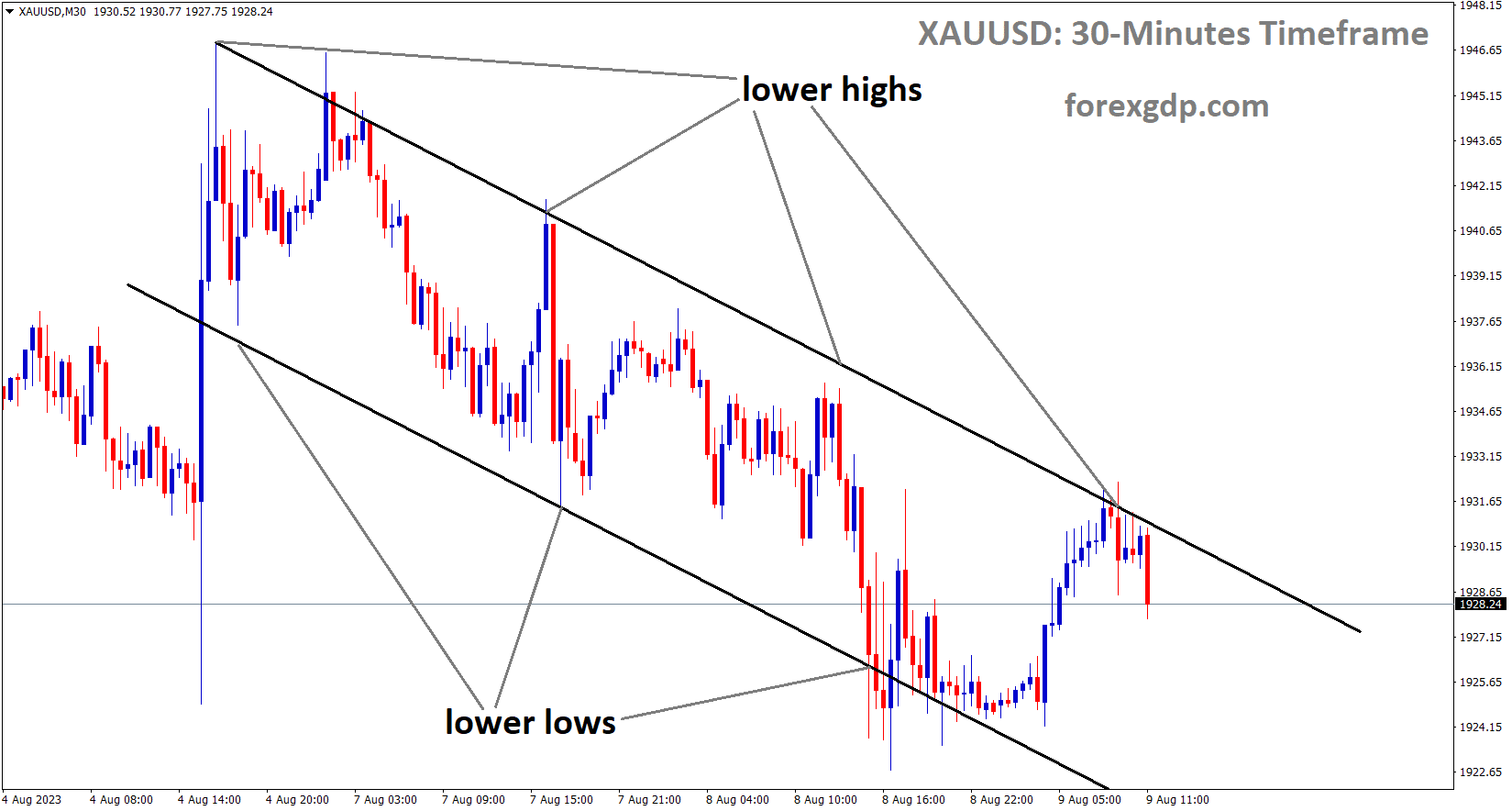

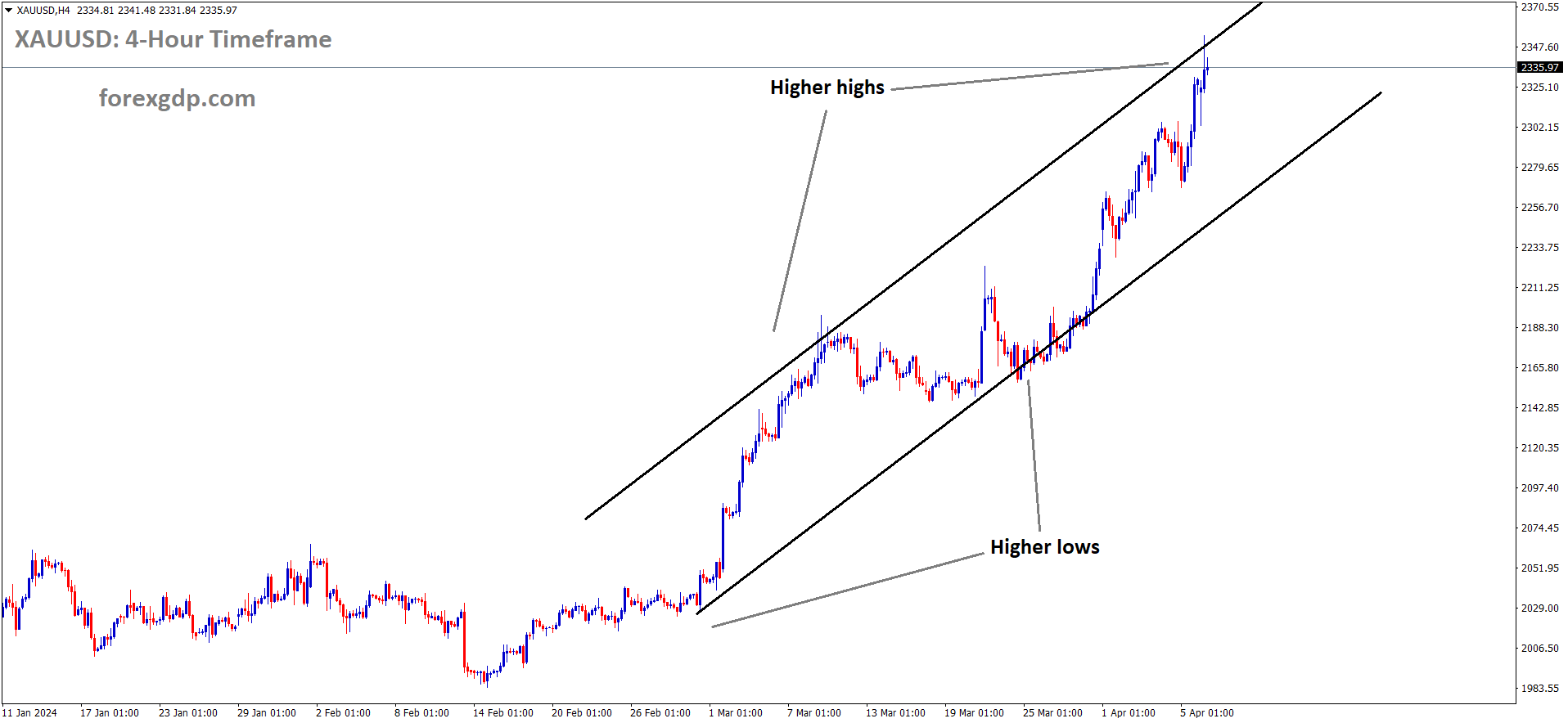

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

XAUUSD – Gold Price Holds Strong Near Record High; Stronger USD and Risk-On Sentiment Limit Upside

The Gold prices are set to higher after the China central banks buying more Golds due to real estate and Stock market crisis. The Israel withdrew troops from Southern Gaza and opened for ceasefire talks of war makes easing tensions in the Middle east. US NFP Data came at robust numbers makes US moving stronger against rivals, But Gold rallying in the war fears of Russia- Ukraine and Israel- Gaza.

Gold prices, denoted as XAU/USD, surged to reach a new all-time high as the new trading week commenced, maintaining its upward trajectory during the European session. This rally has been fueled by expectations that the Federal Reserve (Fed) will initiate interest rate cuts in 2024, coupled with significant purchases from the Chinese central bank, propelling the precious metal to unprecedented levels over the past fortnight. Despite these bullish factors, the prevailing positive market sentiment, amplified by easing tensions in the Middle East, restrains further gains for gold, especially considering the excessively stretched conditions observed on the daily price chart.

")

Moreover, the optimistic US Nonfarm Payrolls (NFP) report, released on the preceding Friday, hinted at a potential delay in the Fed’s rate cut decision, prompting investors to recalibrate their expectations from three anticipated rate reductions in 2024 to two. This outlook has bolstered US Treasury bond yields, thereby reinforcing the strength of the US Dollar (USD) and acting as a limiting factor on gold’s ascent, given its non-yielding nature. Market participants are now eyeing the upcoming release of US consumer inflation data for March and the minutes from the Federal Open Market Committee (FOMC) meeting for guidance on the Fed’s future monetary policy stance before initiating new trading positions.

In summary, the gold market experienced a brief pause amidst prevailing market sentiment and moderate USD strength. The buying spree by China’s central bank, combined with expectations of forthcoming US interest rate cuts, propelled gold prices to unprecedented heights. The global risk environment improved following developments in the Middle East, while robust US economic data tempered expectations of aggressive monetary easing, supporting the USD and capping gains for gold. Traders await further cues from upcoming economic indicators and FOMC minutes for potential market direction.

EURUSD – German Industrial Production Surges: Up 2.1% MoM in February vs. Expected 0.3%

The German Industrial production output came at 2.1% MoM versus 0.30% expected and 1.3% printed in January month. The annual rate of IP output is plunged by 4.9% in February compared to 5.3% plunged by January month. The Euro currency remains flat after the data printed.

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel

According to the most recent data released by Destatis on Monday, Germany’s industrial sector continued its upward momentum in February.

The industrial output in the largest economy of the Eurozone surged by 2.1% month-on-month (MoM), as reported by the federal statistics authority Destatis. This figure is adjusted for seasonal and calendar effects. It notably surpassed market expectations, which had anticipated a more modest increase of 0.3%. The February performance also marked an acceleration from the 1.3% growth recorded in January.

Despite the positive monthly growth, the year-on-year (YoY) comparison reveals a decline in German industrial production. In February, industrial production fell by 4.9% compared to the same period last year. However, this decline represents an improvement from the previous month’s YoY contraction of 5.3% recorded in January.

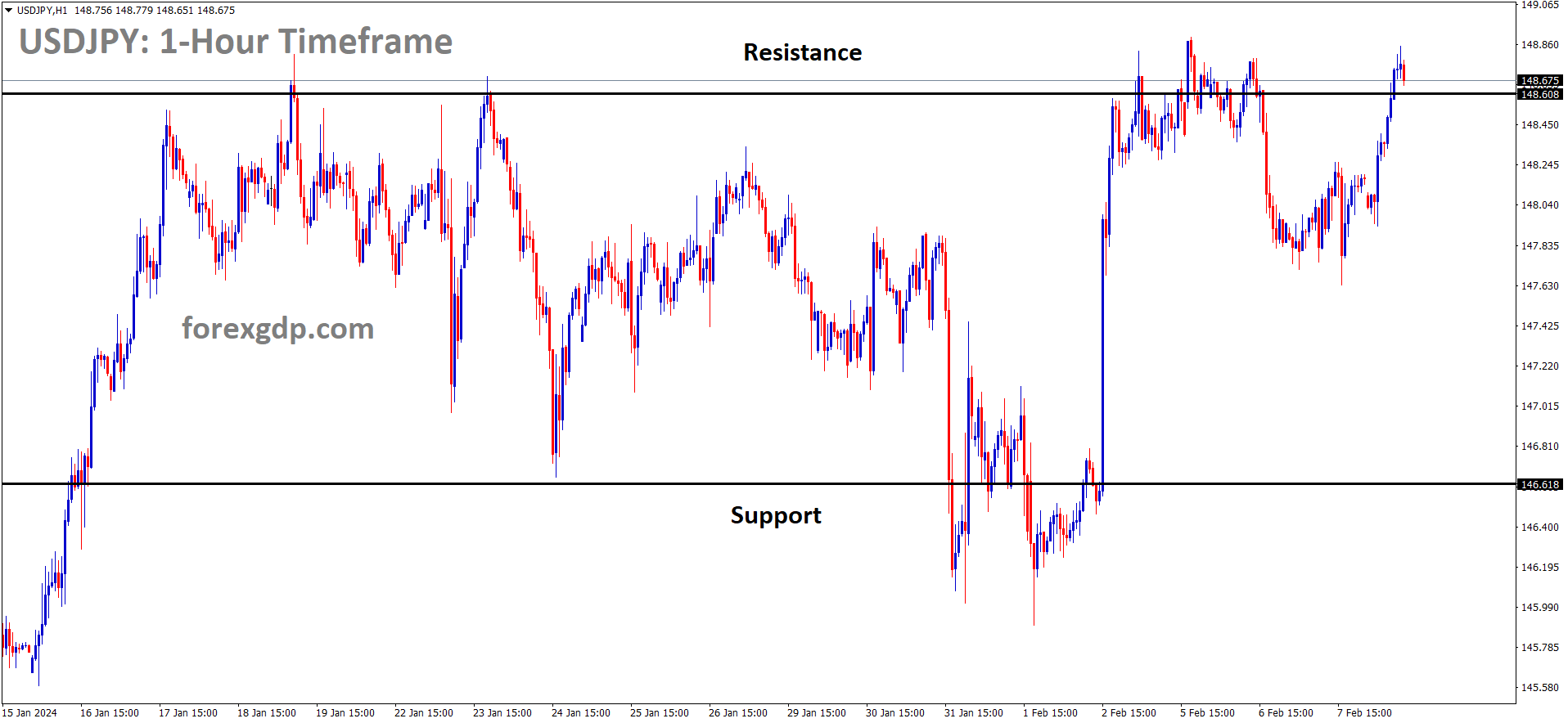

USDJPY – Yen Bears Hold On, Await Move Past Multi-Decade Low

The Inflation adjusted Wages for the February month came at -1.3% from -1.1% printed in the January month. The Japan Current account surplus came at 2.64 Trillion Yuan it is the highest reading since October 2023. The Japanese Yen weakness due to Easing of tensions in the middle east and requirement of Safe haven JPY is lowered.

USDJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

The Japanese Yen (JPY) faces continued downward pressure for the second consecutive trading day on Monday, hovering just above a multi-decade low as the European session begins. The cautious stance of the Bank of Japan (BoJ) regarding any further tightening of monetary policy indicates a persistent gap between US and Japanese interest rates. This divergence, coupled with diminishing geopolitical tensions and a generally positive risk sentiment, contributes to the JPY’s retreat from its two-week peak against the US Dollar (USD) attained on Friday.

Simultaneously, the optimistic US employment report released last Friday suggests a potential delay in interest rate cuts by the Federal Reserve (Fed), bolstering US Treasury bond yields and attracting buyers to the USD. This dynamic serves as another tailwind for the USD/JPY currency pair. However, speculations surrounding potential intervention by Japanese authorities to curb further depreciation of the JPY could limit gains for the currency pair, especially ahead of significant US data releases scheduled for this week.

In a broader market context, the Japanese Yen appears vulnerable amid the BoJ’s dovish monetary policy outlook and a positive risk environment. The BoJ’s cautious stance following its March monetary policy meeting, coupled with softer wage data from Japan, has contributed to the JPY’s decline. Additionally, reports of progress in ceasefire talks in Gaza have bolstered investor confidence, further undermining demand for the safe-haven JPY.

Japanese government officials have continued verbal interventions to support the domestic currency, albeit with limited impact on JPY bulls or hindering the upward movement of the USD/JPY pair. The recent upbeat US jobs data, indicating a strong labor market with 303,000 jobs added in March and a decline in the unemployment rate to 3.8%, has shifted expectations regarding Fed rate cuts from three to two for the year, pushing US Treasury bond yields higher.

Looking ahead, market attention turns to the release of US consumer inflation figures for March, followed by the FOMC meeting minutes, for further insights into potential Fed rate adjustments in 2024. Investors will closely monitor these developments before establishing new directional trends for both the US Dollar and the USD/JPY pair.

GBPJPY – Dips as UK-Japan Interest Rate Expectations Align

The GBP feeling selling pressures after the Rates are more divergence between Japan and UK. UK have lower services PMI data in the March month as 53.1 from 53.4 in the previous month. The BoE said 2 or 3 rate cuts in this year based on incoming data. Inflation survey shows selling prices and wage inflation will be cooled in the next year. Housing prices and mortgage prices are increased in this year so far.

GBPJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

GBP/JPY experienced a slight decline of one-tenth of a percent on Friday, hovering just above the 191.000 level. This dip occurred as investors observed a convergence in interest rate expectations between the United Kingdom (UK) and Japan, eroding the advantage previously enjoyed by holding the Pound Sterling (GBP) over the Japanese Yen (JPY), consequently exerting downward pressure on the exchange rate.

The diminished inflation outlook in the UK has led to speculation among investors that the Bank of England (BoE) may opt for an interest rate cut in June. Such anticipation has weighed on the Pound Sterling as lower interest rates tend to deter foreign capital inflows.

Conversely, in Japan, the Bank of Japan (BoJ) raised interest rates from their exceptionally low, negative 0.1% level during the bank’s March meeting. This decision sparked speculation among investors regarding whether it signifies a one-off adjustment or heralds the beginning of a series of rate hikes that could bolster the Yen over the long term.

In a recent interview with the Asahi Shimbun, Bank of Japan Governor Ueda hinted at the possibility of further interest rate hikes in light of accelerating inflation. Ueda highlighted that the positive outcomes of the Shunto spring wage negotiations are expected to translate into higher wages throughout the summer, subsequently leading to elevated consumer prices later in the year.

Meanwhile, recent data from the Bank of England (BoE) Decision Maker Panel (DMP) survey for February indicated a cooling trend in selling prices and wage inflation anticipated by most firms over the next year. Selling price expectations decelerated to 4.1% from 4.3%, marking the lowest reading in over two years, while wage growth expectations softened to 4.9% on a three-month moving average basis from 5.2% in February.

Bank of England Governor Andrew Bailey’s acknowledgment of market expectations for two or three rate cuts this year as “reasonable” has further fueled speculation that the BoE might indeed implement a rate cut in June.

Soft Services Purchasing Managers’ Index (PMI) data for March, released on Thursday, added to the rationale for a potential rate cut by the BoE, as it suggested a slight deterioration in the UK’s economic outlook. The UK Services PMI fell to 53.1, missing both expectations and the prior reading of 53.4.

However, amidst the somewhat negative economic indicators, not all data from the UK has been bleak. A recent report by the UK’s largest building society, Nationwide, indicated the first rise in house prices since January 2023, according to the Guardian. This positive development follows BoE lending data, which revealed a surprising uptick in Mortgage Approvals, rising to their highest level since September 2022 in February.

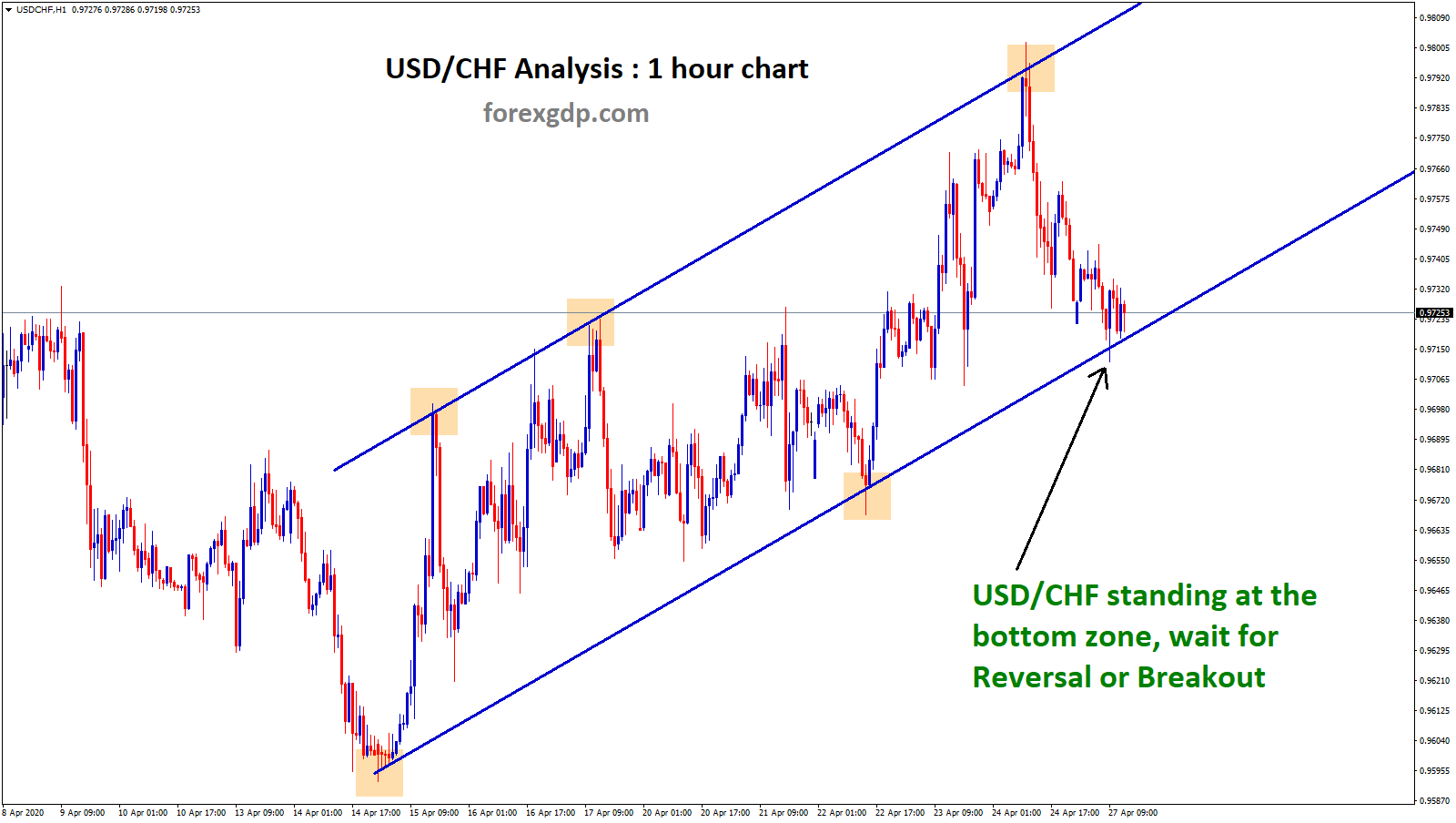

USDCHF – Swiss Government’s ‘Too Big to Fail’ List May Impose Stricter Regulations on UBS

The Swiss Government said banks have to proper regulated and more liquidity has to maintain in order to avoid too big to fail like Credit Suisse collapse of regulations carelessness. UBS have $1.7 trillion Balance sheet it is two times bigger than Swiss economic output. UBS has to allocate the funds properly and maintain proper asset management of 15% in its holdings as per Swiss lower parliament requirement.

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

Since stepping in to aid its struggling counterpart Credit Suisse a year ago, UBS has been awaiting directives from authorities regarding safeguarding Switzerland from the potential collapse of its sole remaining major bank. The Swiss government is set to unveil its recommendations for regulating banks deemed “too big to fail” this month, a move that may subject UBS to more stringent business regulations.

The forthcoming report, expected to span several hundred pages, will attract particular attention to the section concerning capital requirements. UBS could potentially face the need to allocate tens of billions of additional dollars to fortify itself against a crisis akin to that experienced by Credit Suisse.

Stefan Legge, an economist at the University of St. Gallen, emphasized the imperative of preventing UBS from failing, citing the catastrophic repercussions it would have on the Swiss economy. With a balance sheet totaling approximately $1.7 trillion—double the size of Switzerland’s annual economic output—UBS wields exceptional influence within the country’s financial landscape.

The absence of local competitors capable of absorbing UBS in the event of its collapse raises concerns about the financial strain that nationalization would impose on public finances, according to experts.

In May 2023, the Swiss lower house of parliament endorsed a proposal stipulating that systemically significant banks must maintain a leverage ratio of 15% of assets—an amount significantly higher than requirements in the European Union, the United States, and Britain.

With a common equity tier 1 capital of $79 billion, UBS recorded a ratio of 4.7% by the end of 2023. Adhering to the proposed higher ratio would likely necessitate UBS to secure well over $100 billion in additional equity, as noted by Andreas Ita from consultancy Orbit36.

Ita further observed that achieving such a substantial increase in equity through profit retention or capital market fundraising within a reasonable timeframe is implausible. However, he suggested that the bank could potentially mitigate the requirement by reducing its balance sheet and curtailing credit provision.

USDCAD – Holds Firm Near 1.3600 After Trimming Advances

The Canadian Dollar moved down after the Israel announced Cease Fire talks with Hamas on Sunday. War peace makes fears down in the market and Oil consumption, shipping will be easier for imports and exports. So Oil Demand gets slump by OPEC+ cuts in the recent meetings. So revenue from Oil industry will get slip in the Canadian economy. BoC have to hold the rates in this week as widely expected.

USDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

During the Asian trading hours on Monday, the USD/CAD currency pair continues its trend of successive gains, maintaining a higher trading position around the 1.3600 mark for the third consecutive session. This upward movement is attributed to the strengthening of the US Dollar (USD), which is supported by an increase in US Treasury yields. The elevated yields provide a supportive backdrop for the USD/CAD pair, pushing it higher.

Furthermore, the Canadian Dollar (CAD) faces additional downward pressure due to a decrease in crude oil prices. This decline in oil prices impacts the CAD negatively because Canada is one of the largest exporters of crude oil to the United States (US). Specifically, the West Texas Intermediate (WTI) oil price continues to slide, reaching approximately $85.10 per barrel at the time of reporting. The drop in oil prices further weighs on the CAD, contributing to the overall upward trajectory of the USD/CAD pair.

Israel’s decision to withdraw additional troops from Southern Gaza appears to be a response to mounting international pressure. Furthermore, peace negotiations between Israel and Hamas have recommenced in Egypt. This diplomatic development is contributing to a reduction in tensions that had previously fueled the recent surge in oil prices.

Following the release of weaker domestic employment data on Friday, the Canadian Dollar (CAD) faced challenges in the currency markets. This downturn occurred as investors digested the news and shifted their focus towards the upcoming interest rate decision by the Bank of Canada (BoC), slated for Wednesday. Market expectations are leaning towards the BoC maintaining its current interest rate at 5.0%.

As of the latest available data, buoyed by a remarkable performance in the US labor market. The Nonfarm Payrolls (NFP) report for March exceeded expectations, with a notable increase of 303,000 jobs. This figure surpassed the anticipated 200,000 jobs, although the previous growth figure of 275,000 was revised downward slightly to 270,000. The positive NFP report has strengthened the bullish sentiment surrounding the US Dollar.

In light of the robust employment data, the probability of a rate cut, as indicated by the CME FedWatch Tool, has diminished to 46.1%. Market participants are now eagerly awaiting the release of the US Consumer Price Index (CPI) data for March, scheduled for Wednesday. This data will provide further insights into the state of the US economy and potentially influence future monetary policy decisions by the Federal Reserve.

USD INDEX – Yellen: Global Concerns Rise on China’s Excess Capacity

The US Treasury Secretary Janet Yellen met with China Governor on Friday through Monday. Janet Yellen said China is doing overcapacity production it is the biggest threat to other western nations. Excess supply in the Domestic market makes exports to other countries, it is not issue, but over production of Semiconductors, Solar panels and advanced technologies is the threat to competitors in the Global world. We have to give business for others not fully occupying space in the Full sectors. China said US put tariffs on China imports in US. One Third of US Companies treated as low when compared to local china companies in China is claimed by US Companies to US Government. This is tit for Tat scenario going between US and China on Business models.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

This meeting did not change whole business model between US and China, they are just saying the concerns about china and welfare about Global countries due to China excess production.

U.S. Treasury Secretary Janet Yellen addressed mounting concerns on Friday regarding the global economic implications stemming from China’s excessive manufacturing capabilities. This issue took precedence during four days of economic deliberations with Chinese officials.

Yellen emphasized that China’s size renders it unsustainable to pursue rapid growth solely through exports. She stressed the imperative for China to alleviate its surplus industrial capacity, which is exerting pressure on other economies. Her remarks, delivered to an audience of approximately 40 representatives of the American Chamber of Commerce in Guangzhou, underscored the intensification of existing overcapacity problems and the emergence of risks in new sectors.

During her visit to Guangzhou, where she engaged with Vice Premier He Lifeng and Guangdong Province Governor Wang Weizhong, Yellen expressed growing apprehension within the Biden administration regarding China’s overproduction across various sectors such as electric vehicles, solar panels, and semiconductors. She highlighted the adverse effects on both China and producers in other nations, advocating for a transition away from state-driven investment toward market-oriented reforms.

In addition to economic concerns, Yellen emphasized areas of mutual interest between the U.S. and China, including combating climate change and addressing illicit finance. She disclosed the ongoing efforts of a financial working group, comprising representatives from both nations, aimed at mitigating financial risks associated with potential bank failures.

Despite escalating tensions between the two countries, Yellen stressed the importance of maintaining open communication on challenging issues like overcapacity and national security-related economic restrictions, emphasizing the expectations of the global community.

While Yellen refrained from issuing direct threats of new trade barriers during her visit, some trade experts interpret the heightened U.S. criticism of China’s economic model as a precursor to potential tariff adjustments aimed at protecting U.S. industries. Yellen acknowledged the possibility of further actions to safeguard American supply chains.

Moreover, she sought to address concerns regarding the deteriorating business environment for foreign companies in China, citing instances of unfair treatment compared to local competitors. Yellen urged China to rectify such practices, emphasizing the benefits of a more equitable business climate.

Chinese state media countered Yellen’s assertions, characterizing them as indicative of a double standard in international trade discourse. Nevertheless, Yellen’s discussions continue in Beijing, following recent talks between U.S. and Chinese commerce officials in Washington. Both sides raised concerns regarding overcapacity and trade-related issues, underscoring the complex dynamics shaping Sino-U.S. economic relations.

AUDUSD – Yellen: US Won’t Allow New Industries Decimated by Chinese Imports

The US Treasury Secretary Janet Yellen said China imports in the US caused US Companies threat for doing business, workers at risk in the US and Foreign countries. Lower Demand in China and investments makes Exports to other countries from China causing harmful for Foreign countries.

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

China have to stop sending goods to Russia, it facing sanctions from US. The US and China meeting outcome is no more additional tariffs, be smooth insurance climate risk.

On Monday, US Treasury Secretary Janet Yellen issued a stern warning, emphasizing that the United States would refuse to witness the demise of new industries due to Chinese imports, drawing parallels to the decimation experienced by the steel sector a decade ago.

Yellen also highlighted that discussions with Chinese officials have been fruitful in advancing American interests. She expressed particular concern over the vulnerability of workers in the US and other nations due to weak Chinese household consumption and excessive business investment.

Furthermore, Yellen reiterated the stance that financial institutions facilitating transactions to funnel Chinese goods to the Russian military would face sanctions.

The exchanges during this diplomatic trip were structured to address industrial capacity concerns comprehensively. Additionally, both the US and China have agreed to engage in further financial technical exercises aimed at enhancing operational resilience and addressing insurance climate risks.

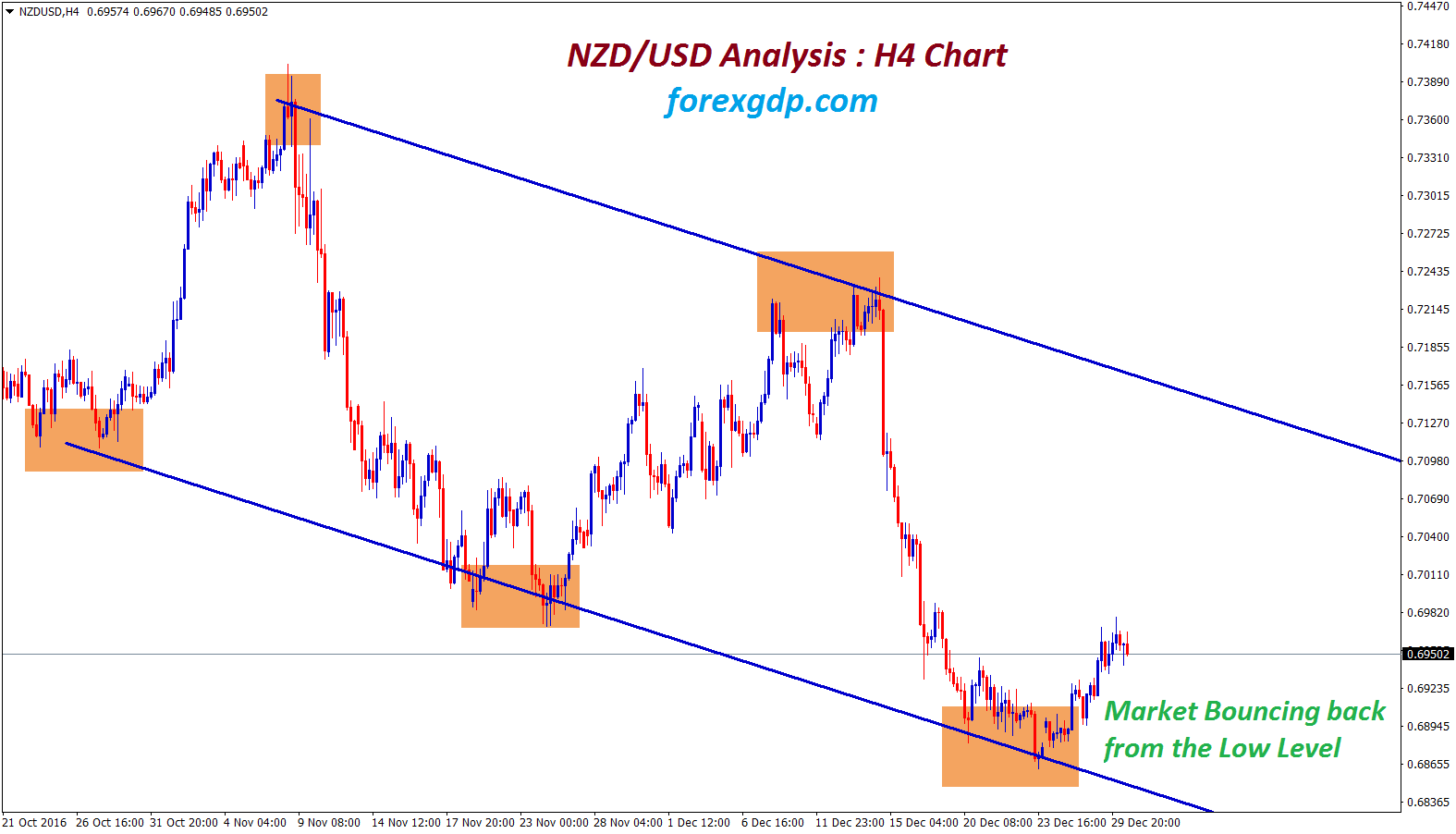

NZDUSD – Consolidates Near 0.6000, Attention Turns to RBNZ Policy

The RBNZ is expected to keep rates at 5.5% due to inflation steady above 2% target. The Kiwi economy is facing technical recession in the second half of 2023. Further economy gets vulnerable then only RBNZ doing for rate cuts.

NZDUSD has broken the Descending channel in upside

In the late Asian session on Monday, the NZD/USD pair is maintaining a sideways trajectory near the key psychological level of 0.6000. Investors are exhibiting caution and refraining from taking significant positions as they await the impending interest rate decision by the Reserve Bank of New Zealand (RBNZ), scheduled for Wednesday.

Market consensus suggests that the RBNZ will likely maintain the current interest rate at 5.5%, given the prevailing inflationary pressures which exceed the desired target of 2%. RBNZ Governor Adrian Orr has recently indicated that the central bank is on a path to restore inflation within the target band, providing some clarity to market participants.

Of particular interest to investors is the indication of when the RBNZ might commence a potential reduction in its Official Cash Rate (OCR). The uncertain economic outlook for New Zealand, compounded by the country’s technical recession experienced in the latter half of 2023, may prompt expectations of earlier rate cuts if economic conditions continue to show vulnerability.

In the broader market context, uncertainties prevail as evidenced by losses in S&P 500 futures during the Tokyo session, reflecting caution among investors. Additionally, the uptick in 10-year US Treasury yields to 4.43% underscores this sentiment. The recent release of the upbeat United States Nonfarm Payrolls (NFP) report for March has tempered speculations regarding the Federal Reserve (Fed) initiating interest rate reductions as soon as the June meeting.

Investors will closely scrutinize the inflation data for March, scheduled for release on Wednesday, for insights into the potential timing of interest rate adjustments by the Fed. This data will provide crucial cues for market participants in assessing the trajectory of monetary policy moving forward.

CRUDE OIL – WTI Rebounds Near Daily Low, Holds at $85 Amid Reduced Geopolitical Tensions

The Crudeoil prices moved down after the Israel called for Ceasefire talks with Hamas on yesterday. This sudden change of cease fire talks comes from Israel due to the Iran retaliation expected attack on Israel due to mismatch of missiles down in Iran embassy in Syria instead of Hamas areas. Already US warned Israel within 48 hours Iran retailiation on Israel, So Now Cease fire talks is only solution for Israel without expanding war further.

XTIUSD Crude Oil price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

At the commencement of a new week, Intermediate (WTI) US crude oil prices began trading with a bearish gap, marking a departure from the upward momentum that saw them reach a peak not witnessed in over five months on the preceding Friday. As the trading session progressed, the commodity experienced further declines, extending its retreat from the recent peak. Despite these losses, during the Asian session, a portion of the earlier decline was mitigated, and currently, the price hovers around the psychologically significant level of $85.00. However, it remains noteworthy that the commodity continues to trade in negative territory for the second consecutive day.

Israel has withdrawn additional soldiers from southern Gaza and has initiated fresh discussions regarding a potential ceasefire with Hamas. This development has alleviated concerns surrounding the possibility of further escalation of conflicts and disruptions to crude oil supplies originating from the Middle East.

Additionally, the optimistic US Dollar (USD) strength, fueled by positive US Nonfarm Payrolls (NFP) data, has prompted some investors to engage in profit-taking activities regarding Crude Oil prices. This move comes especially after witnessing a significant rally in the oil market over the past two months.

Meanwhile, investor concerns persist regarding Ukrainian drone attacks targeting refineries in Russia. Despite this, factors such as the OPEC+ initiative to enforce output cuts among certain member countries and a robust demand outlook continue to provide support for Crude Oil prices. Positive economic indicators from China, the world’s leading importer, further bolster confidence and pave the way for potential dip-buying opportunities in the Crude Oil market.

Given the prevailing fundamental backdrop, it is advisable to await robust follow-through selling before confirming any potential peak in oil prices in the short term. Moreover, from a technical standpoint, the recent breakthrough above the year-to-date peak, approximately around the $83.55 level, favors bullish traders, particularly considering positive indicators on the daily chart that have now moderated from overbought levels.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!