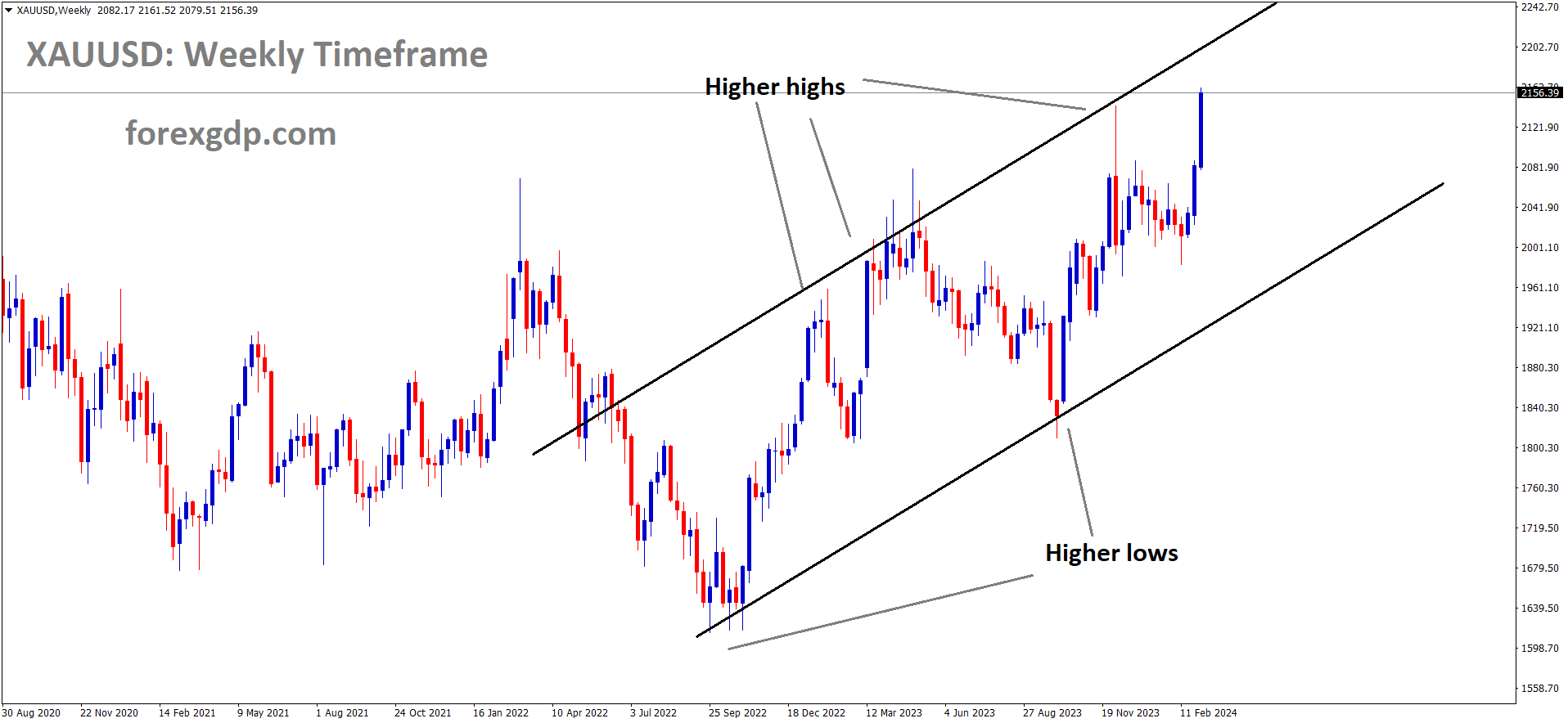

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

GOLD – Hovers Around $2,150 amid Declining US Yields, Fed Powell’s Remarks

Gold prices are moved higher after the FED Powell testimony outcome is unfavourable for US Dollar, FED Powell commented US is going to recession period in some time, then inflation will be falling down to 2% target, then rate cuts will be done in the market. The data dependent approach will be used in the current situation.

As of my last knowledge update in January 2022, Hamas is generally considered a Palestinian militant group and political organization. The designation of groups may vary depending on the perspective of different governments and entities. It’s important to note that geopolitical situations can evolve, and designations may change over time. For the latest and most accurate information, I recommend checking with reputable news sources or official government statements.

In the daily market digest, the surge in gold prices is highlighted despite mixed US jobs data and a drop in US yields. Private companies added 140K jobs to the workforce, surpassing January’s reading of 111K but falling short of the estimated 150K, according to the ADP Employment Change report. The US Job Openings and Labor Turnover Survey (JOLTS) for January reported 8.863 million job openings, slightly below expectations and marginally lower than the previous month’s figures.

Previously released US economic data for the week showed a slight decrease in the S&P Global Services PMI to 52.3 from January’s 52.5. The Composite PMI, covering both manufacturing and service sectors, registered at 53.8, missing expectations and lower than the previous reading of 54.2. The ISM Services PMI declined to 52.6 from 53.4, falling below the anticipated consensus of 53, resulting in a negative impact on the US Dollar.

Factory orders in January experienced a larger-than-expected decline, dropping from 0.2% to -3.6% MoM. Gold prices continue to be supported by robust central bank buying in emerging markets. The near-term demand for gold is expected to be influenced by Fed Chair Jerome Powell’s testimony before Congress on Wednesday and various economic data releases in the United States later in the week.

Atlanta Fed Bank President Raphael Bostic remarked on Monday that a strong labor market and decent economic growth have given the Federal Open Market Committee (FOMC) time to decide on optimal timing for rate cuts. Bostic added that the Fed is experiencing a “rebounding success” as inflation gradually returns to the desired target without negatively impacting labor demand.

EURJPY – BoJ’s Ueda: Exit from Stimulus Possible, Aiming for 2% Inflation Target

The Bank of Japan Kazhao Ueda said it is possible to exit stimulus once 2% inflation target is achieved. We do roll back of Stimulus measures once rates are lifted. We are looking for 2% inflation target soon achieved in the market with Wages hikes to level the inflation area.

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

BoJ’s Ueda: Exit from Stimulus Feasible in Pursuit of 2% Inflation Target

BoJ Governor Kazuo Ueda stated on Thursday that it is “fully possible to seek exit from stimulus while striving to achieve a 2% inflation target.” He mentioned considering rolling back the massive stimulus program once a positive cycle of wages and inflation is confirmed, noting a gradual rise in the likelihood of achieving 2% inflation.

The extent of rate hikes, in case negative rates are lifted, would be determined by the situation at the time. Ueda emphasized that regardless of whether they abandon Yield Curve Control (YCC) or maintain it, the BoJ will continue to buy Japanese Government Bonds (JGBs) and assured that there will be no discontinuation in their monetary policy.

Following the end of negative rates, the BoJ plans to use interest paid to reserves to control short-term interest rates.

EURUSD – German Factory Orders Plunge 11.3% MoM, Missing Expectations

German Factory orders for the month of January came at -11.3% versus -6.0% decline, it is more down from 12.0% Jump in December month.

EURUSD has broken the Box pattern in upside

Germany’s Factory Orders slumped in January, the official data published by the Federal Statistics Office showed Tuesday, suggesting that the German manufacturing sector has returned to contraction.

On a monthly basis, contracts for goods ‘Made in Germany’ plunged 11.3%, as against a 12.0% jump reported in December, missing the forecasts of -6.0%

USD INDEX – USD Drops to 1-Month Lows on Weak Labor Market Data

US Dollar moved down yesterday after the Private jobs data ADP employment numbers came at 140K versus 150K growth forecasted. JOLTs Job Openings for January month came at 8.863M versus 8.9M expected and down from December number of 8.889M.

USD Index has broken the Ascending channel in downside

Daily Digest: DXY Trades Lower on Soft Labor Market Data

Recent reports, including January’s JOLTs Job Quits and Job Openings, and the ADP Employment Change for February, contribute to the current market dynamics. Fed Chair Jerome Powell, following Congressional testimony, affirmed the Fed’s stance against initiating rate cuts at the moment.

The upcoming US labor market data releases on Thursday and Friday will play a crucial role in shaping expectations regarding the timing of the Fed’s easing cycle. The prevailing consensus suggests that the first rate cut may occur in June.

Key Market Movements:

– JOLTs Job Openings for January were 8.863M, slightly below the expected 8.9M but closely aligned with December’s figure of 8.889M.

– ADP Employment Change for February reported an increase of 140K jobs, falling short of the forecasted growth of 150K.

– Powell expressed a desire for more confidence in inflation decline, suggesting that with additional data, the Fed could become more certain about initiating rate cuts.

– US Treasury bond yields continue to decrease, with the 2-year yield at 4.52%, the 5-year yield at 4.08%, and the 10-year yield at 4.09%.

– Thursday’s focus will be on weekly Jobless Claims figures, followed by Nonfarm Payroll data for February on Friday.

USDCHF – Holds above 0.8800, Focus on Swiss Unemployment Rate

The Swiss Franc down turn may be capped by Middle east tensions happened yesterday.

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

The Houthi rebels did merchant ship attack, US Agency reported atleast 3 members killed and 4 members in serious conditions after the attack happened in Gulf of Aden.

Fed Signals Potential Rate Cut; Swiss Franc Faces Mixed Influences

Federal Reserve (Fed) Chair Jerome Powell indicated to the House Financial Services Committee that he believes the US interest rate has peaked and could be lowered later this year. However, Powell emphasized the ongoing economic uncertainty. San Francisco Fed President Mary Daly noted that while Fed policy is in a good position, keeping rates high for an extended period could negatively impact the economy.

Meanwhile, Swiss CPI inflation data for February dropped to its lowest level since October 2021, fueling speculation about a potential interest rate cut by the Swiss National Bank (SNB) later this month.

Despite the potential for lower interest rates, the Swiss Franc (CHF) may find support amid escalating geopolitical tensions in the Middle East. A Houthi missile attack on a merchant ship in the Gulf of Aden resulted in casualties, potentially boosting traditional safe-haven assets like CHF and putting pressure on the USD/CHF pair.

Looking ahead, market participants will closely monitor Switzerland’s February Unemployment Rate and US weekly Initial Jobless Claims on Thursday. Additionally, the second testimony by Fed Chair Powell and a speech by the Fed’s Mester will be key events impacting trading opportunities around the USD/CHF pair.

USDCAD – Nears Weekly Low, Hovers around 1.3500 amid Slight USD Weakness

The Bank of Canada hold the interest rate at 5.00% with no change last day.The Canadian Dollar moved up after the rate hold news. US Dollar moved down after the FED Powell testimony outcome is rate cuts plans in 2024 Second half.

USDCAD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Mixed signals on the Federal Reserve’s (Fed) rate-cut path fail to assist the US Dollar (USD) to register any meaningful recovery from its lowest level since early February, which, in turn, is seen acting as a headwind for the USD/CAD pair. Fed Chair Jerome Powell told US lawmakers on Wednesday that the central bank will cut interest rates this year, though wants to see more evidence that inflation is falling to the 2% target. Minneapolis Fed President Neel Kashkari, however, downplayed speculations about more aggressive policy easing and said that he may reduce the number of cuts this year, possibly to only one in the wake of the incoming stronger US macro data.

The Canadian Dollar (CAD), on the other hand, continues to draw support from a hawkish hold from the Bank of Canada (BoC) on Wednesday. Meanwhile, subdued Crude Oil prices do little to provide any meaningful impetus to the commodity-linked Loonie. Furthermore, the yield on the benchmark 10-year US government bond rebounds from a one-month low touched on Wednesday, which, along with a generally softer tone around the equity markets, acts as a tailwind for the safe-haven buck. This, in turn, should help limit any meaningful downside for the USD/CAD pair and warrants some caution before positioning for any further depreciating move.

Moving ahead, investors now look to Fed Chair Powell’s second day of testimony before the Senate Banking Committee. Apart from this, traders will take cues from Thursday’s economic docket – featuring the US Weekly Initial Jobless Claims, and Trade Balance figures from the US and Canada. This, along with the US bond yields and the broader risk sentiment, will influence the USD demand and provide some impetus to the USD/CAD pair.

GBPUSD – Strengthens Below 1.2750 on Weak US Dollar, UK Budget

The UK Chancellor Jeremy Hunt said Pandemic, Financial Crisis, Energy Crisis happened in UK due to war in Europe. The higher rates in the market to suppress the inflation level in the economy.He said UK Economy is expected to grow by 0.80% in 2024 and 1.9% in 2025. GBP pairs moving higher against counter pairs after the speech.

GBPUSD has broken the Descending channel in upside

GBP/USD Gains on Weaker USD and Positive UK Spring Budget

The major pair experiences an upswing driven by a weakened US Dollar (USD) and favorable updates from the UK Spring Budget.

Federal Reserve (Fed) Chair Jerome Powell conveyed to House lawmakers on Wednesday that interest rates may decrease this year. However, he emphasized a cautious approach, stating that the Fed will proceed carefully until there is greater confidence in inflation sustaining toward the 2% target. Powell’s remarks underscore the Fed’s commitment to preserving progress against inflation, with decisions guided by incoming data.

Regarding US data, JOLTS job openings for January declined to 8.863M from the previous 9.026M, below the market consensus of 8.900M. ADP private sector employment rose to 140,000 in February, falling short of the expected 150,000.

In the UK, Chancellor of the Exchequer Jeremy Hunt presented the spring budget to the House of Commons. Hunt highlighted the UK’s resilience through crises and projected a 0.8% and 1.9% economic growth in 2024 and 2025, respectively, surpassing forecasts from November. Positive comments and the narrative of high interest rates in the UK boost the Pound Sterling (GBP), acting as a tailwind for the GBP/USD pair.

Upcoming events include US weekly Initial Jobless Claims and Trade Balance on Thursday, along with the second testimony by Chair Powell and Fed’s Mester speech. Friday’s focus shifts to US Nonfarm Payrolls, expected to show 200K job additions in February.

AUDUSD – China’s Jan-Feb Trade Surplus Expands with Export Surge

China trade Balance data came at 125.00 Billion for the month of February, it is more than expected $110 billion and $75 billion in December month. Exports grew by 7.1% from 1.9% expected. So Australian Dollar moved higher after the Data flashed.

AUDUSD has broken the Descending channel in upside

China’s Jan-Feb Trade Balance in Chinese Yuan reached CNY 890.8 billion, up from CNY 540.90 billion.

Exports surged by 7.1% YoY during the period, exceeding the expected 1.9%, while imports increased by 3.5% YoY compared to the previously booked 0.2%.

In US Dollar terms, China’s trade surplus climbed to $125.16 billion, surpassing expectations of +103.7 billion and the December figure of +75.34 billion.

AUDNZD – Australia’s Trade Surplus Widens to 11,027M in February, Missing Expectations

Australian Trade Balance data came at 11027M in February month versus 10743M in the previous month. Exports data grew by 1.6% in February month versus 1.8% previous month. Imports grew by 1.3% from 4.8% previous.

AUDNZD is moving in the Descending channel and the market has reached the lower high area of the channel

Australia’s Trade Surplus Expands to 11,027M in February, Missing Expectations

According to the latest data from the Australian Bureau of Statistics, Australia’s trade surplus widened to 11,027M month-on-month in February, falling short of the expected 11,500M and the previous reading of 10,743M, published on Thursday.

Further details indicate that Australia’s Goods/Services Exports for December showed a 1.6% monthly growth, down from the previous 1.8%. Additionally, the Goods/Services Imports for February increased by 1.3% month-on-month, compared to the previous 4.8%.

NZDUSD – Approaches 0.6150 on Powell’s Rate Cut Remarks

NZ Dollar moved positive against counter pairs, RBNZ Chief economist Paul Conway said we do rate cuts before FED has to started for doing rate cuts in this year. RBNZ Governor ORR said inflation is remain higher so rates should be higher in the current scenario. In 2025 Policy rate can go to normal from this higher rates.

NZDUSD has broken the Box pattern in upside

Fed Chair Powell Hints at 2024 Rate Cuts, US Dollar Weakens

During his House Financial Services Committee testimony, Federal Reserve (Fed) Chair Jerome Powell suggested potential rate cuts in 2024, contingent on achieving higher confidence in inflation progress toward the 2% target. The US Dollar Index (DXY) declined for the fifth consecutive session, reaching around 103.23, despite stable US Treasury yields.

With 2-year and 10-year yields at 4.56% and 4.11%, respectively, the CME FedWatch Tool indicates a 5.0% probability of a 25 basis points rate cut in March. Odds for cuts in May and June are at 19.3% and 55.8%.

The New Zealand Dollar (NZD) strengthened, likely influenced by positive Chinese Trade Balance data, where February figures surged to $125.16 billion, exceeding expectations of $103.7 billion. Year-on-year, Chinese imports and exports grew by 3.5% and 7.1%.

Reserve Bank of New Zealand (RBNZ) Chief Economist Paul Conway hinted at possible interest rate cuts if the Fed pursues monetary easing later in the year. However, Governor Adrian Orr affirmed the RBNZ’s plan for policy normalization in 2025, citing persistent inflationary pressures as a reason to maintain a restrictive monetary policy stance in the near term.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/