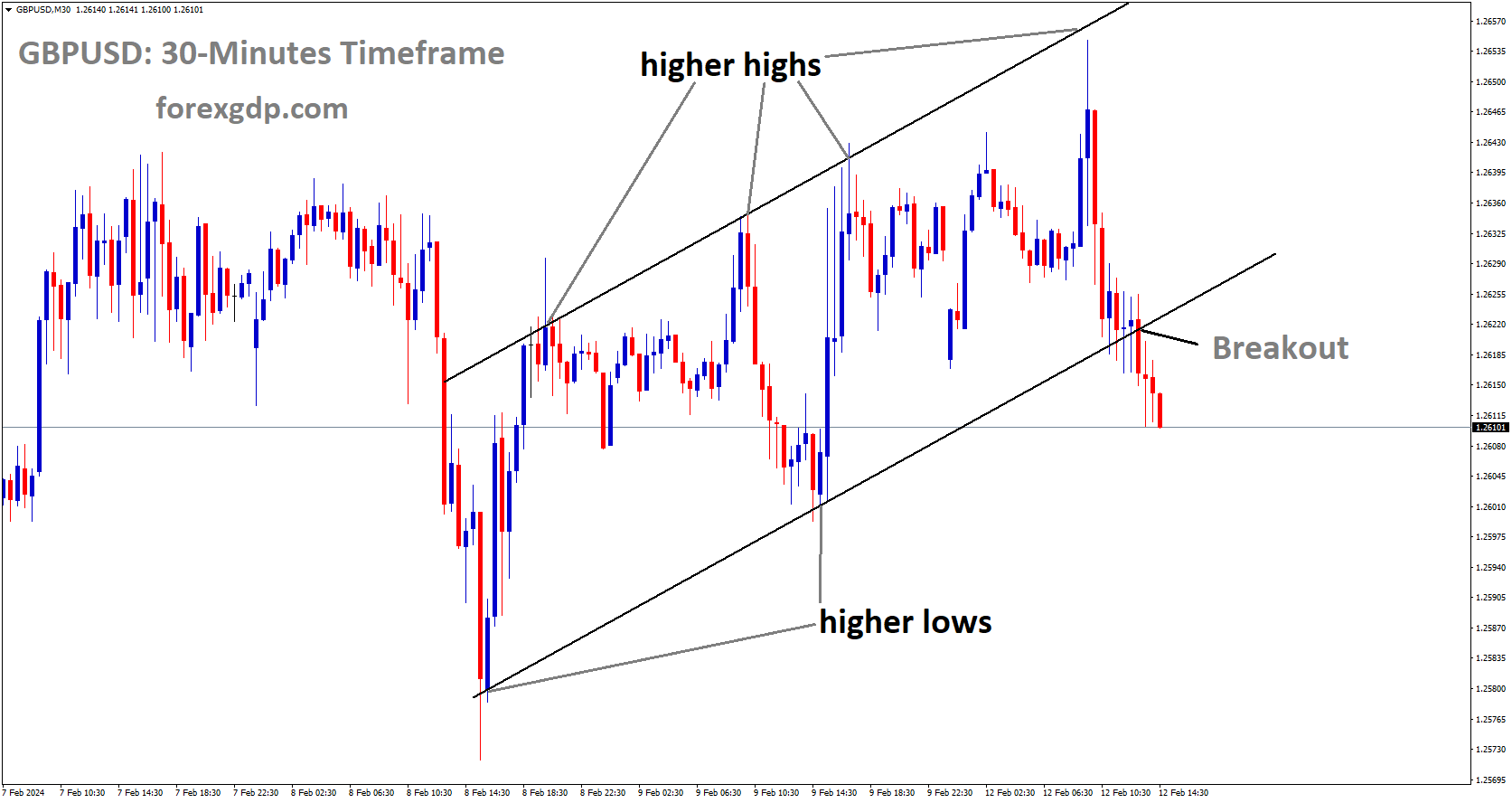

GBPUSD has broken Ascending channel in downside

GBPUSD – Factors Influencing GBP/USD Movement and Market Sentiment

– GBP/USD experiences a slight uptick, primarily influenced by a modest weakness in the US dollar (USD). However, the potential for further gains is limited.

– The prevailing uncertainty regarding potential rate cuts by the Federal Reserve (Fed) and a prevailing positive tone in market risk sentiments contribute to a defensive stance among USD bulls.

– Speculative bets on the likelihood of the Bank of England (BoE) initiating rate cuts within the next few months act as a ceiling on the GBP’s upward trajectory.

– The USD continues to grapple with challenges in gaining significant traction, largely due to uncertainties surrounding the Fed’s stance on rate adjustments.

– Furthermore, the prevailing bullish sentiment within global equity markets undermines the traditional safe-haven appeal of the USD, offering some degree of support to the GBP/USD pair.

– Market dynamics are shifting as expectations for imminent and aggressive rate cuts by the Fed in 2024 diminish.

– Comments from key figures within the Federal Reserve, such as Dallas Fed Bank President Lorie Logan, emphasizing a cautious approach to rate adjustments, lend support to US Treasury bond yields, thus bolstering the USD and restraining meaningful gains for GBP/USD.

– Additionally, remarks from Atlanta Fed President Raphael Bostic underscore concerns about persistent inflation and suggest that the US economy is on track to return to pre-pandemic levels of activity, further supporting USD strength.

– The growing consensus among market participants that the Bank of England may opt for rate cuts in the near future dampens investor enthusiasm for the GBP.

– Market pricing indicates the possibility of multiple rate cuts by the BoE by the conclusion of the year, which acts as a deterrent for aggressive bullish positioning on the GBP.

– Consequently, traders exercise prudence and adopt a wait-and-see approach, anticipating clearer indications of sustained bullish momentum before committing to significant positions.

– Moreover, market participants remain attentive to forthcoming macroeconomic data releases, particularly the latest consumer inflation figures from both the US and the UK, which are expected to provide further insights into the direction of monetary policies and currency movements.

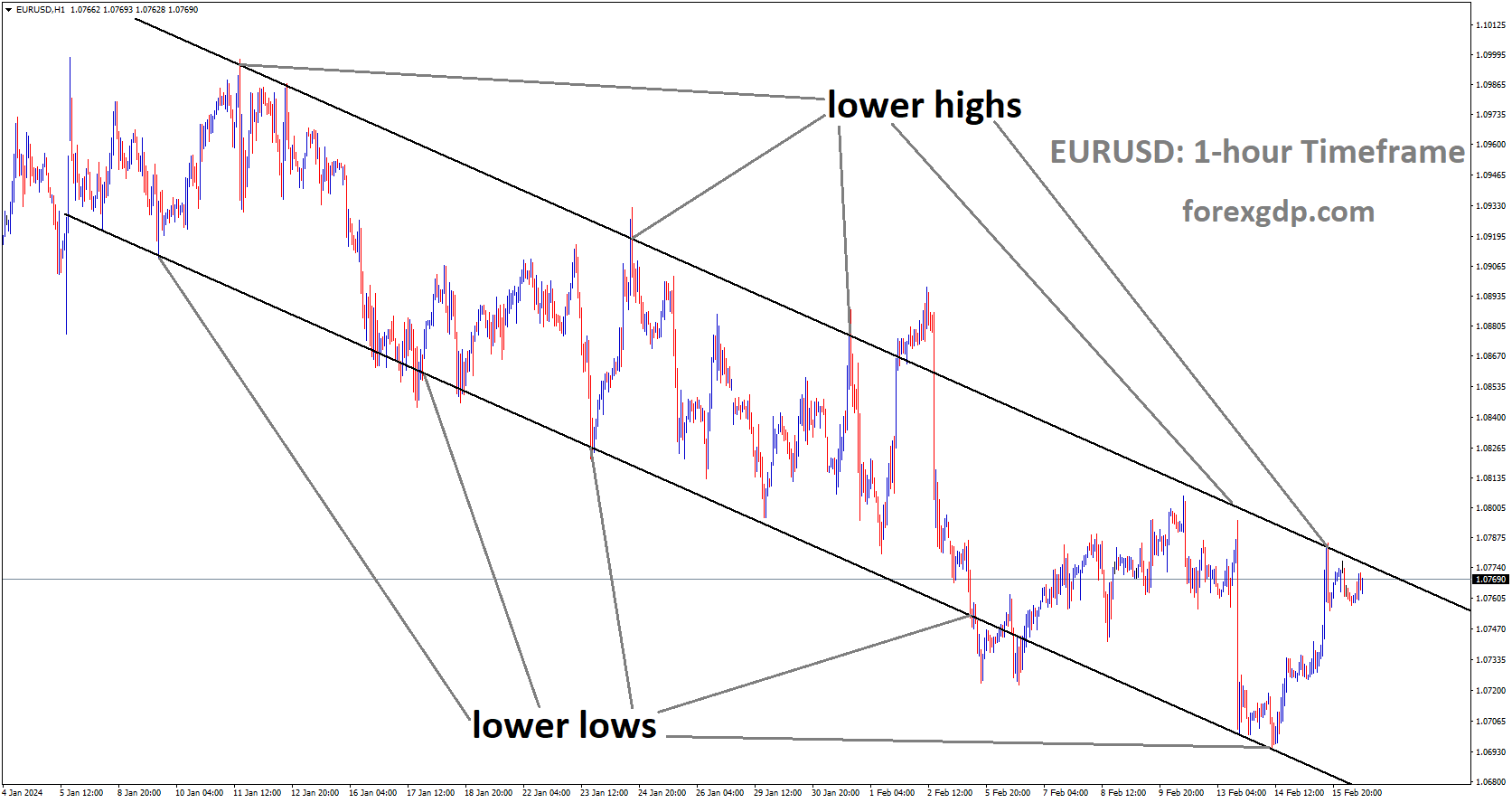

EURUSD – Market Update: USD Dips Pre-CPI Release, ECB and Fed Signals Awaited

– The US Dollar (USD) experienced a decline before the weekend due to an announcement by the Bureau of Labor Statistics (BLS). The BLS revised the monthly increase in the Consumer Price Index (CPI) for December downward from 0.3% to 0.2%.

– The BLS is set to release CPI figures for January on Tuesday. Given this impending release, investors may exercise caution in taking significant positions prior to the publication of the inflation report.

EURUSD is moving in Ascending channel and market has reached higher low area of the channel

-Over the weekend, Fabio Panetta, a member of the European Central Bank (ECB) Governing Council, asserted that the timing for an interest rate cut was nearing. Panetta emphasized that speculating on the exact timing of monetary easing would be futile. Despite his remarks, there was minimal impact on the EUR/USD pair at the beginning of the week.

-The US economic calendar for Monday does not include any high-impact data releases. Concurrently, US stock index futures indicate a lack of significant movement in the early European session, suggesting a neutral risk sentiment prevailing in the market.

-Later in the day, multiple Federal Reserve (Fed) policymakers are scheduled to deliver speeches. However, prevailing market sentiment indicates a widespread belief that a rate reduction in March is unlikely. Consequently, comments from these officials are not anticipated to exert significant influence on market positioning.

USD Outlook Positive, EUR Remains Uncertain

– Fed easing expectations have been substantially adjusted, placing emphasis on forthcoming data to validate the optimistic outlook.

– Anticipated economic resilience and potential resistance to early, significant rate cuts are projected from Fed officials.

– Conversely, sentiment regarding the eurozone remains recessionary, despite economic data consistently surpassing expectations across the bloc, as indicated by Citigroup’s surprise index.

– While there are high expectations for the USD, contrasting sentiments prevail for the EUR, suggesting differing market perceptions and outlooks for the two currencies.

USDJPY – BoJ’s Shift: Negative Rates in April?

USDJPY is moving in Ascending channel and market has fallen from higher high area of the channel

– Monday’s focus will be on the Bank of Japan (BoJ) as it remains under scrutiny regarding its monetary policies.

– A recent Japan Times article highlighted wage growth patterns in Japan, indicating a positive trend. Japanese companies are reportedly increasing entry-level salaries for new hires. Notably, firms like Nomura Holdings are planning substantial wage hikes of up to 16% for younger employees.

– This report emerges just ahead of the annual wage negotiations set to commence in March. The progress observed in wage increases could potentially bolster the BoJ’s intentions to shift away from negative interest rates.

– Bank of Japan’s remarks concerning wage growth trends and plans regarding interest rate adjustments are poised to have a significant impact on market dynamics on Monday.

FOMC Members Await US CPI Report

– Monday’s attention will be on the Federal Reserve (Fed) as investors assess the potential timeline for a Fed rate cut.

– FOMC members Michelle Bowman and Neel Kashkari are scheduled to deliver speeches, garnering significant interest from market participants. Bowman recently indicated that it was premature to consider implementing rate cuts. Conversely, Kashkari expressed the need for greater confidence in inflation returning to the target before supporting any rate reduction.

– The impact of similar remarks from FOMC members following the release of the latest US economic indicators could potentially constrain the upside potential for the AUD/USD currency pair.

– The US Consumer Price Index (CPI) Report, scheduled for release on Tuesday, holds significant importance for market sentiment regarding expectations of a Fed rate cut in March.

– Notably, there are no major US economic indicators slated for release on Monday, implying that the USD/JPY pairing may lack significant directional cues for the day.

Short-Term Outlook: USD/JPY

– Short-term movements in the USD/JPY pair will be influenced by central bank speakers and the upcoming US Consumer Price Index (CPI) Report scheduled for Tuesday.

– Any indications of weaker-than-expected inflation in the US could impact the Federal Reserve’s forward guidance regarding monetary policy.

– Conversely, recent reports suggesting growth in wages might prompt the Bank of Japan (BoJ) to consider moving away from negative interest rates.

– Increasing expectations of a shift in policy by the BoJ away from negative rates would potentially strengthen the Yen, altering the monetary policy divergence between the US Dollar and the Japanese Yen.

XAGUSD – Analyzing Silver Price Trends: Focus on US CPI Release

Silver, renowned as a safe-haven asset, is subject to significant market scrutiny, with its price movements closely tied to fundamental factors. This analysis focuses on the fundamental aspects driving recent trends in the silver market, particularly in anticipation of the forthcoming release of the US January Consumer Price Index data.

XAGUSD is moving in Descending channel and market has reached lower high area of the channel

Importance of US January CPI Release:

Traders eagerly await the US January CPI data, slated for release on Tuesday, recognizing its pivotal role in shaping market sentiment.

The CPI serves as a critical gauge of inflationary pressures, with a potential decline signaling a case for Federal Reserve rate cuts. Such expectations can significantly impact silver prices, as investors seek refuge in precious metals amid economic uncertainties.

Potential Impact on Silver Prices:

The anticipation of rate cuts driven by declining inflation has the potential to bolster silver prices. Investors perceive silver as a hedge against inflation, making it a favored asset in times of monetary easing.

Currently, the XAG/USD pair trades around $22.80, having registered a gain of 0.82% for the day. This reflects market optimism surrounding the potential implications of the impending CPI release.

Factors Driving Market Sentiment:

Geopolitical tensions, economic data releases, and monetary policy decisions are among the key factors shaping sentiment in the silver market.

Geopolitical uncertainties, such as conflicts or trade disputes, often heighten demand for safe-haven assets like silver, exerting upward pressure on prices.

Economic indicators, particularly the CPI data, play a crucial role in guiding investor expectations. A lower-than-expected CPI reading could heighten expectations of monetary stimulus, bolstering silver prices.

Considerations for Traders:

Traders must closely monitor fundamental factors, including economic data releases and geopolitical developments, to gauge silver market dynamics accurately.

The US January CPI release presents a significant event for traders, offering insights into inflation trends and potential monetary policy responses.

Understanding market sentiment and interpreting economic indicators are vital for making informed trading decisions in the silver market.

USDCHF – Decline Amidst Weak US Dollar and Fed Commentary

USDCHF is moving in box pattern and market has reached resistance area of the pattern

The USDCHF pair experiences a decline as the US Dollar faces challenges against subdued US yields.

Lorie Logan, a Federal Reserve official, emphasizes the necessity of gathering further evidence to confirm progress in inflation, adding to the cautious sentiment surrounding the US Dollar.

Factors Contributing to USD/CHF Decline

– US Dollar Weakness: Despite hawkish remarks from some Fed officials, the US Dollar encounters downward pressure due to prevailing risk-on sentiment in the market.

– Fed’s No Urgency for Rate Cuts: Dallas Fed President Lorie Logan suggests no immediate need for rate cuts, stressing the importance of confirming the sustainability of inflation progress.

– Declining US Treasury Yields: The US Dollar faces headwinds as US Treasury yields decline, reflected in the slide of the US Dollar Index (DXY) to around 104.00. Notably, 2-year and 10-year US yields hover at 4.47% and 4.16%, respectively.

Market Focus on CPI Data Release

– Anticipation for CPI Data: Market attention is directed towards the forthcoming release of Consumer Price Index (CPI) data on Tuesday.

– Expected CPI Figures: Analysts anticipate a decrease in January’s year-on-year CPI to 3.0%, down from December’s 3.4%, with the monthly CPI expected to ease to 0.2% from the previous reading of 0.3%.

Swiss Economic Indicators and SNB Policy

– Swiss Unemployment Rates: In January, the non-seasonally adjusted Swiss Unemployment Rate (year-on-year) rose, while the seasonally adjusted rate remained stable.

– SNB Monetary Policy: The Swiss National Bank (SNB) opts to maintain its key interest rate at 1.75%, signaling the conclusion of its recent tightening cycle.

Anticipation of SNB Actions and CPI Data

– Swiss CPI Release: Market participants eagerly await the release of Swiss Consumer Price Index (CPI) data for January.

– Projected Inflation Figures: Projections suggest headline Swiss inflation could grow by 1.6%, lower than the previous growth of 1.7%.

– Market Expectations on SNB: Analysts widely anticipate that the SNB might initiate its first rate cut in September 2024, indicating market anticipation of potential monetary policy adjustments.

USDCAD – Stability Amid Oil Price Fluctuations and CPI Anticipation

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

USDCAD Sideways Movement:

USDCAD remains relatively stable during the quiet Asian trading session on Monday, suggesting a lack of significant directional momentum in the currency pair.

Impact of Declining WTI Prices:

The decrease in the price of West Texas Intermediate (WTI) crude oil could exert downward pressure on the Canadian Dollar (CAD). Canada’s status as a major oil exporter to the US makes its currency sensitive to fluctuations in oil prices.

US CPI Projections:

Analysts anticipate a potential decline in the US Consumer Price Index (CPI) for January, with year-on-year (YoY) and month-on-month (MoM) figures expected to decrease to 3.0% and 0.2%, respectively.

Market Dynamics on Monday:

USD/CAD maintains a sideways trajectory on Monday, following a period of volatility in the previous session. The decline in crude oil prices likely contributed to pressure on the Canadian Dollar.

Impact of Crude Oil Price Decline:

Crude oil prices, represented by West Texas Intermediate (WTI), experienced a slight dip, halting a five-day winning streak. This decline followed the conclusion of hostilities in Gaza’s southern city of Rafah, easing concerns about potential disruptions to oil supply in the Red Sea region.

Reaction to Canadian Employment Data:

On Friday, USD/CAD faced downward pressure after the release of mixed Canadian employment data. However, sentiment shifted as traders adjusted their positions in response to adjustments made by the US Bureau of Labor Statistics (BLS) to the calculation of the CPI, resulting in minor changes to inflation projections.

Canadian Employment Figures:

The Canadian Unemployment Rate unexpectedly decreased to 5.7% in January, surpassing market expectations. Additionally, the Net Change in Employment exceeded forecasts, rising to 37.3K. However, Average Hourly Wages (YoY) grew at a slower rate of 5.3% compared to the previous period.

Market Sentiment Impacting USD:

The US Dollar experiences downward pressure, influenced by a prevailing risk-on sentiment in the market. This sentiment intensifies ahead of the release of the CPI data, scheduled for Tuesday.

Anticipated US CPI Figures:

Analysts expect a decrease in January’s CPI (YoY) to 3.0% from December’s 3.4%, with the monthly CPI data anticipated to ease to 0.2% from the previous 0.3%.

EURGBP – Market Focus: BoE Guidance, ECB Precedence, and UK Employment Data

EURGBP is moving in box pattern and market has reached support area of the pattern

BoE’s Interest Rate Guidance:

BoE Governor Andrew Bailey is poised to offer fresh insights into the Bank of England’s stance on interest rates, a pivotal factor influencing market sentiment and currency movements.

ECB Precedence in Rate Adjustments:

Market analysts speculate that the European Central Bank (ECB) may opt to ease key rates before the Bank of England (BoE), potentially impacting currency crosses and relative strength between the Euro and the Pound Sterling.

Anticipation for UK Employment Data:

Investors are on edge awaiting the release of United Kingdom employment data for the three-month period ending December, scheduled for publication on Tuesday. This data is expected to significantly influence market dynamics and investor sentiment.

Forecasted Employment Metrics:

Projections suggest a potential decrease in the Unemployment Rate to 4.0% from the previous 4.2%, alongside a moderation in Average Earnings (Excluding bonuses) growth to 6.0% from the prior reading of 6.6%. These figures will likely shape expectations regarding potential rate adjustments by the BoE.

Market Focus on BoE Governor’s Speech:

Today’s session places significant emphasis on the speech by BoE Governor Andrew Bailey, who is expected to provide crucial cues regarding the Bank of England’s upcoming monetary policy actions, particularly in anticipation of March’s policy meeting.

Pound Sterling Volatility:

The Pound Sterling is anticipated to experience heightened volatility, especially with the impending release of additional economic data, including inflation, factory output, and retail sales figures, following the publication of Tuesday’s employment data.

Euro’s Weakness Against Pound Sterling:

Despite the Pound Sterling’s own uncertainties, the Euro struggles against it due to market expectations favoring the ECB initiating rate cuts before the BoE. This sentiment is fueled by declining price pressures in the Eurozone.

ECB President’s Remarks:

ECB President Christine Lagarde’s remarks signal a potential consideration of rate cuts by the ECB in late Spring, contingent upon achieving sustained inflation levels aligned with the central bank’s 2% target. These comments contribute to the prevailing market sentiment regarding the Euro’s performance relative to the Pound Sterling.

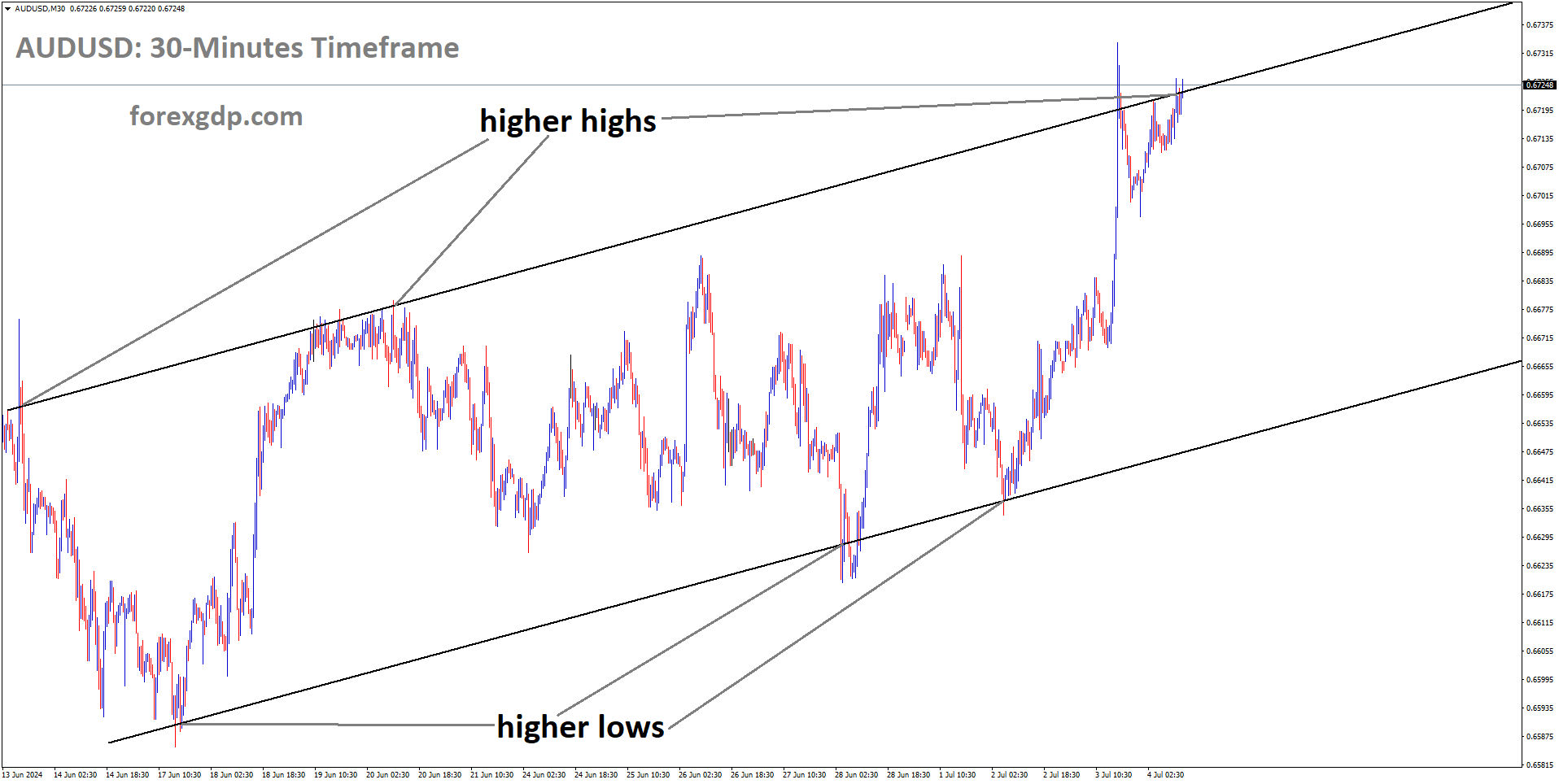

AUDUSD – Factors Influencing AUDUSD Pair Amidst Lunar New Year Holidays and CPI Data

AUDUSD is moving in Descending channel and market has fallen from the lower high area of the channel

– AUDUSD pair starts the week on the defensive during early Asian trading hours, with Chinese markets closed for Lunar New Year holidays.

– Traders in Asia focus on overall risk sentiment amidst the quiet market conditions.

– Attention turns to upcoming US Consumer Price Index (CPI) data for January later in the week.

– Revised CPI figures for December showed a 0.2% rise from the previous month, revised down from the initial estimate of 0.3%, as reported by the Bureau of Labor Statistics.

– December 2022 inflation reportedly increased, contrary to earlier expectations of a decrease.

– Federal Reserve (Fed) officials stress the need for further evidence of progress on inflation before considering rate cuts.

– January CPI data, due on Tuesday, is anticipated to show a 0.2% month-on-month (MoM) increase and a 3.0% year-on-year (YoY) rise.

– Core CPI, excluding volatile food and energy prices, is forecasted to rise by 0.3% MoM and 3.8% YoY.

– Fed Funds futures reflect a decrease in priced-in rate cuts for 2024, down to 107 basis points (bps) from 158 bps a month prior.

– The Reserve Bank of Australia (RBA) presents a more hawkish stance than expected, with Governor Michele Bullock stating the board hasn’t ruled out further interest rate hikes but hasn’t confirmed them either.

– Concerns about deflation in China contribute to market sentiment, potentially weighing on the Australian Dollar (AUD) and acting as a headwind for AUD/USD.

– Trading volume is expected to remain light due to Lunar New Year holidays, influencing market activity.

– Alongside the CPI data release, investors will closely monitor speeches from multiple Fed speakers throughout the week for insights into future monetary policy decisions.

– These events are anticipated to provide clearer direction for the AUD/USD pair amidst prevailing market conditions.

NZDUSD – RBNZ Outlook and Market Dynamics: NZDUSD Trends and Policy Insights

NZDUSD is moving in Ascending channel and market has reached higher low area of the channel

– NZDUSD experiences a decline as RBNZ OIS rates retract from Friday’s post-ANZ forecast firming.

– ANZ predicts RBNZ to raise cash rates by a quarter point in February and April, projecting them to reach 6.0% amid elevated cost pressures.

– RBNZ Governor Adrian Orr underscores persistent inflation concerns during his testimony before the Finance and Expenditure Committee.

– Despite subdued USD, NZD/USD pair faces downward pressure due to RBNZ OIS rates retracement.

– RBNZ’s first policy meeting of the year is scheduled for the month’s end, with expectations of addressing the ongoing inflationary pressures.

– Orr maintains RBNZ’s cash rate at 5.5%, citing elevated inflation levels.

– RBNZ Deputy Governor Christian Hawkesby highlights the robustness of New Zealand’s financial system during his testimony, noting stable house prices and resilience to high-interest rates.

– New Zealand Finance Minister Nicola Willis announces the government budget announcement for May 30th.

– USD Index declines, reflecting market risk-on sentiment, especially ahead of the upcoming release of CPI data.

– Analysts anticipate a moderation in January’s CPI to 3.0% YoY and a monthly decline to 0.2%.

– Dallas Fed Bank President Lorie Logan states no immediate need to lower interest rates, emphasizing the necessity for further evidence to ensure sustained progress in curbing inflation.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/