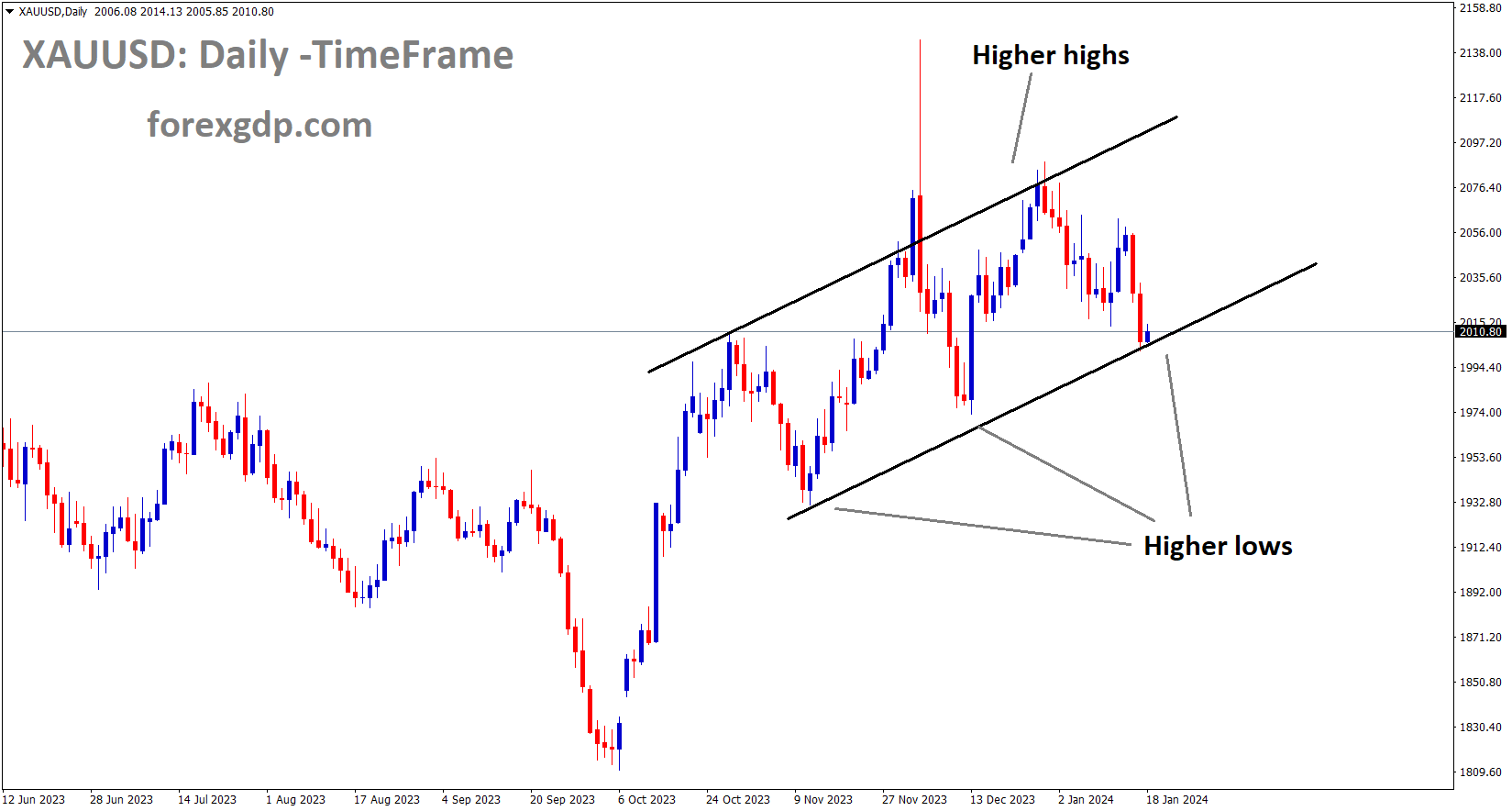

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices have dipped as geopolitical tensions escalated in the Red Sea region. On the other hand, the US Dollar strengthened following hints from central bank speakers at the Federal Reserve that interest rates would be kept steady until inflation reaches the target of 2%.

The decline in the price of gold is being driven by robust economic data in the United States, which has tempered expectations of an imminent interest rate cut. Currently, the gold price stands at $2,007, showing a slight 0.07% increase for the day. Meanwhile, the US Dollar Index, which measures the USD’s strength against most major trading partners, has surged to a new 2024 high, nearing 103.70. US Treasury yields have also inched higher across the yield curve, with the 10-year yield at 4.10%. Investors are uncertain about the timeline for potential interest rate discussions at the Federal Reserve (Fed). According to the CME Fed watch tool, traders now see a 57% chance of a 25 basis points interest rate cut in March, down from 70% earlier in the week.

Moreover, the release of better-than-expected US Retail Sales data has pushed back expectations for rate cuts. December’s Retail Sales showed a 0.6% month-on-month increase, surpassing the previous 0.3% figure. The Retail Sales Control Group also saw growth, with a 0.8% increase in December compared to the previous reading of 0.5%. Additionally, concerns about deteriorating Chinese economic data are impacting the gold price, as China is a significant consumer of gold. China’s Gross Domestic Product expanded by 5.2% last year, falling slightly short of the expected 5.3%. Industrial production rose by 6.8% year-on-year in December, while Retail Sales slowed to a 7.4% year-on-year increase in December from 10.1% the previous month.

Traders will closely monitor several US economic indicators scheduled for release on Thursday, including Housing Starts, Building Permits, weekly Initial Claims, and the Philly Fed Manufacturing Index. These data points may provide clearer direction for the gold price. And Gita Gopinath, the Deputy Managing Director of the International Monetary Fund, the relatively elevated services inflation in both the United States and the Euro area is causing a more gradual decline in the overall inflation rate, as opposed to a sharp decrease. Additionally, the tight labor market conditions are contributing to inflation maintaining a faster pace. As a result, it is anticipated that central banks will primarily consider rate cuts in the latter half of 2024, rather than during the first half.

During a recent interview with the Financial Times, Gita Gopinath, the First Deputy Managing Director of the International Monetary Fund, shared her perspective regarding inflation and the anticipated interest rate cuts by central banks. Gopinath emphasized the importance of central banks exercising caution when considering interest rate reductions for the current year. She pointed out that the inflation rate is expected to decrease less rapidly than in the previous year, primarily due to the presence of tight labor markets and elevated services inflation not only in the United States and the Euro area but also in other regions. Based on the available data, Gopinath suggested that rate cuts are more likely to occur in the second half of the year rather than the first half.

CRUDE OIL Analysis:

Crude oil price is moving in the Descending channel and the market has reached the lower high area of the channel

US Federal Reserve Governor Christopher Waller emphasized that any potential rate cuts would depend solely on inflation reaching the target level. As long as central banks keep rates steady, this approach will be maintained. Following this announcement, the US Dollar strengthened against its counterparts in the currency market.

US Treasury yields along the yield curve surged to their highest levels in five weeks. The 10-year note reached 4.129%, while the 30-year bond spiked as high as 4.344%. This rise in yields was driven by investors adhering to the US Federal Reserve’s “higher for longer” stance. Consequently, it contributed to a strengthening of the US Dollar, which, although it retraced some of its gains, managed to hold onto a marginal 0.05% increase, reaching a level of 103.38.

During the US session, traders observed the release of US Retail Sales data for December, which displayed a 0.6% increase, surpassing both the expected 0.4% rise and the November figures. Additionally, the US Federal Reserve reported a modest improvement in Industrial Production, which grew by 0.1%. This positive shift followed a period of contraction and stagnation in October and November of the previous year.

Furthermore, earlier data released during the European session revealed that UK inflation exceeded expectations, leading to an upsurge in global bond yields. At the beginning of the week, investors were anticipating the possibility of 175 basis points of rate cuts by the Fed in 2024. However, as the session progressed, they adjusted their expectations and now anticipate 145 basis points of monetary easing, indicating a reduction of one rate cut.

Federal Reserve Governor Christopher Waller’s remarks on Tuesday also influenced market sentiment. Waller emphasized that the Fed is in no rush to implement monetary policy easing, as inflation is “within striking distance” of their target. While he expressed openness to the idea of lowering interest rates, Waller cautioned that any such policy changes should be approached with careful calibration and not rushed. He stressed the importance of waiting until the risks of inflation resurgence have significantly diminished.

The US 10-year Treasury note saw a four-basis-point increase, reaching 4.106%, while the 30-year bond climbed five basis points to 4.344%, before settling at 4.323%. Meanwhile, the divergence in the US 10s-2s yield curve paused, as the 2-year Treasury note rose by 13 basis points due to expectations that the Fed would remain hesitant to ease policy as the markets had initially anticipated.

Looking ahead, the US economic calendar will feature US Initial Jobless Claims, and there will be additional speeches by Fed officials on Thursday. Friday will bring the University of Michigan Consumer Sentiment report.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

The US Dollar initially strengthened against the Swiss Franc in response to anticipated rate cuts from the Federal Reserve. However, this gain was reversed following last week’s release of US inflation data, which exceeded expectations. Today, investors are eagerly awaiting a speech from Thomas Jordan, the Chairman of the Swiss National Bank.

The US Dollar is gaining support from investor sentiment as expectations for the Federal Reserve’s initial rate cut in March have diminished. This shift in expectations has been reinforced by robust US Retail Sales data released on Wednesday. The probability of a rate cut has notably decreased to 57%, marking a significant decline from its previous level of over 70%. The December data for US Retail Sales shows a month-over-month growth of 0.6%, surpassing market expectations of 0.4% and exceeding the previous figure of 0.3%. Additionally, the Retail Sales Control Group has shown improvement, rising to 0.8% compared to the previous reading of 0.5%. Market participants will likely closely monitor US housing data scheduled for release on Thursday.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc is facing downward pressure in anticipation of Swiss National Bank Chairman Thomas Jordan’s speech at the World Economic Forum in Davos on Thursday. In their most recent policy update in December, the Swiss National Bank (SNB) affirmed their commitment to adjusting monetary policy as necessary to maintain inflation within a range consistent with price stability over the medium term. The SNB’s recent policy stance has been relatively neutral, devoid of any significant surprises.

Recent economic indicators, such as a slight uptick in Swiss consumer prices in December and improved consumer demand in November, could influence the SNB’s decision-making in the upcoming meeting. These moderate figures might discourage the SNB from making alterations to its monetary policy. Furthermore, the SNB has signaled its readiness to intervene in the foreign exchange market, if required, to support the Swiss Franc.

GBPUSD Analysis:

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The latest UK Consumer Price Index (CPI) figures for December revealed a rise to 4.0%, up from the 3.9% reported in November. In light of this elevated inflation level, the Bank of England is expected to uphold its hawkish stance on interest rates during the first half of 2024.

The UK Office for National Statistics released data on Wednesday indicating that the Consumer Price Index increased for the first time in 10 months, rising from 3.9% in the previous month to 4.0% in December. Additionally, the core CPI, which excludes volatile prices of food, energy, alcohol, and tobacco, remained steady at 5.1% in December, defying expectations of a decline to 4.9%. These developments had an immediate impact on the markets, with the probability of the Bank of England initiating rate cuts by mid-May decreasing from just over 80% late on Tuesday to approximately 60%. This change in sentiment is providing support for the British Pound.

Conversely, the US Dollar is experiencing a slight decline, potentially driven by profit-taking following its recent rally to its highest level since December 13. This trend is contributing to the strength of the GBP/USD pair. Additionally, the release of upbeat US Retail Sales figures on Wednesday has led investors to reconsider their expectations for a March interest rate cut by the Federal Reserve (Fed), which is keeping US Treasury bond yields elevated and preventing a significant depreciation of the USD. As a result, traders are refraining from making aggressive bullish bets on the currency pair.

Furthermore, ongoing speculations regarding the Fed’s intention to maintain higher interest rates for a more extended period, along with concerns about geopolitical risks and China’s economic challenges, are dampening overall market sentiment. This sentiment is evident in the generally weaker performance of equity markets, which could further bolster the US Dollar’s reputation as a safe-haven currency compared to the British Pound. Therefore, it is advisable to await confirmation of strong sustained buying before concluding that the GBP/USD pair has established a short-term bottom and considering further appreciation, especially in the absence of significant market-moving economic releases from the UK.

Later in the early North American session, traders will monitor the US economic calendar, which includes regular updates such as Weekly Initial Jobless Claims, the Philly Fed Manufacturing Index, Building Permits, and Housing Starts. Additionally, a scheduled speech by Atlanta Fed President Raphael Bostic and fluctuations in US bond yields will influence USD price dynamics, potentially impacting the GBPUSD pair.

GBPJPY Analysis:

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

The Japanese Yen experienced a decline following the Bank of Japan’s announcement that it would continue its accommodative monetary policy until inflation reaches the 2% target level. This week, Japan is set to release Machinery Orders data, which is anticipated to show a decrease in November, dropping to -0.80% from the previous -0.70% recorded in October.

The British Pound gained strength against the struggling Japanese Yen (JPY) following a UK Consumer Price Index inflation report that exceeded expectations. On Wednesday, the UK CPI for December showed a month-on-month (MoM) increase of 0.4%, doubling the median market forecast of 0.2% and reversing the previous month’s decline of -0.2%. With inflation proving more resilient than anticipated, the likelihood of the Bank of England initiating a series of rate cuts is diminishing, which in turn led to a decline in risk assets and a broad strengthening of the GBP due to repatriation flows. Additionally, the UK Retail Price Index for December also rose by 0.5%, surpassing the forecast of 0.4% and reversing the previous month’s -0.1% reading, further disappointing rate-hungry investors.

Meanwhile, the Bank of Japan remains firmly committed to maintaining a highly accommodative monetary policy, as policymakers at the Japanese central bank are concerned about the possibility of future inflation falling below the BoJ’s 2% target. Looking ahead, Japanese Machinery Orders data for November is anticipated early in Thursday’s Asian market session. MoM Machinery Orders are expected to decline by 0.8% compared to the 0.7% growth observed in October. The year-on-year (YoY) Machinery Orders through November are expected to recover from the previous period’s -2.2% to 0.2%, as recent declines are factored into the data series. GBP traders will have another opportunity to react to economic data on Friday when UK Retail Sales figures for December are released. Market forecasts suggest a MoM decline of -0.5% (compared to the previous 1.3%) and a YoY increase of 1.1% (compared to the previous 0.1%) for the year ending in December.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

BostJan Vastle, a member of the CB Governing Council, has stated that the ECB will refrain from implementing rate cuts until inflation returns to the targeted level of 2%. Given that current inflation in the Euro area remains elevated, it is unlikely that rate cuts will be considered in the foreseeable future.

The ongoing geopolitical tension in the Red Sea is currently benefiting safe-haven assets such as the Japanese Yen, which is putting pressure on the EURJPY cross. Nonetheless, the potential downside for EURJPY may be limited as the market expects the Bank of Japan to maintain its ultra-dovish stance. Currently, the cross is trading around 161.20, showing a minor 0.03% decline for the day.

Bostjan Vasle, a member of the European Central Bank (ECB) Governing Council, recently commented that it is premature to anticipate the first rate cuts at the beginning of the second quarter. He added that inflation in the Euro area remains relatively high and must return to the 2% target before any changes are made to the central bank’s monetary policy.

Conversely, the Japanese Yen’s strength has been tempered by investor expectations that the Bank of Japan will maintain its ultra-dovish stance at its upcoming January policy meeting. Eiji Maeda, a former executive at the Japanese central bank, mentioned on Wednesday that the BoJ might consider ending negative interest rates in April, but it is likely to proceed cautiously in normalizing its ultra-loose monetary policy, in contrast to the more aggressive approach taken by the ECB.

Moreover, the escalating tension in the Middle East could limit the downside for the Japanese Yen. Late on Wednesday, Houthi rebels from Yemen targeted a US-owned cargo ship using a kamikaze drone in the Red Sea, following the Biden administration’s decision to re-designate the Houthis as global terrorists.

AUDCAD Analysis:

AUDCAD has broken the Box pattern in downside

The Canadian Dollar experienced only a modest uptick in value following the OPEC committee’s projection of increased oil demand for the years 2024 and 2025. This appreciation occurred despite the Canadian Raw Material Index contracting for the second consecutive month, marking its lowest point since June of the preceding year.

In December, Canada’s Raw Material Price Index continued to contract for the second consecutive month, maintaining a significant deflationary trend in materials prices not seen since June of the previous year. According to the report released on Wednesday, the index displayed a consistent contraction of 4.9%, matching the previous month’s figure. Additionally, the Industrial Product Price (MoM) experienced a larger-than-expected decline of 1.5%, surpassing the anticipated decrease of 0.7% and the previous month’s fall of 0.3%.

Meanwhile, the US Dollar Index saw its winning streak come to an end due to disappointing US Treasury yields. The DXY is currently trading lower, near 103.30, with the 2-year and 10-year yields on US bond coupons standing at 4.33% and 4.08%, respectively, at the time of this press release.

In the United States, Retail Sales (Month-over-Month) for December exhibited growth of 0.6%, exceeding market expectations of 0.4% and surpassing the previous figure of 0.3%. The Retail Sales Control Group also displayed improvement, reaching 0.8% from the previous reading of 0.5%. Furthermore, Retail Sales excluding Autos (Month-over-Month), which excludes the motor vehicles and parts sector, increased by 0.4%, surpassing market expectations of a steady figure at 0.2%. Traders are likely to closely monitor US housing data set to be released on Thursday. In Canada, Retail Sales data will be eagerly awaited and is scheduled for release on Friday.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

In December, the Australian unemployment rate remained steady at 3.9%, matching the figure reported in the previous month. However, the employment change figure was significantly negative, with a decline of 65.1K jobs, in contrast to the forecast of a gain of 17.6K jobs and the 61.5K jobs added in the previous month.

In December, the Australian unemployment rate held steady at 3.9%, mirroring the previous month’s figure. However, there was a notable negative shift in employment change, showing a decrease of 65.1K jobs. This contrasted sharply with the anticipated increase of 17.6K jobs and the 61.5K jobs added in the previous month. Official data from the Australian Bureau of Statistics, released on Thursday, confirmed that Australia’s unemployment rate remained at 3.9% in December, in line with both expectations and the previous month’s figure. Additionally, the Australian Employment Change for the same period registered a substantial decline of -65.1K, diverging significantly from the consensus forecast of a 17.6K job gain and the 61.5K jobs added in November.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

In December, the New Zealand Dollar Food Price Index showed a slight decrease of -0.10%, which was an improvement compared to the -0.20% decline observed in November. It’s worth noting that food prices have risen in comparison to the levels recorded last year.

According to StatsNZ, New Zealand’s Food Price Index (FPI) recorded its lowest annual increase in food prices since December 2021. While food prices generally rose across the five primary categories for the year ending in December, the month of December itself marked the fourth consecutive month of month-on-month declines in food inflation. In December, monthly food prices declined by 0.1%, indicating a slower pace of decrease compared to November’s 0.2% downturn, although still reflecting a downward trend.

Despite experiencing headline FPI declines in 5 out of 12 months, food prices remain notably higher compared to the same period last year. Groceries and non-alcoholic beverages increased by 5.4% and 5.5%, respectively, over the course of the year, while restaurants and ready-to-eat foods showed the most significant gains, with a 7.1% increase. The overall price gains year-on-year for fruits and vegetables were relatively modest, at 1.5%, helping to prevent a more significant overall increase in food prices.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/