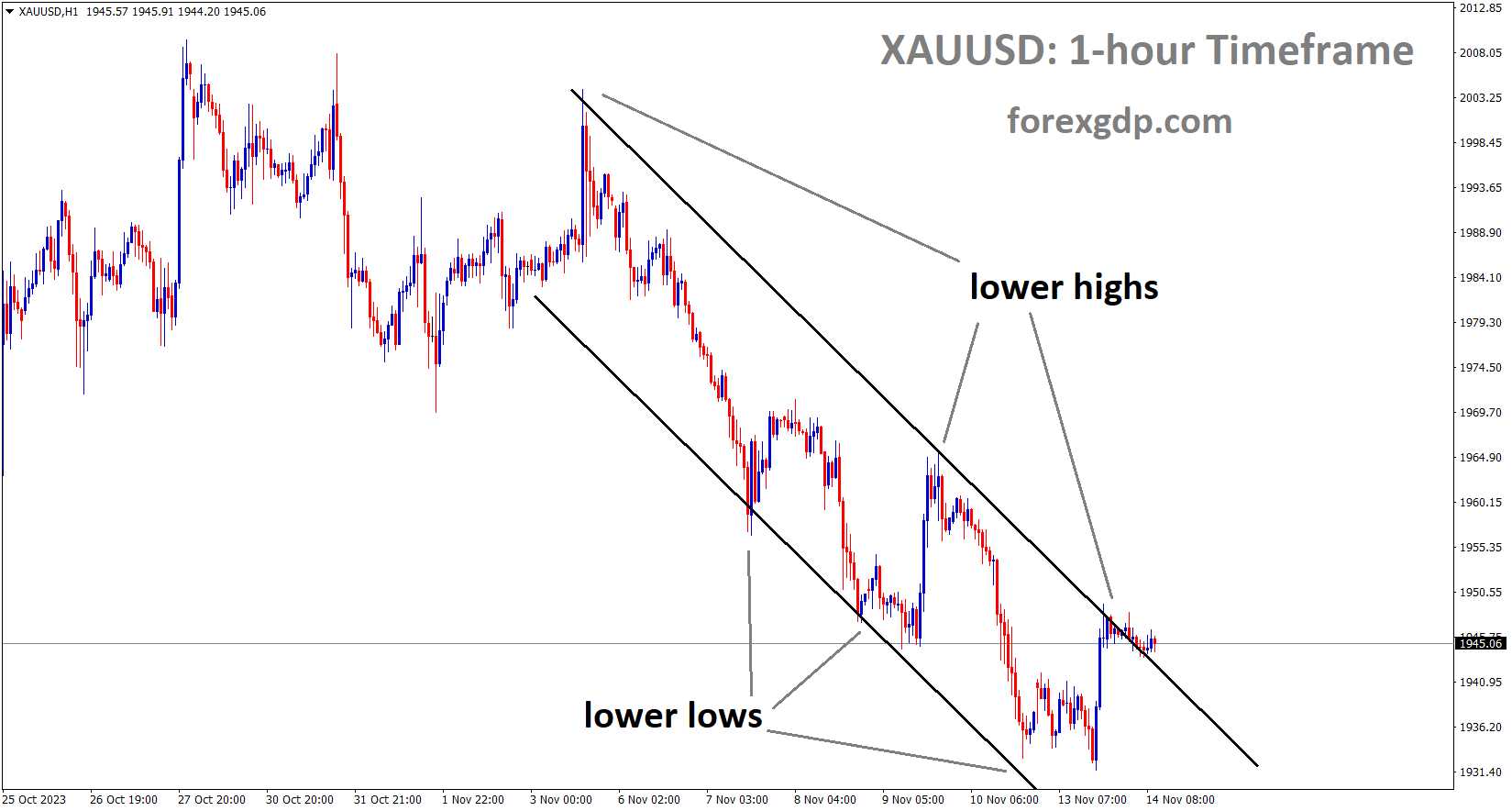

XAUUSD Gold price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

XAUUSD – Gold Bulls Pause Ahead of Key FOMC Meeting

The Israel- Hamas meeting over ceasefire talks going in Cairo makes Growing optimism in the middle east tensions. Ukraine attacked many Russian Oil refineries on Sunday with the help of US weapons. This news makes fears in the market and buying scope of Gold is increasing by the central banks.

The price of gold, represented by XAU/USD, struggled to build on its slight gains observed over the last two trading days as it dipped on the first day of the new week, although the decline was limited. Market sentiment remained firm in the belief that the Federal Reserve (Fed) would hold off on interest rate cuts, a sentiment reinforced by the release of the US Personal Consumption Expenditures (PCE) Price Index on Friday, which indicated persistent inflationary pressures. Additionally, the generally positive sentiment in equity markets acted as a deterrent to demand for gold, typically considered a safe-haven asset.

Conversely, the US Dollar (USD) faced renewed selling pressure, reversing its modest recovery from a two-week low on Friday, largely due to a sharp rebound in the Japanese Yen (JPY), fueled by speculation of government intervention. Furthermore, ongoing geopolitical tensions stemming from the Russia-Ukraine conflict played a role in supporting gold prices by keeping risk aversion elevated. Traders also opted to stay on the sidelines ahead of the crucial two-day FOMC meeting starting on Tuesday, as well as key US macroeconomic data releases scheduled at the beginning of the month, including the Nonfarm Payrolls (NFP) report.

In summary, the gold market remained subdued amidst expectations of a hawkish Fed stance, buoyant equity markets, and geopolitical uncertainties. However, the persistent inflationary backdrop, coupled with upcoming economic data releases, could influence market sentiment in the near term.

EURUSD – Stays Up Above 1.0700, Awaits German CPI Figures

The German CPI Data for April month is scheduled today, ECB President Lagarde hinted June month meeting may see a rate cut from 4.00% in the last meeting. ECB rate cuts before US is downtone for Euro against USD in the market.

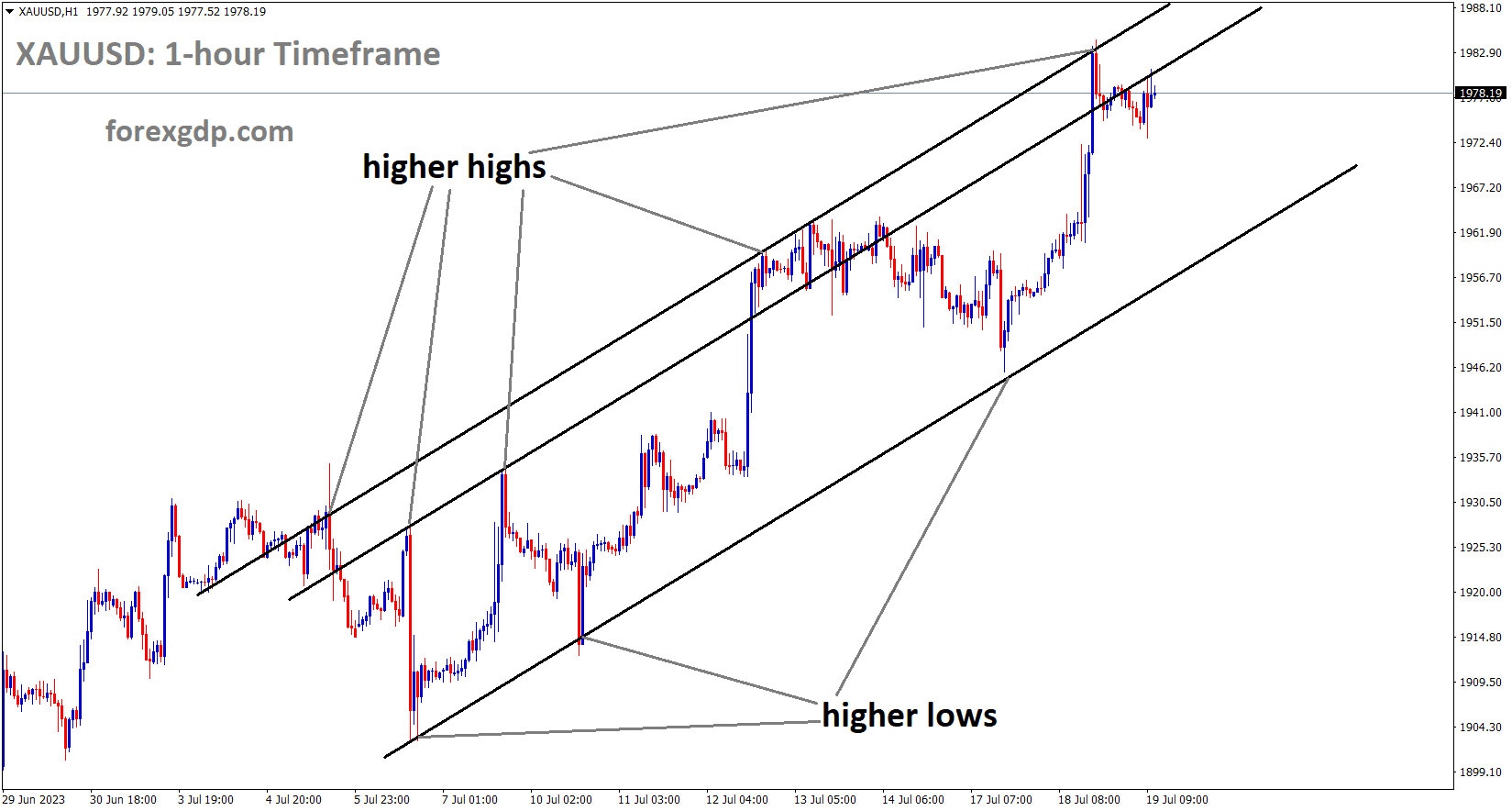

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

Market participants eagerly anticipate the release of the first reading of the German Consumer Price Index (CPI) for April, scheduled for Monday. Attention is also focused on the upcoming Federal Reserve monetary policy meeting on Wednesday, where no change in interest rates is expected.

Recent US inflation data has adjusted market expectations regarding the timing of potential interest rate cuts by the Federal Reserve (Fed). According to the CME FedWatch tool, the probability of a rate cut by the July meeting has declined from 50% last week to 25%. Traders have priced in nearly 60% odds of a rate cut at the Fed’s September meeting. This shift in expectations may buoy the Greenback and limit the upside potential of the EUR/USD pair in the near term.

On Friday, the US Bureau of Economic Analysis unveiled that the Personal Consumption Expenditures (PCE) Price Index surged by 2.7% year-over-year (YoY) in March, surpassing the previous reading of 2.5% and exceeding the estimated 2.6%. The Core PCE figure, the Fed’s preferred inflation gauge, remained stable at 2.8% YoY in March, surpassing the anticipated 2.6%. On a monthly basis, both the headline PCE and the core PCE Price Index recorded a 0.3% increase in March.

Meanwhile, the European Central Bank (ECB) has emphasized subdued inflation levels in the Eurozone and hinted at the possibility of interest rate cuts before the Fed. ECB President Christine Lagarde suggested that the central bank may commence reducing its deposit rate from the current record-high of 4% in June. However, the ECB remains cautious and has left room for flexibility in its future

USDJPY – JPY Holds Firm Near 155.00 vs. USD After Strong Recovery

The Japanese Yen sudden recovery against USD after the Japan Ruling party lose 3 seats in the By Election in Japan. This is lose confidence on Ruling PM Fumio Kishida Government by Public.But Japanese Yen sudden jump indicated is a healthy correction after the USDJPY reached 1986 level.

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The Japanese Yen (JPY) underwent a remarkable intraday reversal against the US Dollar (USD), surging by more than 500 pips from its lowest point since October 1986, recorded earlier this Monday. The sudden upturn was attributed to speculation regarding potential intervention by Japanese authorities to bolster the domestic currency, although no official announcement has been made thus far. Concurrently, renewed selling pressure on the USD contributed significantly to the downward momentum of the USD/JPY pair.

Despite the downward pressure on the USD, its decline was somewhat mitigated by growing expectations that the Federal Reserve (Fed) would postpone interest rate cuts, given the persistent inflationary pressures in the United States. This contrasts sharply with the uncertain rate outlook of the Bank of Japan (BoJ), implying that the substantial interest rate differential between the US and Japan will likely persist for an extended period. Furthermore, a positive sentiment in risk markets acted as a constraint on the safe-haven appeal of the JPY, thereby supporting the USD/JPY pair’s ability to attract buyers near the psychologically significant level of 155.00.

In recent developments, the BoJ opted to maintain its short-term interest rates unchanged during its meeting on Friday, indicating confidence that inflation would reach the targeted 2% mark in the upcoming years, potentially paving the way for rate hikes later in the year. However, Governor Kazuo Ueda provided limited insight into the timing of the next rate increase and dismissed the possibility of transitioning to a comprehensive reduction in bond purchases, urging caution among JPY bulls.

Additionally, data releases such as the Tokyo Consumer Price Index suggested a cooling inflationary trend in Japan, further dampening the JPY’s appeal as a safe-haven asset. Political developments, including the Liberal Democratic Party’s loss of three key by-election seats, also added to uncertainties surrounding Prime Minister Fumio Kishida’s tenure, potentially influencing market sentiment.

Looking ahead, investors are keenly awaiting this week’s central bank events, particularly the two-day FOMC monetary policy meeting starting on Tuesday and the highly anticipated US Nonfarm Payrolls (NFP) report, which could provide fresh insights and direction to the currency markets.

USDCAD – Pressured Below 1.3650 Amid Weaker Dollar

The Canadian Dollar moved higher against USD after the US Core PCE index came at 2.8% in the March month against 2.6% printed in the previous month.Canadian inflation rate is moving at 2.9% in the March month and it is with in 1-3% target range of Bank of Canada . BoC is expected to cut the rates in the June month is possible from economists view.

USDCAD is moving in Descending channel and the market has fallen from the lower high area of the channel

In the absence of significant economic releases from Canada, the movements of the US Dollar (USD) will remain pivotal in shaping the trajectory of the USD/CAD pair. The upcoming Federal Open Market Committee (FOMC) interest rate decision, scheduled for Wednesday, followed by US employment data on Friday, are set to be the focal points for market participants.

The conclusion of the two-day FOMC monetary policy meeting on Wednesday is not expected to bring about any changes in interest rates. However, investors will closely scrutinize the statements of Fed Chair Jerome Powell and other policymakers, anticipating a generally hawkish stance. Powell has emphasized the need for the US central bank to gain more confidence in inflation returning to its 2% target before considering rate cuts. Market sentiment reflects a diminishing likelihood of a rate cut in July, with only a 25% probability compared to 50% the previous week. Furthermore, expectations of a rate cut in September have risen to nearly 60%, as indicated by the CME FedWatch tool.

Regarding economic indicators, US inflation, measured by the Personal Consumption Expenditures (PCE) Price Index, exceeded expectations, reaching 2.7% year-over-year (YoY) in March, up from 2.5% in February. The Core PCE, preferred by the Fed, also surpassed market consensus, rising by 2.8% YoY in March.

Turning to the Canadian Dollar (CAD), the Bank of Canada’s (BoC) governing council members exhibited a division on the timing of potential interest rate cuts during their recent meeting. Canada’s inflation rate stood at 2.9% in March, within the BoC’s target range of 1-3%, while core inflation witnessed a slight decline in recent months. Market expectations lean towards the BoC initiating rate cuts possibly in June or July, a factor that could suppress the Canadian Dollar (CAD) and limit the downside of USD/CAD.

Meanwhile, the depreciation of crude oil prices adds downward pressure on the Loonie, given Canada’s significant role as a crude oil exporter to the United States (US).

USDCHF – SNB’s Jordan: Close Inflation Monitoring, Policy Adjustments as Needed

The SNB Chairman Thomas Jordan said inflation is tough stance and kept it cool by increasing rates last year and now we did rate cuts after the cool down stance. Anytime it will shoot up we have caustious on monetary policy management. If data are remain in the same stance then we do another rate cut in the next meeting.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Swiss National Bank (SNB) Chairman Thomas J. Jordan addressed shareholders at the SNB’s General Meeting on Friday, emphasizing the central bank’s commitment to closely monitoring inflationary trends. Jordan underscored the SNB’s readiness to “adjust policy again when necessary,” signaling a proactive stance in response to evolving economic conditions. This statement follows the SNB’s unexpected decision in March to reduce its main policy rate by 0.25 percentage points to 1.5%.

In his remarks, Jordan highlighted the SNB’s success in its ongoing efforts to combat inflation. However, he cautioned that despite progress, uncertainties persist, and the economy remains vulnerable to unforeseen shocks. Emphasizing the importance of maintaining price stability, Jordan reiterated the SNB’s unwavering focus on its primary mandate.

Addressing criticisms and calls for the SNB to broaden its mandate, Jordan expressed reservations, labeling such demands as “dangerous.” He warned against deviating from the central bank’s core objective of ensuring price stability, suggesting that expanding the mandate could introduce complexities and potentially undermine the effectiveness of monetary policy.

USD INDEX – USD Hits Session High After PCE Release

The US Dollar moved higher after the US PCE data came at higher than expected in the March month. Ahead of FOMC Meeting in this week, US Dollar moved higher against counter pairs.Rate cuts from July month poll is declined to 25% from 50%.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

The US Dollar (USD) demonstrates strength as it heads into the last batch of economic data for the week, following a volatile session on Thursday driven by the release of the preliminary US Gross Domestic Product (GDP) figures for the first quarter. Initially, the USD surged in response to robust readings in the Personal Consumption Expenditure (PCE) numbers, leading to speculations that interest rate cuts may be delayed further, with probabilities for December briefly surpassing those for September. However, market sentiment eventually shifted, interpreting the data as indicative of stagflationary conditions. Equities soared in response, weighing on the USD, as the possibility of rate cuts in 2024 remained on the table, dispelling earlier rumors of a potential rate hike.

Turning to economic data, the release of the Personal Consumption Expenditure (PCE) Price Index, the US Federal Reserve’s (Fed) preferred inflation gauge, did not yield any significant surprises apart from Personal Income and Spending figures. Continued consumer spending suggests that inflationary pressures persist, reinforcing expectations for a steady rate path and lending support to a stronger US Dollar.

In the global market landscape, the Bank of Japan (BoJ) maintained its interest rates unchanged, prompting the USD/JPY pair to surge to 156.80. However, the pair experienced a volatile swing during European trading hours, briefly plummeting to 155.00 before retracing back to 156.75. Market participants speculated about potential intervention by the Japanese Ministry of Finance or the BoJ.

At 12:30 GMT, the release of the Personal Consumption Expenditures (PCE) data for March included unchanged monthly headline and core PCE figures, while yearly headline PCE increased from 2.5% to 2.7%. Additionally, monthly Personal Income rose to 0.5%, and Personal Spending remained unchanged at 0.8%. Later, at 14:00 GMT, the University of Michigan released its final data for April, showing a slight decline in Consumer Sentiment from 77.9 to 77.2, while five-year consumer inflation expectations remained stable at 3%.

Equities globally are predominantly in positive territory following the Bank of Japan’s rate decision. Major indices across Asia, Europe, and US futures are trading with gains.

According to the CME Fedwatch Tool, there is an 88.5% probability that there will be no change to the Federal Reserve’s feds fund rate in June. The likelihood of a rate cut in July is minimal, while for September, the tool indicates a 44.6% chance of rates being lower than current levels. The benchmark 10-year US Treasury Note remains steady around 4.68%.

GBPUSD – Sterling Gains, Dollar Falls Before Fed Meeting

The BoE Deputy Governor Dave Ramesden said inflation is receded and 2% will reach in the May month. But chief Economist Huw Pill said Services inflation is still higher than expected levels, So rate cuts are still far way off in the market. Controversial views among BoE members makes no clarity view on BoE rate cuts in the June month.

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Pound Sterling (GBP) notches up a fresh two-week high against the US Dollar (USD), hovering around 1.2550 during Monday’s London session. The upward movement of the GBP/USD pair is attributed to buoyant market sentiment coupled with a dip in the US Dollar. The Cable strengthens amid mixed signals from Bank of England (BoE) policymakers regarding the inflation outlook, leading to heightened uncertainty regarding the timing of the BoE’s initiation of interest rate cuts.

In mid-April, BoE Deputy Governor Dave Ramsden suggested that the risks of sustained inflation had diminished. Ramsden forecasted that headline inflation would return to the 2% target in May and predicted it would likely persist at this level for the ensuing two years. However, some other BoE policymakers, including Chief Economist Huw Pill, Jonathan Haskel, and Catherine Mann, expressed less optimism about the inflation outlook. They have emphasized the significance of the core Consumer Price Index (CPI) in decision-making regarding interest rates, highlighting persistent service inflation. Last week, Pill remarked that “the time for cutting bank rate remains some way off.”

Market expectations indicate a potential shift by the BoE towards rate cuts in either the June or August meeting. James Smith, an economist at ING Financial Markets, suggested that the decision might lean slightly towards August due to considerations surrounding service inflation, although the distinction between June and August remains finely balanced.

In the broader market landscape, the Pound Sterling rallies to 1.2550, capitalizing on improved market sentiment. S&P 500 futures register significant gains during the Asian session, indicating an uptick in investors’ risk appetite. The slight decline in the US Dollar ahead of the Federal Reserve’s interest rate decision further bolsters the GBP/USD pair. However, firm expectations that the Fed will maintain a hawkish tone could provide support to the US Dollar.

The upcoming monetary policy meeting of the Federal Reserve, scheduled for Wednesday, is widely anticipated to witness a steady maintenance of interest rates within the range of 5.25%–5.50%. Fed policymakers are expected to remain data-dependent in their decision-making process, reiterating the necessity for increased confidence before considering rate cuts.

Recent consumer inflation data has failed to provide relief to Fed policymakers, with the United States core Personal Consumption Expenditure Price Index (PCE) for March indicating that elevated service prices are exerting upward pressure on prices. Annually, the core PCE inflation data rose by 2.8%, exceeding expectations of 2.6%, mirroring the pace observed in February.

Apart from the Fed’s monetary policy decision, investors will closely monitor the Institute for Supply Management (ISM) Manufacturing Purchasing Managers Index (PMI) data for April, slated for release on Wednesday. The ISM Manufacturing PMI is expected to remain above the 50.0 threshold, indicating expansion, albeit slightly lower than the prior reading. Subsequent to this, the US Nonfarm Payrolls (NFP) data, scheduled for later in the week, will serve as a crucial indicator of the current state of the labor market.

AUDUSD – AUD Shows Gains Despite Weak USD

The Australian Dollar moved higher after the Economy advisor at Judo bank Warren Hogan said there are 3 rate hike from RBA is expected in this year. First rate hike will be at November month.

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Australian CPI index points rose to 137.40 in Q1 2024 from 136.10 in Q4 2023. This reading shows good upward momentum in the Australian inflation trends.

The Australian Dollar (AUD) maintained its upward trajectory on Monday, extending a winning streak that commenced on April 22, hovering around the three-week high of 0.6560. This surge in the AUD is underpinned by a growing hawkish sentiment surrounding the Reserve Bank of Australia (RBA), fueled by last week’s Consumer Price Index (CPI) inflation data surpassing expectations.

Warren Hogan, chief economic adviser at Judo Bank, speculated that the RBA could implement three cash rate hikes throughout 2024, potentially reaching 5.1%, with the initial increase anticipated in August. Investors are keenly awaiting the release of March Retail Sales data scheduled for Tuesday, as it offers insights into Australia’s consumer spending patterns, which significantly influence inflation and Gross Domestic Product (GDP) trends.

On the other hand, the US Dollar Index (DXY), reflecting the performance of the US Dollar (USD) against six major currencies, retraced recent gains, signaling a potential shift towards a risk-on sentiment in the market. However, market analysts anticipate that the US Federal Reserve (Fed) will maintain the current interest rate range of 5.25%–5.5% in its upcoming announcement on Wednesday, likely due to concerns over elevated inflation levels. According to the CME FedWatch Tool, the likelihood of the Fed keeping interest rates unchanged in the June meeting has risen to 87.7%, up from last week’s 81.7%.

The annual US Core Personal Consumption Expenditures (PCE) Price Index data for March, released on Friday, showed an uptick, reinforcing speculation that the Fed may postpone any potential rate cuts until September.

In the stock market realm, Monday witnessed a robust surge in Australia’s stock market, spurred by a bullish performance on Wall Street. The ASX 200 Index extended its gains, with all 11 industry sectors recording positive movements following the momentum from Wall Street on Friday, driven by strong earnings reports from tech giants such as Microsoft and Alphabet, the parent company of Google, which propelled the Nasdaq up by over 2%.

TD Securities’ recent revision suggested a delay in the anticipated rate cut by the Reserve Bank of Australia (RBA) until February 2025, shifting from the previously projected date in November. This adjustment has bolstered the Australian Dollar (AUD), consequently boosting the AUD/JPY pair.

In the economic data realm, the US Personal Consumption Expenditures (PCE) Price Index increased by 0.3% month-over-month in March, matching market forecasts, with an annual rate edging up to 2.7%, above the anticipated 2.6%. The US Core PCE – Price Index, the Fed’s preferred gauge to measure inflation, rose by 2.8% year-over-year in March 2024, exceeding market forecasts of 2.6%.

Moreover, the first quarter saw a deceleration in the US Gross Domestic Product Annualized (Q1) expansion, falling short of market expectations, suggesting potential headwinds or slowdowns in various sectors of the economy.

Australia’s Consumer Price Index (CPI) rose to an all-time high of 137.40 points in the first quarter of 2024 from 136.10 points in the fourth quarter of 2023, indicating upward inflationary pressure.

NZDUSD – Holds Near Two-Week High Around 0.5975-80 Amid Weaker USD

The NZ Dollar moved higher against USD after the Israel- Hamas war is going to ceasefire soon and Cairo talks makes optimism about war escalation is going to end as all economists hopes. This move makes NZ Dollar positive against USD.

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Optimism stemming from progress in Israel-Hamas peace talks in Cairo contributed to a positive sentiment in equity markets, leading to a decline in the safe-haven US Dollar (USD) and favoring riskier assets like the New Zealand Dollar (NZD). However, expectations of a hawkish stance from the Federal Reserve (Fed) could limit the decline of the USD and restrain significant gains in the NZD/USD pair.

Investors are anticipating that the Fed will maintain higher interest rates for a longer duration, supported by persistent inflation, as evidenced by the release of the Personal Consumption Expenditures (PCE) Price Index. This hawkish outlook supports elevated US Treasury bond yields and may prompt some USD dip-buying, prompting caution among traders before positioning for further NZD/USD appreciation.

Additionally, market participants may adopt a wait-and-see approach ahead of the critical two-day FOMC monetary policy meeting starting on Tuesday. The release of key US macroeconomic data, including the Nonfarm Payrolls (NFP) report on Friday, will also play a crucial role in shaping near-term USD dynamics and determining the direction of the NZD/USD pair.

CRUDE OIL – WTI Falls Below $83.00 on Demand Worries, Supply Disruption Fears Check Decline”

The Crude Oil prices are moving lower after the US PCE data and GDP data reading came higher than last week. Israel- Hamas war talks on ceasefire is going on Cairo, positive outcome any from these meetings makes Oil prices will be dented more. Ukraine attacked Russia oil refineries, Russia already told Oil output cuts in the 2024, it will create demand if Oil refineries losing in Russia.

XTIUSD Oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

West Texas Intermediate (WTI) crude oil prices initiate the new week on a downward trajectory, slipping below the significant threshold of $83.00 per barrel during the Asian session.

The decline in WTI prices unfolds against the backdrop of diminishing concerns regarding a potential escalation of the Israel-Iran conflict. Concurrently, apprehensions arise over the impact of higher interest rates in the United States on fuel demand, given that the US is the world’s largest consumer of oil, exerting pressure on the commodity. These worries were reinforced by the release of weaker-than-anticipated US Q1 GDP growth figures last week.

Additionally, the US Personal Consumption Expenditures (PCE) Price Index, unveiled on Friday, solidified expectations of a delay in interest rate cuts by the Federal Reserve (Fed). The prevailing hawkish outlook supports a bullish sentiment surrounding the US Dollar (USD), which may continue to weigh on crude oil prices.

Moreover, recent events such as Ukraine’s attacks on Russian oil refineries over the weekend compound supply concerns. This follows Russia’s prior announcements of export and production cuts earlier in the year. Coupled with limited signs of de-escalation in tensions within the Middle East, these factors keep supply risks in play, potentially curbing significant declines in crude oil prices.

Market participants eagerly anticipate the release of official Purchasing Managers’ Index (PMI) data from China on Tuesday, given China’s status as the world’s leading oil importer, which could provide fresh impetus to the market. Subsequently, attention will turn to the outcome of the two-day Federal Open Market Committee (FOMC) policy meeting on Wednesday and crucial US macroeconomic data releases, including the Nonfarm Payrolls (NFP) report, at the onset of the new month.

Nevertheless, the complex mix of fundamental factors necessitates prudence in making aggressive directional bets and positioning for potential intraday downward movements, especially in the absence of notable economic data releases from the US on Monday.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!