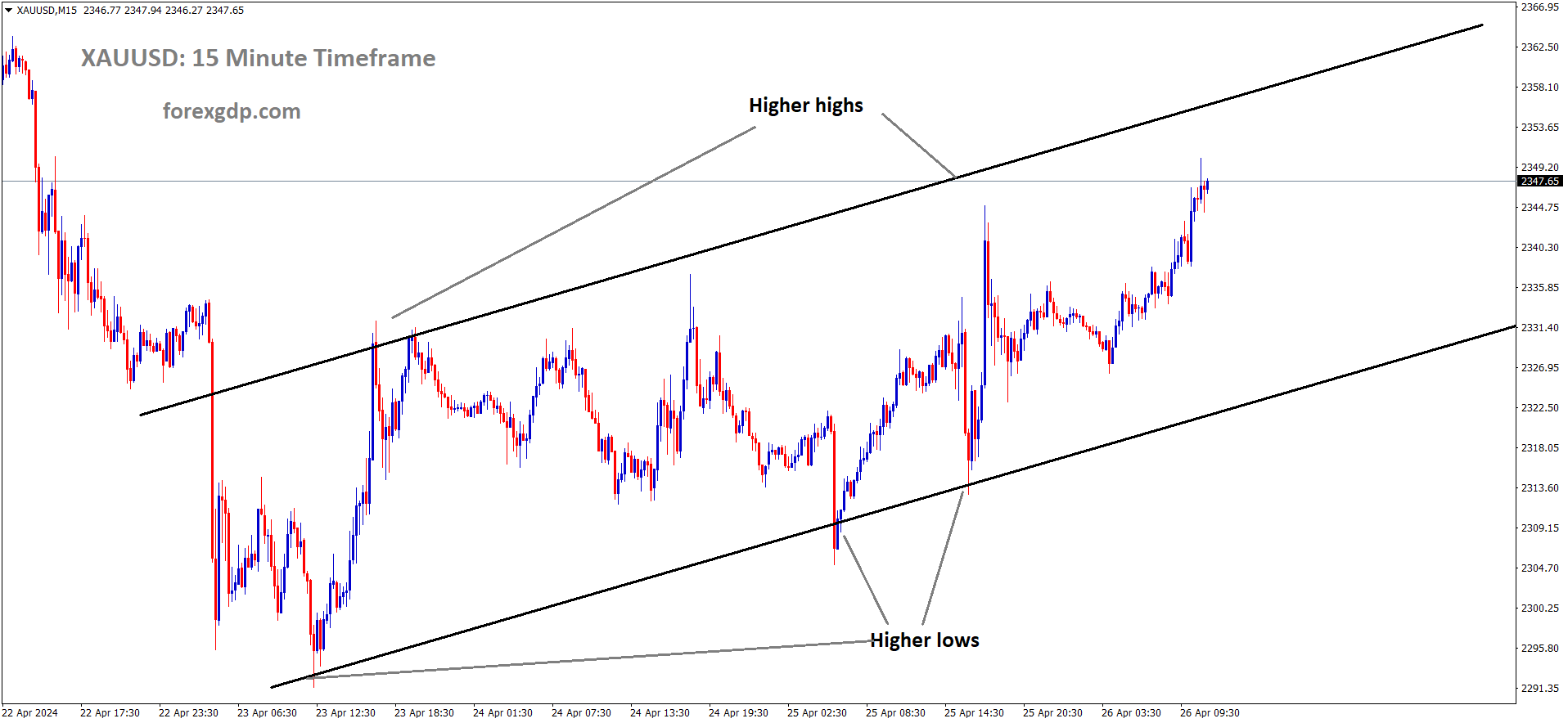

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

XAUUSD – Gold Price Trades Near Multi-Day Highs, US PCE Price Index in Focus

The Gold prices are moving in the lower against USD after the US Q1 GDP came at 1.6% lower than the expected level last day. But Inflation expectations are elevated to 3.7% this year, So rates from the FED will keep higher for longer time.

The price of gold (XAU/USD) has attracted buyers for the second consecutive day, trading just below the recent swing high as the European session approaches on Friday. The release of the US GDP report on Thursday indicated a significant slowdown in growth momentum at the beginning of 2024, coupled with an unwelcome uptick in inflation. This development is perceived to offer some support to the precious metal. However, the upward movement lacks strong bullish conviction amidst the emergence of renewed buying in the US Dollar (USD), fueled by hawkish expectations regarding the Federal Reserve (Fed).

Investors appear convinced that the Fed will postpone interest rate cuts due to persistent inflation, which keeps US Treasury bond yields elevated and bolsters demand for the USD. Additionally, the generally positive sentiment in equity markets contributes to limiting gains for safe-haven gold prices. Traders are now eagerly awaiting the release of the US Personal Consumption Expenditures (PCE) Price Index for clues about the Fed’s stance on rate cuts and to ascertain the next direction for gold.

The US GDP report released on Thursday highlighted a significant slowdown in economic growth and persistent inflation, factors seen as supporting gold prices. According to data from the US Commerce Department, the largest economy in the world expanded by 1.6% at an annualized rate in the first quarter, marking its weakest performance since mid-2022. Further details of the report revealed that underlying inflation exceeded expectations, reaching 3.7% in the first quarter, reinforcing expectations that the Federal Reserve will maintain higher interest rates for an extended period.

The yield on the benchmark 10-year US government bond surged to its highest level in over five months in response to the mixed data, acting as a headwind for the non-yielding precious metal. Additionally, easing concerns about further escalation of geopolitical tensions in the Middle East undermine the safe-haven appeal of gold and contribute to limiting its upside potential.

Meanwhile, US Dollar bulls are awaiting further signals regarding the Fed’s future rate cut trajectory, with attention focused on the release of the Personal Consumption Expenditures (PCE) Price Index. This crucial inflation data will play a significant role in shaping the Fed’s future policy decisions and influencing demand for the USD, thereby determining the short-term trajectory of gold prices.

EURUSD – bears persist above 1.0700 ahead of US PCE Data

The ECB rate cut bets more in the June month by the ECB Policy makers choice makes Euro weaker against USD. Eurozone data came at lesser than expected makes Euro currency weaker against Strong data printed US Dollar. Today US PCE Data for the month of March is scheduled.

EURUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

During the Asian trading session on Friday, the EUR/USD pair exhibits a slight downtrend, retreating from the previous day’s two-week high around the 1.0740 level. Currently hovering around the 1.0725-1.0720 range, the pair’s movement is heavily influenced by dynamics in the US Dollar (USD) as traders await the release of crucial US economic data.

Of particular interest is the US Personal Consumption Expenditures (PCE) Price Index data, scheduled for release later in the North American session. This data is closely watched by investors for insights into the Federal Reserve’s (Fed) monetary policy decisions, particularly regarding potential interest rate adjustments. Consequently, the outcome of the PCE data is expected to significantly impact short-term USD price movements.

Market sentiment suggests a growing belief that the Fed will maintain higher interest rates for an extended period, lending support to the Greenback. This sentiment is reinforced by recent data indicating that underlying inflation surpassed expectations in the first quarter. Despite a slowdown in economic growth, with the US economy expanding at a 1.6% annualized rate in the first quarter, investors remain optimistic, keeping US Treasury bond yields elevated and supporting the USD.

Meanwhile, expectations of interest rate cuts by the European Central Bank (ECB) in June due to a faster-than-expected decline in Eurozone inflation add to the downward pressure on the EUR/USD pair. However, confirmation of sustained selling pressure is awaited before concluding that the recent recovery from the year-to-date low around the 1.0600 level has come to an end. Traders remain cautious as they await the release of key US inflation data.

USDJPY – Tokyo CPI Up 1.8% YoY in April, Below 2.6% Forecast

The Japan Tokyo CPI Data for the month of April came at 1.8% YoY versus 2.6% printed in the previous reading. Japanese Yen down after the lower reading printed in the Japan.

USDJPY is moving in an Ascending trend line and the market has rebounded from the higher low area of the trend line

The latest data released by the Statistics Bureau of Japan reveals that the headline Tokyo Consumer Price Index (CPI) for April exhibited a year-on-year increase of 1.8%. This figure represents a decline from the previous reading, which recorded a 2.6% rise. Moreover, the Tokyo CPI excluding Fresh Food and Energy also showed a similar trend, rising by 1.8% year-on-year, falling short of the market expectation of a 2.7% increase. This result comes in contrast to the previous reading, which indicated a 2.9% rise.

Furthermore, the Tokyo CPI excluding Fresh Food experienced a more subdued growth, increasing by 1.6% in April. This figure is below the market consensus of a 2.4% rise, suggesting a slower rate of inflation compared to expectations.

USDCHF – climbs past 0.9100, awaits US PCE stats

The Swiss franc moved lowered against counter pairs ahead of SNB Thomas Jordan speech scheduled today. Yesterday US Q1 GDP came at 1.6% QoQ boosted US Dollar against Swiss Franc.

USDCHF is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Swiss ZEW Survey in the April month came at 17.6 from 11.5 printed in the March month.

The USD/CHF currency pair exhibits strength, hovering around the 0.9130 mark during the initial hours of the European trading session on Friday. This upward movement is supported by a modest recovery in the value of the US Dollar (USD). Investors are exercising caution, opting to stay on the sidelines ahead of an upcoming speech by the Swiss National Bank’s (SNB) Chairman Jordan. Additionally, they await the final release of the US March Personal Consumption Expenditures Price Index (PCE), a key economic indicator.

Thursday’s data from the Bureau of Economic Analysis revealed that the US advance estimate of Gross Domestic Product (GDP) for the first quarter of 2024 fell short of expectations. The economy expanded at an annualized rate of 1.6%, missing the forecasted 2.5% growth and posting a lower figure compared to the revised fourth-quarter GDP of 3.4%. This unexpected outcome prompted some selling pressure on the US Dollar.

However, the quarterly Personal Consumption Expenditure (PCE) inflation measure delivered a surprising upside, indicating that the US Federal Reserve (Fed) might delay interest rate cuts until at least September. The PCE figure recorded a notable increase, rising at an annualized rate of 3.4% in Q1, compared to the 1.8% pace observed in Q4 2023. Consequently, market expectations for rate cuts in June have diminished, with investors now anticipating only one rate cut this year, down from earlier projections of three cuts.

In Switzerland, the ZEW Survey Expectations for April showed an improvement, climbing to 17.6 from the previous reading of 11.5, as reported by the Centre for European Economic Research. Additionally, escalating geopolitical tensions in the Middle East, particularly between Israel and Iran, may lead to increased demand for safe-haven assets, benefiting the Swiss Franc (CHF).

USDCAD – nears 1.3650 on rising oil, US PCE in focus

The Israel invasion of Southern City of Gaza made supporting for Oil prices to rise up. US Crudeoil inventories are declined to 6.349 million barrels ending April 19 also supported Oil prices to rampup. Canadian Retail sales deceleration in the February month and inflation stood at 2.9% in the March month makes BoC to cut rates in the June month is more possible.

USDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The USD/CAD pair continues its downward trajectory for the second consecutive day, hovering around 1.3640 during the Asian trading session on Friday. The Canadian Dollar (CAD) is finding support from the surge in US crude oil prices, which is exerting downward pressure on the USD/CAD pair.

West Texas Intermediate (WTI) crude oil prices are inching higher, reaching close to $83.80 per barrel. This increase is driven by concerns over potential geopolitical tensions arising from the possibility of an Israeli invasion of the southern Gaza city of Rafah.

In terms of economic data, recent figures on Canadian retail sales for February pointed to a slowdown in economic activity. Furthermore, Canada’s annual inflation rate for March stood at 2.9%, falling below market expectations. This suggests the potential for weaker underlying inflation, which might prompt the Bank of Canada to consider interest rate cuts to stimulate the economy, thereby limiting the upside potential for the Canadian Dollar.

On the other hand, US labor market data offset the sluggish GDP growth, dampening expectations for interest rate cuts by the Federal Reserve. The US Gross Domestic Product Annualized (Q1) expanded at a slower pace of 1.6% compared to the previous quarter’s reading of 3.4%, falling short of market expectations. This slowdown indicates possible challenges or deceleration in various sectors of the US economy. Market focus is now shifting to the release of the US Personal Consumption Expenditures (PCE) Price Index data for March, scheduled for Friday.

Additionally, the US Initial Jobless Claims for the week ending April 19 witnessed a significant decline, dropping by 5,000 to 207,000. This figure marks the lowest level seen in two months and surpasses both market expectations and the previous reading. The unexpected decrease in jobless claims suggests a strengthening labor market, implying reduced layoffs and potentially increased hiring activity.

USD INDEX – US Core PCE Inflation to Soften Annually in March, Monthly Figure Stable

The US PCE Index data is scheduled today and expected 0.30% in the March month, Core PCE index annual rate at 2.6% is expected and Core PCE inflation index is expected at 2.6% from 2.5% in the last month. US Dollar is outperformed last day after the Q1 GDP data printed at lower than expected.

USD INDEX is moving in an Ascending channel and the market has reached the higher low area of the channel

The upcoming core Personal Consumption Expenditures (PCE) Price Index report, scheduled for release by the US Bureau of Economic Analysis (BEA) at 12:30 GMT on Friday, holds significance as it is the US Federal Reserve’s (Fed) preferred inflation gauge.

Anticipating the Federal Reserve’s PCE inflation report, analysts forecast a monthly increase of 0.3% for the core PCE Price Index in March, consistent with February’s rise. Meanwhile, the annual pace of core PCE inflation is expected to reach 2.6%, mirroring February’s figure, while headline PCE inflation is projected to edge up to 2.6% year-on-year from the previous 2.5%.

In the revised Summary of Economic Projections (SEP) published after the March meeting, policymakers indicated an expectation for annual core PCE inflation to reach 2.6% by the end of 2024, up from the 2.4% forecast in the December SEP.

Earlier this week, the BEA reported a robust 3.4% increase in the core PCE Price Index for the first quarter, significantly higher than the 1.8% growth observed in the final quarter of 2023. While this initially bolstered the US Dollar (USD), the impact on the monthly PCE figures is likely to be subdued, given the prior release of quarterly data.

In terms of market impact, the PCE inflation data is crucial, especially the monthly core PCE figure, as it offers insights into underlying inflation trends. Currently, market expectations suggest a high probability of the Fed maintaining the policy rate at 5.25%-5.5% in June. However, any deviation from forecasted figures, particularly if the monthly core PCE Price Index falls short, could prompt a brief period of USD weakness. Conversely, a surprise to the upside may not offer much room for further USD strength, considering current market positioning.

GBPUSD – softens below 1.2530 before US PCE data

The BoE Governor Andrew Bailey said inflation in the UK is cooling down and inline with expected reading. BoE Policy makers are agreed with this point, may be second quarter of 2024 rate cuts will be expected and before the FED is also possible based on the incoming data.

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The GBP/USD pair is trading at 1.2502 during the early Asian trading hours on Friday, exhibiting a weaker stance. Despite weaker-than-expected US GDP growth numbers, the US Dollar (USD) sees a modest rebound, exerting pressure on the major pair. The focus now shifts to the upcoming release of the US Personal Consumption Expenditures (PCE) Price Index data.

In Thursday’s data release, the US economy reported a slower growth rate of 1.6% in the first quarter (Q1) of 2024, down from the previous quarter’s 3.4%. This figure fell short of the market’s expectation of 2.5%. However, prices remained resilient, with the Q1 Personal Consumption Expenditures Price Index indicating a 3.4% annual rate, surpassing the Fed’s 2% target. Following this data, the Greenback dipped to a two-week low near mid-105.00.

Market sentiment regarding potential interest rate cuts by the US Federal Reserve (Fed) has shifted, with financial markets pricing in less than a 10% chance of a rate cut in June, and the likelihood dropping below 58% for a September cut. Investors are awaiting further cues from Friday’s inflation report, with expectations of a 0.3% month-on-month increase in both headline and core PCE figures. Year-on-year, the headline PCE and Core PCE figures are estimated to rise by 2.6% and 2.7%, respectively.

Meanwhile, in the UK, Bank of England (BoE) Governor Andrew Bailey and other policymakers noted a drop in inflation in line with the central bank’s projections, reducing the risk of elevated inflation. This development sets the stage for a potential rate cut. Market consensus suggests that the BoE may hold off on rate cuts until the next quarter, potentially preceding the US Fed. Such expectations may limit the upside potential of the Pound Sterling (GBP).

AUDUSD – AUD Steady, Awaits US PCE

Luci Ellis , Former Assistant RBA Governor and Chief economist of Westpac said the inflation exceeded in this March Quarter to 3.5% from 3.4% expected. So Rate cuts from RBA seen in September through November is possible. TD Securities said rate cuts from RBA is started from February 2025. Monthly CPI data for March month came at 4.1% from 3.9% printed in the February month.

AUDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Australian Dollar (AUD) maintains its upward trajectory for the fifth consecutive session on Friday, buoyed by a strengthening against the US Dollar (USD). This surge is fueled by increasing support for a hawkish stance from the Reserve Bank of Australia (RBA). The sentiment is reinforced by TD Securities’ revision of the expected rate cut timeline by the RBA, pushing it back to February 2025 from November.

Furthermore, the Australian Dollar finds additional strength from the uptick in yields of Australian government bonds, with the 10-year yield reaching a 21-week high of 4.59%. This surge follows the release of Australia’s Consumer Price Index (CPI) data earlier in the week, which exceeded expectations and fostered a hawkish outlook regarding the RBA’s monetary policy.

On the other hand, the US Dollar Index (DXY), which measures the USD’s performance against six major currencies, experiences a rebound, potentially influenced by a shift towards risk-off sentiment. However, this rebound may be limited due to a correction in US Treasury yields, contributing to the USD’s weakening.

Despite mixed preliminary data from the US on Thursday, including higher-than-expected Core Personal Consumption Expenditures and lower-than-expected Gross Domestic Product Annualized for the first quarter, the USD remains subdued.

Investor focus now turns to the US Personal Consumption Expenditures (PCE) Price Index data for March, scheduled for release on Friday. This data is expected to garner significant attention as investors assess its implications for inflationary pressures and potential impacts on US monetary policy.

NZDUSD – holds steady near 0.5950 as risk sentiment improves

The NZ- ANZ Roy Morgan Consumer confidence reading came at 82.1 in the April month from 86.4 in the March month.Consumer confidence remain elevated in the NZ economy. NZ Trade surplus for the month of March came at higher than expected, exports grown to 10-month higher, Imports fell down to 2%, due to consumer spending less in the higher rates.

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The NZD/USD pair exhibited positive movement, hovering around 0.5960 during the Asian trading session on Friday. The New Zealand Dollar (NZD), often influenced by shifts in risk sentiment, gained traction as investor appetite for risk improved, providing support to the NZD/USD pair. However, the pair experienced a slight pullback from its intraday highs due to a rebound in the US Dollar (USD).

The US Dollar Index (DXY), which measures the USD against a basket of six major currencies, edged higher, approaching 105.70. Nonetheless, the USD’s gains were tempered by a corrective movement in US Treasury yields, which contributed to the overall weakness of the Greenback.

On Thursday, mixed preliminary data from the United States (US) exerted pressure on the US Dollar. The US Gross Domestic Product Annualized (Q1) expanded at a slower pace of 1.6% compared to the previous reading of 3.4%, falling short of market expectations of 2.5%. This slowdown in economic growth suggested potential challenges or slowdowns across various sectors of the economy.

Conversely, US consumer prices displayed resilience, with the Personal Consumption Expenditures (QoQ) Price Index for Q1 rising at a 3.7% annual rate. This surpassed both market forecasts of 3.4% and the previous reading of 2.0%, indicating persistent inflationary pressures that could influence the monetary policy decisions of the Federal Reserve (Fed).

On the New Zealand front, Friday saw the ANZ-Roy Morgan Consumer Confidence dipping to 82.1 in April, down from the previous reading of 86.4. This marked its lowest level since 2008, although New Zealand’s consumer confidence remains relatively elevated. Additionally, Stats NZ reported a trade surplus in March, driven by exports reaching a 10-month high while imports fell to a 2-month low. The decline in imports reflects a sluggish economy, as both households and businesses grapple with the impact of high interest rates.

Looking ahead, investors are eagerly awaiting the release of the US Personal Consumption Expenditures (PCE) Price Index data for March, scheduled for Friday. This data is anticipated to draw significant attention as market participants assess its implications for inflationary pressures and its potential impact on US monetary policy.

CRUDEOIL – WTI climbs over $83.50 amid US GDP woes, geopolitical tensions

The US Oil moved higher after the US Stock piles down in the April ending 19 as 6.389 million barrels from the increase of 2.735 million barrels ending last week. The Israel- Gaza war increases the tensions in the Middle east makes Oil prices to rise up.

XTIUSD Oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the Channel

Western Texas Intermediate (WTI), the US crude oil benchmark, is trading around $83.60 on Friday, with prices edging higher amid a complex interplay of economic data and geopolitical tensions.

The rebound in WTI prices follows a sell-off triggered by the release of disappointing US economic growth data. According to the Commerce Department’s report on Thursday, the US economy expanded at its slowest pace in nearly two years in the first quarter of 2024, with the advanced US GDP growing by 1.6% on an annualized basis. This figure fell short of market expectations of 2.5% and marked a notable slowdown from the 3.4% growth recorded in the previous quarter. Moreover, elevated inflation levels have raised speculation that the Federal Reserve may delay any interest rate cuts until at least September.

However, WTI prices found support after Treasury Secretary Janet Yellen suggested that US economic growth may be stronger than indicated by the disappointing quarterly data.

In addition to economic factors, geopolitical tensions are contributing to the upward pressure on WTI prices. Concerns over potential oil supply disruptions have escalated amid reports of Israeli airstrikes on the southern Gaza city of Rafah, signaling preparations for a potential invasion.

Furthermore, market sentiment is buoyed by reports of the largest drawdown in US commercial crude stockpiles since mid-January. According to the Energy Information Administration (EIA), crude inventories for the week ending April 19 experienced a significant decrease of 6.368 million barrels, contrasting with the previous build of 2.735 million barrels.

Amid these dynamics, WTI prices remain in focus as traders assess the evolving economic landscape and geopolitical developments for cues on future market direction.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!