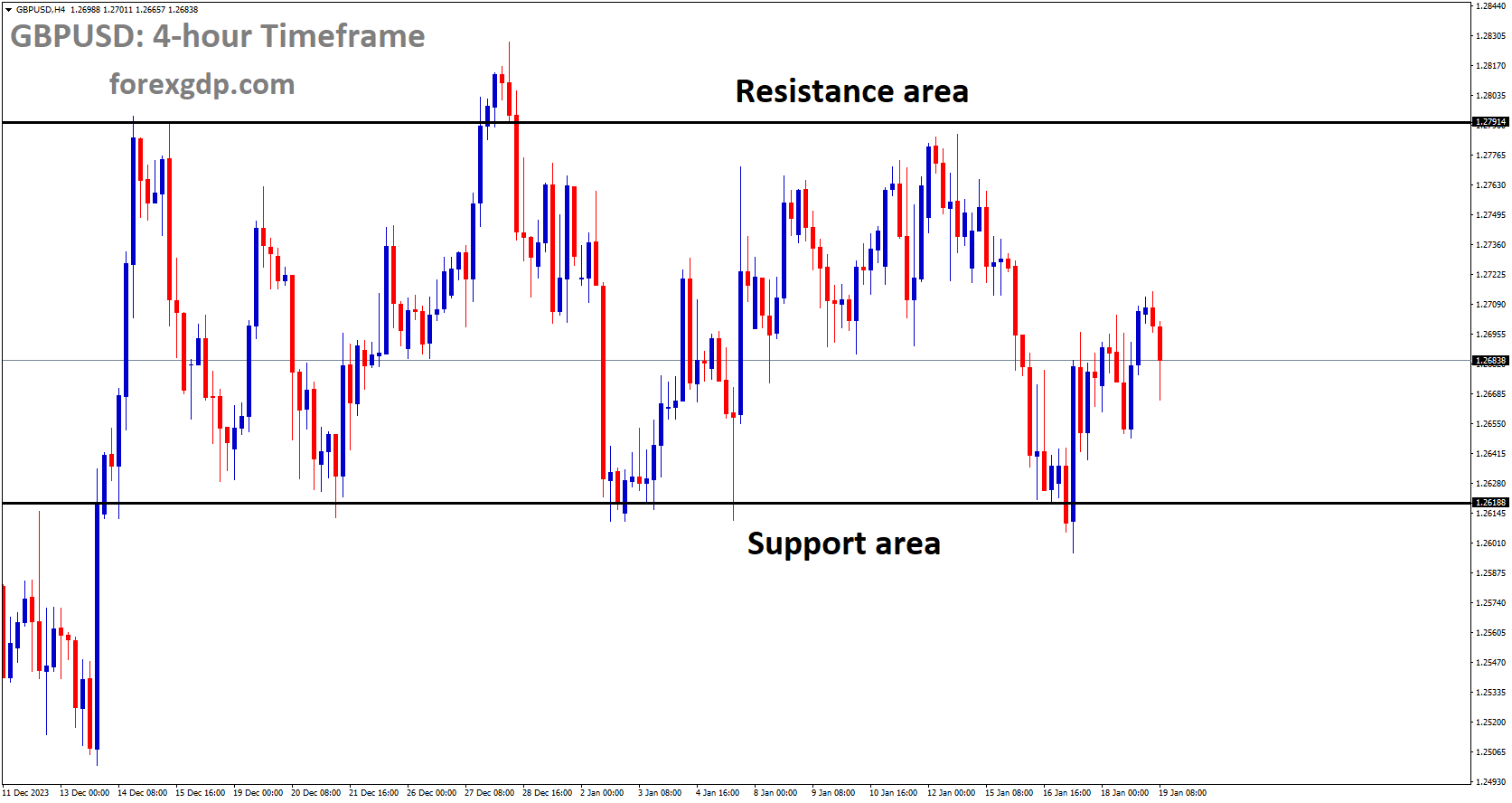

GBPUSD Analysis:

GBPUSD is moving in box pattern and market has rebounded from the support area of the pattern

The Pound Sterling took a sharp nosedive following the release of discouraging Retail Sales data for December by the United Kingdom’s Office of National Statistics (ONS). Household spending in the UK contracted significantly as individuals grappled with the heavy burden of higher interest rates and rising consumer price inflation, further intensifying the ongoing cost-of-living crisis. Despite expectations that a notable decline in high street sales would alleviate pressure on the persistently high inflation outlook, it ultimately failed to have a substantial impact. While a substantial contraction in Retail Sales could have increased the likelihood of an early rate cut by the Bank of England, policymakers are expected to maintain a cautious monetary policy stance until they are confident that underlying inflation will return to the 2% target in a sustainable and timely manner.

Looking ahead, market observers will shift their attention to the preliminary S&P Global PMI data for January, which is scheduled for release in the upcoming week. The UK Manufacturing PMI has been in contraction for over a year and is expected to continue facing challenges. The Pound Sterling experienced a sharp sell-off as the ONS reported a significant 3.3% decline in Retail Sales excluding fuel prices, far surpassing the anticipated 0.6% decrease. This follows a 1.5% expansion in November. Surprisingly, on an annual basis, consumer spending contracted by 2.1%, a stark contrast to the projected 1.3% increase. Monthly retail store sales saw a notable 3.2% contraction after a 1.4% expansion in November, defying expectations of a more modest 0.5% decline. Annually, consumer spending unexpectedly shrank by 2.4%, while investors had foreseen a growth of 1.1%. In November, there was a slight increase of 0.2%. The downbeat Retail Sales data is expected to provide some relief in addressing the persistent inflation concerns.

This development is anticipated to offer temporary respite to Bank of England policymakers, who had been increasingly concerned about the upside risks to price pressures following the release of stubbornly high inflation data for December. Nevertheless, the looming threat of a deepening recession due to a fragile economic outlook will keep BoE policymakers cautious. They face a delicate balance between potentially adopting a dovish stance to protect the economy from a recession and maintaining a restrictive monetary policy to bring inflation down to the 2% target. Meanwhile, investment banking firm Goldman Sachs is forecasting that the BoE will commence interest rate reductions starting in August this year. The firm now expects interest rates to be lowered by 75 basis points (bps) by the end of 2024. As of now, the market sentiment is relatively quiet, with a lack of prominent US economic indicators. Market participants will also focus on a speech by San Francisco Fed President Mary Daly. It is anticipated that Fed Daly will provide a hawkish perspective on interest rates, emphasizing that policymakers will only consider rate cuts once they are convinced that inflation will return to the 2% target in a sustainable manner. On Thursday, Federal Reserve Bank of Atlanta President Raphael Bostic cautioned against premature rate cuts, suggesting that they could exacerbate inflationary pressures and undermine the efforts made thus far to curb higher inflation.

GOLD Analysis:

XAUUSD is moving in box pattern and market has fallen from the resistance area of the pattern

Geopolitical tensions in the Middle East escalated further as Pakistan conducted retaliatory airstrikes inside Iran on Thursday. This development adds to the ongoing US-Houthi clashes in the Red Sea. These geopolitical concerns, combined with apprehensions about China’s sustained economic weakness, are significant factors supporting the safe-haven precious metal, gold. Concurrently, the US Dollar continues its sideways consolidation below a one-month high reached on Wednesday, providing additional backing for gold prices. However, the diminishing likelihood of a more aggressive policy easing by the Federal Reserve continues to drive US Treasury bond yields higher, thereby bolstering the Greenback. Furthermore, the generally positive sentiment in equity markets may limit the upside potential for XAUUSD.

US-led forces remain engaged in clashes with the Iran-backed Houthi group in the Red Sea, contributing to the support for gold prices amid a relatively stable US Dollar. Houthi rebels in Yemen launched two anti-ship ballistic missiles at a US-owned, Greek-operated tanker ship on Thursday, prompting the US to respond with its fifth strike against Houthi targets. Simultaneously, Pakistan carried out a series of military strikes against terrorist hideouts in Iran’s Sistan-Baluchistan province, while Iran commenced planned air defense exercises from its Chabahar port near Pakistan.

The USD is consolidating below its highest level since December 13, reached earlier this week. However, the reduced expectations for a rate cut by the Federal Reserve in March continue to provide tailwinds. Resilient US economic data released this week has indicated a healthy economy, giving the central bank room to maintain higher interest rates for a longer period. Following the upbeat US Retail Sales figures on Wednesday, Thursday’s data revealed that Initial Jobless Claims fell to their lowest level since September 2022. Market reactions to these strong labor market indicators have resulted in the likelihood of a rate cut at the March FOMC meeting being reduced to just over 50%, down from 75% a week ago. The yield on the benchmark 10-year US government bond reached its highest level since mid-December, favoring the USD bulls and potentially limiting gains for gold. Traders are now turning their attention to US economic data, including the Preliminary Michigan Consumer Sentiment and Inflation Expectations, along with Existing Home Sales, in search of short-term trading opportunities.

SILVER Analysis:

XAGUSD is moving in box pattern and market has reached support area of the pattern.

The most recent data reveals that the US weekly Initial Jobless Claims have reached their lowest point in almost a year and a half. This suggests a tightening labor market, which in turn reduces the likelihood of a rate cut by the Federal Reserve (Fed) in March. The CME Group’s FedWatch Tool currently indicates a probability of a March Fed rate cut of less than 60%, compared to the approximately 75% chance perceived at the beginning of the week.

Strong US economic data and hawkish statements from Fed officials have propelled US Treasury bond yields to fresh multi-week highs, further pushing back against market expectations of an early March rate cut. Atlanta Fed President Raphael Bostic emphasized on Thursday that while rate reductions may be on the horizon in the third quarter, it’s crucial not to rush into a rate cut prematurely, as doing so could risk reigniting inflationary pressures. At the time of this writing, the US Dollar Index has dipped by 0.09% to 103.45 for the day, while benchmark 10-year US Treasury bond yields have climbed by 0.75%, reaching five-week highs near 4.18%.

USDCAD Analysis:

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

The US Dollar remains on an upward trajectory, driven by strong economic data from the United States and higher US Treasury yields. The US Dollar Index is currently trading around 103.40, supported by 2-year and 10-year US bond yields at 4.35% and 4.15%, respectively. In December, US Housing Starts surpassed expectations, reaching 1.46 million compared to the anticipated 1.426 million. Building Permits also showed growth, rising to 1.495 million, exceeding the market consensus of 1.48 million. Additionally, Initial Jobless Claims for the week ending January 12 decreased to 187,000 from the previous reading of 203,000. On the other hand, the Canadian Dollar received a boost from higher crude oil prices, as Canada is the largest oil exporter to the United States. West Texas Intermediate crude oil prices are struggling to sustain their gains for the third consecutive day, currently hovering around $73.90 per barrel. The increase in crude oil prices is attributed to a decline in crude oil stockpiles.

The US Energy Information Administration reported that for the week ending January 12, US Crude Oil Stocks decreased by 2.492 million barrels, contrary to the expected decline of 0.323 million barrels and a reversal from the previous stockpile increase of 1.338 million barrels. On Friday, economic data to watch includes Canada’s Retail Sales for November, offering insights into consumer spending trends in the country. Concurrently, the United States will release the Michigan Consumer Sentiment Index for January, reflecting consumer confidence in the economic outlook. In addition to economic indicators, market participants will be attentive to speeches from central bank officials, which can provide further context and insights into the direction of monetary policies.

USDJPY Analysis:

USDJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

Data released earlier today confirmed that Japan’s inflation eased as expected, reinforcing market expectations that the Bank of Japan will delay its plan to move away from its ultra-dovish policy stance. This, combined with a generally positive sentiment in equity markets, is eroding the Japanese Yen’s status as a relative safe haven. Additionally, the decreasing likelihood of a more aggressive policy easing by the Federal Reserve (Fed) continues to drive US Treasury bond yields higher, widening the US-Japan interest rate differential and diverting funds away from the JPY. Meanwhile, incoming US economic data indicates a resilient economy, giving the US central bank room to maintain higher interest rates for an extended period, bolstering the USD and benefiting the USDJPY pair.

Traders are now turning their attention to the US economic calendar, which includes the release of the Preliminary Michigan Consumer Sentiment and Inflation Expectations, as well as Existing Home Sales. Furthermore, speeches by influential members of the Federal Open Market Committee and developments in US bond yields will influence the dynamics of the USD. However, the spotlight remains on the highly-anticipated Bank of Japan (BoJ) monetary policy meeting scheduled for January 22-23, which will likely determine the JPY’s short-term direction.

The Japanese Yen has fallen to nearly a two-month low against the US Dollar due to the growing belief that the Bank of Japan will stick with its accommodative policy stance. According to the Statistics Bureau, the headline Consumer Price Index (CPI) eased from a year-on-year rate of 2.8% to 2.6% in December, marking its lowest level since June 2022. Japan’s core inflation rate, which excludes volatile fresh food prices, also decelerated from 2.5% in November to 2.3%, reaching its lowest point since July 2022. This situation, combined with the New Year’s Day earthquake in Japan and weak wage growth data, reinforces the expectation that the Bank of Japan will not shift away from its ultra-dovish stance. Japan’s Finance Minister, Shunichi Suzuki, mentioned that the government is closely monitoring foreign exchange developments, but this statement does little to provide relief to JPY bulls.

Investors have scaled back their expectations for an early interest rate cut by the Federal Reserve after Thursday’s data revealed that Jobless Claims had dropped to the lowest level since September 2022. The strong labor market report, along with positive US Retail Sales figures from Wednesday, indicates an enduringly robust economy and reduces the likelihood of a Fed rate cut in March. According to the CME Group’s FedWatch Tool, markets are currently pricing in a 57% chance of an interest rate cut at the March FOMC meeting, down from 75% just a week ago.

In recent geopolitical developments, Iranian-backed Houthi militants in Yemen launched two anti-ship ballistic missiles at a US-owned, Greek-operated tanker on Thursday. The risk of escalating military actions in the Middle East could support the JPY’s safe-haven status and limit substantial gains in the USDJPY pair. Traders are now awaiting fresh impetus from US economic data, including the Preliminary Michigan Consumer Sentiment and Inflation Expectations, as well as Existing Home Sales. Nevertheless, the primary focus will remain on the upcoming Bank of Japan monetary policy meeting, which will play a pivotal role in shaping short-term JPY price movements.

EURUSD Analysis:

EURUSD is moving in Ascending channel and market has reached higher low area of the channel

The forthcoming meetings of the European Central Bank and the Federal Reserve the following week have piqued the interest of economists at Commerzbank, who are analyzing what the FX market can anticipate from these gatherings. It appears that the ECB is inclined to exercise caution regarding the possibility of initiating interest rate cuts. Although it’s improbable that they will completely dismiss the notion of potential rate reductions later in the year, they will likely attempt to temper premature expectations. However, the effectiveness of their efforts remains uncertain. As there are no major data releases scheduled before the meeting, the FX market is expected to exhibit a reluctance to push the EUR lower in the lead-up to the event.

EURJPY Analysis:

EURJPY is moving in Ascending channel and market has reached higher low area of the channel

The European Central Bank’s minutes, which were disclosed on Thursday, indicate that the earliest point at which they might gauge whether inflation has been successfully managed would be in June. The central bank expressed concerns that market expectations for rate cuts as early as March had significantly loosened financial conditions, potentially jeopardizing the process of countering inflation. ECB President Christine Lagarde suggested the possibility of rate cuts at the World Economic Forum in Davos on Thursday, mentioning that interest rate reductions could be considered by the summer, though the central bank continues to prioritize data-driven decisions. Additionally, the ECB will closely monitor developments related to geopolitical tensions in the Red Sea, as these may impact goods inflation in the eurozone.

Conversely, the escalating geopolitical tensions in the Middle East may provide support for safe-haven assets like the Japanese Yen and limit the upside potential of the EURJPY currency pair. Furthermore, the upcoming Bank of Japan (BoJ) monetary policy meeting next week is a critical event that could introduce volatility to the market. The decrease in the Japanese Consumer Price Index (CPI) in December reinforces market expectations that the Bank of Japan will maintain its highly accommodative stance at the forthcoming monetary policy meeting. Early on Friday, December’s Japanese CPI was reported at a 2.6% YoY rate, compared to the previous 2.8%, while the National CPI excluding Fresh Food recorded a 2.3% YoY rate in December, down from the previous 2.5%. Looking ahead, the German Producer Price Index (PPI) for December is scheduled for release on Friday. Additionally, ECB President Lagarde is set to deliver a speech, which may provide insights into the future path of monetary policy. Next week, market attention will shift to the Bank of Japan’s interest rate decision.

EURGBP Analysis:

EURGBP is moving in box pattern and market has fallen from the resistance area of the pattern

The Pound Sterling is facing challenges due to Retail Sales data from the United Kingdom. The recent positive UK inflation data, disclosed on Wednesday, has provided some support for the British Pound. This has also exerted downward pressure on the EUR/GBP exchange rate. Simultaneously, traders have scaled back their expectations for potential rate cuts by the Bank of England. Previously, the market had priced in an 80% likelihood of a 25 basis points rate cut by the BoE in May earlier this week. However, these odds have now been adjusted to 50%. This shift in expectations may provide additional support to the GBP while acting as a hurdle for the EURGBP exchange rate.

Conversely, speculations regarding potential rate cuts by the European Central Bank in September have been contributing to the Euro’s weakening. Market sentiment received a boost when ECB President Christine Lagarde, speaking at the World Economic Forum in Davos, hinted that interest rate cuts could be on the table by the summer. President Lagarde emphasized the possibility of reaching the peak in the ECB’s interest rates and stressed the central bank’s reliance on economic data. She acknowledged the presence of ongoing uncertainties and indicators that have not yet firmly stabilized, adding to the nuanced approach to future monetary policy. Market participants will keep a close eye on Germany’s Producer Price Index (PPI) data, which is scheduled for release on Friday.

EURNZD Analysis:

EURNZD is moving in Ascending channel and market has rebounded from the higher low area of the channel

Christine Lagarde, who serves as the President of the European Central Bank (ECB), is scheduled to deliver a speech on Friday at 10:00 GMT during the World Economic Forum in Davos. This marks her third appearance at the WEF Annual Meeting this week, following her participation in panels discussing “How to Trust Economics” on Wednesday and “Uniting Europe’s Markets” on Thursday. On Friday, ECB President Lagarde will join a panel discussion focusing on “The Global Economic Outlook.” This debate will center on how policymakers can strike a balance between addressing the imperatives of growth and inflation by implementing appropriate tools while also ensuring sustained and long-term economic prosperity. Analysts and observers will closely examine Lagarde’s remarks for any indications regarding the growth and inflation outlook in the Euro area, as these insights could significantly influence policy decisions. However, it is unlikely that she will discuss monetary policy, as the ECB has entered a “blackout period” in preparation for next week’s policy meeting.

During an interview with Bloomberg on Wednesday, Lagarde made comments suggesting that it is probable that the ECB will consider rate cuts by the summer. These remarks led to a revision of earlier expectations for an imminent rate cut. ECB policymakers have consistently pushed back against the notion of aggressive rate cuts, emphasizing the central bank’s reliance on data in shaping its interest rate outlook. In its December meeting, the European Central Bank opted to maintain rates for the second consecutive time, revising its growth and inflation forecasts downward. The ECB’s accompanying statement indicated that the Governing Council’s future decisions would aim to maintain policy rates at suitably restrictive levels for as long as necessary.

GBPJPY Analysis:

GBPJPY is moving in box pattern and market has reached resistance area of the pattern

According to the most recent figures released by the National Statistics on Friday, UK Retail Sales experienced a notable decline of 3.2% on a month-on-month (MoM) basis in December. This decline follows a 1.4% increase in November and falls significantly below market expectations, which had anticipated a more modest 0.5% decrease. When excluding fuel sales, Retail Sales also took a hit, dropping by 3.3% MoM in December compared to the previous month’s 1.5% rise.

Looking at the annual figures, UK Retail Sales posted a year-on-year (YoY) decline of -2.4% in December, a stark contrast to the 0.2% growth observed previously. This annual performance falls well short of market projections, which had predicted a 1.1% increase. As a result of this disappointing UK data, the Pound Sterling has depreciated further in value.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/