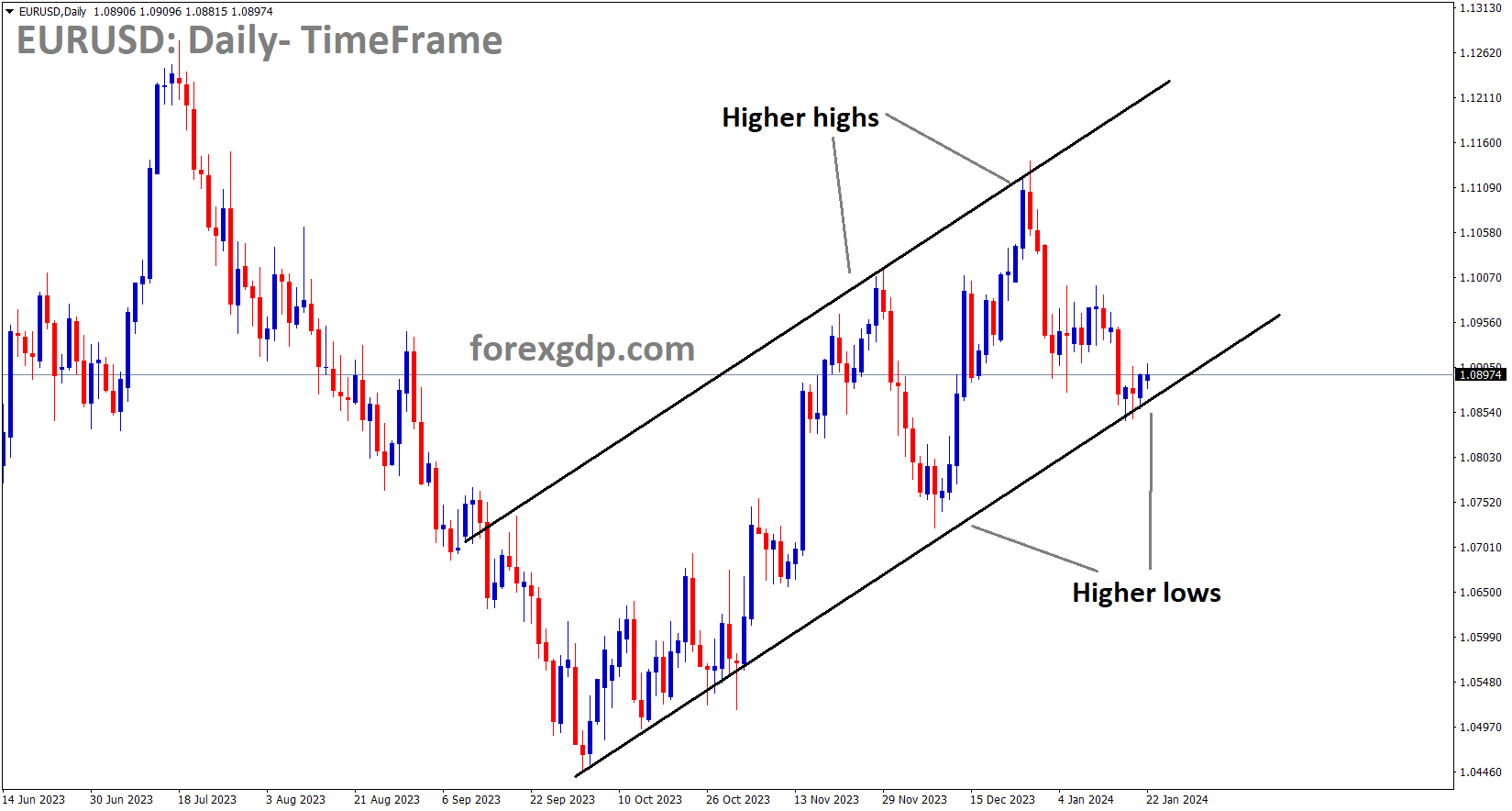

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

During last week’s Davos meeting, ECB President Lagarde refrained from discussing policy settings. However, economic data from the Eurozone indicates further contractions across various sectors, leading to expectations of a forthcoming rate cut in response to this incoming data.

The focus in the markets has been on news coming out of the World Economic Forum held in Davos, Switzerland. European Central Bank (ECB) policymakers have been actively engaging with the media to temper market expectations of potential rate cuts by the ECB. ECB President Christine Lagarde made a deliberate effort to avoid discussing monetary policy in her numerous scheduled appearances at the WEF. In fact, she concluded her third scheduled appearance in Davos without delving into the specifics of monetary policy.

ECB officials have been consistently cautioning that market anticipations of rate cuts have exceeded what the ECB is currently willing to implement. President Lagarde emphasized that overly optimistic market sentiment could hinder rather than assist in combating inflation.

While there is a possibility of an ECB rate cut by the summer, this is contingent on the absence of new inflationary pressures. On the sidelines of the Davos event, President Lagarde expressed her concern that aggressive bets on rate cuts do not align with the ECB’s stance. Additionally, the euro area witnessed a temporary respite from major headline shocks this week due to a lack of significant economic data.

The ECB has now entered a blackout period in preparation for the ECB policy meeting and rate decision scheduled for the following Thursday. Market forecasts suggest a modest improvement in the Euro area Purchasing Managers’ Index (PMI) for January, with the Composite PMI expected to rise from 47.6 to 48.1, based on figures due to be released next Wednesday.

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices have declined due to reduced expectations of Federal Reserve rate cuts, as indicated by economists. However, the demand for Gold remains robust, particularly from central bank purchases, as highlighted by ANZ Strategists.

Gold has experienced an upward trend in response to escalating geopolitical uncertainties and the anticipation of forthcoming interest rate reductions in the United States. ANZ bank strategists have assessed the future prospects of this precious metal. While the increased geopolitical risks are expected to bolster Gold’s status as a safe-haven investment, the diminishing market anticipation of imminent Federal Reserve rate cuts and a resurgence in the value of the US dollar are expected to impose constraints on its potential for further gains. The buying spree of Gold by central banks remains robust and is projected to reach 1,050 tonnes in 2023. The demand for physical Gold continues to exhibit a healthy outlook.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Mary Daly, President of the San Francisco Federal Reserve, has noted a cooling down of inflation in the United States, with goods and prices showing signs of contraction in the market. As a result, a rate cut in the near term is not anticipated. It is unlikely that the Federal Reserve will implement a rate cut in the first half of 2024.

San Francisco Federal Reserve President Mary C. Daly made headlines once again on Friday, providing further insights into remarks she had initially shared during an interview with Fox Business earlier in the day. She emphasized that the Federal Reserve’s current policy stance remains favourable, and the overall state of the US economy is also in good shape. Daly stressed the importance of exercising patience, as there is still a substantial amount of work ahead. The Federal Reserve is cautious about prematurely relaxing its policy or attempting to swiftly combat inflation.

In terms of the year 2024, the primary focus will be on carefully calibrating monetary policy. Daly emphasized that taking measures to ease policy too quickly or before reaching the 2% inflation target would have adverse consequences. She noted that both goods and services prices are steadily declining, indicating a measured approach to policy adjustments.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Thomas Jordan, the Chairman of the Swiss National Bank, has voiced his worries regarding the Swiss Franc’s strengthening against major currency pairs. He has indicated that the SNB has the ability to maintain inflation levels above 0% in the upcoming months.

The US Dollar may face downward pressure as market participants anticipate that the US Federal Reserve could implement more significant policy rate reductions in 2024 compared to other major central banks worldwide. However, hawkish comments from Federal Reserve members could potentially help mitigate the US Dollar’s losses.

San Francisco Fed President Mary Daly, in her remarks on Friday, conveyed the view that the central bank still has substantial work ahead to achieve the goal of bringing inflation back down to the 2.0% target. Additionally, Atlanta Fed President Raphael Bostic emphasized his willingness to adjust his outlook on the timing of rate cuts, highlighting the Fed’s commitment to a data-dependent approach.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc experienced selling pressure after Swiss National Bank (SNB) Chairman Thomas Jordan issued a warning last week regarding the Swiss Franc’s appreciating trend (CHF). Speaking at the World Economic Forum in Davos, Jordan expressed concerns about the potential impact of the Swiss Franc’s strength on the SNB’s ability to maintain inflation above zero in the Swiss domestic economy. The Federal Statistical Office of Switzerland reported that Producer and Import Prices declined by 1.1% in December. While this represents a decrease, it is slightly less than the previous decline of 1.3%. On a monthly basis, the data showed a decrease of 0.6%, in line with expectations. With no new data on the Swiss economic calendar for this week, traders are likely to await the release of Real Retail Sales and the ZEW Survey – Expectations next week to gain further insights into Switzerland’s economic landscape.

GBPUSD Analysis:

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The Bank of England holds concerns about the economy, with a heightened risk of recession if further rate hikes are pursued. The incoming data presents a mixed picture, and as a result, there is an expectation of rate cuts due to a cooling down of inflation in the market.

The United Kingdom’s economy is at risk of slipping into a technical recession due to vulnerable household spending and a significant sense of pessimism among business owners regarding the economic outlook. The Bank of England is expected to face difficulties in reaching a decision, as it grapples with persistently high price pressures and mounting recession concerns. This challenging situation may make it tough for policymakers to maintain a restrictive interest rate stance.

Despite investors shifting their expectations for the first rate cut by the Federal Reserve (Fed) from March to the May monetary policy meeting, the overall market sentiment remains positive. Fed policymakers have been endorsing the notion of keeping interest rates elevated for a longer duration to ensure that inflation returns to the 2% target in a timely manner. Pound Sterling has managed to sustainably rise above the critical resistance level of 1.2700, despite the unfavorable conditions facing Bank of England policymakers, particularly after a significant drop in December’s Retail Sales data.

The UK Office for National Statistics (ONS) reported an unexpected 2.4% decline in annual Retail Sales, contrary to the anticipated 1.1% growth. The ONS attributed this decline to households starting their Christmas shopping earlier than usual, with sales at food stores experiencing a particularly sharp drop. This significant decrease in consumer spending signals a deepening cost-of-living crisis, driven by higher interest rates and persistent price pressures. It has raised concerns about the UK economy entering a recession, as weak household spending may discourage firms from maintaining their current production levels.

Notably, the latest estimates from the ONS indicate a 0.1% decline in the UK’s Q3 Gross Domestic Product growth in 2023. If the economy contracts in Q4 as well, it would officially be considered a technical recession. On the inflation front, the UK economy is grappling with core inflation at 5.1% and a service price index at 6.4%, which are the Bank of England’s preferred inflation indicators when making monetary policy decisions. These stubborn price pressures in the UK economy create a complex dilemma for policymakers, forcing them to choose between a restrictive policy stance to combat higher inflation or loosening tight interest rates to shield the economy from slipping into a recession.

In the week ahead, market participants will closely monitor the preliminary S&P Global PMI for January, set to be published on Wednesday, with expectations for positive economic data. Meanwhile, the market sentiment remains optimistic despite a significant increase in the likelihood of the Federal Reserve (Fed) keeping interest rates unchanged in March, as indicated by the CME FedWatch tool, which shows a probability of over 54%. The US Dollar Index (DXY) has dipped to nearly 103.20, reflecting the positive market sentiment, while 10-year US Treasury yields have declined to approximately 4.12%.

GBPJPY Analysis:

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel

The Japanese yen has been depreciating against other currencies following the New Year’s Day earthquake incident and a significant drop in wage growth readings, which reached a 20-month low. Consequently, the Bank of Japan (BoJ) is not inclined to pursue rate hikes in their upcoming meetings, if avoidable.

The Bank of Japan is expected to maintain its negative interest rates and the Yield Curve Control policy following a two-day meeting on Tuesday. This stance, combined with positive sentiment in the equity markets, is weakening the safe-haven status of the Japanese Yen (JPY). Concerns about China’s slowing economic growth and the potential for increased geopolitical tensions in the Middle East may temper market optimism, thus limiting significant downside for the JPY ahead of the anticipated BoJ decision.

Geopolitical tensions in the Middle East and China’s economic challenges, which typically benefit the safe-haven JPY, are also influencing the USDJPY pair. The US has conducted multiple strikes against Houthi targets in response to their attacks on merchant vessels in the Red Sea. There have been approximately 140 attacks on US bases since October 17, with seven occurring in the past week, including a significant strike on Ain al-Assad base in Iraq. This attack resulted in injuries to both US and Iraqi soldiers. Iran has vowed retaliation for a strike in Damascus that killed five senior military officials, an incident attributed to Israel but not confirmed by them. Israel and Hamas forces clashed in several areas, and Israeli airstrikes resumed in the southern Gaza Strip. Israeli Prime Minister Benjamin Netanyahu indicated a departure from the two-state solution and emphasized the need for Israel to maintain security control over the territory west of Jordan.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Reserve Bank of Australia is inclined to keep interest rates at their current level, primarily in response to the recent decline in Australian consumer confidence and a decrease in employment figures over the past few months.

Australia’s dollar is experiencing a setback amid speculations of potential early interest rate cuts by the Reserve Bank of Australia. This speculation has been fueled by recent subdued figures in Aussie Consumer Confidence and Employment Change. However, the Australian Dollar (AUD) may find support from the domestic share market’s surge, mirroring a rally in the US that saw the S&P 500 and the Nasdaq reach new records on Friday. This surge was driven by expectations of future interest rate cuts by the US Federal Reserve (Fed). Additionally, optimism was boosted by Taiwan Semiconductor Manufacturing’s projection of over 20% revenue growth in 2024, positively impacting global stocks.

The People’s Bank of China has chosen to keep its Loan Prime Rate (LPR) unchanged for both the one-year and five-year terms, with rates standing at 3.45% and 4.20%, respectively. Meanwhile, the US Dollar Index continues its decline, although it could receive some support due to concerns about potential maritime trade disruptions in the Red Sea. The US and the UK are intensifying their campaign without provoking a broader conflict with Iran, leading more ships to divert away from the Suez Canal and the Red Sea. As shipping vessels assess the risks and insurance costs associated with navigating the Red Sea, opting for the alternative route around the southern tip of Africa may lead to longer delivery times, increased shipping costs, and inflation. This situation could boost risk aversion sentiments, causing traders to seek the safe-haven US Dollar and potentially exerting downward pressure on the AUDUSD pair.

San Francisco Fed President Mary Daly stated on Friday that the central bank still has significant work to do in bringing inflation back to the 2.0% target. She emphasized that considering interest-rate cuts as an imminent measure is premature. Atlanta Fed President Raphael Bostic reiterated his stance on expectations for rate cuts before the Fed enters the blackout period before the next rate meeting on January 31. Bostic emphasized his willingness to adjust his outlook on the timing of rate cuts, highlighting the Fed’s data-dependent approach.

In terms of economic data, Australia’s Consumer Inflation Expectations remained steady at 4.5% in January, while the Aussie’s seasonally adjusted Unemployment Rate held at 3.9% for December, in line with expectations. However, Australian Employment Change saw an unexpected decrease of 65.1K, contrary to the anticipated increase of 17.6K.

On the US front, the preliminary Michigan Consumer Sentiment Index for January rose to 78.8 from the previous reading of 69.7, surpassing the expected figure of 70. However, US Existing Home Sales Change declined by 1.0% in December, following a previous rise of 0.8%. In contrast, US Housing Starts exceeded expectations for December, reaching 1.46 million compared to the anticipated 1.426 million. US Building Permits also increased, rising to 1.495 million, surpassing the market consensus of 1.48 million. Additionally, US Initial Jobless Claims for the week ending on January 12 decreased to 187,000 from the previous reading of 203,000.

AUDCAD Analysis:

AUDCAD has broken the Box pattern in downside

The Canadian Dollar experienced an upward trajectory following a drop in Canadian retail sales for the month of November. This increase in the Canadian Dollar’s value in the market is further bolstered by rising crude oil prices.

Crude oil prices remained resilient as Canadian Dollar traders brushed off current challenges. In November, Canada witnessed a sharper decline in retail sales than expected, and the Bank of Canada joined the growing list of central banks worldwide, signaling that rate cuts would occur at a slower and less aggressive pace than initially anticipated.

Retail sales in Canada dropped by 0.2% in November, falling short of the anticipated 0.0% and deteriorating from October’s 0.7%. Core retail sales recorded a more significant decline, registering at -0.5% compared to the expected -0.1% and the previous 0.4%. Additionally, there was a 1.7% increase in Canada’s Employment Insurance Beneficiaries Change in November, surpassing the previous 0.7%.

And According to the Maritime Sea Intelligence report, incidents caused by Iran-backed Houthi rebels in the Red Sea represent the second-largest disruption to vessel capacity in sea transport. This comes after the Ever Given, the giant cargo ship that was famously stuck and repaired in the Suez Canal in March 2021.

Sea-Intelligence, a maritime advisory firm, has reported that the disruptions caused by Houthi rebel attacks in the Red Sea are now having a more significant impact on the supply chain compared to the early stages of the COVID-19 pandemic. This reduction in vessel capacity is the second-largest in recent years, with the only event surpassing it being the Ever Given incident when the giant cargo ship became lodged in the Suez Canal for six days in March 2021.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

The New Zealand Dollar experienced a downward shift as a result of the decline in the NZ Manufacturing Index, which dropped from 46.5 in the previous month to 43.1. This decrease underscores the ongoing struggles within the manufacturing sector, attributed to the Reserve Bank of New Zealand’s decision to keep interest rates elevated.

The US Dollar is facing modest downward pressure as a result of an improved risk appetite in the market. Despite hawkish comments from Federal Reserve (Fed) members, the Greenback is experiencing this downward pressure as members of the Federal Open Market Committee (FOMC) enter the blackout period leading up to the January meeting. Market sentiment seems to be influenced by the expectation that the Fed may implement more interest rate cuts in 2024 compared to other major central banks, potentially leading to selling pressure on the US Dollar.

San Francisco Fed President Mary Daly’s acknowledgment of the significant work required to bring inflation back to the 2.0% target reflects a cautious approach. Additionally, Atlanta Fed President Raphael Bostic has expressed openness to adjusting his outlook on the timing of rate cuts, highlighting the US Fed’s commitment to a data-dependent approach.

On a positive note for the US Dollar, the upbeat US Consumer Sentiment Index has helped limit its losses. The preliminary Index for January rose to 78.8, surpassing the market consensus of 70 and exceeding the previous reading of 69.7. However, US Existing Home Sales Change declined by 1.0% after a previous increase of 0.8%.

Turning to New Zealand, the Business NZ Performance of Manufacturing Index reported a contraction on Friday, dropping to 43.1 from the previous figure of 46.5. This indicates potential challenges in New Zealand’s manufacturing sector. Looking ahead, market participants will closely monitor the upcoming release of New Zealand’s Consumer Price Index (CPI) data scheduled for Wednesday, with expectations of a reduction in the fourth quarter.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/