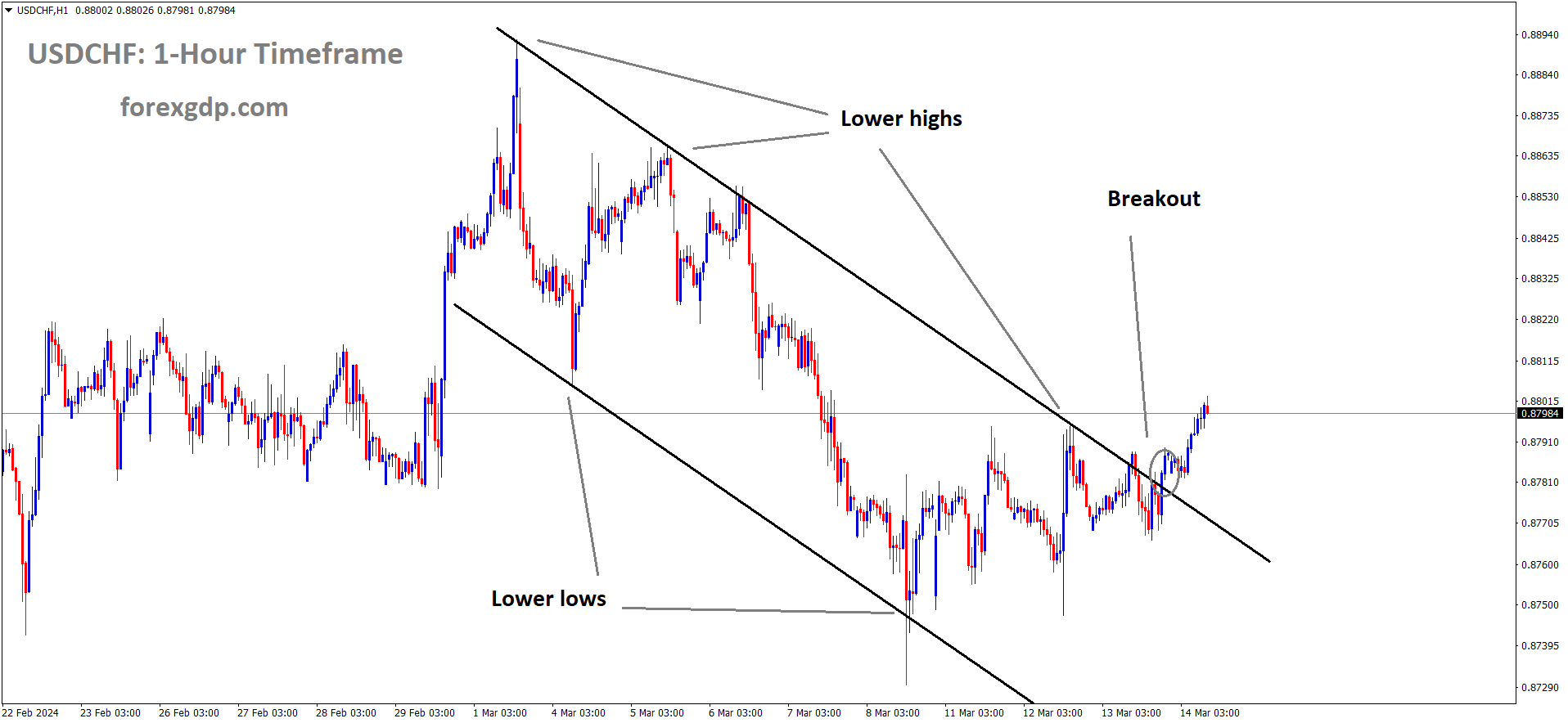

USDCHF has broken the Descending channel in upside

USDCHF – Near 0.8790 as US Inflation Holds Strong

The Consumer confidence indicator in February month decline to -42.3 from -41.1 in January month in Swiss Economy. This reading shows Public financial situation and Overall swiss economy is moving down. So SNB is expected to rate cut in March month is mostly possible to depreciate Swiss Franc currency strengthened.

USD/CHF Rises on Strong US Inflation; SNB Concerned About Swiss Franc Strength

The pair’s ascent is driven by a robust US Dollar (USD), supported by higher US Treasury yields, propelled by recent data indicating “resilient inflation” in the United States (US).

The positive US Consumer Price Index (CPI) has tempered expectations for imminent interest rate cuts by the Federal Reserve (Fed). However, market sentiment still favors a rate reduction in June, with a likelihood of 67.2%, as per the CME FedWatch Tool. Additionally, expectations for a rate cut in July have surged to 84.2%.

US Treasury Secretary Janet Yellen remarked on the unlikelihood of interest rates returning to pre-COVID-19 levels. She also endorsed the interest rate assumptions in President Biden’s budget plan, deeming them “reasonable” and consistent with a wide range of forecasts.

Conversely, the Swiss Franc (CHF) faces challenges as the Swiss National Bank (SNB) adjusts its stance, no longer prioritizing a strong domestic currency. Moreover, the prevailing risk-on sentiment applies downward pressure on the Swiss Franc, traditionally considered a safe haven currency.

SNB Chairman Thomas Jordan voiced concerns about the Swiss Franc’s excessive strength, particularly for Swiss businesses, notably exporters. His comments align with data from Switzerland’s Foreign Exchange Reserves (CHFER), indicating a rebound in Forex reserves, hinting at SNB’s interventions to counter the CHF’s appreciation.

Meanwhile, Switzerland’s consumer confidence indicator continued its decline, dropping to -42.3 in February from January’s -41.1. This trend reflects heightened concerns about personal financial situations and the overall economy in the upcoming months. Thursday will witness the release of Producer and Import Prices for February, providing further insights into Switzerland’s economic outlook.

XAUUSD – Gold Price Depressed Amid Renewed USD Buying, Awaits US Data

The Gold prices are rebounded after the Russian President Vladimir Putin warned US if US Sent troops to Ukraine then we will be ready for Nuclear War. Israel attacked UN Aid Centre Rafah, Gaza, two of Hezobollah Fighters killed in this attack. War fears driven Gold prices to higher against USD in the market.

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

A recent surge in US inflation has led to speculation that the Federal Reserve (Fed) could postpone interest rate cuts. Consequently, this has helped sustain higher US Treasury bond yields, bolstering the US Dollar (USD) and applying downward pressure on gold, which doesn’t yield interest.

Despite this, markets still anticipate a possibility of interest rate cuts by the US central bank in June, which could restrain aggressive bullish bets on the USD. Additionally, ongoing geopolitical tensions from the prolonged Russia-Ukraine conflict and other Middle East disputes may continue to support the safe-haven status of gold. Investors may adopt a cautious stance ahead of the upcoming two-day FOMC meeting scheduled for next Tuesday.

Gold price traders in the Daily Digest Market Movers appear hesitant and are seeking more clarity regarding the Federal Reserve’s stance on interest rate cuts. The prospect of a rate cut by the Fed at the June policy meeting could keep USD bulls cautious and continue to support the non-yielding gold price, especially amid ongoing geopolitical risks.

The US Consumer Price Index (CPI) report released on Tuesday showed signs of inflation persisting, potentially prompting the Fed to maintain its current stance of higher interest rates for a longer period. This may deter XAU/USD bulls from making new bets.

Investors remain wary of geopolitical tensions stemming from the extended Russia-Ukraine conflict and the Israel-Hamas conflict. These uncertainties further contribute to gold’s status as a safe-haven asset.

Recent events, such as Russian President Vladimir Putin’s remarks on the potential escalation of the conflict with the US and Israeli attacks in Rafah and the Bekaa Valley, underscore the geopolitical risks.

A report from US news site Politico indicates that senior US officials have communicated the Biden administration’s support for targeting high-value Hamas targets in Rafah to their Israeli counterparts.

The uncertainty surrounding the Fed’s rate-cut path keeps US Treasury bond yields elevated, preventing significant declines in the USD and capping substantial upward movements in the gold price.

Traders are closely monitoring Thursday’s US macroeconomic data, including monthly Retail Sales, the Producer Price Index, and Weekly Jobless Claims, for potential market-moving insights. However, the focus remains on next week’s Federal Open Market Committee (FOMC) policy meeting.

EURUSD – Yellen: Unlikely Interest Rates Return to Pre-Pandemic Lows

US Treasury Secretary Janet Yellen said in a Speech, Inflation in the US is not smooth, it will be difficult to come at pre-pandemic lows, This year we expect the inflation down to our target but not immediate transition. US President Joe Biden properly budget on US Economy, he was focussing more on US EV Industry running on Chinese Battery parts, if tax increased to China then it will affect our US EV Industry. So Tariffs rising plan is properly managed by US over China.

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

US Treasury Secretary Janet Yellen expressed doubt that US interest rates will revert to pre-COVID-19 levels.

Key Quotes:

– “Interest rate assumptions in Biden’s budget plan were reasonable and consistent with a broad range of forecasts.”

– “The US is taking measures to support the domestic electric vehicle industry amidst competition from China.”

![]()

– “Tax credit rules targeting foreign entities may pose challenges for US-produced electric vehicles to limit Chinese battery content.”

– “When questioned about imposing further tariffs on Chinese EVs, President Biden is dedicated to securing the success of the US EV industry.”

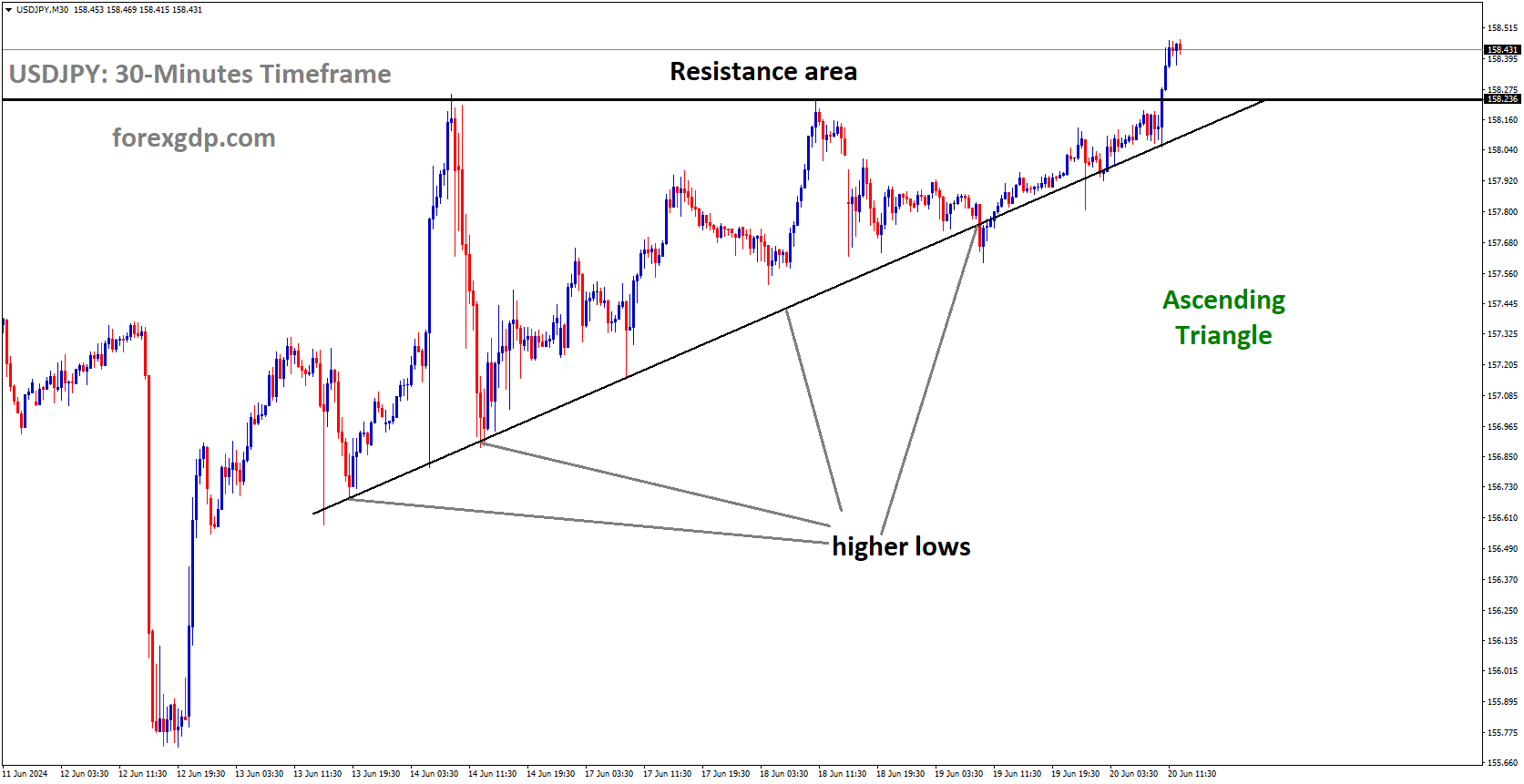

USDJPY – JPY Bears Eye 148.00 Before US Data

The Japanese Yen slight weakness in the market after the reducing bets of rate hike from the Bank of Japan in the next week meeting. Most Japanese Firms agreed to pay the hikes for Labours demanded pay hikes last day. The BoJ Governor Ueda said if 2% inflation target is achieved by wage hike inflation driver it is well satisfied to do end of Negative rates. But it takes time to do watch is real wage hike impacting the inflation to drive higher, then only we do rate hikes in the market.

USDJPY is moving in an Ascending triangle pattern and the market has fallen from the resistance area of the pattern

The Japanese Yen (JPY) continues to be under pressure as the European session begins on Thursday, hovering near the lower end of its weekly range. This is attributed to diminishing expectations for an early interest rate hike by the Bank of Japan (BoJ). Additionally, the prevailing risk-on sentiment in the market is dampening the appeal of the safe-haven JPY, providing support for the USD/JPY pair. However, traders appear hesitant to make bold directional moves and may opt to stay on the sidelines ahead of significant central bank events next week.

The BoJ is set to announce its policy decision on Tuesday, followed by the outcome of the two-day FOMC meeting on Wednesday. Meanwhile, the results of Japan’s spring wage negotiations suggest that most companies have agreed to the wage increase demands of trade unions, hinting at a potential shift in the BoJ’s policy stance. Moreover, the growing consensus that the Federal Reserve (Fed) will commence interest rate cuts in June could limit further upside for the USD and the USD/JPY pair.

Daily Digest Market Movers: Despite positive Japan wage hike data, Japanese Yen bulls remain unmoved

Japan’s major corporations responded favorably to the Union’s wage increase demand, potentially paving the way for the Bank of Japan to terminate its negative interest rates as early as next week, bolstering the Japanese Yen.

Additionally, Japan’s largest industrial union, UA Zensen, disclosed on Thursday that the average pay hike offered by 231 service-sector firms hit a record high not seen since 2013.

Reports from Japanese media suggest that more policymakers at the Bank of Japan are supporting the notion of a policy shift at the upcoming meeting, as substantial pay increases by leading companies bring the 2% price stability target within reach.

According to insiders, the Bank of Japan officials believe that the central bank is nearing liftoff, regardless of whether the first rate hike since 2007 occurs in the March or April policy meeting.

However, Bank of Japan Governor Kazuo Ueda indicated earlier this week that the central bank will only begin to ease its policy stance when achieving a 2% inflation rate is imminent, dampening expectations for an early interest rate hike.

Former central bank executive Hideo Hayakawa suggested on Thursday that Bank of Japan Governor Kazuo Ueda will likely proceed cautiously in normalizing ultra-loose monetary policy after discontinuing negative interest rates.

In separate developments, an Israeli strike targeted a UN aid distribution center in Rafah, while Lebanon’s Hezbollah reported the deaths of two fighters in the Bekaa Valley following consecutive days of Israeli attacks in the region.

The release of slightly warmer US consumer inflation data on Tuesday sparked speculation that the Federal Reserve might maintain its stance of keeping interest rates elevated for a longer duration. Despite this, the market sentiment still anticipates a rate cut by the Fed in June. As a result, the US Dollar bulls are adopting a defensive stance, offering limited momentum to the USD/JPY pair. Traders are cautiously observing developments as they await the upcoming monetary policy meetings of both the Bank of Japan (BoJ) and the Federal Open Market Committee (FOMC) next week. Additionally, the release of US macroeconomic data, including Retail Sales, the Producer Price Index (PPI), and Weekly Initial Jobless Claims on Thursday, could present short-term trading opportunities amidst the looming risks associated with central bank decisions.

USDCAD – Slides to 1.3470, Investors Await US Retail Sales

The Bank of Canada left the rates earlier this month. The BoC Governor Tiff Mackhlem said inflation is reaching close to our target. But Economists expected the BoC won’t cut or hike rates until FED has to do in the rates. Crudeoil prices are supporting Canadian Dollar due to Canada is the largest exporter of Oil to US.

USDCAD is moving in the Box pattern and the market has rebounded from the support area of the pattern

USD/CAD Dips as Investors Await US Retail Sales

During early Asian trading on Thursday, the USD/CAD pair continued its decline for a second consecutive day. The US Dollar (USD) slipped below the 1.03 mark, exerting downward pressure on the pair. Market participants are awaiting the release of US Retail Sales data for February, expected to show a 0.8% month-on-month increase. Currently, USD/CAD is trading at 1.3468, down 0.02% for the day.

Earlier in the week, higher-than-expected US inflation data may keep the Federal Reserve (Fed) on course to delay interest rate cuts until at least the summer. However, the upcoming Retail Sales data could influence the Fed’s decision-making in its March meeting next week. A stronger report might prompt the Fed to adopt a wait-and-see approach, potentially boosting the USD and providing support for the USD/CAD pair.

Conversely, the Bank of Canada (BoC) recently kept interest rates unchanged, emphasizing the importance of achieving target inflation levels. Market expectations suggest the BoC will likely refrain from aggressive rate cuts until after the Fed, potentially strengthening the Canadian Dollar in the coming months.

Additionally, rising crude oil prices could temporarily support the commodity-linked Loonie, given Canada’s status as a major oil exporter to the US.

Looking ahead, traders will monitor the release of Canadian Manufacturing Sales data. In the US, focus will be on Retail Sales figures for February, alongside the Producer Price Index (PPI), Business Inventories, and weekly Initial Jobless Claims.

USD INDEX – US Retail Sales: Economists Anticipate February Rebound

US Retail sales for the month of February is expected at 0.80% higher than 0.80% drop in January month. US Inflation is rose to 3.2% this week for the month of February. So retail sales and Core retail sales also expansion is expected from Economists side today.

USD Index is moving in the Descending channel and the market has rebounded from the lower low area of the channel

US Census Bureau to Release US Retail Sales Report, Expected to Show February Rebound

The United States Census Bureau is set to publish the country’s Retail Sales report on Thursday, anticipated to reverse the 0.8% monthly contraction witnessed in January. Consumer spending among US residents has been inconsistent in recent months as market participants continue to assess the Federal Reserve’s (Fed) tightening credit conditions.

According to the Census Bureau, the “advanced estimates of U.S. retail and food services sales for January 2024, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $700.3 billion, down 0.8 percent (±0.5 percent) from the previous month, and up 0.6 percent (±0.7 percent) above January 2023.”

Meanwhile, the US Dollar has managed to stabilize, prompting the USD Index (DXY) to rebound from recent multi-week lows near 102.30 (March 8). This comes amidst increasing speculation that the Fed may commence its easing cycle in the summer, with June being the favored option.

The recent uptick in the US Dollar was primarily fueled by higher-than-expected US inflation figures for February. Despite a downward trend in domestic consumer prices, inflation remains a persistent concern. According to the US Bureau of Labor Statistics, the headline Consumer Price Index (CPI) rose 3.2% year-on-year in February, with the Core CPI up by 3.8%.

Regarding potential rate cuts in the coming months, Federal Reserve Chair Jerome Powell’s remarks during congressional testimonies hinted at the possibility of interest rate reductions within the year. However, such actions will only be taken once the Fed gains greater confidence in inflation returning to its targeted annual rate of 2%.

What to Expect in the February US Retail Sales Report?

The headline Retail Sales are expected to expand by 0.8% month-on-month, following a 0.8% decline recorded in the previous month. Core Retail Sales, excluding the automobile sector, are projected to increase by 0.5% on a monthly basis.

Ahead of the release, analysts at TD Securities commented, We also look for retail sales to rebound a strong 0.8% m/m in February following January’s retreat of a similar magnitude. Volatile auto and gasoline station sales will likely boost growth, with the control group also acting as a key driver.

EURNZD – ECB’s Stournaras Urges Interest Rate Cuts

ECB Governing Council member Yannis Stournaus said ECB has to do rate cuts in near term, but it may be before the FED rate cuts also. But there should be a two rate cuts before summer break is expected.

EURNZD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

Yannis Stournaras, a member of the European Central Bank (ECB) Governing Council, emphasized on Thursday the necessity for the ECB to initiate interest rate reductions promptly.

He dismissed the notion that the ECB should wait for the Federal Reserve to act before implementing rate cuts. Stournaras advocated for avoiding excessively restrictive monetary policies and proposed two rate cuts before the summer recess.

GBPUSD – Rebounding to 1.3000 Zone: Rabobank

RABO BANK economists said GBP will be stronger in the near term against Euro. The Bank of England will do the rate cuts in September month most probably, But ECB has to do rate cuts in June month. This interest rate differentials made GBP to drive stronger against Euro. Dull Political elections in this year and Political backdrop makes GBP to move higher against Euro.

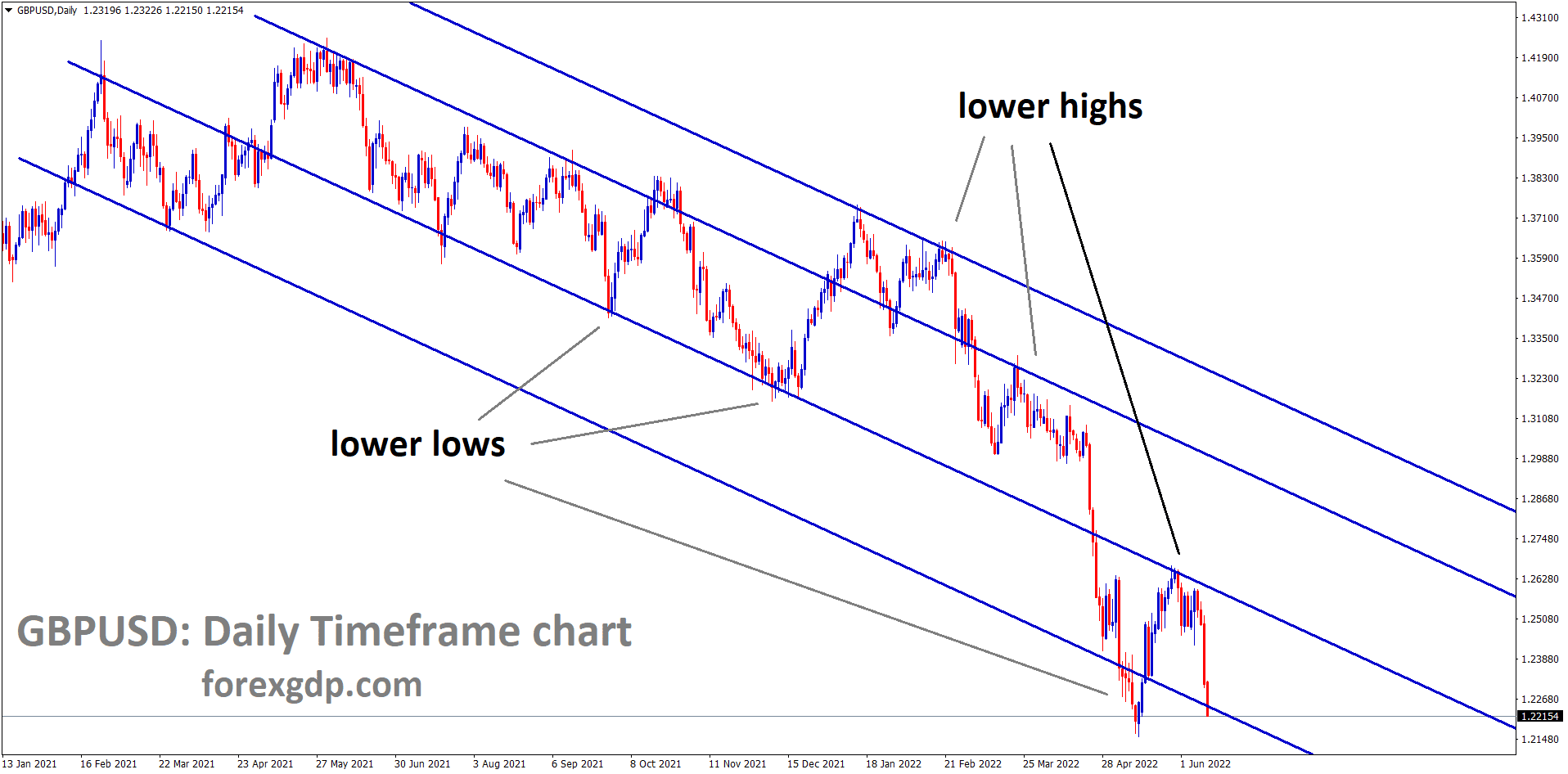

GBPUSD has broken the Descending channel in upside

Rabobank Economists Optimistic on GBP, Predict EUR/GBP Decline

Rabobank maintains a positive outlook for the Pound Sterling (GBP) this year.

They anticipate EUR/GBP to decrease towards 0.8400 in the latter part of the year. Their optimism stems from their belief that the Bank of England (BoE) may maintain a stable policy until September, contrasting with their expectations of rate cuts from the European Central Bank (ECB) and the Federal Reserve in June. Rabobank forecasts a shift to EUR/GBP 0.8400 in the latter half of the year.

They attribute this forecast to the interest rate differential, positive signs in the UK economic outlook, expectations of a subdued UK election, and a relatively stable political environment, all contributing to moderate Pound support.

Furthermore, they predict Cable (GBP/USD) to recover to the 1.3000 area within 12 months, although they foresee possible downward movements in the shorter term due to sporadic periods of widespread USD strength.

AUDUSD – climbs on RBA’s hawkish stance

The Rate cuts is expected from FED is June month, if rate cut is done in US then Foreign inflow capital to US will be down. RBA is remaining hawkish stance until the inflation has to 2% target level. So Rate cuts is more expected from FED than RBA is positive for Australian Dollar in the market against US Dollar.

AUDUSD has broken the Descending channel in upside

It inches up by 0.2% as markets anticipate a June rate cut by the Federal Reserve (Fed), despite persistent inflation.

Lower rates are detrimental to USD due to reduced foreign capital inflows, contrasting with potential hikes by the Reserve Bank of Australia (RBA).

NZDUSD – edges up to 0.6160 as US Dollar falls.

The Fears of inflation expectations in NZ is diminished, 0.80% is projected by the end of march 2024, Annual inflation rate is expected to rose at 4.2% in 2024 than 4.7% in 2023. So RBNZ will be holding the higher rates this year will support the NZ Dollar in the market.

NZDUSD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

The Kiwi asset remains mostly flat as attention turns to the upcoming release of United States Retail Sales data for February on Thursday. This data will offer insight into household spending and its impact on consumer price inflation.

Despite diminished expectations for a June interest rate cut by the Federal Reserve (Fed), the US Dollar slips to 102.80. The CME Fedwatch tool indicates a 65% probability of rate cuts in June, down from over 72% prior to the release of February’s inflation figures.

On the other hand, easing inflation expectations in New Zealand are anticipated to provide some relief to households. The Reserve Bank of New Zealand (RBNZ) forecasts a 0.8% increase in consumer prices for the March quarter, with annual inflation projected to decrease to 4.2% from 4.7% in the previous quarter. With current price pressures significantly exceeding the desired rate of 2%, the RBNZ is expected to maintain higher interest rates for an extended period.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/