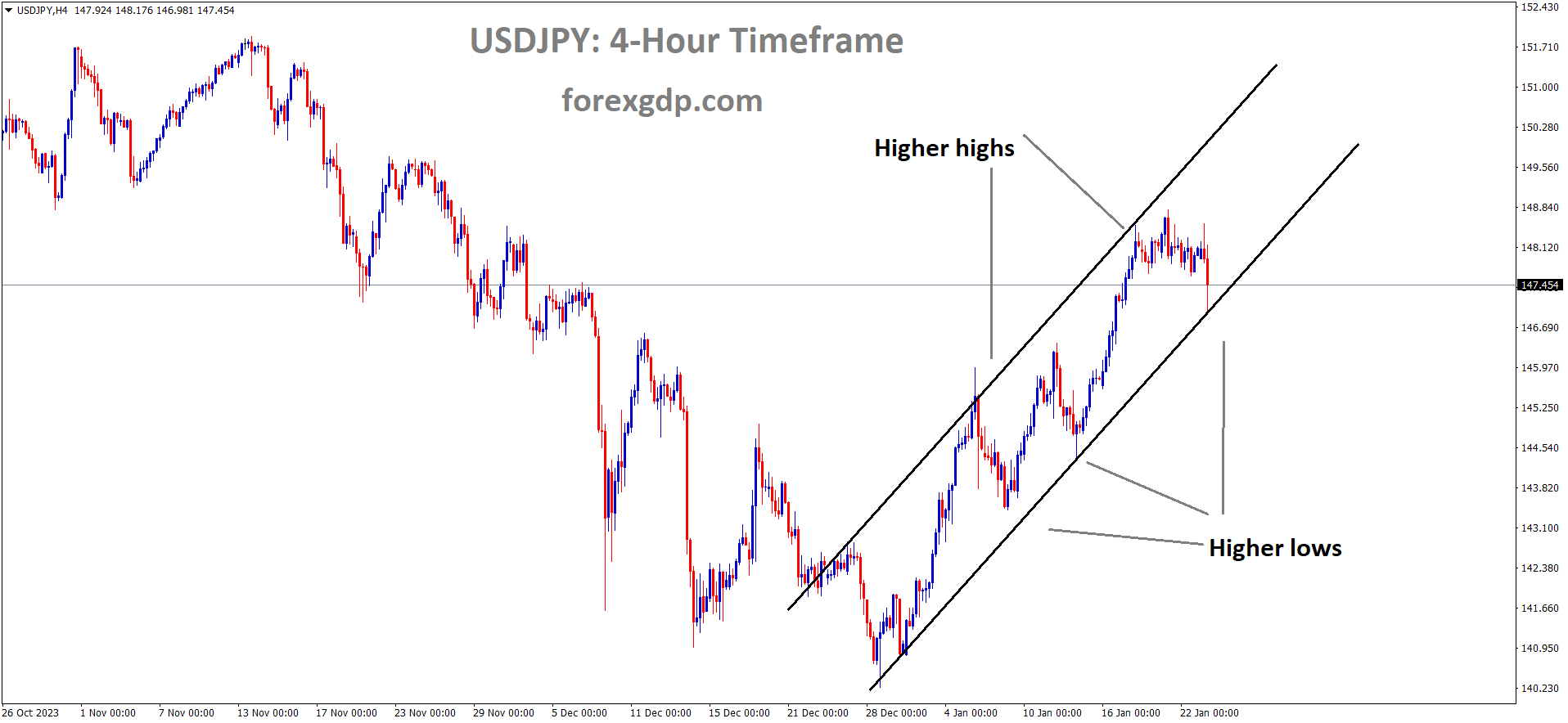

USDJPY Analysis:

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The Bank of Japan has decided to keep the interest rate at -0.10% and maintain the YCC rate unchanged. The inflation outlook remains moderately down, and consumption is expected to stay within a moderate range. We will adjust our monetary policy settings as needed when inflation approaches the 2% target and wage hikes become evident. Following the meeting’s outcome, the Japanese Yen experienced a decline in value.

Following its January monetary policy review meeting, the Bank of Japan board members have chosen to keep their existing policy settings unchanged. The Japanese central bank has decided to maintain the interest rate at -10 basis points and the 10-year Japanese Government Bond yield target at 0%. The BoJ is adhering to its yield curve control policy, which permits 10-year government bond yields to fluctuate up to approximately 1.0%. Furthermore, the BoJ has opted to leave the forward guidance on monetary policy unaltered.

The BoJ’s assessment of risks to economic activity remains relatively balanced. There is a need for vigilant monitoring to determine whether a virtuous cycle between wages and prices will intensify. The BoJ has committed to continuing its Quantitative and Qualitative Monetary Easing with Yield Curve Control for as long as necessary, and they are prepared to take additional easing measures if required. The BoJ emphasizes its commitment to maintaining monetary easing while remaining responsive to evolving circumstances. On the whole, Japan’s financial system has demonstrated stability, though some uncertainty persists. Nevertheless, the likelihood of achieving sustained 2% inflation continues to gradually increase, and Japan’s economy is expected to sustain its moderate recovery.

The BoJ also underscores the importance of staying vigilant regarding financial and foreign exchange market movements and their potential impact on Japan’s economy and prices. Inflation expectations are steadily on the rise, even as core consumer inflation has moved below 2.5%, partly due to a modest increase in service prices. Consumption continues to experience moderate growth.

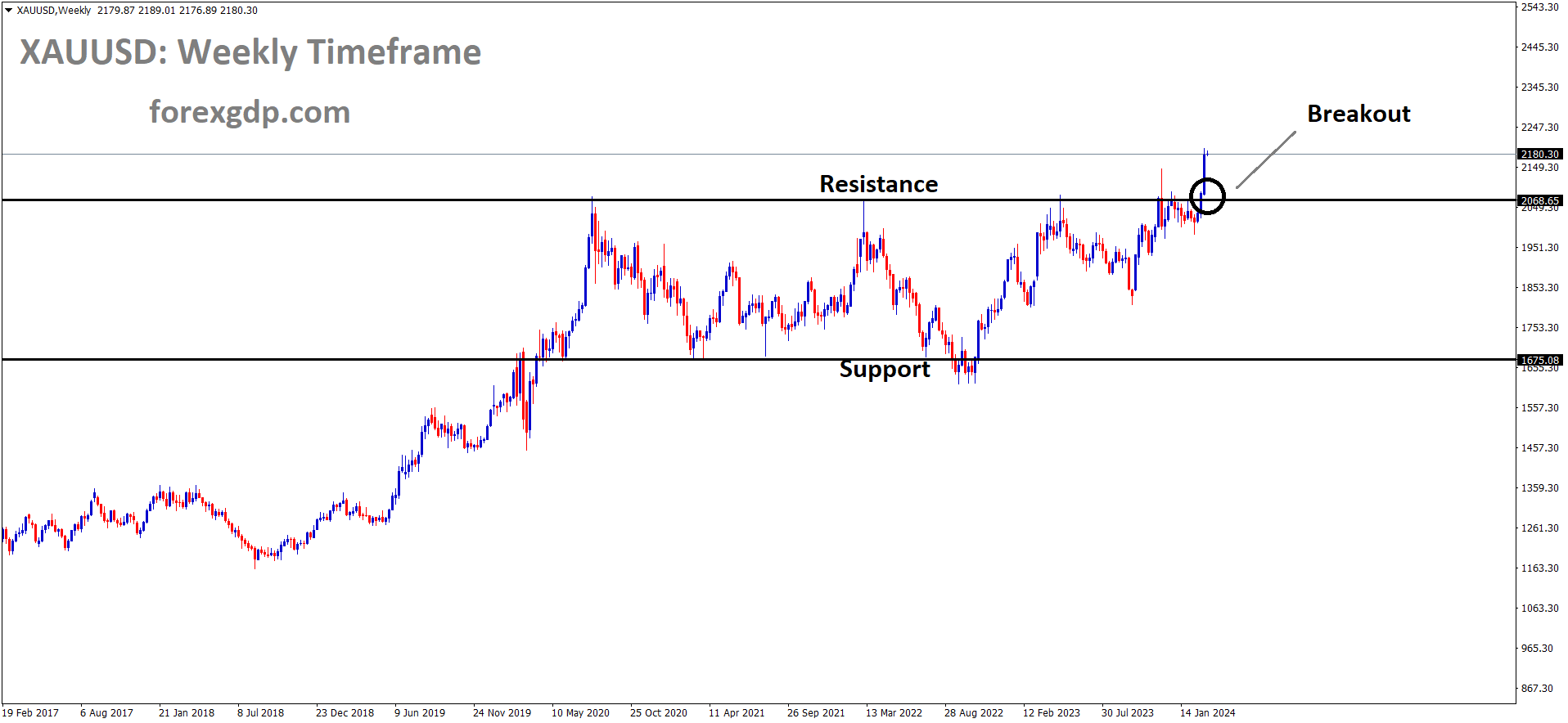

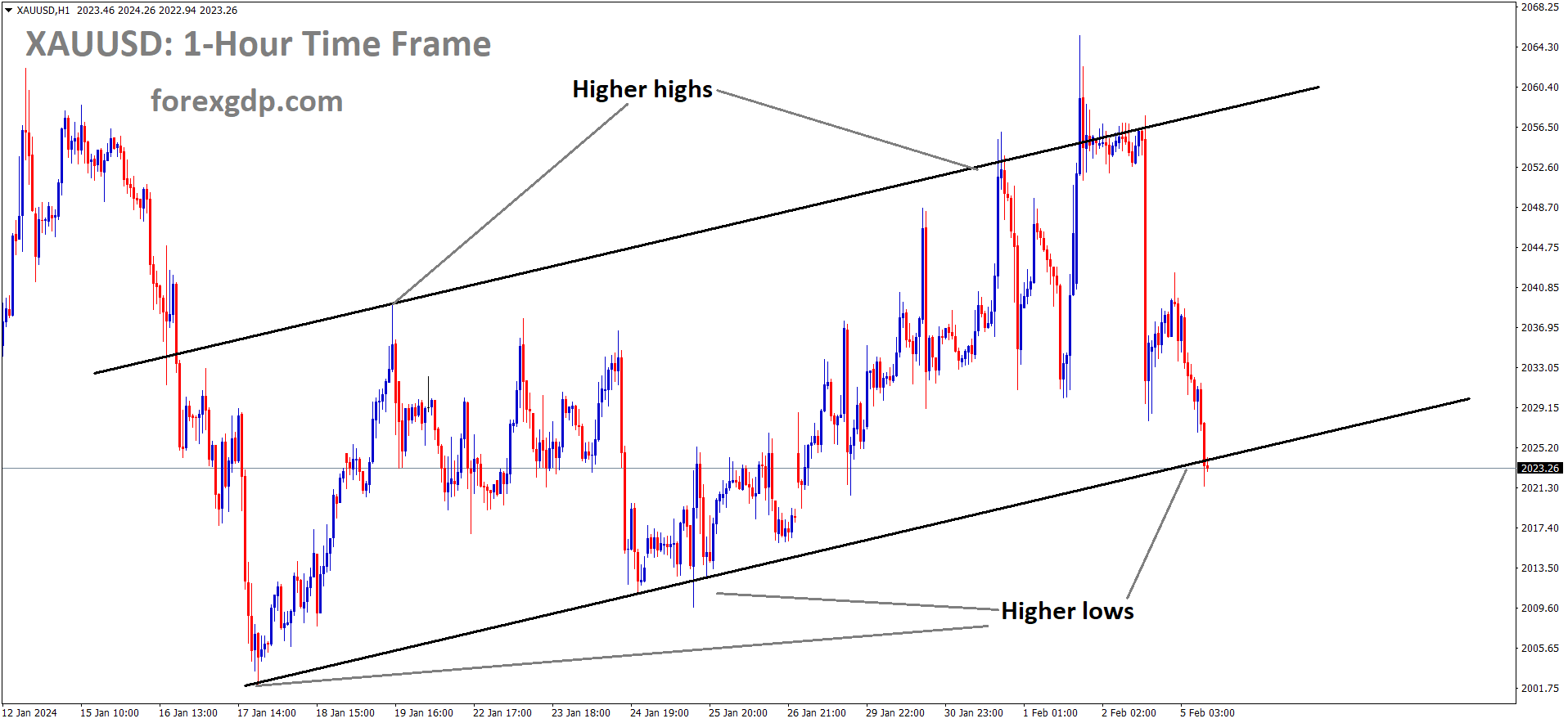

GOLD Analysis:

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

UBS economists have conducted an analysis predicting that the price of gold will reach the targeted level of $2250 by December 2024. There is a consistent demand for gold among central banks, and rate cuts are anticipated in the first half of 2024, which is expected to provide support for gold prices during the latter part of the year.

Gold experienced a remarkable turnaround in 2023, registering a gain of over 15%. UBS economists have conducted an analysis of the outlook for the precious metal in 2024. Their assessment suggests a positive trajectory for Gold prices throughout the year, making Gold an attractive hedge within investment portfolios. As the Federal Reserve is expected to initiate rate cuts starting in the second quarter, it is anticipated that demand for Gold through exchange-traded funds will become favorable. UBS has set a price target of $2,250 for December 2024 and recommends considering new long positions when Gold dips below the $2,000 mark.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending triangle pattern and the market has reached the support area of the pattern

The release of Michigan consumer sentiment last Friday reached its highest level since July 2021, registering at 78.8. As a result, the US Dollar gained strength against other currencies. Additionally, the possibility of future rate cuts by the Federal Reserve has diminished in the medium term, following the hawkish tone expressed by Fed members.

During early European trading, the US dollar is exhibiting a downward drift, coinciding with the commencement of the FOMC blackout period. This period restricts Federal Reserve staff from making public statements from one week before the Saturday preceding an FOMC meeting until the Thursday following the meeting. In the preceding two weeks, Federal Reserve members have been notably vocal, expressing their reservations about what they perceive as excessively high expectations for interest rate cuts. Their efforts have yielded some results, with market forecasts for 2024 rate cuts being reduced by approximately 30 basis points, resulting in the current reading of 133 basis points.

According to a report from the University of Michigan, Consumer sentiment surged by 13% in January, reaching its highest level since July 2021, thereby confirming that the significant increase observed in December was not an isolated occurrence. Consumers’ outlook was bolstered by growing confidence that inflation has taken a positive turn, accompanied by strengthening expectations of higher income. Over the past two months, consumer sentiment has climbed by a cumulative 29%, marking the most substantial two-month increase since 1991, when a recession came to an end. For the second consecutive month, all five components of the sentiment index have risen, featuring a remarkable 27% surge in short-term expectations for business conditions and a 14% improvement in current personal finances.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

In December, Swiss import and producer prices experienced a decrease. This reading has prompted the Swiss National Bank (SNB) to consider necessary adjustments in future monetary policy meetings. The strength of the Swiss franc has a positive impact on imports but a negative impact on exports.

The US Dollar is currently grappling with the challenge of declining US Treasury yields. As of the latest data available, the yields on US bond coupons for the 2-year and 10-year durations stand at 4.38% and 4.09%, respectively. Nevertheless, the Greenback has found support from hawkish statements made by members of the US Federal Reserve. San Francisco Fed President Mary Daly has expressed her belief that the central bank still has substantial work ahead to achieve the goal of bringing inflation back down to the 2.0% target. Furthermore, Atlanta Fed President Raphael Bostic has emphasized his readiness to adapt his outlook on the timing of potential rate cuts, underscoring the Fed’s commitment to a data-driven approach. These statements have bolstered support for the US Dollar. The US Dollar Index has slightly receded, nearing 103.20. The demand for the US Dollar is being driven by risk aversion sentiment, likely influenced by the heightened geopolitical tensions in the Middle East. Moreover, the US Conference Board Leading Economic Index improved from -0.5% in November to -0.1% in December, surpassing expectations for a reading of -0.3%. Looking ahead, the release of the Richmond Fed Manufacturing Index for January later in the North American session will provide further insights into the state of the US economy.

The Swiss Franc has faced selling pressure following remarks from Swiss National Bank Chairman Thomas Jordan expressing concerns about the potential impact of the CHF’s strength on the SNB’s ability to maintain inflation above zero within the Swiss domestic economy. Recent economic indicators have shown a slight increase in Swiss consumer prices in December and improved consumer demand in November. These factors could influence the SNB’s decision-making in the upcoming meeting. However, Swiss Producer and Import Prices declined in December, following a decrease in November. These more moderate figures might deter the Swiss National Bank from making adjustments to its monetary policy. In its last policy update in December, the SNB reaffirmed its commitment to adapting monetary policy if necessary to sustain inflation within the range consistent with price stability over the medium term.

USDCAD Analysis:

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The drone strikes in Ukraine targeting the Russian oil fields region have raised concerns about the oil supply, leading to a rebound in crude oil prices after the news was made public. Consequently, the Canadian dollar strengthened against other currencies.

In the previous trading session, the Canadian Dollar faced a decline against the US Dollar, a move attributed to the prevailing risk-averse sentiment stemming from the heightened geopolitical tensions in the Middle East. Meanwhile, the price of West Texas Intermediate (WTI) crude oil continued its upward trajectory for the second consecutive session, reaching approximately $74.70 per barrel at the time of this report. The surge in crude oil prices is primarily driven by concerns surrounding global energy supplies. These concerns have been exacerbated by a drone strike on Russia’s Novatek by Ukraine, further escalating geopolitical tensions. Additionally, disruptions in crude oil production within the United States due to extreme cold weather have contributed to the upward pressure on oil prices.

Traders are anticipated to closely monitor Canada’s December New Housing Price Index on Tuesday. On Wednesday, the Bank of Canada (BoC) is scheduled to announce its Interest Rate Decision. Market expectations suggest that the BoC will maintain its current policy rate of 5.0%.

is scheduled to announce its Interest Rate Decision")

The US Dollar Index (DXY) is currently holding steady following recent gains. The demand for the US Dollar is being fueled by the risk-averse sentiment, which is believed to be linked to the heightened geopolitical situation in the Middle East. Military actions, such as recent air strikes in Yemen conducted by the United States and the United Kingdom targeting Iran-led Houthi militants, have prompted investors to seek refuge in the safe-haven US Dollar. This, in turn, is providing support for the USDCAD currency pair.

Furthermore, the US Conference Board has reported a modest improvement in the Leading Economic Index for December. The index has moved from -0.5% in November to -0.1% in December, surpassing expectations for an improvement to -0.3%. Looking ahead, Tuesday is expected to bring the release of the Richmond Fed Manufacturing Index for January, offering additional insights into the state of the US economy.

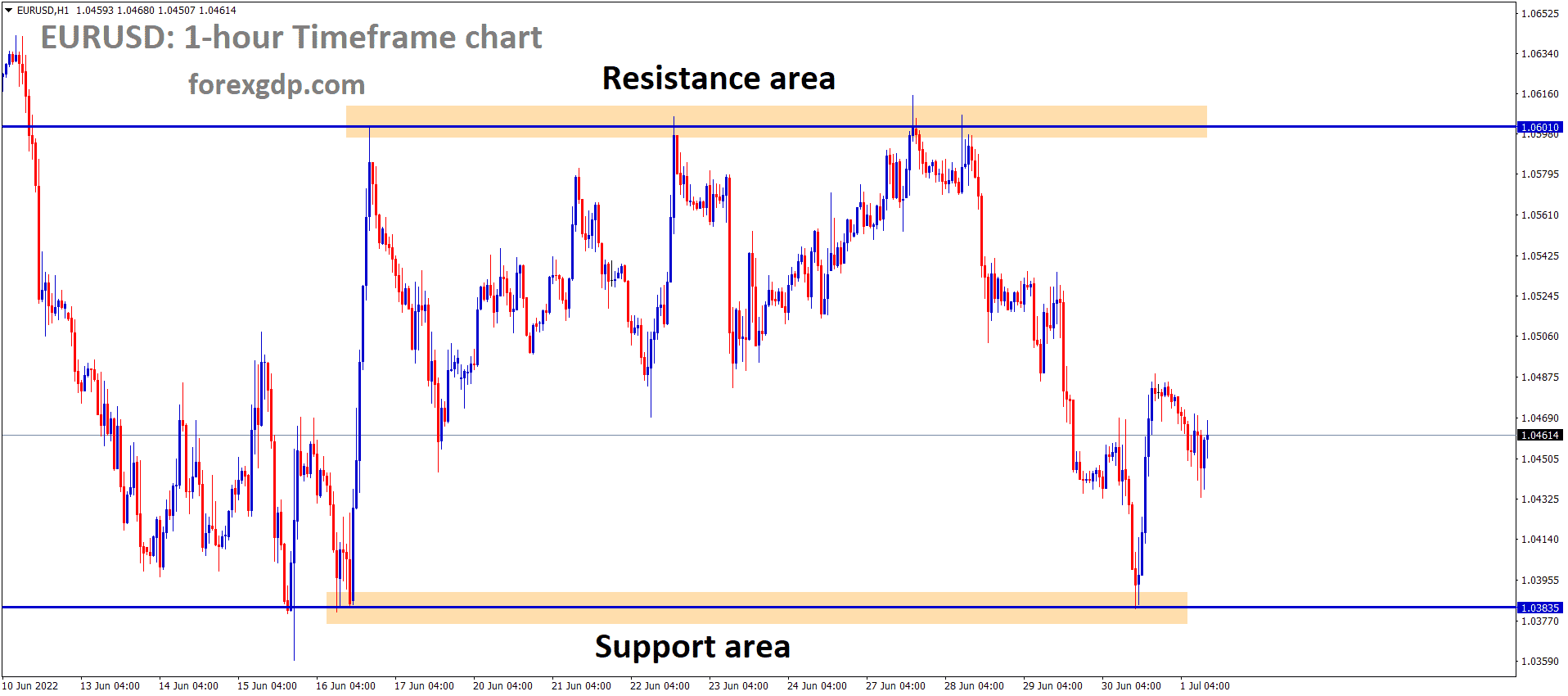

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

ECB President Christine Lagarde indicated that rate cuts are likely to be considered in the summer, but only if inflation aligns with our target range. Otherwise, interest rates will remain stable.

Traders appear cautious about making bold directional trades and are opting to stay on the sidelines due to the uncertainty surrounding the timing of a potential interest rate cut by the European Central Bank (ECB). Market expectations suggest the first ECB policy rate cut could occur in April, with a total reduction of 135 basis points by the end of 2024 already factored in by markets. However, ECB President Christine Lagarde indicated last week that any reduction in borrowing costs would likely begin in the summer, contingent upon supportive incoming economic data. As a result, the market’s attention remains firmly fixed on the ECB monetary policy meeting scheduled for Thursday, which is poised to significantly impact the euro and provide impetus to the EURUSD pair.

Simultaneously, decreasing odds of an early interest rate cut by the Federal Reserve (Fed) are bolstering the US Dollar while acting as a headwind for the EURUSD pair. Investors have moderated their expectations for aggressive policy easing in 2024, owing to the enduring resilience of the US economy and recent hawkish statements from several Fed policymakers. This has supported higher US Treasury bond yields, coupled with heightened geopolitical tensions in the Middle East, which have bolstered the safe-haven appeal of the US Dollar.

Nonetheless, USD bulls are displaying reluctance to make bold moves, given the prevailing risk-on sentiment in the market. Coupled with a mixed fundamental backdrop, this reluctance is likely to limit the downside for the EURUSD pair leading up to the crucial central bank event risk and important macroeconomic data releases scheduled for this week. On Wednesday, flash PMI figures for both the Eurozone and the US are set to be unveiled. Thursday will feature the release of the Advance US Q4 GDP report, followed by the US Core PCE Price Index, the Fed’s preferred inflation gauge, on Friday. These data releases are anticipated to inject volatility into the financial markets.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

A decrease in retail sales during the month of December prompted the Bank of England to keep its policy rate unchanged. Despite concerns of a potential recession in the UK’s economic outlook, the British Pound surprisingly saw a strong uptick in value instead of a decline.

The Bank of England is expected to maintain its current cautious monetary policy stance during its upcoming meeting. This expectation is bolstered by a Reuters poll in which economists predict that the Bank of England will keep the policy rate steady at 5.25% in its February meeting. The anticipation of stability in monetary policy has contributed to the positive performance of the Pound Sterling, providing support to the GBPUSD currency pair. The lackluster Retail Sales data for December from the United Kingdom, reported on Friday, likely added to the downward pressure on the British Pound. The significant decline in UK Retail Sales reflects deep economic challenges and heightened price pressures, raising concerns about the possibility of a technical recession. In this challenging economic environment, policymakers at the Bank of England find themselves in a difficult position as they navigate the path forward.

Investors will closely watch the preliminary UK S&P Global PMI data for January, scheduled for release on Wednesday. This data will offer additional insights into the current state of economic activity in the UK and could impact market sentiment and the performance of the GBPUSD pair. The US Dollar Index has retreated to around 103.10. However, the demand for the US Dollar may be influenced by risk aversion sentiment, likely triggered by the heightened geopolitical tensions in the Middle East. This has led investors to seek refuge in the safe-haven USD, putting pressure on the GBPUSD pair. Later in the North American session, the release of the Richmond Fed Manufacturing Index for January will provide further information on the state of the US economy. Traders will carefully analyze this data for potential effects on the US Dollar and broader economic trends.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

After 16 years of negotiations, India and Switzerland have successfully concluded a free trade agreement on Monday. This deal holds promise for creating job opportunities for the youth in both India and Switzerland.

After 16 years of negotiations, Switzerland and India have achieved a significant breakthrough in their free-trade discussions, as confirmed by Swiss Economy Minister Guy Parmelin. Following the World Economic Forum in Davos, Parmelin wasted no time and promptly traveled to India to meet with his counterpart, Piyush Goyal, as disclosed in a post on X over the weekend.

While the general framework of the agreement has been established, officials are currently working diligently to iron out the finer details. Parmelin emphasized that the agreement is poised to create employment opportunities for the youth in India and ensure job security in Switzerland, as reported by the Swiss newspaper Sonntagszeitung.

AUDCAD Analysis:

AUDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

The People’s Bank of China has decided to keep the LPR steady at 3.45% for one year and 4.2% for five years. Following this announcement, the Australian Dollar showed no significant movement in the exchange rates.

Chinese authorities opted to maintain lending rates unchanged on Monday, keeping the one-year and five-year loan prime rates at 3.45% and 4.2%, respectively, in line with anticipated outcomes.

The market sentiment still leans toward expecting additional measures to stimulate the economy, as demonstrated by the recent decision to leave the medium-term lending facility rate unchanged, resulting in a downturn in the markets. Given Australia’s substantial trading connections with China, the Australian economy and its currency are influenced by developments in China. It is worth noting that China holds the position of being the second-largest economy globally.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

The New Zealand Services Index for December showed a reading of 48.8, down from the November reading of 51.2. This contraction in the services PMI is concerning for the short-term prospects of growth and employment in New Zealand.

Data from Business NZ reveals that New Zealand’s Business NZ Performance of Services Index retreated from its six-month high in November to fall back into contraction in December. December’s NZ PSI recorded a reading of 48.8, a decline from the previous 51.2. The six-month average for the NZ PSI stood at 49.3, reflecting New Zealand’s ongoing struggle to cultivate economic confidence, as indicated by the survey results.

BNZ Head of Research Stephen Toplis expressed concern over the softening of the PSI, coupled with the weakness seen in the PMI, noting that this development bodes poorly for both short-term economic growth and employment in New Zealand. While tourism has played a pivotal role in driving the services sector and continues to provide support to the economy, it cannot bear the entire burden on its own.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/