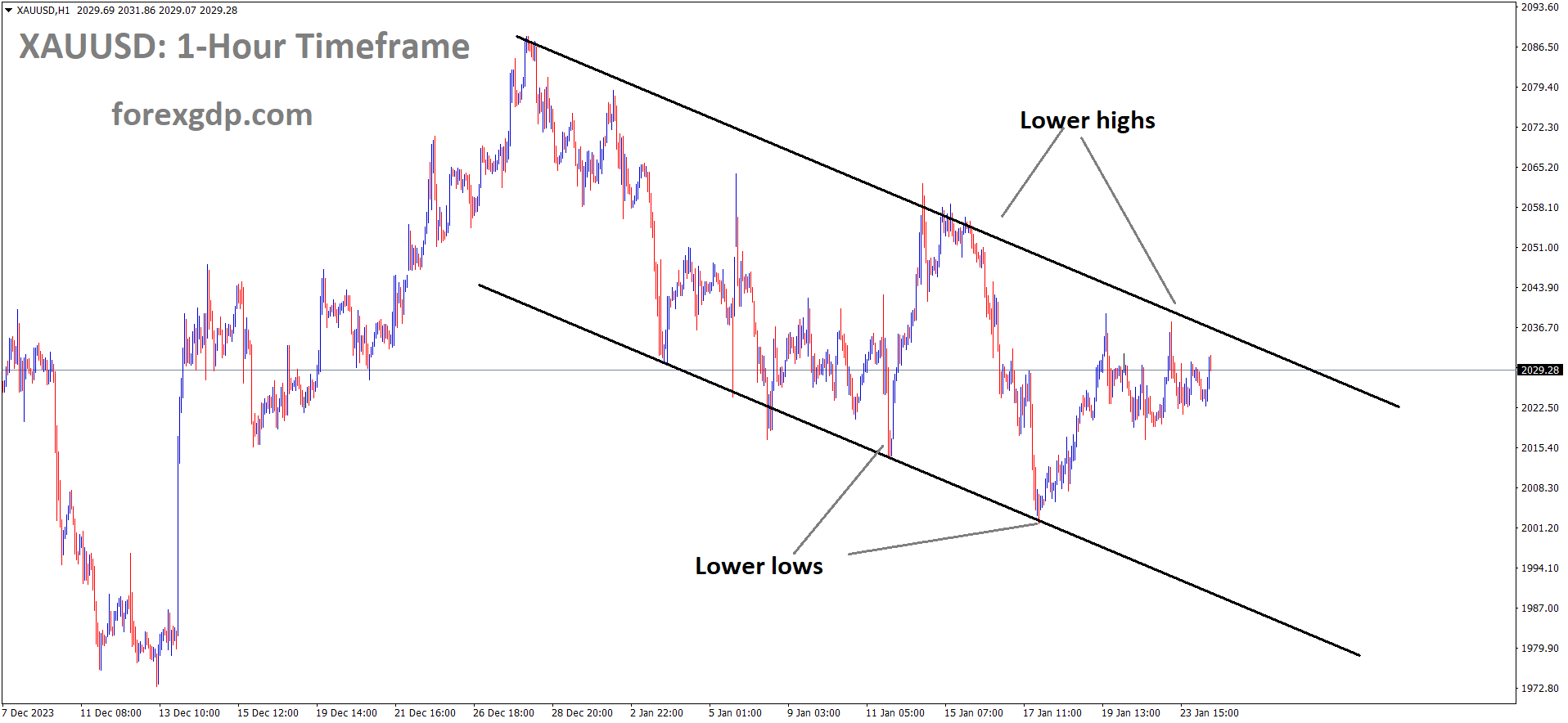

GOLD Analysis:

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

The decline in gold prices can be attributed to signals from US Federal Reserve speakers indicating a postponement of rate cuts in 2024. The increased likelihood of rate hikes or a stable rate environment in the first half of 2024 is bolstering the US Dollar’s position in the market.

The price of gold remains subdued as the European session begins on Wednesday, displaying a lack of significant selling pressure and remaining within a trading range that has persisted for several days. Traders appear hesitant to make bold moves and are choosing to await further indications regarding when the Federal Reserve might initiate interest rate cuts. Consequently, all eyes are on this week’s crucial US economic releases, starting with the flash PMIs later today, followed by the Advance Q4 GDP report on Thursday and the Core PCE Price Index on Friday.

As we approach these pivotal data releases, market participants have seemingly delayed their expectations for the Fed’s first interest rate cut from March to May. This shift in sentiment is viewed as a primary factor dampening the appeal of gold, which offers no yield. However, the US Dollar is facing some downward pressure due to a modest retreat in US Treasury bond yields, keeping the greenback bulls at bay, despite reaching its highest level since December 13th just the day before. Additionally, concerns persist regarding the ongoing conflict in the Middle East and the uncertain global economic outlook, factors that should help limit potential losses for the safe-haven XAUUSD.

Incoming US economic data continues to suggest a robust economy, providing the Federal Reserve with more flexibility to maintain higher interest rates for an extended period. This, in turn, acts as a headwind for the price of gold. The current market pricing reflects an increased likelihood of the Fed’s first interest rate cut occurring in May, a shift from the initial expectation of March, and suggests a less aggressive approach to policy easing than what investors had previously anticipated. While the US Dollar is consolidating near multi-week highs, exerting some pressure on the non-yielding precious metal, geopolitical risks and the uncertain global economic outlook serve as buffers, preventing more significant declines.

Recent US military strikes against facilities used by Iranian-affiliated militant groups in western Iraq have heightened tensions in the Middle East and raise the risk of further escalations. Traders, cautious about these geopolitical developments, are refraining from making aggressive directional bets and are opting to stay on the sidelines until after this week’s key US economic releases. These data points, including the flash PMIs, the Advance Q4 GDP report, and the Core PCE Price Index, will play a crucial role in shaping market expectations regarding the Federal Reserve’s future policy decisions. As a result, they will impact the demand for the US Dollar and determine the short-term trajectory of XAUUSD.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

The scheduled release of US Q4 GDP data today is expected to reveal a contraction, which has led to a consolidation of the US Dollar against other currencies.

The US Dollar index has been on an upward trajectory, currently trading around the 103.70 level. This surge is driven by anticipation surrounding crucial inflation data and the impact of rising yields, as markets scale back their expectations of a dovish stance by the Federal Reserve. The US economy continues to exhibit strength, and traders are eagerly awaiting significant data releases and central bank meetings later this week. Despite the absence of major data releases or Federal Reserve speakers, the market has adjusted its expectations for rate cuts in 2024, reducing them from approximately 175 basis points earlier this month to around 125 basis points, which has contributed to the US Dollar’s recovery.

On Thursday, the US is set to unveil December’s Personal Consumption Expenditures data, with expectations that inflation may have stalled. Additionally, Gross Domestic Product figures for Q4 are scheduled for release, and there is an anticipation of a slowdown in economic activity. US bond yields are on the rise, with the 2-year yield at 4.40%, the 5-year yield at 4.06%, and the 10-year yield at 4.15%. All three rates are nearing their highest levels in January, reflecting adjustments in expectations regarding the next Federal Reserve decision. Projections from the CME Fed Watch Tool indicate that the market’s timeline for the start of an easing cycle has shifted to May.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

SNB Chairman Thomas Jordan has stated that the strengthening of the Swiss Franc against foreign currencies is acting as a restraint on inflation. Consequently, concerns of a recession occurring in the Swiss economy in 2024 are unfounded. The policy can be adjusted in response to incoming data as needed.

The US Dollar Index has slightly dipped, nearing the 103.40 mark, as of the latest update. This movement comes alongside the 2-year and 10-year yields on US bond yields, which currently stand at 4.32% and 4.11%, respectively. The prevailing market sentiment indicates a reduced probability of the Federal Reserve implementing an interest rate cut in March.

However, it’s worth noting that former St. Louis Fed President, James Bullard, holds a differing perspective. Bullard anticipates that the Fed may initiate interest rate cuts even before inflation reaches the 2.0% target, with the possibility of such cuts occurring as early as March. Additionally, there is full pricing in of a 25 basis point rate cut in May, while the likelihood of a 50 basis point cut stands at 50%. Market participants are eagerly awaiting the release of the S&P Global Purchasing Managers Index PMI data from the United States.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Swiss National Bank President, Thomas Jordan, addressed the strength of the Swiss Franc during an event in the Swiss town of Brig on Tuesday. He acknowledged that the robust Swiss Franc has played a role in curbing inflation. Furthermore, Jordan expressed confidence in the Swiss economy, asserting that economists and the central bank share the belief that a recession is not on the horizon. He emphasized that while a recession is not expected, the economic outlook does indicate subdued growth.

In terms of economic indicators, the Federal Statistical Office of Switzerland reported last week that the decline in Producer and Import Prices moderated in December compared to the previous month’s decrease. Looking ahead, traders are eagerly anticipating the release of Real Retail Sales data and the ZEW Survey Expectations in the coming week, which are expected to provide further insights into the potential trajectory of the Swiss National Bank’s interest rates.

GBPUSD Analysis:

GBPUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

Anticipated data for today’s scheduled release suggests that both the UK Services and Manufacturing PMI readings are likely to exceed their previous levels. However, given the ongoing contraction in domestic data readings, it is expected that the Bank of England will maintain its current interest rates in the upcoming meeting.

Investors are eagerly awaiting the release of January’s advanced Manufacturing and Services PMI data in the UK, hoping for fresh market-moving insights. In the United States, the Richmond Fed Manufacturing Survey reported a decline in the composite manufacturing index for January, dropping to -15 from -11 in December, which was worse than the market’s expectation of -7. Among the survey’s three component indices, shipments increased from -17 to -15, new orders declined from -14 to -16, and employment saw a significant drop from -1 to -15.

Federal Reserve governor Christopher Waller emphasized the need for the Fed to approach rate cuts “methodically and carefully” rather than rushing into them. Atlanta Fed President Raphael Bostic hinted at the possibility of rate cuts starting in the third quarter, while San Francisco Fed President Mary Daly stressed the importance of patience regarding rate adjustments. This less aggressive stance on rate cuts by the Fed is providing support to the US Dollar (USD) and is acting as a headwind for the GBPUSD pair.

Conversely, investors are speculating that the Bank of England may begin reducing rates as early as May, with three additional cuts anticipated throughout 2024, bringing rates down to 4.25% from the current 5.25%. However, there is no expected change in monetary policy during the Bank of England’s February meeting. Market participants will closely watch the data release on Wednesday for further guidance.

The preliminary UK S&P Global Services PMI is expected to ease from 51.4 in December to 51.0 in January, while the Manufacturing PMI is projected to remain stable at 47.9. Both the UK S&P Global/CIPS Purchasing Managers Index and the US S&P Global PMI reports are set to be released on Wednesday. Attention will then shift to the US Gross Domestic Product for Q4 on Thursday and the Core Personal Consumption Expenditures Price Index on Friday. These figures could influence central bank policymakers’ decisions regarding the future course of monetary policy.

GBPJPY Analysis:

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The Bank of Japan’s decision to maintain interest rates on the last day has contributed to the prevailing weakness of the JPY in the market. Tomorrow, we anticipate the release of Tokyo CPI data, with inflation expected to decrease from 2.1% to 1.9%.

The Bank of Japan has decided to maintain its policy rate in negative territory at -0.1%, and it intends to continue doing so until it observes more indications that inflation will not fall below expectations in the future. Unlike most global central banks, the BoJ is facing the opposite challenge.

Japan has long struggled to generate significant inflation in its domestic economy, and the BoJ is concerned that any upward adjustments in interest rates, in the absence of already rising wages and inflation pressures, could trigger structural deflation. On Thursday, Japan will release the next round of Tokyo Consumer Price Index inflation figures, and both the markets and the BoJ will closely monitor them for any signs that price pressures will not dip significantly below the BoJ’s desired 2% level. The forecast for January’s Tokyo CPI suggests a slight decline from 2.1% to 1.9%.

Additionally, on Friday, the United States will publish Personal Consumption Expenditure (PCE) inflation figures, which are the Federal Reserve’s preferred indicators for tracking US inflation. It is anticipated that December’s Core US PCE Price Index will exhibit a slight increase from 0.1% to 0.2%, while the year-on-year Core figure is expected to ease from 3.2% to 3.0%.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

In anticipation of the upcoming ECB meeting tomorrow, the Euro currency has displayed a positive trend against its counterparts. The ECB is inclined towards maintaining steady interest rates rather than implementing rate cuts or hikes. Additionally, today marks the scheduled release of Manufacturing PMI data for the Eurozone.

The market is eagerly awaiting the release of European and US Purchasing Managers’ Index (PMI) data. Expectations for the pan-European HCOB Composite PMI figures in January are for a rebound from 47.6 to 48.0. This would mark the eighth consecutive month of PMI activity below the 50.0 threshold, indicating a continued slowdown in economic activity across Europe. On the US front, market forecasts anticipate that the S&P Global Manufacturing PMI component will remain unchanged at 47.9, while the Services PMI component is expected to dip from 51.4 to 51.0.

Following the release of the PMI data, Thursday brings another interest rate decision and monetary policy statement from the European Central Bank (ECB). The prevailing consensus suggests that interest rates will remain unchanged until the summer, barring any significant shifts in economic indicators. However, investors will closely scrutinize the ECB’s policy statement for hints about the central bank’s leaning toward dovish or hawkish policies, especially in light of Wednesday’s PMI data. Thursday also features an update on the US Gross Domestic Product on an annualized basis, with year-on-year GDP forecasted to decline from 4.9% to 2.0% for the year ending in December.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Bank of Canada is anticipated to maintain its interest rates at 5.00% during today’s meeting, in line with recommendations from leading economists. This decision comes against the backdrop of elevated inflation in recent months and a deceleration in business activity, resulting in reduced public spending.

The Bank of Canada is set to make its first policy announcement of 2024, which has garnered significant attention from economists and major banks who are eagerly awaiting the Interest Rate Decision. Alongside this decision, we can anticipate receiving a fresh Monetary Policy Report with updated forecasts. It is widely anticipated that the BoC will maintain the overnight rate at the current level of 5.00%. The financial community will closely monitor the subsequent press conference for insights.

Canadian core inflation in December exceeded expectations, suggesting that the BoC is unlikely to pivot toward a dovish stance during the January policy meeting. Nevertheless, the impact of higher interest rates is being felt, as evidenced by the recent BoC Business Outlook Survey, which reported reduced demand and less favorable business conditions in the fourth quarter. The majority of firms have been negatively affected by these high interest rates, resulting in no plans to expand their workforce. Consequently, it appears that inflation may ease in the coming months, leading us to favor rate cuts starting in the second quarter, possibly in April. We expect the BoC to adhere to its current course by keeping the overnight rate at 5.00% and maintaining its existing guidance. With core inflation and wage growth gaining momentum, there is limited room for a shift in the Bank’s messaging. The statement is expected to lean hawkish, emphasizing the persistence of price pressures despite minor downward revisions to MPR forecasts. This stance can strengthen the Canadian Dollar, especially when compared to G10 peers whose central banks lean more dovish, such as the Swiss Franc.

In summary, the BoC is widely expected to keep the overnight rate unchanged at 5% in its first policy decision of 2024, extending the pause initiated after the last rate hike in July. While there may be some mention of potentially ending quantitative tightening policy earlier than expected, the primary goal would be to ensure adequate liquidity in funding markets, rather than signaling an imminent shift to easier monetary policy and rate cuts. The BoC is likely to exercise caution in prematurely declaring victory over inflation and is expected to implement the first rate cut around the middle of the year, followed by additional reductions totaling 75 basis points by the end of 2024. The focus will be on the guidance provided by the Governing Council, which is not expected to significantly alter its leaning towards rate hikes, given recent core inflation trends. The press conference is likely to emphasize the need for further progress on inflation before discussing rate cuts and may also highlight a broader range of inflation measures as a guide for monetary policy.

For the fourth consecutive meeting, no change in the overnight rate is anticipated. While there have been some discussions about potential changes to quantitative tightening (QT), no significant shifts are expected in that regard at this time. Progress has been made in bringing inflation down, but there is still work to be done to reach the 2% target. Rate cuts are likely in 2024, but the BoC will exercise patience to ensure that inflation and inflation expectations retreat further. Following several years of inflation above the target, policymakers aim to avoid easing policy prematurely and allowing inflation to accelerate again. Therefore, we anticipate the BoC will maintain its policy rate at 5.00%, with the accompanying statement potentially leaning toward a hawkish tone. The BoC is expected to reiterate its concerns about inflation risks and its readiness to raise the policy rate further if necessary. Wage growth and services inflation are likely to be focal points for BoC policymakers, and updated economic projections will be offered at the meeting, with forecasts of a gradual return of CPI inflation toward the 2% target viewed as a hawkish signal.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Australian Dollar has gained strength against its counterparts due to the better-than-expected Australian PMI data. The Manufacturing Index PMI rose to 47.6 from 50.3, the Services Index improved from 47.1 to 47.9, and the Composite PMI increased to 48.1 from 46.9.

Despite the positive preliminary Purchasing Managers Index (PMI) from Australia, which is released monthly by Judo Bank and S&P Global, the Australian Dollar retraced its recent gains on Wednesday. In contrast, the US Dollar maintained stability and retained its positive position from the previous session, despite a decline in the 2-year United States bond yield.

Australia’s PMI data for January indicated a favorable shift in business activity across all sectors. The Manufacturing PMI improved significantly, rising from 47.6 to 50.3. Similarly, the Services PMI showed an uptick, increasing from 47.1 to 47.9. The Composite PMI also registered growth, reaching 48.1 compared to December’s 46.9. Additionally, Australian shares continued their upward trajectory, achieving a third consecutive record high. This surge was attributed to improved performance in mining and energy stocks, which had a positive impact on the AUDUSD pair.

In contrast, the US Dollar Index remained stable following its recent upward trend. This stability was driven by continued buying interest in the US Dollar due to risk aversion sentiment, likely related to escalating geopolitical tensions in the Middle East. The US Secretary of Defense confirmed that US military forces conducted strikes on facilities used by Iranian-backed groups in Iraq, responding to a series of escalating attacks.

Traders are keenly awaiting the release of the S&P Global Purchasing Managers Index data from the United States, scheduled for Wednesday. This data is expected to provide valuable insights into the nation’s business activities, influencing market sentiment regarding the Federal Reserve’s interest rate trajectory. Money market futures indicated a reduced likelihood of a rate cut by the Fed in March. However, by May, there is full pricing for a 25 basis point cut, with a 50 basis point cut standing at a 50% probability.

Other economic indicators from Australia include a decline in the Westpac Leading Index for December compared to November’s growth. National Australia Bank’s Business Conditions decreased from 9 to 7 in December, while Business Confidence improved to -1 from the previous figure of -9. Australia’s Consumer Inflation Expectations remained steady at 4.5% in January. The Chair of Australia’s sovereign wealth fund, Peter Costello, noted early signs of inflation moderation but emphasized the need for further progress to align prices with the RBA’s target band.

The People’s Bank of China maintained its Loan Prime Rate at 3.45% for the one-year term and 4.20% for the five-year term. In the United States, the Leading Economic Index for December showed slight improvement, moving from -0.5% in November to -0.1% in December, surpassing expectations. Additionally, the preliminary US Michigan Consumer Sentiment Index for January rose to 78.8, exceeding the expected figure of 70, up from the previous reading of 69.7.

Governor Pan Gongsheng of the People’s Bank of China remarked on Wednesday that China’s monetary policy is tailored to the nation’s domestic circumstances. He further indicated a commitment to enhancing the credit structure and increasing support for private enterprises and small businesses, according to Reuters.

Pan also affirmed their intention to utilize a range of policy instruments to maintain a reasonable level of liquidity and reiterated their steady promotion of Yuan internationalization.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The New Zealand Q4 CPI data has surprised by coming in lower than anticipated, registering at 4.7% compared to the 5.6% reported in Q3. However, it is worth noting that this figure remains above the Reserve Bank of New Zealand’s 2% target. Given the persistent high inflation in the market, immediate rate cuts in the near term are unlikely. As a result, the New Zealand Dollar showed a positive response following the release of this data.

According to data released by Statistics New Zealand, domestic consumer inflation in the final quarter of 2023 slowed down, moving from a year-on-year rate of 5.6% to 4.7%. However, it’s worth noting that this figure remains significantly higher than the Reserve Bank of New Zealand’s target range of 1% to 3%. As a result, the chances of the central bank implementing an interest rate cut in the near future are limited. This, combined with the relatively quiet performance of the US Dollar, may offer some support to the NZDUSD currency pair.

Nonetheless, the potential downside for the USD appears to be constrained due to expectations that the Federal Reserve will not hastily reduce interest rates, given the ongoing resilience of the US economy. Additionally, factors such as the possibility of further escalations in geopolitical tensions in the Middle East and the uncertain global economic outlook could continue to favor the safe-haven Greenback, thus capping any substantial gains for the risk-sensitive New Zealand Dollar.

Market participants may exercise caution in making aggressive directional bets, instead opting to wait for key US economic releases scheduled for later in the week. These releases include the Advance Q4 GDP report and the Core PCE Price Index. In the interim, developments such as the flash US PMIs, movements in US bond yields, and broader risk sentiment will likely provide some impetus to the NZDUSD exchange rate.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/