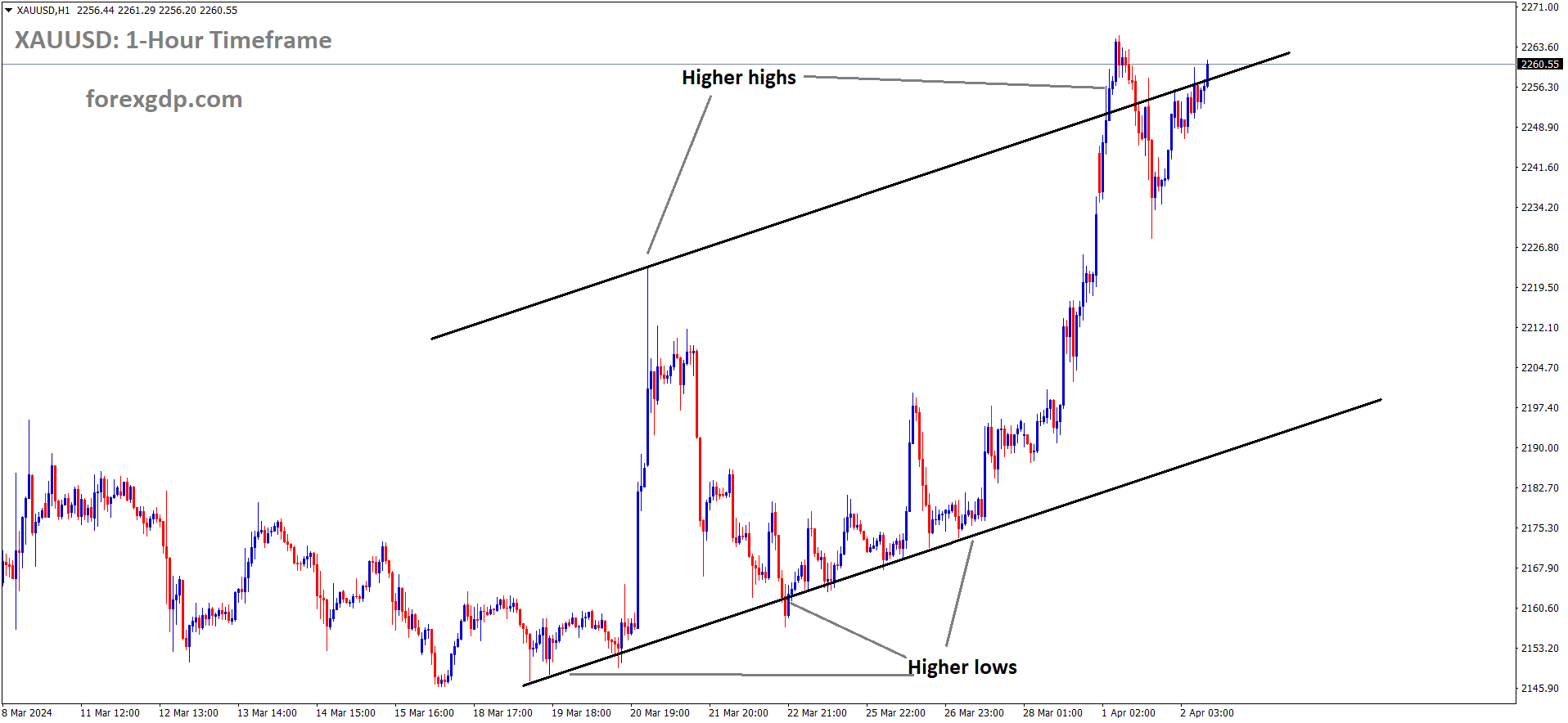

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

XAUUSD – Gold price consolidates below all-time high with bullish outlook intact

The Israel attacked Syria Capital near Iran Embassy and killed 7 peoples. Missiles closed to Iranian Embassy created fears of war between Iran and Israel from Gaza conflicts. Gold prices are increased after the fears of war continued in the middle east.

The price of gold (XAU/USD) has continued to exhibit a positive trend for the sixth consecutive day, remaining within striking distance of its all-time high reached around the $2,265-$2,266 area in the previous session. This sustained upward movement comes against a backdrop of escalating geopolitical tensions, notably following reports of an Israeli strike targeting a building adjacent to Iran’s embassy in Syria’s capital. Such geopolitical unrest tends to bolster demand for gold, given its status as a safe-haven asset.

Furthermore, uncertainty surrounding the Federal Reserve’s monetary policy stance has also contributed to the positive bias in gold prices. Doubts persist regarding whether the Fed will implement three interest rate cuts throughout the year, influencing global risk sentiment. This uncertainty has acted as a tailwind for gold, as investors seek refuge in the precious metal amid market volatility.

In contrast, upbeat manufacturing data released in the United States on the previous day has prompted investors to scale back their expectations of a Fed rate cut in June. This has led to higher US Treasury bond yields and a consequent strengthening of the US Dollar (USD), which has somewhat limited the upward movement of gold prices. The USD has reached its highest level since February 14, putting pressure on gold, which lacks yield and competes with interest-bearing assets when the greenback appreciates.

Moreover, traders are also waiting for some consolidation in gold prices in the near term due to overstretched conditions on the daily chart. This pause in the rally is anticipated ahead of the release of key US macroeconomic data and speeches by influential Federal Open Market Committee (FOMC) members scheduled for later in the day. These events are expected to provide further clarity on the direction of Fed policy and could influence market sentiment towards gold.

The Institute for Supply Management’s report indicating expansion in the US manufacturing sector for March after 16 months of contraction has altered market expectations regarding Fed rate cuts. This shift has driven up yields on US government bonds, including the two-year and ten-year Treasury bonds, supporting the USD and weighing on gold prices.

Additionally, recent Israeli airstrikes in Syria, resulting in casualties including a senior Revolutionary Guard commander, have heightened tensions in the Middle East. This geopolitical uncertainty has further boosted demand for gold as a safe-haven asset.

Furthermore, the moderate rise in the US Personal Consumption Expenditures (PCE) Price Index for February, released last Friday, has kept hopes of Fed rate cuts alive, providing some support for gold prices by limiting the downside potential.

Looking ahead, the market will closely monitor Tuesday’s economic calendar, particularly the release of JOLTS Job Openings and Factory Orders data from the US. Moreover, speeches by several influential FOMC members are anticipated to provide fresh insights into the Fed’s policy outlook, which could drive demand for the USD and influence the direction of gold prices.

EURUSD – meets resistance at 1.0730, awaits Fedspeaks

The ECB Governing council member Robert Holzmann said on Saturday, ECB has to do rate cut before FED in this year. US Manufacturing PMI data came at 50.3 in March it is the largest expansion in the US since September 2022. The Euro currency is more weaker against USD after the data printed yesterday.

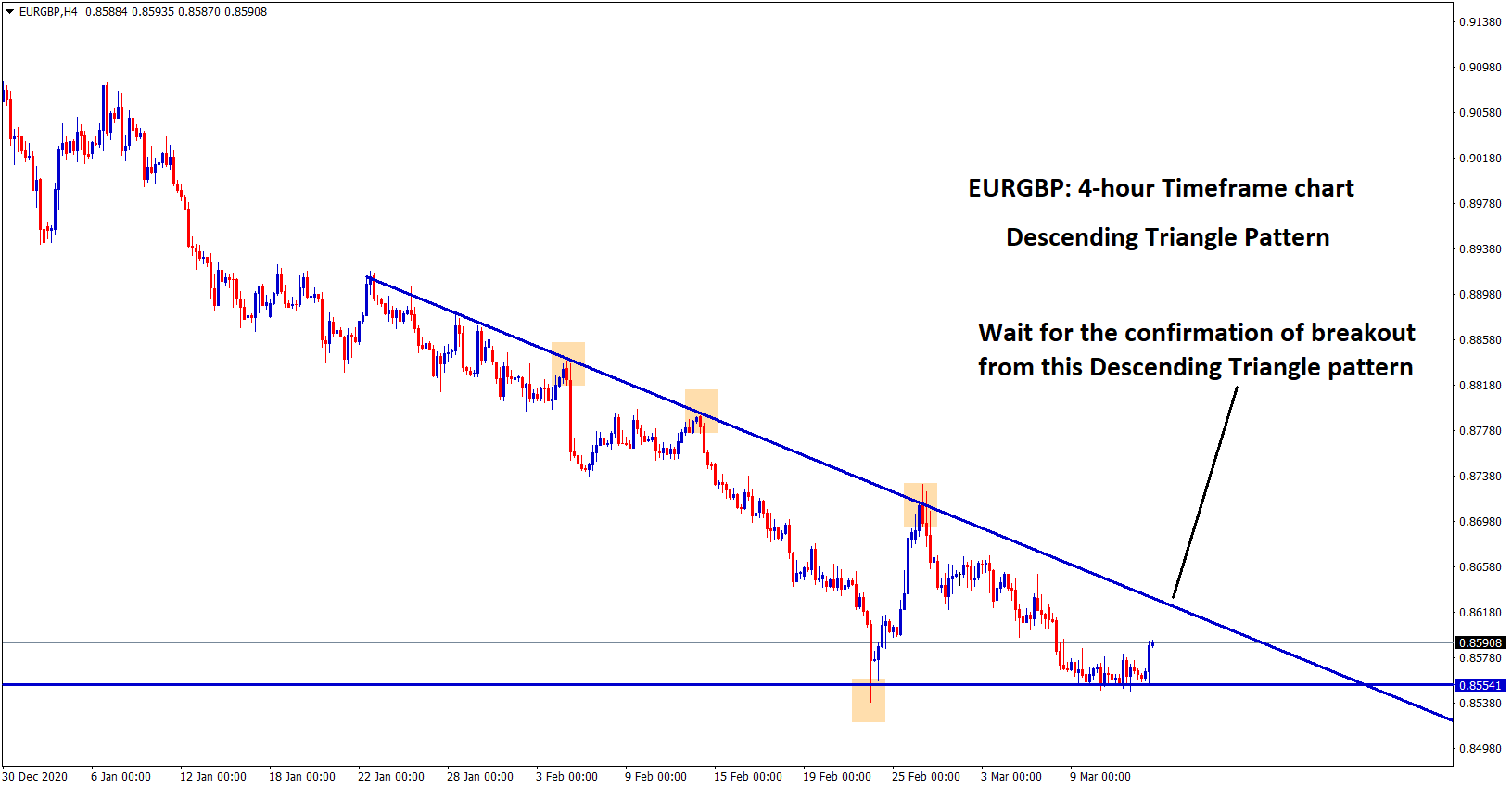

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

Notably, several Federal Reserve (Fed) officials, including Michelle Bowman, Loretta Mester, John Williams, and Mary Daly, are scheduled to deliver speeches later in the day, drawing attention from traders and investors alike.

On the US front, the Institute for Supply Management (ISM) reported that manufacturing activity in March marked its first expansion in nearly 18 months, with increased production and new orders. The Manufacturing Purchasing Managers’ Index (PMI) rose to 50.3 in March from 47.8 previously, surpassing market expectations of 48.4. This upbeat data strengthens the US Dollar, as reflected in investor sentiment, with the CME FedWatch Tool indicating a 61% probability of a 25 basis points rate cut by the Fed in June, up from 55.2% before the data release.

Meanwhile, European Central Bank (ECB) Governing Council member Robert Holzmann suggested over the weekend that the ECB could potentially lower its key interest rate ahead of the Fed. Additionally, ECB policymaker Yannis Stournaras mentioned the possibility of a total rate cut of 100 basis points by the ECB this year, although consensus remains elusive. Stournaras emphasized that the ECB has no need to wait for the Fed to act first. Such dovish remarks from ECB officials contribute to the selling pressure on the Euro (EUR), serving as a hindrance to the EUR/USD pair’s upward movement.

Market participants are keenly awaiting the release of manufacturing PMI data for Spain, Italy, France, Germany, and the Eurozone, as well as the preliminary Eurozone Harmonized Index of Consumer Prices (HICP) for March. Furthermore, attention will turn to US Nonfarm Payrolls data on Friday, shaping market sentiment and influencing trading decisions.

USDJPY – Suzuki of Japan Silent on FX Intervention Details

The Japanese Fianance Minister Shunuchi Suzuki said FX Intervention is possible, we do not say specific times for that. FX Moves mostly by Fundamentals is acceptable, not by Speculative moves.

USDJPY is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Japanese Finance Minister Shunichi Suzuki addressed concerns regarding foreign exchange (FX) intervention during a statement made on Tuesday. Suzuki emphasized the importance of closely monitoring FX movements with a heightened sense of urgency. He stated that he remains open to taking necessary actions to address any disorderly movements in the currency markets. Suzuki highlighted the significance of maintaining stability in currency movements, emphasizing that rapid fluctuations in FX rates are undesirable.

Additionally, he refrained from commenting on specific interventions in the FX market when questioned, stating that he would not disclose the methods the Ministry of Finance (MOF) might employ for intervention. Suzuki acknowledged that various factors influence FX movements, not solely monetary policy, suggesting a multifaceted approach to understanding and responding to currency fluctuations.

USDCHF – Approaches 0.9080 on Weak Swiss Real Retail Sales

The Retail sales of Switzerland came at 0.20% decline in February from 0.30% increase in January month and 0.40% increase is expected. The SNB said interest rate cuts is possible if inflation is moving in the downtrend continues. The ING Analysts expected 2 rate cuts from SNB in this 2024 Year.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The US Dollar (USD) experienced a surge in value driven by a rise in US Treasury bond yields, particularly bolstered by favorable ISM Manufacturing PMI data emanating from the United States (US). This surge provided support for the USD/CHF currency pair.

Market analysts attribute this sustained positive movement to a reduction in expectations among traders regarding a potential quarter-point interest rate cut by the Federal Reserve during its June meeting.

Federal Reserve Chairman Jerome Powell’s remarks on Friday further reinforced market sentiment, indicating that recent US inflation data aligns with the central bank’s anticipated trajectory. This served to solidify the Fed’s stance on interest rate adjustments for the remainder of the year.

Conversely, Real Retail Sales (Year-over-Year) figures from Switzerland revealed a decline of 0.2% in February, a departure from the expected increase of 0.4% and the previous month’s rise of 0.3%. This unexpected downturn exerted downward pressure on the value of the Swiss Franc (CHF).

In light of these developments, the Swiss National Bank (SNB) underscored the feasibility of monetary policy easing, citing the effectiveness of its inflation-fighting measures implemented over the past two and a half years.

Looking ahead, analysts at ING anticipate the possibility of two additional rate cuts by the SNB in 2024, contingent upon the absence of unforeseen global economic disruptions that could swiftly reignite inflationary pressures.

USDCAD – Trades higher on strong USD, but bullish oil prices could limit gains.

The Canadian Dollar strengthened by US Oil prices gained in the market. Middle east tensions day by day increasing supporting Canadian Dollar in the market. Domestic data of Canada last week printed higher than expected makes additional support for CAD.

USDCAD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The USD Index (DXY), reflecting the USD against a basket of currencies, has surged to its highest level since February 14. This follows uncertainties surrounding the likelihood of the Federal Reserve (Fed) implementing three interest rate cuts this year. Market sentiment shifted as investors scaled back expectations for a June Fed rate cut, prompted by encouraging US data. Notably, the manufacturing sector recorded growth in March for the first time since September 2022. Elevated US Treasury bond yields, consequentially, bolster the USD and the USD/CAD pair.

Additionally, a risk-averse sentiment in the market bolsters the appeal of the safe-haven USD. Conversely, Crude Oil prices maintain a robust stance, nearing a five-month high achieved on Monday. This is fueled by indications of improved demand and the looming threat of heightened tensions in the Middle East. Consequently, the commodity-linked Canadian Dollar (CAD) gains strength, potentially hindering fresh bullish positions in the USD/CAD pair. Moreover, repeated failures to surpass the 1.3600 threshold in recent trading sessions advise cautious optimism.

Market focus shifts to the US economic calendar, which includes the release of JOLTS Job Openings and Factory Orders during the early North American session. Additionally, speeches by influential FOMC members, US bond yields, and broader market sentiment will influence USD demand, thereby impacting the USD/CAD pair. Traders will also monitor Oil price dynamics for short-term trading opportunities.

USD INDEX – USD begins week positively, focus on labor stats and Fed talks

The US Manufacturing data came at 18 month higher and 50-level mark. The Strong US Domestic data represents FED has cut rate in June poll has decreased from 85% to 65%. The Poll decreasing is favouring US Dollar stronger against counter pairs.

USD Index has broken Ascending channel in upside

The robust Institute for Supply Management (ISM) report for March, revealing the strongest growth since September 2022, might temper the Federal Reserve’s (Fed) eagerness to initiate an easing cycle. The forthcoming labor market data scheduled for release later in the week will significantly influence market expectations.

The current state of the US economy presents a stable outlook, with the Fed under Chairman Powell’s leadership adopting a cautious approach. Despite upward revisions in inflation forecasts, the Fed remains vigilant, refraining from reacting hastily to transient inflationary spikes. The speculated commencement of an easing cycle in June hinges on the trajectory of incoming economic indicators.

Key Points:

– The ISM report for March indicates a notable improvement in business activity, marking the first upswing since September 2022, thereby reflecting a resilient economy.

– The Manufacturing Purchasing Managers Index (PMI) surged to 50.3 in March, surpassing projections of 48.4 and notably exceeding the previous month’s reading of 47.8.

– The Prices Paid Index in the ISM report reached its highest level since August 2022, indicating an increase in year-on-year inflationary pressures.

– The robust economic performance might dissuade the Fed from considering monetary policy relaxation.

– Consequently, the likelihood of a rate cut in the June meeting decreased from 85% to approximately 65% in response to ongoing economic strength.

– In the bond market, US Treasury bond yields experienced a sharp ascent, with the 2-year yield at 4.71%, the 5-year yield at 4.33%, and the 10-year yield at 4.33%, reflecting heightened optimism for a hawkish monetary policy stance.

– Crucial labor market indicators such as Average Hourly Earnings, Nonfarm Payrolls, and the Unemployment Rate will provide valuable insights into the workforce’s health and trends.

– Tuesday will witness several Fed officials delivering speeches, contributing further to the evolving market sentiment and expectations.

GBPUSD – below 1.2550 as US Dollar strengthens, US PMI data upbeat

The US ISM Manufacturing Data came at 50.3 in March month and 47.8 is printed at last month. 18 months after the US has entered into 50 level mark and expansion zone. The Bank of England Governor Bailey already said there will be a 2 or 3 rate cuts in this year 2024. The Dovish comments from BoE makes GBP weaker against USD.

GBPUSD is moving in the Box pattern and the market has reached the support area of the pattern

US Treasury bond yields experienced a notable increase overnight, driven by the release of positive US ISM data. This development presents a challenge for the GBP/USD pair.

The US ISM Manufacturing Purchasing Managers’ Index (PMI) unexpectedly showed expansion in March. The index surged to 50.3 from February’s 47.8, surpassing the anticipated 48.4. This reading marked the highest level since September 2022, signaling the first expansion in manufacturing activity since October 2022. A reading above 50 indicates overall expansion in the manufacturing sector, while a reading below 50 suggests contraction. The strong data prompted increased demand for the US Dollar (USD) across various currency pairs.

Additionally, the Bank of England (BoE) conveyed a dovish message in its recent monetary policy statement. BoE Governor Andrew Bailey indicated that market expectations for two or three rate cuts this year are reasonable, hinting at potential rate cuts in the near future. Bailey also noted the absence of significant persistent factors, further supporting expectations for rate cuts. These remarks weighed on the value of the Pound Sterling (GBP) relative to the US Dollar, contributing to the downward pressure on the GBP/USD pair.

Looking ahead, the UK Nationwide Housing Prices and S&P Global/CIPS Manufacturing PMI for March are scheduled for release later on Tuesday. Moreover, Federal Reserve (Fed) officials, including Governor Michelle Bowman, Loretta Mester, John Williams, and Mary Daly, are slated to deliver speeches, which could influence market sentiment and currency movements.

AUDUSD – RBA Minutes: No Interest Rate Rise Considered

The RBA Meeting minutes happened today, outcome is no rate hike or cut in near term. It is difficult situation for taking one decision in monetary policy settings, Inflation is slight higher, it will come down once productivity increased, then Labour unit cost get down, really House hold suffered from higher rates. Consumption is lower due to higher inflation, it will be arrested soon by our policy settings.

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The Reserve Bank of Australia (RBA) released the detailed Minutes of its March monetary policy meeting on Tuesday, revealing that the Board members opted not to entertain the possibility of increasing interest rates. Further insights from the RBA Minutes indicate a nuanced perspective on potential future adjustments to the cash rate.

Key Highlights:

– The minutes conspicuously lacked any mention of the board contemplating the prospect of raising rates.

– The Board reached a consensus that assessing forthcoming changes to the cash rate presented considerable challenges.

– Despite an uncertain economic outlook, risks appeared to be evenly distributed.

– The Board acknowledged that it would require a significant amount of time before they could confidently anticipate a return of inflation to the target level.

– While inflation rates were elevated, there were no immediate signs of upward pressure, with consumer spending notably subdued.

– Despite inflation trending gradually towards the target, there was evidence of a softening labor market.

– The gap between demand and supply in the economy was noted to be narrowing swiftly.

– The Board assessed that demand would likely outpace supply for the foreseeable future, leading to a marginally tighter labor market.

– Although wage growth may have peaked, a rapid decline was not anticipated.

– A recovery in productivity was deemed necessary to counterbalance the persistently high unit labor costs.

– Overall, financial conditions were observed to be restrictive, particularly impacting households.

NZDUSD – RBNZ’s Orr: Laser-focused on controlling inflation

The RBNZ Governor Adrian Orr said, we are looking as a Laser point in controlling inflation in our economy. Many central banks expected we are back on the top of the inflation,we are still having higher inflation in our economy. People expected moderate rise of inflation in next year.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

We are ready to adjust the monetary policy according to the inflation moved to our target.

Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr reaffirmed the central bank’s commitment to controlling inflation during his remarks on Tuesday. He emphasized that the bank maintains a laser-like focus on its mandate to keep inflation in check and expressed confidence that they are making progress in returning inflation to the target range.

Orr highlighted the significance of the Monetary Policy Committee (MPC) in guiding the bank’s discussions, indicating the pivotal role of members Carl and Prasanna in these deliberations.

While acknowledging improvements in the inflation outlook, Orr noted that concerns about inflation expectations persist. He emphasized the interplay between public perceptions of future inflation and the actual trajectory of inflation, underscoring the importance of managing expectations to achieve price stability.

Despite ongoing challenges, Orr expressed optimism about the bank’s efforts to steer inflation back toward the target band, indicating that they are on course to achieve this goal.

CRUDE OIL – WTI Eyes Further Gains, Holds Above $83.50

The Crude Oil prices are gained after the US Manufacturing data came at robust numbers last day. China and US picked up in Manufacturing activity is positive for Oil demand. Iraq and Nigeria also output cuts inline with OPEC+ cuts. Wednesday this week meeting will conclude how much barrels per day is going to reduce by OPEC+. Russia have more oil refineries and 10% of Oil refineries is attacked by Ukraine Drone attacks. 1 million barrel per day is shortage for Russia refineries from this attack.

XTIUSD Crude Oil price is moving in an Ascending channel and the market has reached the higher high area of the channel.

During the Asian trading hours on Tuesday, the price of West Texas Intermediate (WTI) crude oil remains relatively stable, hovering around the $83.50 per barrel mark. Despite this, crude oil prices are experiencing an upward trend, primarily driven by robust manufacturing data from both the United States (US) and China, which surpassed market expectations. The expansion of manufacturing activities in these two major economies in March is perceived as a positive indication of increased oil demand globally.

Moreover, crude oil prices are receiving additional support from a Reuters survey indicating a decline in oil output from the Organization of the Petroleum Exporting Countries (OPEC) during March. Countries like Iraq and Nigeria have reportedly reduced their oil exports, aligning with the ongoing voluntary supply cuts by select OPEC members as part of the broader OPEC+ alliance. In March, the group collectively produced 26.42 million barrels per day (bpd), marking a decrease of 50,000 bpd compared to the previous month.

The upcoming joint ministerial meeting of OPEC+ scheduled for Wednesday is anticipated to focus on evaluating market fundamentals and member compliance with production targets. It is widely expected that the current output policies will be upheld during this meeting.

According to Patrick De Haan, a petroleum analyst at GasBuddy.com, the US gasoline market could witness a spike in prices by up to 15 cents per gallon due to tighter global fuel supplies resulting from recent attacks by Ukraine on Russian refineries. Ukrainian drone strikes have significantly disrupted operations at several Russian refineries, leading to a reduction in Russia’s fuel exports. As a result, nearly 1 million barrels per day of Russian crude processing capacity has been rendered inactive.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/