cuts. Additionally, Atlanta Federal Reserve President Raphael Bostic, in remarks made over the weekend, cautioned against premature interest rate cuts, warning of potential fluctuations in inflation.

Recent Swiss economic data, which includes a slight uptick in consumer prices in December and improved Swiss consumer demand in November, as indicated by Real Retail Sales figures, could potentially dissuade the Swiss National Bank from considering interest rate reductions in their upcoming monetary policy meeting. In the absence of high-impact data on the Swiss economic calendar, market participants are closely following developments at the 54th World Economic Forum Annual Meeting in Davos, where more than 28,000 global leaders are in attendance. Discussions and insights shared at this event can significantly influence market sentiments. On the US economic front, traders are eagerly awaiting the release of US Retail Sales data for December, scheduled for Wednesday.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

During the Davos Economic Forum, ECB President Christine Lagarde expressed her confidence in the eventual return of inflation to the 2.0% target. She emphasized that the ECB is not declaring victory over inflation and stressed that there is still time and effort required to reach their target.

During a conversation held on the sidelines of the World Economic Forum Annual Meeting in Davos, European Central Bank President Christine Lagarde expressed her optimism regarding the attainment of the 2.0% inflation target. She acknowledged that inflation is currently not at the desired level but emphasized that progress is being made towards the 2.0% goal, though it has not been achieved yet. Additionally, she cautioned against excessive optimism in the financial markets, noting that it can hinder the central bank’s efforts in combating inflation.

EURAUD Analysis:

EURAUD is moving in the Descending channel and the market has reached the lower high area of the channel

According to the China National Bureau of Statistics, China’s economy is expected to encounter greater challenges in 2024, with the property sector having additional room for recovery. The year 2023 proved to be a more challenging period for China as it sought to recover from the impacts of the COVID-19 pandemic.

The National Bureau of Statistics conducted a press conference on Wednesday following the release of significant economic data for December in China. They highlighted that final consumption played a substantial role, contributing to 82.5% of the GDP growth in 2023. While acknowledging the hard-fought nature of China’s economic growth in 2023, the bureau also pointed out that the country is confronting a complex external environment and a deficiency in demand for 2024.

Capital formation accounted for 28.9% of the GDP growth in 2023, while net exports had a negative impact of -11.4% on the GDP growth for the same year. In the fourth quarter (Q4), final consumption continued to be a dominant factor, contributing to 80% of the GDP growth, while capital formation played a role in 23.1% of the Q4 GDP growth. Net exports had a -3.1% impact on the Q4 GDP growth.

The bureau expressed concern about low consumer prices, which reflect inadequate effective demand, but they anticipate a modest rise in consumer prices in 2024. They emphasized that China’s economy is currently at a crucial stage of recovery, with some positive changes in the property market. Furthermore, they believe there is still substantial room for development in China’s property sector.

Despite acknowledging challenges, the bureau stated that China’s economy is poised to benefit from more favorable conditions than difficulties in 2024. They expect China’s economy to continue its path of recovery throughout the year.

EURNZD Analysis:

EURNZD has broken the Box pattern in Upside

This week, the financial markets are eagerly anticipating a speech from RBNZ Policy Maker Paul Conway. The presence of higher inflation within the New Zealand economy has led the Reserve Bank of New Zealand to opt for maintaining interest rates at a stable level, dispelling expectations of a rate cut.

The New Zealand Dollar has undergone a sharp sell-off, driven by a rush of investors towards safe-haven assets amid escalating crises in the Middle East and uncertainties surrounding the Federal Reserve’s initiation of a rate-cut cycle. The S&P500 is anticipated to open on a bearish note, influenced by negative indications from overnight futures. The overall market sentiment leans bearish, primarily due to the threats issued by Iran-backed Houthi rebels, vowing retaliation for US military airstrikes in Yemen.

Concurrently, the US Dollar Index maintains its strength, hovering near a fresh weekly high around 103.20. Market participants are reevaluating strong positions that had previously supported expectations of a Fed rate cut in March. Investors have adopted a cautious stance regarding the likelihood of the Fed implementing rate cuts in March, as December’s inflation data has proven more resilient than initially forecasted.

Furthermore, Atlanta Fed President Raphael Bostic has asserted that it is premature to discuss rate cuts, emphasizing that progress in inflation’s return to the 2% target has slowed. Investors are eagerly awaiting the release of US Retail Sales data for December, scheduled for Wednesday, with expectations of a 0.4% growth compared to a 0.3% increase in November.

Turning to the New Zealand Dollar, investors are keenly anticipating a speech by Reserve Bank of New Zealand policymaker Paul Conway. In this speech, Conway is expected to push back against market expectations that suggest an imminent rate cut. The inflation rate in the New Zealand economy currently exceeds the threshold desired by RBNZ policymakers, providing them with justification to maintain a restrictive stance.

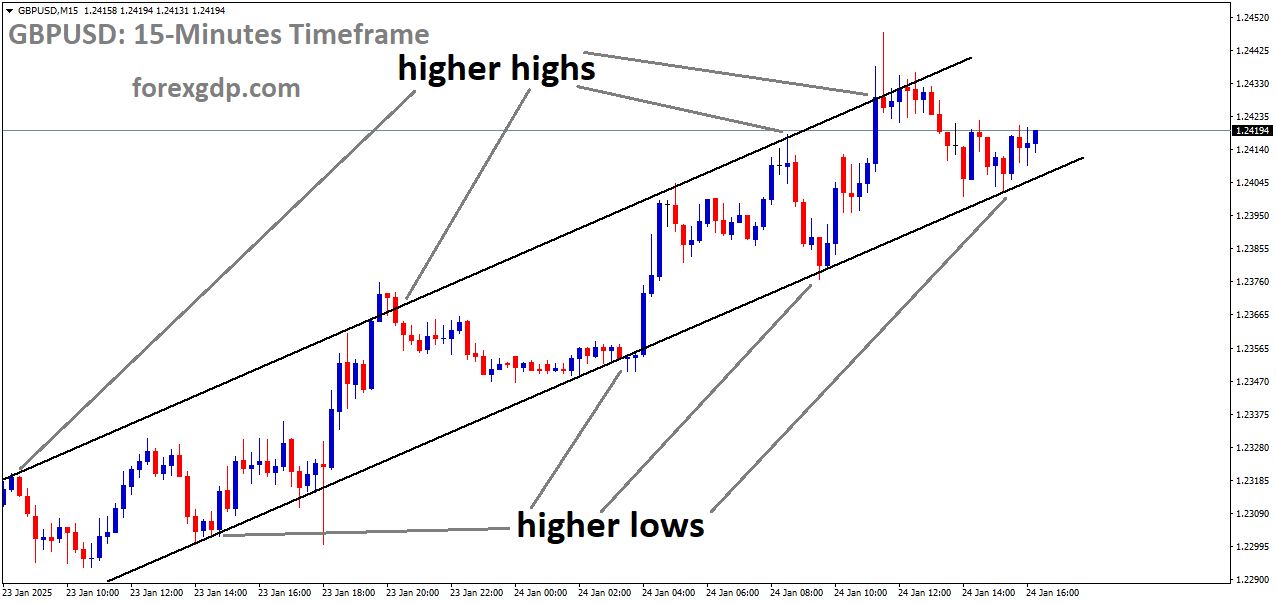

GBPUSD Analysis:

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The UK Consumer Price Index data for December showed a rise to 4.0%, up from the 3.9% recorded in November. This data prompted a more hawkish stance from the Bank of England.

According to data released by the Office for National Statistics on Wednesday, the United Kingdom’s Consumer Price Index experienced an annual increase of 4.0% in December, surpassing the 3.9% rise observed in November.

This figure exceeded the market consensus, which had anticipated a growth rate of 3.8%. Furthermore, the Core CPI, which excludes the volatile categories of food and energy, maintained its year-on-year growth rate at 5.1% in December, the same as in November, but slightly below the estimated 4.9%. Additionally, the UK Consumer Price Index showed a month-on-month rebound of 0.4% in December, surpassing expectations of a 0.2% increase and reversing the -0.2% reading observed in November.

AUDJPY Analysis:

AUDJPY is moving in an Ascending triangle pattern and the market has reached the higher low area of the pattern

The Bank of Japan maintained its negative interest rates policy in response to the earthquake in central Japan, subdued inflation data, and limited wage increases. As a result, the Japanese yen began to depreciate against other currencies in the market.

The Japanese Yen has continued its depreciation against the US Dollar for the third consecutive day, reaching its lowest level since early December as the European session begins on Wednesday. Several factors are contributing to this decline. First, there are expectations that the Bank of Japan will postpone its plan to shift away from its ultra-dovish monetary policy due to a devastating earthquake in central Japan, declining inflation rates in Tokyo, and weak wage data, all of which undermine the strength of the JPY.

And Japan’s National Core CPI release on Friday, which will influence the JPY’s direction before the upcoming Bank of Japan decision next Tuesday. Given the current fundamentals, the path of least resistance for the currency pair appears to be upward, supporting the continuation of the uptrend observed since the beginning of the month.

The Japanese Yen continues to be weighed down by the diminishing likelihood of the Bank of Japan ending its negative rate policy due to domestic factors, including the recent earthquake, declining inflation, and weak wage data. Despite the general weakness in global equity markets and ongoing geopolitical tensions, the JPY has failed to find relief.

In the latest development, the US conducted another airstrike targeting a Houthi missile facility in Yemen, citing a threat to merchant vessels and US Navy ships.

AUDCAD Analysis:

AUDCAD has broken the Box pattern in downside

Canada has ramped up production of the Trans Mountain pipelines, which are vital for both exporting and refining purposes. Canada holds the distinction of being the largest oil exporter to the United States. However, the Canadian Dollar has experienced a modest, a trend attributed to a combination of factors, including the Red Sea conflicts on one side and inventory levels on the other.

The unfolding geopolitical tensions in the Middle East have prompted investors to adopt a more cautious approach, resulting in the bolstering of the US Dollar against various major currencies, including the Canadian Dollar. The decrease in crude oil prices is placing downward pressure on the Canadian Dollar. Canada, as the largest oil exporter to the United States, is particularly sensitive to fluctuations in oil prices.

The West Texas Intermediate crude oil is currently trading at approximately $72.10 per barrel after recent declines. This downward pressure on WTI prices can be attributed, in part, to a modest increase in net output from US crude oil production facilities during the week. Additionally, the completion and expansion of the Trans Mountain pipeline in Canada play a significant role in facilitating the transportation of crude oil from production areas to refineries and export terminals. Canada’s increased crude oil production in November has positioned the country as the fourth-largest global producer of barrels.

AUDCHF Analysis:

AUDCHF has broken the Box pattern in downside

The Australian Dollar has experienced a significant drop against the US Dollar following a slowdown in consumer confidence during January, coupled with a recent decline in inflation data. These factors have raised expectations that the Reserve Bank of Australia will keep interest rates stable.

And the Australia consumer sentiment for January has deteriorated, with higher mortgage rates and the cost of living being cited as contributing factors, according to reports. It is worth noting that the Reserve Bank of Australia (RBA) has raised rates to 4.35%, marking a 12-year high, and has indicated the possibility of further tightening if inflationary figures remain elevated. Nevertheless, a decline in the latest monthly inflation report could dissuade the RBA from proceeding with rate increases.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/