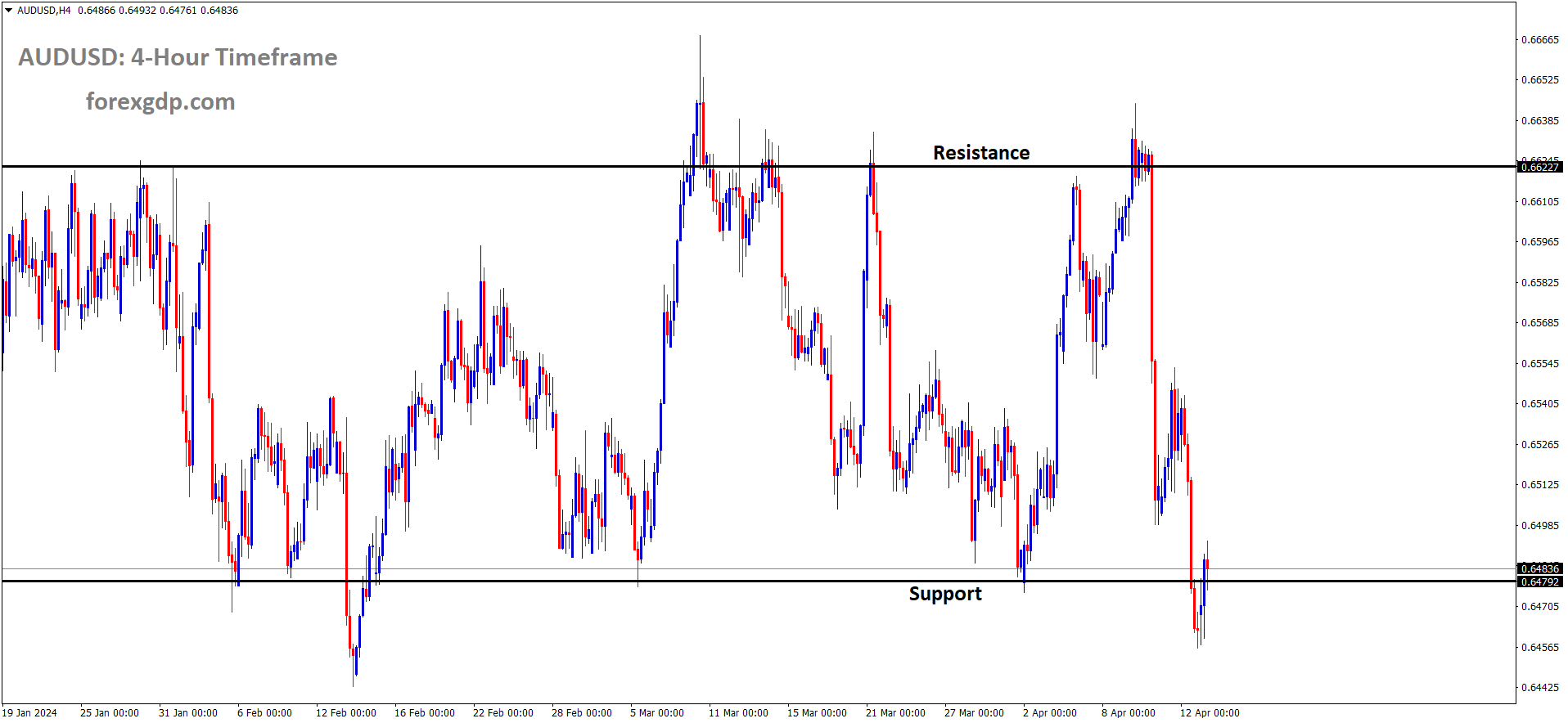

AUDUSD is moving in the Box pattern and the market has reached the support area of the pattern

AUDUSD – Aussie Dollar Holds Slight Increase with Steady USD, Focus on Retail Sales

The Australian Dollar moved lower against USD, This week CPI data is scheduled and 4.6% is expected in April month and 4.3% printed in March month. Labour data is scheduled and China kept its lending rate at 2.5% for One year term and 100 Billion Yuan is injected and Drain of 70 Billion Yuan in the One year bond rate. China GDP and Industrial production data is scheduled on tomorrow.

The Australian Dollar (AUD) staged a recovery on Monday, bouncing back from the eight-week low it hit last Friday at 0.6456 against the US Dollar (USD). However, the AUD/USD pair faced resistance as traders sought safety in the US Dollar amidst heightened tensions in the Middle East.

Further challenges lie ahead for the Australian Dollar as the ASX 200 Index declined, reflecting investor apprehension regarding a potential retaliatory response from Israel following Iran’s attack on Saturday. Iran launched explosive drones and missiles targeting military sites in Israel, with Israel reportedly intercepting the majority of the incoming projectiles, according to Reuters reports.

Despite the hawkish sentiment surrounding the Federal Reserve’s (Fed) monetary policy outlook, the US Dollar Index (DXY) edged lower due to subdued US Treasury yields. Strong US inflation and positive macroeconomic indicators have prompted the Fed to reconsider its stance on monetary easing. Market participants are eagerly awaiting the release of US Retail Sales figures on Monday, along with speeches from Fed officials.

Market Movers:

– Australia’s Consumer Inflation Expectations for April rose to 4.6%, up from the previous increase of 4.3%.

– Australian labor market data, including seasonally adjusted Employment Change and Unemployment Rate for March, is scheduled for release on Thursday.

– The People’s Bank of China (PBoC) maintained the 1-year medium-term lending facility (MLF) interest rate at 2.5% and injected 100 billion Yuan through a one-year MLF operation, resulting in a net drain of 70 billion Yuan.

– Chinese Gross Domestic Product (GDP) and Industrial Production data are expected to be released on Tuesday.

– Boston Federal Reserve (Fed) President Susan Collins suggested ‘approximately two’ rate cuts for 2024, while also anticipating inflationary pressures to ease later in the year. She noted that although a rate hike is not currently part of the baseline scenario, it cannot be completely ruled out.

– According to the CME FedWatch Tool, the probability of interest rates remaining unchanged in the June meeting increased to 63.5% from the previous week’s 46.8%.

– The US Michigan Consumer Sentiment Index for April decreased to 77.9, down from the previous reading of 79.4 and below the market expectation of 79.0, as reported by the University of Michigan.

– The Core US Producer Price Index (PPI) report for March showed a year-on-year increase of 2.4%, exceeding the market expectation of a rise to 2.3% from the previous 2.1%.

XAUUSD – Gold Holds Modest Gains Amid Geopolitical Risks, Lacks Momentum

The Gold prices are moved flat after the US said to Israel we will not take part against Iran in this conflict. Iran put drone attacks on Israel after the 7 soldiers killed in Iran Embassy in Syria. Fears of Geopolitical tensions little calm by US not taken into part between Iran and Israel.

XAUUSD Gold price is moving in an Ascending trend line and the market has reached the higher low area of the trend line

Gold price (XAU/USD) experienced some buying interest on the first day of the new week, halting its downward correction from the recent all-time high reached around the $2,431-2,432 range on Friday. The weekend’s escalation of tensions in the Middle East due to Iran’s attack on Israel heightened concerns about further conflict in the region, consequently bolstering demand for the traditional safe-haven asset, gold. Additionally, the subdued performance of the US Dollar (USD) provided additional support to the precious metal.

On another front, investors adjusted their expectations for the timing of the first interest rate hike by the Federal Reserve (Fed), pushing it back from June to September in response to persistent inflation pressures. This adjustment has kept US Treasury bond yields elevated, enabling the USD to maintain its strength near the year-to-date peak recorded on Friday. However, the robust USD has acted as a deterrent for gold, as it does not offer any yield, contrasting with the returns from Treasury bonds.

Market Movers:

– Iran’s direct attack on Israeli territory heightened concerns of a broader conflict in the Middle East, prompting a renewed interest in gold as a safe-haven asset.

– Although Israeli officials expressed a desire for retaliation, the US clarified its stance, indicating it would not participate in offensive actions against Iran. This tempered immediate market reactions and limited further gains for XAU/USD.

– Following the release of higher-than-expected US consumer inflation data last week, investors postponed expectations for the first Fed rate cut to September from June.

– Market sentiment now suggests the possibility of fewer than two rate cuts in 2024, compared to the Fed’s projection of three, bolstering the USD and maintaining pressure on gold prices.

– With the Fed’s hawkish stance and the USD’s bullish trend, investors may hesitate to make aggressive bets on gold ahead of key US economic data releases, including Retail Sales and the Empire State Manufacturing Index.

EURUSD – ECB’s Simkus: Over 50% Chance of More Than 3 Rate Cuts in 2024

The ECB Governing Council member Gediminas Simkus said there will be a three rate cuts in this year. Due to Global shocks of Iran-Israel conflict Rate cuts from ECB may be delayed to July from June month.

EURUSD has broken the Descending triangle pattern in downside

On Monday, European Central Bank (ECB) Governing Council member Gediminas Šimkus shared insights indicating a higher than 50% likelihood of witnessing more than three rate cuts throughout the year, as reported by Reuters.

Šimkus elaborated that potential geopolitical shocks, such as an escalation in the Israel-Iran conflict, might prompt a delay in implementing the initial rate cut. Specifically, there could be a shift from June to July for the first rate reduction, according to Šimkus’s remarks.

USDJPY – Japanese Yen Slumps Near 154.00, Hits New Multi-Decade Low vs. USD

The Japanese Yen moved lower against USD after the Iran Retaliation on Israel on Sunday.The Bank of Japan Accommodative policy settings and Policy divergence from FED to BoJ Makes JPY weakness in the market against USD.

USDJPY has broken the Ascending triangle pattern in upside

The Japanese Yen (JPY) is persisting with a heavily offered stance as the European session kicks off on Monday, hovering near a multi-decade low, approximately around the 154.00 mark against the US Dollar (USD). The Bank of Japan (BoJ) maintains a dovish outlook, signaling no urgency for policy normalization, a factor that continues to weigh on the JPY. Despite recent warnings from Japanese authorities about potential intervention to bolster the domestic currency, bullish sentiment largely remains intact.

Adding to the pressure on the safe-haven JPY is the deteriorating risk sentiment, fueled by escalating tensions in the Middle East. Meanwhile, the USD is consolidating recent gains, reaching its highest level since November. Market expectations of a delayed interest rate cut by the Federal Reserve (Fed) contribute to this strength. The persisting interest rate differential between the US and Japan further favors the USD/JPY pair.

Market Movers:

– The Bank of Japan’s cautious stance, emphasizing the maintenance of accommodative financial conditions, fails to support the Japanese Yen’s recovery from multi-decade lows.

– Japanese government officials’ attempts to verbally support the domestic currency, coupled with geopolitical tensions in the Middle East, restrain bearish momentum on the JPY.

– Escalating conflict in the Middle East, with Iran launching attacks on Israel, enhances demand for safe-haven assets like the JPY.

– US economic data, particularly concerning inflation and interest rate expectations, influence market sentiment. Investors have postponed expectations for the first Fed rate cut to September from June, supporting elevated US Treasury bond yields and the USD.

– The diverging policy outlooks of the BoJ and Fed suggest further upside potential for the USD/JPY pair, reinforcing last week’s breakout momentum.

– Market participants are awaiting US Retail Sales figures and the Empire State Manufacturing Index, along with speeches from Fed officials, to gauge USD demand and provide direction for major currency pairs.

USDCAD – Holds Above Mid-1.3700s with Modest Losses on Soft Oil Prices

The sustaining Geopolitical tensions between Israel and Iran calmed the Oil prices to lower after the US said Iam not take part against Iran in this conflict. USDCAD is moving higher after the US Statement and makes down for Crude Oil prices in the market.

USDCAD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Investor sentiment regarding the Federal Reserve’s (Fed) monetary policy has shifted, with expectations for the first interest rate cut pushed back to September from June. This adjustment follows recent US data releases indicating persistent inflationary pressures. Additionally, market participants are now pricing in fewer rate cuts for 2024 compared to the Fed’s initial projections, supporting elevated US Treasury bond yields and bolstering the USD Index (DXY) near its year-to-date peak. Consequently, this scenario should provide tailwinds for the USD/CAD pair.

On the other hand, Crude Oil prices struggle to attract buyers despite heightened geopolitical tensions following Iran’s attack on Israel over the weekend. The potential for a broader conflict in the Middle East raises concerns about Oil supply disruptions, which could negatively impact the commodity-linked Canadian Dollar (CAD) and help limit the downside for the USD/CAD pair. Thus, any subsequent declines in the pair may be viewed as buying opportunities, although caution is warranted before confirming a near-term top in spot prices.

Market focus now shifts to the US economic calendar, with the release of monthly Retail Sales data and the Empire State Manufacturing Index scheduled for later during the early North American session. Additionally, Fedspeak and broader risk sentiment will influence USD demand, while dynamics in Oil prices will continue to shape short-term trading opportunities for the USD/CAD pair.

USDCHF – Swiss Climate Policy Under Scrutiny After Court Ruling

The Swiss Government failed to maintain the climate change and fault said by European court on Monday. The Elders in Swiss are more affected by heat waves due to industrial emissions are higher than decade ago. The Swiss Government said Co2 emissions are controlled by 50.00% in 2030 and fully by 2050.

USDCHF is moving in an Ascending trend line and the market has fallen from the higher high area of the trend line

Swiss Climate Policy Under the Microscope Following Landmark Court Decision

Switzerland, renowned for its picturesque landscapes and majestic mountains, finds itself under scrutiny for its environmental practices after becoming the first nation reprimanded by an international court for inadequate action against climate change.

The recent ruling from the European Court of Human Rights has brought to light several deficiencies in Swiss policies, although experts emphasize that the affluent Alpine nation is not uniquely culpable compared to its counterparts.

According to Tiffanie Chan, a climate change law specialist at the London School of Economics and Political Science, the judgment underscores critical gaps in Switzerland’s regulatory framework but reflects broader global challenges rather than exclusive Swiss inadequacies.

Corina Heri, a postdoctoral researcher at Zurich University’s Climate Rights and Remedies Project, concurs, asserting that Switzerland’s climate policy deficiencies are not exclusive to the country.

The court’s decision, issued last Tuesday, favored Elders for Climate Protection, a Swiss association representing 2,500 women aged 64 and above. The group contended that Swiss authorities’ failure to address climate change adequately posed a severe threat to their health, particularly amid increasing heatwaves fueled by climate change.

In a significant ruling, the court determined that Switzerland’s climate policy failures infringed upon Article 8 of the European Convention on Human Rights, which safeguards the right to a private and family life.

Switzerland’s climate targets aim to reduce emissions by 50% by 2030 compared to 1990 levels and achieve carbon neutrality by 2050. However, independent monitor Climate Action Tracker deems Switzerland’s climate targets, policies, and financial commitments insufficient to align with the Paris Agreement’s objectives.

To meet its 2030 target, Switzerland must drastically reduce emissions by at least 35% by next year, a goal it has yet to achieve, having only managed to cut emissions by less than 20% by 2020.

Unlike its European Union counterparts, Switzerland heavily relies on carbon offset projects abroad to achieve its emissions reduction goals, a practice criticized as “highly problematic” by experts due to its lack of transparency and accountability.

Switzerland’s unique direct democracy system, allowing citizens to vote on various policy matters, poses a significant challenge to implementing effective climate policies. The rejection of a new CO2 law by voters in 2021 delayed climate action, although a climate bill was eventually approved in 2023.

While Switzerland’s direct democracy system can hinder swift action, experts emphasize that the government has demonstrated its ability to act decisively in emergencies, such as the bailout of Credit Suisse last year.

Moving forward, experts stress the need for Swiss authorities to prioritize effective climate action over procedural obstacles, urging the government to address climate change with urgency and commitment.

USD INDEX – USD Holds Strong at Multi-Month Highs, Geopolitics in Focus

The US Dollar moved higher after the Iran hit the military areas of Israel by Drone attacks. The UN Secretary General Antonio Guteress said it is the serious escalation of Regional conflict and it must be stopped by Several countries to conclude this serious war.

USD Index is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Last week witnessed a remarkable rally in the US Dollar (USD) amid growing expectations of a delay in the Federal Reserve’s (Fed) policy pivot and escalating geopolitical tensions. After surging over 1.5% in the preceding week and reaching its highest level since early November, the USD Index is currently in a consolidation phase, hovering around 106.00 early on Monday. The US economic calendar includes the NY Empire State Manufacturing Index and Retail Sales data, which are anticipated to provide further insights into the state of the economy.

Over the weekend, Iran retaliated with a drone assault following a suspected Israeli attack on Iran’s consulate in Damascus on April 1. The Iranian Foreign Ministry issued a statement asserting that Iran will not hesitate to take additional defensive measures to protect its legitimate interests against military aggression. Meanwhile, UN Secretary-General Antonio Guterres condemned Iran’s drone attacks on Israel, labeling them as a “serious escalation,” and urged all parties to exercise restraint to prevent a catastrophic regional conflict.

After a significant decline on Friday, US stock index futures are trading modestly higher as the new week kicks off.

GBPUSD – Rises Above 1.2450 on Fed’s Hawkish Sentiment

The BoE Policy Maker Megan Greene said inflation in the UK is more higher than US, So Rate cuts will be quite lower than expected. The BoE is expected to keep the rates at 4.75% from 5.25% in the current stance. The Surrounding Geopolitical tensions makes GBP lower against USD.

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The US Dollar Index (DXY) remains steady around the 106.00 mark, supported by the 2-year and 10-year yields on US Treasury bonds, which are currently standing at 4.91% and 4.55%, respectively. These elevated yields may provide additional strength to the US Dollar (USD) against its counterparts.

Meanwhile, the Federal Reserve (Fed) is reevaluating its monetary policy stance in light of ongoing inflationary pressures and robust macroeconomic indicators in the US. According to the CME FedWatch Tool, there has been a noticeable increase in the likelihood of interest rates remaining unchanged at the upcoming June meeting, rising to 63.5% from 46.8% the previous week.

Market participants will closely watch Federal Reserve Bank of Kansas President Lorie Logan’s participation in a panel discussion at the BoJ-IMF conference scheduled for Monday. Additionally, the release of US Retail Sales figures later in the North American session will be closely monitored for insights into the state of the US economy.

On the other hand, the Pound Sterling (GBP) experienced a decline against the US Dollar on Friday, dropping to its lowest level since November at 1.2426. Heightened tensions in the Middle East likely drove traders to seek safety in the US Dollar.

However, market expectations for interest rate cuts by the Bank of England (BoE) have been revised, with the policy rate now anticipated to decline to around 4.75% by the end of 2024, down from the current rate of 5.25%. This adjustment reflects a shift from previous forecasts, which projected a drop to 4.5% by December.

BoE policymaker Megan Greene emphasized that rate cuts in the United Kingdom (UK) should still be seen as distant possibilities, citing a higher risk of persistent inflation in the UK compared to the US. Additionally, traders will closely monitor a speech by Sarah Breeden, BoE’s Deputy Governor for Financial Stability, at the Innovate Finance Global Summit 2024 on Monday.

NZDUSD – Holds Around 0.5950 as Business NZ PSI Returns to Contraction

The NZ Business service index came at 47.5 in March month from 52.6 in February month.The BNZ Senior economists Doug Steel said that the NZ economy is expected to fall down of GDP to 2% after the Services index, manufacturing , Composite PMI fell down in this March month.

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The NZD/USD pair staged a recovery from a five-month low of 0.5927 observed on Monday, maintaining its position around the 0.5950 level during the Asian trading session. The New Zealand Dollar (NZD) encountered resistance following news that the country’s services sector regressed into contraction territory in March, as reported by the Business NZ Performance of Services Index (PSI). The PSI for March recorded a reading of 47.5, down from the previous month’s reading of 52.6.

BNZ’s Senior Economist Doug Steel expressed concerns, suggesting that the weak PSI activity, coupled with similarly subdued PMI activity from the previous week, could signal a potential decline in GDP of over 2% compared to year-ago levels. This forecast stands in stark contrast to the projections made by most analysts.

Meanwhile, market participants are poised to closely monitor a series of crucial data releases from China, New Zealand’s top trading partner, scheduled for Tuesday. These include Q1 Gross Domestic Product (GDP) figures, as well as Retail Sales and Industrial Output data for March. Attention will then turn to the release of New Zealand’s Consumer Price Index (CPI) data on Wednesday.

On the other hand, the Federal Reserve (Fed) appears to be reassessing its plans for monetary easing in light of persistent inflationary pressures and robust macroeconomic indicators in the US. The recent Core US Producer Price Index (PPI) report for March revealed a year-on-year increase of 2.4%, exceeding market expectations. Market participants are eagerly awaiting the release of US Retail Sales figures on Monday, along with a panel discussion featuring Federal Reserve Bank of Kansas President Lorie K. Logan at the BoJ-IMF conference.

CRUDE OIL – WTI Holds Steady Near $85.00 Amid Escalating Middle East Tensions

The Crude oil is moving flat after the US did not participated in war against Iran by joining hands with Israel. The IEA Forecasted 130K million barrels per day will be decreased to 120K million barrels per day is needed in 2024 due to Oil demand is decreasing on the electrical car investments.

XTIUSD Crude Oil price is moving in an Ascending channel and the market has reached the higher low area of the channel

Despite escalating tensions in the Middle East following Iran’s attack on Israel over the weekend, WTI (West Texas Intermediate) crude Oil prices struggle to attract buyers and exhibit muted trading activity during the Asian session on Monday. The commodity hovers near the $85.00/barrel mark, showing minimal changes for the day as market participants await Israel’s response to the Iranian strike before committing to fresh directional positions.

Iran’s deployment of explosive drones and missiles towards Israel on Saturday, in retaliation for a suspected Israeli attack on its consulate in Syria, marks a significant escalation in regional tensions. However, despite Israeli officials advocating for retaliation, the US has clarified its stance of refraining from participating in any offensive action against Iran. This stance dampens market reaction and acts as a limiting factor for Crude Oil prices.

Additionally, the International Energy Agency’s downward revision of the 2024 global oil demand growth forecast by 130,000 barrels per day (bpd) on Friday adds further pressure. This adjustment, coupled with last week’s unexpected build in gasoline inventories reported by the Energy Information Administration, signals a potential slowdown in fuel demand. Moreover, expectations of the Federal Reserve (Fed) delaying interest rate cuts due to persistent inflation could hamper economic activity and dampen fuel consumption.

Despite these bearish factors, mixed fundamentals keep traders cautious, resulting in subdued and range-bound price action at the beginning of the week. WTI Crude Oil prices remain near a multi-month peak reached around the $87.10-$87.15 area on April 5, serving as a crucial resistance level. A sustained breakthrough above this level could signal bullish momentum and pave the way for further upside, extending the recent uptrend observed over the past month.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!