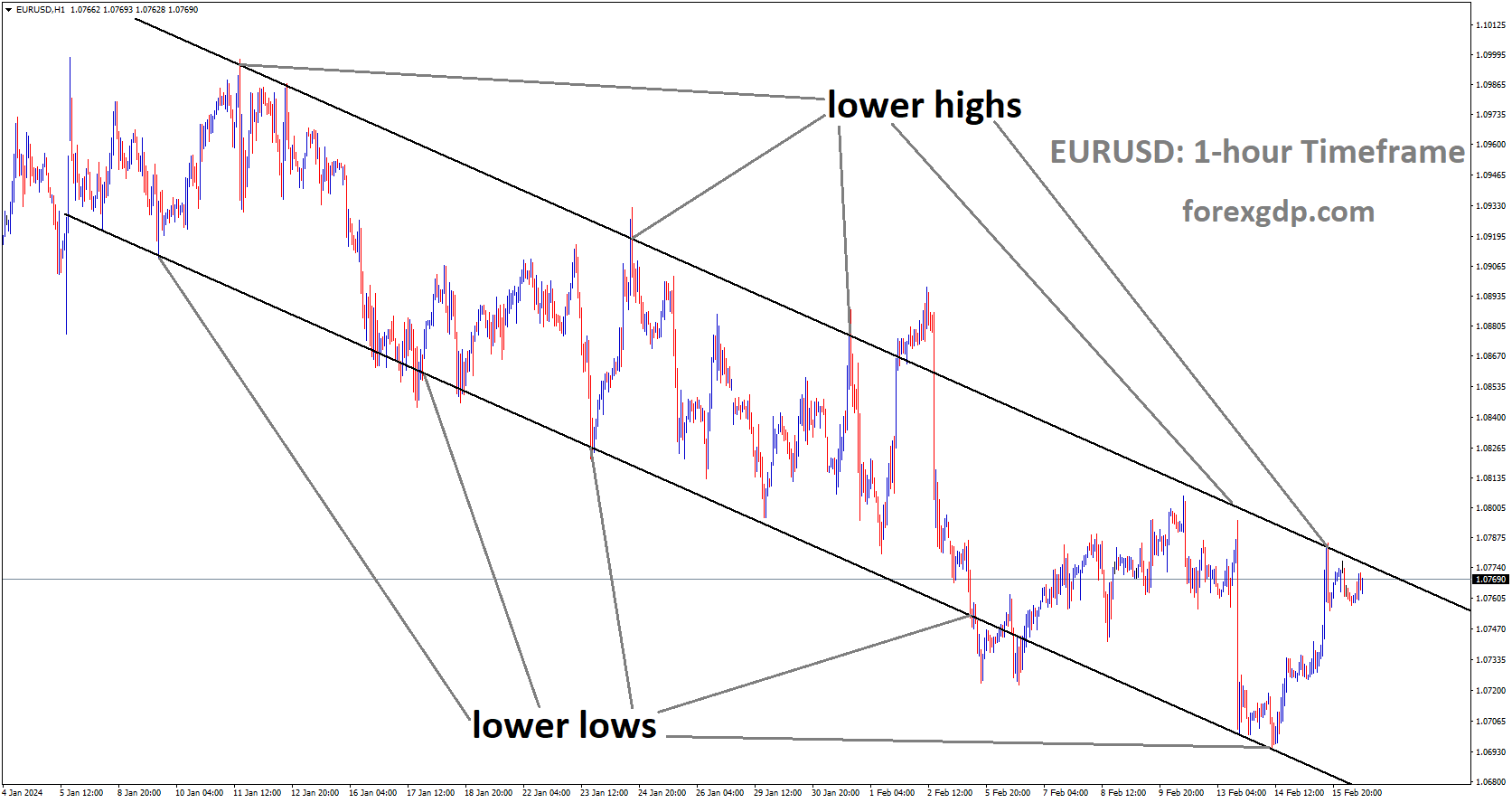

EURUSD is moving in Descending channel and market has reached lower high area of the channel

EURUSD – Dynamics and Market Outlook

EUR/USD Retreats Amidst Strengthening US Dollar: The EUR/USD currency pair experiences a decline as the US Dollar shows signs of improvement, driven by an overall optimistic market sentiment.

Anticipation of Key US Economic Data Releases: Market participants await the release of crucial US economic indicators, including the Producer Price Index and the Michigan Consumer Sentiment Index, scheduled for Friday. These releases are expected to significantly influence market sentiment and currency movements.

Disappointing US Retail Sales Figures: In January, US Retail Sales recorded a notable decline of 0.8% month-over-month, falling far short of the projected 0.1% decrease. This unexpected contraction contributes to the retreat observed in the EUR/USD exchange rate.

Insights from ECB’s Wage Tracker: The European Central Bank provides insights into potential wage pressures through its forward-looking wage tracker, indicating a possible impact on future economic dynamics following stable Gross Domestic Product data.

Market Optimism Supports USD: Despite the disappointing US Retail Sales data, the US Dollar receives support from prevailing market optimism, particularly ahead of key economic data releases. Additionally, improved US yields contribute to the USD’s strength against the Euro.

USD Resilience Amid Rate Cut Speculations: The US Dollar Index maintains stability amidst speculations suggesting that the Federal Reserve may opt to refrain from implementing rate cuts in the upcoming months. However, the probability of a 25 basis points rate cut in June stands at 52%, according to the FedWatch Tool.

Challenges and Support for the USD: While weaker-than-expected US Retail Sales initially posed challenges for the USD, the currency finds some support from reduced Initial Jobless Claims, indicating a potential balancing effect on market sentiment.

Detailed Analysis of US Retail Sales Decline: The sharp decline of 0.8% in US Retail Sales for January comes as a surprise, significantly deviating from market expectations. Moreover, the Retail Sales Control Group witnesses a notable decline of 0.4%, contrasting with previous positive growth trends.

Fed’s Inflation Outlook and Potential Impact: Federal Reserve Bank of Atlanta President Raphael W. Bostic provides insights into the Fed’s inflation outlook, cautioning about potential hurdles in curbing inflation. Bostic suggests that a faster-than-anticipated moderation in inflation could prompt a reassessment of the central bank’s interest rate policies.

Remarks from ECB President Christine Lagarde: ECB President Christine Lagarde acknowledges ongoing challenges in the Eurozone economy, emphasizing the critical role of confidence-building measures in achieving the ECB’s inflation target amidst persistent disinflationary trends.

GOLD – Factors Influencing Gold Prices and USD Dynamics

Bond Yields and USD Support: The increase in US bond yields provides a foundation for the strength of the US Dollar, a trend that simultaneously acts as a constraint on gold’s upward movement. This dynamic is particularly notable amidst a prevailing positive risk sentiment.

Fed Rate Cut Speculation and Geopolitical Factors: Heightened speculation surrounding an early rate cut by the Federal Reserve, coupled with ongoing geopolitical tensions, offers considerable backing to gold. Investors tend to flock towards gold as a safe-haven asset during periods of uncertainty.

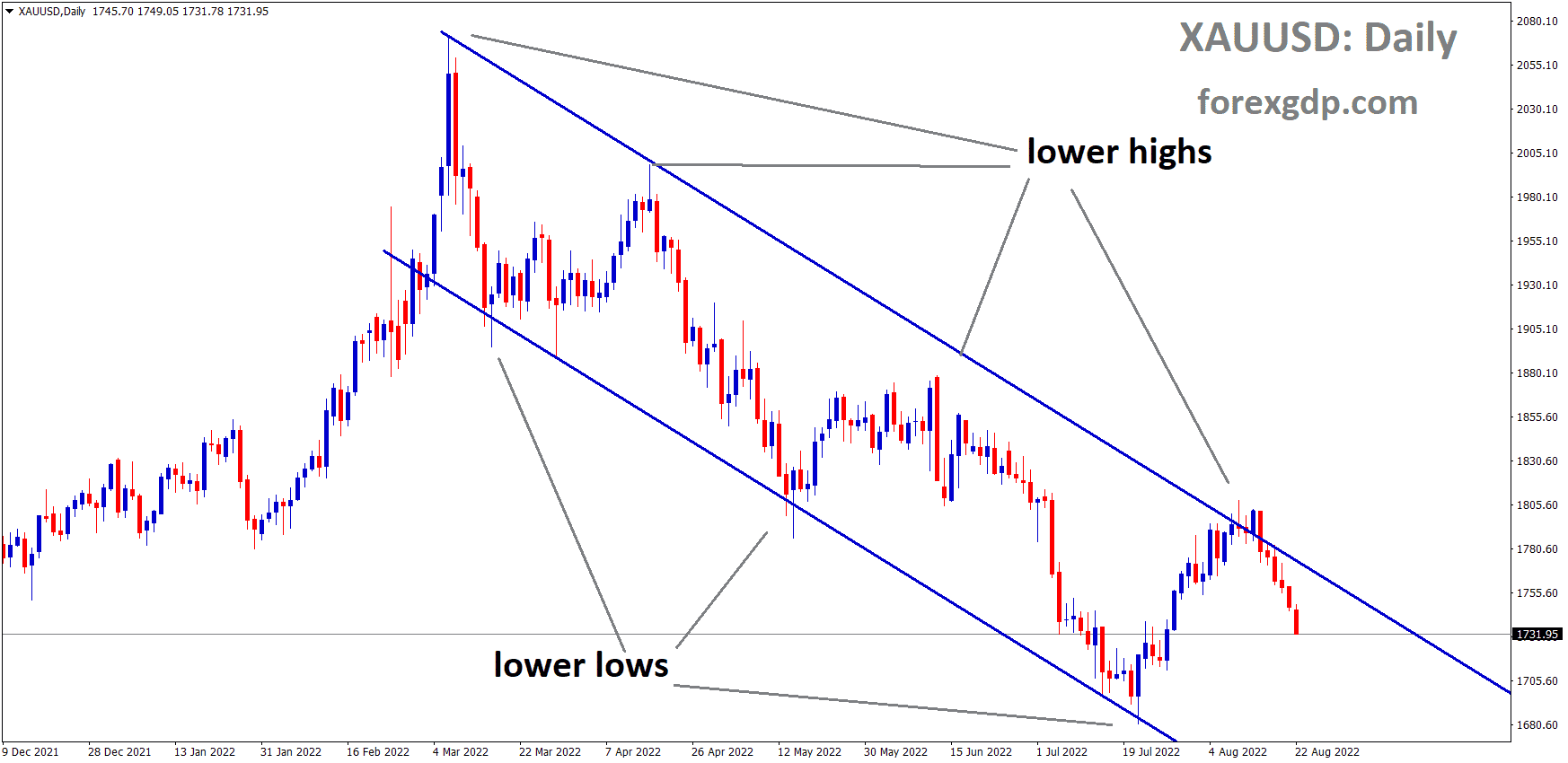

XAUUSD is moving in Descending channel and market has rebounded from the lower low area of the channel

USD Behavior and Equity Market Influence: Following a minor uptick in US Treasury bond yields, the USD attracts some buyer interest, momentarily halting its recent decline from a three-month peak. This stabilization in the USD also serves to limit potential gains for gold. Additionally, the overall positive sentiment in equity markets contributes to suppressing any significant increases in the value of gold.

Gold’s Resilience Amidst Downside Pressure: Despite facing downward pressure, gold finds support in the anticipation of forthcoming interest rate cuts by the Federal Reserve, reinforced by disappointing US Retail Sales figures. This expectation acts as a deterrent for aggressive USD betting, alongside geopolitical uncertainties emanating from conflicts in the Middle East, thus mitigating losses for gold. Market participants are eagerly awaiting the release of key US macroeconomic indicators, such as the Producer Price Index, Housing Starts, and Michigan Consumer Sentiment Index.

Impact of Economic Data and FOMC Commentary: The impending release of economic data and speeches by influential Federal Open Market Committee members is expected to steer USD demand and provide a fresh impetus to gold prices. Traders remain vigilant, monitoring broader risk sentiment for short-term trading opportunities within the gold market. Nevertheless, the XAU/USD pair is anticipated to sustain losses for the second consecutive week, with market attention shifting towards the forthcoming release of FOMC meeting minutes and global Purchasing Managers’ Index figures.

Complex Market Dynamics: Gold faces challenges in capitalizing on its recent modest recovery due to a blend of conflicting factors. The yield on the 10-year US government bond remains above 4.0%, sparking renewed demand for the USD and restraining upward momentum for XAU/USD. Furthermore, Thursday’s disappointing US economic data fuels expectations for an earlier-than-anticipated rate cut by the Federal Reserve, thereby dampening investor appetite for safe-haven assets such as gold.

Market Sentiment and Monetary Policy Outlook: Speculative bets on a 25 basis points rate cut in May surged to 40%, while those for June stood at 80%, following the release of weaker-than-expected US Retail Sales data. The Commerce Department reported a substantial 0.8% decline in January’s Retail Sales, with auto sales excluding autos down by 0.6% in the same month. Additionally, import prices witnessed their most significant increase in nearly two years, rising by 0.8% in January, although the yearly rate fell by 1.3%. Concurrently, Jobless Claims experienced a decline, reaching a one-month low of 212K by the week ending February 10th.

Fed’s Monetary Policy Stance: Atlanta Fed President Bostic remarked on Thursday regarding the central bank’s progress in curbing inflation and hinted at potential rate cuts in the near future. Nevertheless, he stressed the importance of patience in adjusting monetary policy, citing a robust economy and downplaying the urgency for rate cuts.

XAGUSD is moving in Descending channel and market has reached lower high area of the channel

Geopolitical Unrest and Market Focus: The Israeli military’s airstrikes in Lebanon have heightened geopolitical tensions, adding another layer of uncertainty for traders. Market participants are now eagerly awaiting cues from the US Producer Price Index to evaluate the Federal Reserve’s future policy trajectory and its potential ramifications for gold prices.

Upcoming Economic Releases and FOMC Communications: Friday’s economic agenda includes the release of Housing Starts and the Preliminary Michigan Consumer Sentiment Index for February. These events, coupled with speeches by influential FOMC members, are poised to drive USD demand and present short-term trading opportunities within the gold market.

USDJPY – USD’s Downward Correction Amid Mixed Data and Central Bank Updates

USD Continues Downward Correction:

The US Dollar experienced a further decline in value, continuing its downward correction.

On Thursday, the USD Index dropped by 0.4% compared to the previous day’s performance.

USDJPY is moving in Ascending channel and market has reached higher low area of the channel

Mixed Data Releases Impact USD:

The decline in the USD was influenced by mixed data releases.

Despite some positive economic indicators, the overall sentiment weighed on the USD.

Focus Shifts to Economic Indicators:

Attention shifted towards the January Producer Price Index data, expected to provide insights into inflationary pressures.

Investors closely monitored these indicators to gauge the health of the US economy.

Upcoming Consumer Sentiment Index Release:

Later in the American session, the University of Michigan was set to release the preliminary Consumer Sentiment Index for February.

This data release was anticipated to offer further clues regarding consumer confidence and spending patterns.

Retail Sales Decline Reported:

The US Census Bureau reported a decline of 0.8% in Retail Sales for January.

This negative figure suggested a potential slowdown in consumer spending, contributing to the USD’s downward trend.

Positive News on Jobless Claims:

Despite the decline in Retail Sales, there was a positive aspect with weekly Initial Jobless Claims decreasing to 212,000 for the week ending February 10.

This decrease indicated a strengthening labor market, which could have counteracted some of the negative sentiment surrounding the USD.

Impact on Bond Yields and Stock Market:

The benchmark 10-year US Treasury bond yield retreated to around 4.2%.

Wall Street’s main indexes experienced modest gains following the data release.

These movements in bond yields and stock market performance influenced the USD’s ability to gain strength.

European Market and Futures Trading:

In the European morning, the 10-year yield remained in positive territory, hovering near 4.25%.

US stock index futures were trading mixed, indicating uncertainty in investor sentiment.

Bank of Japan’s Stance:

Bank of Japan Governor Kazuo Ueda announced that they would assess whether to maintain various easing measures, including the negative interest rate.

The decision would depend on achieving a sustained and stable target for inflation.

Ueda refrained from commenting on short-term fluctuations in forex markets, keeping the focus on long-term policy objectives.

Stabilization of USD/JPY Pair:

Following two consecutive days of negative performance, the USD/Japanese Yen currency pair stabilized and even edged higher during Asian trading hours.

This stabilization could indicate a temporary pause in the USD’s decline against the Japanese Yen.

NZDUSD – Inflation Targeting Efforts by RBNZ Governor Orr

RBNZ Governor’s Inflation Remarks:

Reserve Bank of New Zealand Governor Adrian Orr restated on Friday the ongoing efforts needed to anchor inflation expectations to the 2% target.

Emphasizing the importance of bringing core inflation within the 1-2% target band, Orr highlighted this as a crucial step towards achieving the overall 2% inflation target.

NZDUSD is moving in box pattern and market has rebounded from the support area of the pattern

Market Reaction to Orr’s Comments:

Despite Orr’s remarks, the NZD/USD currency pair largely disregarded these statements.

NZD/USD exhibited marginal downward movement on the day, suggesting that the market response to Orr’s comments was muted or neutral.

RBNZ’s Inflation Anchoring Efforts:

Orr’s repetition of the need for further action underscores the RBNZ’s commitment to its inflation targeting framework.

The central bank’s proactive stance reflects its determination to stabilize inflation expectations within the target range, a key objective of monetary policy.

Importance of Core Inflation:

Orr’s emphasis on bringing core inflation within the target band highlights its significance in achieving the broader inflation target.

Core inflation, which excludes volatile components like food and energy prices, provides a more stable measure of underlying inflationary pressures.

Market Sentiment and NZD/USD Movement:

Despite the RBNZ Governor’s statements, market sentiment towards the NZD/USD pair remained relatively unchanged.

The marginal decline in NZD/USD suggests that other factors may have been influencing currency movements on that particular day, potentially overshadowing Orr’s comments.

Ongoing Policy Focus:

Orr’s reaffirmation of the RBNZ’s commitment to inflation targeting underscores the central bank’s ongoing policy focus.

The RBNZ’s efforts to stabilize inflation expectations are crucial for maintaining price stability and supporting sustainable economic growth.

Future Implications:

Orr’s comments may have implications for future monetary policy decisions by the RBNZ.

Market participants will continue to monitor central bank communications and economic data releases for insights into the direction of monetary policy and its potential impact on currency markets.

USDCAD – Retail Sales Impact and Oil Price Influence

USD/CAD Strengthens Amid Risk Aversion:

USD/CAD shows upward movement as the US Dollar gains strength due to risk aversion sentiments in the market. This appreciation of the USD contributes to the pair’s advance against the Canadian Dollar.

USDCAD is moving in Ascending channel and market has reached higher low area of the channel

Upcoming US Economic Data Releases:

Market attention is focused on the release of US Producer Price Index data and the Consumer Sentiment Index scheduled for Friday.

These data releases are anticipated to provide insights into inflationary pressures and consumer sentiment, influencing market sentiment and currency movements.

Disappointing US Retail Sales Data:

US Retail Sales for January experienced a significant decline of 0.8% month-on-month, contrary to the expected decrease of 0.1%.

This unexpected decline in retail sales exerts downward pressure on the USD/CAD pair, leading to extended losses following the data release.

WTI Price Decline Affects CAD:

Lower West Texas Intermediate oil prices contribute to downward pressure on the Canadian Dollar.

Canada, being a major oil exporter to the US, experiences currency depreciation as falling oil prices impact its economy.

USD/CAD Rebounds Despite Retail Sales Data:

USD/CAD reverses a two-day losing streak, approaching levels near 1.3480 during Asian trading hours on Friday.

The USD receives support against the CAD amid risk aversion sentiments, despite losses incurred after disappointing US Retail Sales data release.

Impact of Initial Jobless Claims:

USD receives support from lower-than-expected Initial Jobless Claims, which reported 212,000 unemployment claims for the week ending February 9.

This better-than-expected jobless claims figure contributes to stabilizing the USD against the CAD.

Crude Oil Price Decline Weakens CAD:

The decline in crude oil prices negatively affects the Canadian Dollar due to Canada’s significant reliance on oil exports.

Concerns about demand outlook in the US arise following a larger-than-anticipated increase in US Crude Oil Stockpiles, leading to the decline in West Texas Intermediate oil prices.

Canadian Economic Data Highlights:

In absence of high-impact data from Canada, recent figures include seasonally adjusted Housing Starts settling at 223.6K in January, below expectations.

Additionally, Manufacturing Sales declined by 0.7% month-over-month in December, indicating a downturn in manufacturing activity.

Investors await investment and Wholesale Sales data from Statistics Canada on Friday, which could provide further insights into the Canadian economy.

EURGBP- UK Retail Sales Surpass Expectations Amid Economic Concerns

Strong UK Retail Sales for January:

UK retail sales for January surpassed expectations, registering a month-on-month growth of 3.4%.

This robust performance comes in contrast to softer-than-expected GDP numbers reported earlier in the week, which led to the British economy entering a recession in late 2023.

EURGBP is moving in box pattern and market has rebounded from the support area of the pattern

Limited Impact on BoE Policy Outlook:

Despite the significant retail sales figures, the implications for the Bank of England’s policy outlook are not profound.

The central bank’s focus remains primarily on inflation, particularly within the services sector, and wage growth.

It is unlikely that the BoE will adopt a significantly more hawkish stance solely based on softer economic growth without assurances regarding inflation.

Market Response and Pound’s Behavior:

The Pound Sterling’s reaction reflects this narrative, with only modest declines observed following the release of GDP numbers.

Furthermore, the Pound saw a slight uptick in trading following the strong retail sales data.

This indicates a cautious approach by investors, as they await further developments in monetary policy and economic indicators.

Expectations for Stabilization and Rebound in EUR/GBP:

Despite the current fluctuations, there are expectations for a stabilization followed by a potential rebound in the EUR/GBP currency pair.

This projection is based on the perceived mispricing of monetary policy in both the UK and the Eurozone.

Investors anticipate a correction in the exchange rate as policy adjustments are made and economic conditions evolve in both regions.

GBPUSD – Reacts to US Retail Sales and UK Recession News

GBP/USD Rebounds Following Soft US Retail Sales:

Despite initially trading at daily lows, the GBP/USD pair staged a recovery, registering a 0.17% increase.

This upward movement was triggered by the release of a US retail sales report showing weaker-than-expected figures.

GBPUSD is moving in Descending channel and market has rebounded from the lower low area of the channel

UK Enters Recession as GDP Contracts:

Official data confirmed that the UK economy had entered a recession, with GDP shrinking during the final quarter of 2023.

The contraction in GDP by 0.3% highlighted the economic downturn faced by the UK.

BoE Governors Signal Potential Interest Rate Adjustments:

Bank of England Governors hinted at the possibility of adjusting interest rates in response to economic conditions.

Megan Greene, known for her hawkish stance, suggested that interest rates might need to be higher, depending on indicators such as wage growth.

Catherine Mann expressed cautious optimism about the economic outlook for 2024 and emphasized the importance of monitoring indicators like the Purchasing Managers Index.

GBP Strengthens Amid Weak US Retail Sales:

The Pound Sterling exhibited strength during the North American trading session, supported by disappointing US retail sales data.

Retail sales in the US for January experienced a significant decline of 0.8% month-on-month, falling below market expectations.

Factors contributing to this decline included reduced sales at auto dealerships and gasoline service stations, compounded by adverse weather conditions.

Mixed Bag of US Economic Data:

US economic data released during the period presented a mixed picture.

While retail sales figures disappointed, there was a slight increase in unemployment claims for the week ending February 10, which came in lower than anticipated.

Despite expectations of a rebound in claims following recent layoffs, the actual numbers were more favorable than forecasted.

Confirmation of UK Recession:

The contraction in GDP by 0.3% during the last quarter of 2023 officially marked the UK’s entry into a recessionary phase.

This economic downturn underscored the challenges facing the UK economy, necessitating careful policy considerations by authorities.

Insights into BoE Monetary Policy:

BoE Governors provided insights into potential monetary policy adjustments based on evolving economic conditions.

Megan Greene’s remarks hinted at a possible need for higher interest rates, contingent upon specific economic indicators.

Catherine Mann’s comments suggested a more nuanced approach, focusing on future economic prospects and the importance of monitoring leading indicators.

Market Expectations for Central Bank Actions:

Market sentiment indicated expectations of a rate cut by the Federal Reserve in June, with a probability of around 51%.

Additionally, there were speculations of a 50 basis points rate cut by the Fed, reflecting concerns about economic conditions.

Meanwhile, the Bank of England was expected to implement a more modest 25 basis points rate cut in its August meeting, highlighting differences in monetary policy approaches between the two central banks.

GBPJPY – UK Data Releases and BoJ Assessment

GBP/JPY Prepares for UK Data Releases:

GBP/JPY shows signs of strength ahead of a series of data releases from the United Kingdom.

Market participants anticipate significant movements in the currency pair in response to the incoming data.

GBPJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

Expectations for UK Retail Sales Improvement:

UK Retail Sales are forecasted to rebound to 1.5% after experiencing a notable 3.2% decrease in the previous period.

This anticipated improvement in retail sales could potentially bolster the Pound Sterling against the Japanese Yen.

BoJ Governor’s Assessment of Monetary Conditions:

Bank of Japan Governor Kazuo Ueda anticipates that monetary conditions in Japan have remained accommodative.

Ueda’s remarks suggest that the BoJ’s monetary policy stance is likely to persist, even amid discussions about rolling back stimulus measures.

GBP/JPY Receives Upward Support:

GBP/JPY benefits from optimistic expectations surrounding the release of UK Retail Sales data.

Investors show confidence in the potential for positive economic indicators from the UK, supporting the GBP/JPY exchange rate.

Challenges Faced by GBP/JPY:

Despite the positive sentiment, GBP/JPY encounters challenges as the Japanese Yen gains strength.

Remarks from Japan’s top officials hinting at potential intervention in the Forex market contribute to the JPY’s appreciation.

Additionally, escalated geopolitical tensions in the Middle East increase demand for the safe-haven JPY, exerting downward pressure on GBP/JPY.

BoJ’s Monetary Policy Outlook:

BoJ Governor Kazuo Ueda underscores that the specific measures for rolling back stimulus will depend on prevailing economic conditions.

Even as discussions about ending negative interest rates continue, Ueda indicates that monetary conditions in Japan will remain supportive.

UK Economy Enters Technical Recession:

The United Kingdom officially enters a technical recession as its economy contracts for two consecutive quarters.

This downturn is highlighted by a decline of 0.3% in quarterly Gross Domestic Product growth, along with a surprising 0.2% year-on-year contraction against expected growth.

BoE Policy Outlook:

Bank of England policymaker Catharine L. Mann emphasizes the need for additional inflation data before determining the central bank’s next policy steps.

This cautious approach suggests that the BoE is closely monitoring economic indicators before making any further policy adjustments.

AUDUSD – AUD vs. USD and Economic Data Insights

AUD Faces Pressure Against USD Stability:

The Australian Dollar struggles against a stable US Dollar as it attempts to recover from intraday losses on Monday.

Despite its efforts, the AUD faces headwinds as the USD gains ground, supported by improved US Treasury yields.

AUDUSD is moving in Ascending channel and market has rebounded from the higher low area of the channel

RBA Likely to Maintain Interest Rates:

Australia’s employment data suggests that the Reserve Bank of Australia is unlikely to raise interest rates in its March meeting.

Modest growth in the Australian economy, coupled with ongoing labor market challenges and subdued inflationary pressures, contribute to this expectation.

Market Optimism Boosts S&P/ASX 200:

The S&P/ASX 200 index in Australia sees improvement following a surge in Wall Street, driven by market optimism.

Investor sentiment remains positive, particularly ahead of key economic data releases such as the US Producer Price Index and Michigan Consumer Sentiment Index.

USD Holds Firm Amid Rate Cut Postponement Speculation:

The US Dollar maintains its stability, supported by market sentiment indicating potential postponement of interest rate cuts by the US Federal Reserve in upcoming meetings.

Expectations suggest the Fed might delay rate cuts until June, with a probability of 53%, as per the FedWatch Tool.

Mixed Australian Employment Data:

Australia’s employment data for January presents a mixed picture:

Employment Change falls short of expectations at 0.5K compared to the anticipated 30K.

Part-Time Employment declines to 10.6K from the previous 46.7K.

Full-Time Employment shows improvement to 11.1K from a prior decline.

Participation Rate remains steady at 66.8%, slightly lower than anticipated.

Consumer Inflation Expectations remain unchanged at 4.5% for February.

RBA Governor’s Assessment:

RBA Governor Michele Bullock provides insights during her address to the Australian parliament’s Senate Economics Legislation Committee.

She acknowledges global economic resilience but remains vigilant about potential challenges, expressing confidence in managing inflation within a reasonable timeframe.

US Retail Sales Disappoint:

US Retail Sales data for January disappoints, showing a decline of 0.8% month-on-month against the expected decrease of 0.1%.

The Retail Sales Control Group also decreases by 0.4%, contrasting with the previous increase.

Jobless Claims and Industrial Production Data:

US Initial Jobless Claims for the week ending February 9 report 212,000 claims, slightly lower than market expectations.

January’s Industrial Production contracts by 0.1%, deviating from the anticipated improvement of 0.3%.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/