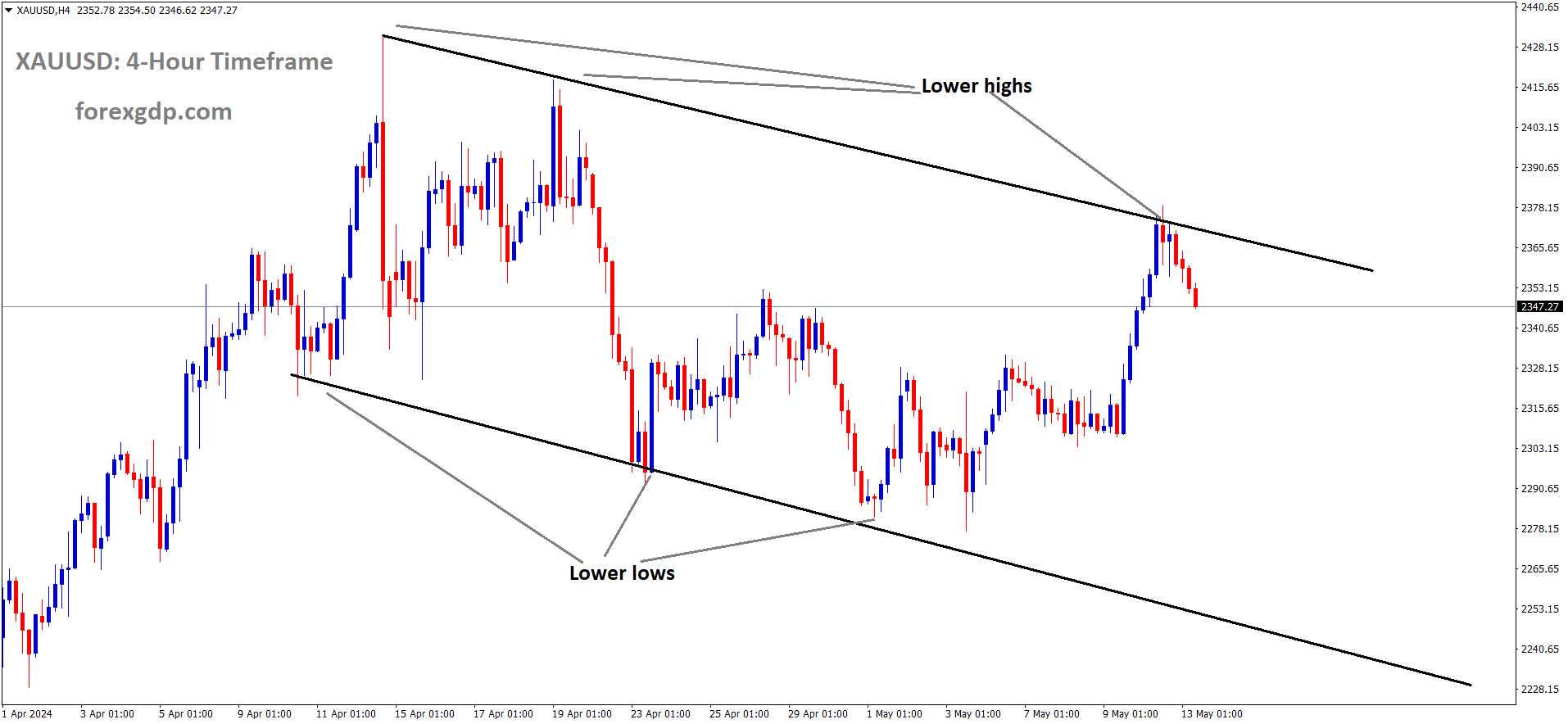

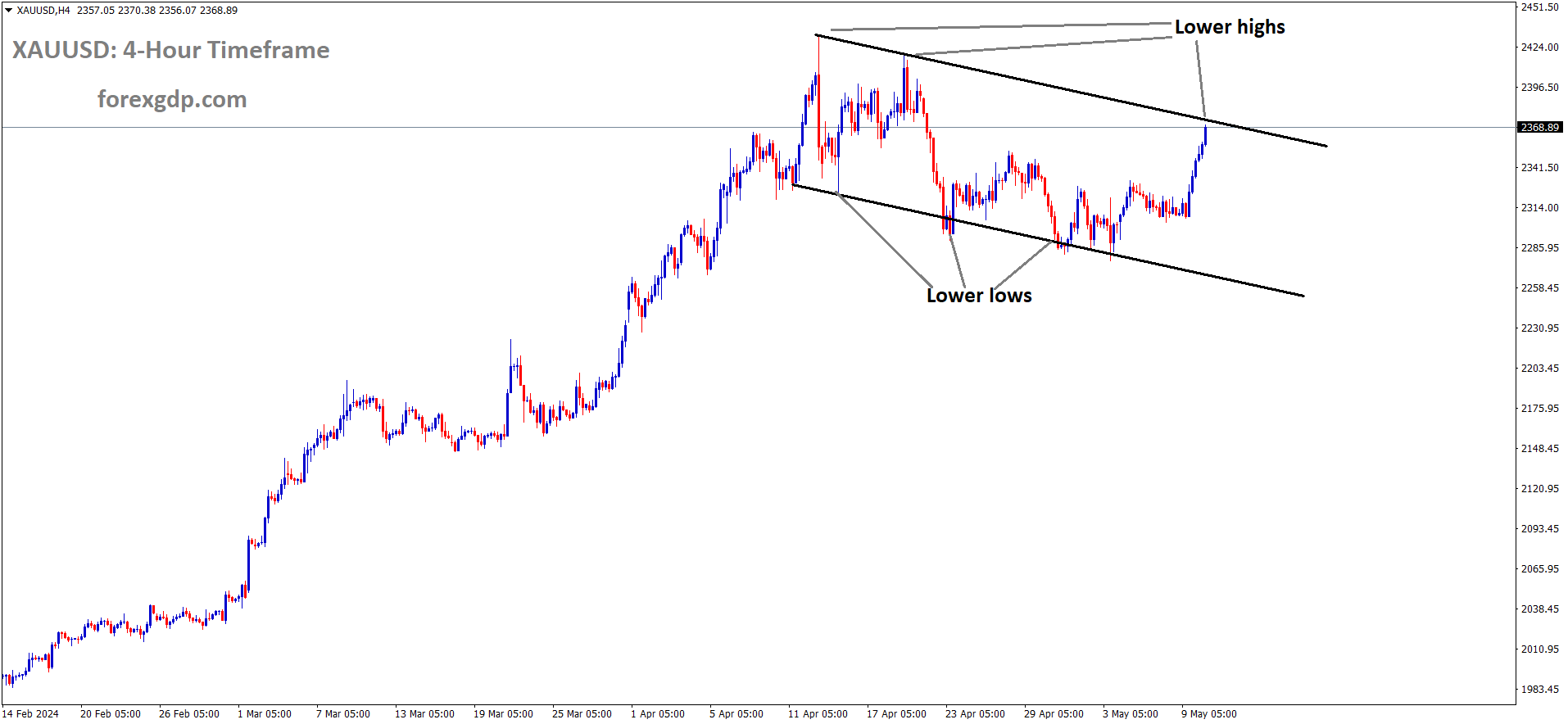

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

XAUUSD – Gold Price Draws Buyers Despite Hawkish Fed Comments

The Gold prices are moving higher after the US President Joe Biden said If Israel going to invade full south part of Gaza then we hold the supply of Weapons to Israel. US Initial Jobless claims increased to 231K from 209K in the previous week and 210K is expected. The Labour Market is cooling seen in the Initial Jobless claims increased in the last week data.

Despite a modest rebound in the US Dollar (USD) on Friday, the price of gold (XAU/USD) experienced a surge. This uptick can be attributed to several factors, including expectations among economists that a weakening labor market could prompt the Federal Reserve (Fed) to implement interest rate cuts sooner than previously anticipated, thereby stimulating economic growth. Additionally, renewed geopolitical tensions have contributed to the positive sentiment surrounding gold’s value in the market.

However, the bullish tone of recent statements from the US Fed regarding interest rates, coupled with the strength of the US dollar, may exert downward pressure on gold prices. Gold traders are closely monitoring various factors, including the first reading of the US Michigan Consumer Sentiment Index for May and speeches from Fed officials Bowman, Goolsbee, and Barr. Furthermore, attention will turn to the upcoming release of the US Consumer Price Index (CPI) report next week.

San Francisco Fed President Mary Daly highlighted the challenges posed by uncertainty surrounding the inflation outlook, emphasizing the need for more clarity before making policy projections. Meanwhile, US Initial Jobless Claims for the week ending May 4 rose to 231,000, surpassing market expectations and indicating a cooling labor market, particularly when coupled with April’s lackluster US Nonfarm Payrolls (NFP) report.

The situation in the Middle East added to market uncertainty, with Israeli forces mobilizing tanks near built-up areas of Rafah following President Joe Biden’s statement that the US would withhold weapons from Israel in the event of a major invasion of the southern Gaza city.

Despite these developments, global gold demand remained robust, driven by strong investment in the over-the-counter market, ongoing central bank purchases, and increasing demand from Asian buyers, according to the World Gold Council’s (WGC) report.

Looking ahead, the preliminary US University of Michigan Consumer Sentiment Index is expected to decline in May from April’s reading of 77.2 to 76.0, further influencing market sentiment and potentially impacting gold prices.

EURUSD – Surpasses 1.0780 Amid Broad Market Risk Appetite Rebound

The Euro currency moved higher after the US initial Jobless claims data came at higher than expected last day. FED Speaker Mary.C. Daly said inflation outlook is uncertain and Employment numbers are lower than expected. This readings are showing 70% of rate cuts in the September month and one more rate cut in the end of 2024.

EURUSD is moving in the Descending channel and the market has reached lower high area of the channel

On Thursday, EUR/USD experienced an upward trajectory, benefiting from a weakening US Dollar (USD) amid renewed speculation surrounding potential rate cuts by the Federal Reserve (Fed). The USD faced broad-based pressure following the release of US Initial Jobless Claims data, which revealed a rise to 231,000 for the week ending May 3. This figure marked the highest number of new jobless benefit claimants since August of the previous year. The unexpected uptick in jobless claims fueled concerns about the strength of the US labor market, prompting investors to shift towards riskier assets.

Market sentiment swiftly pivoted towards risk appetite as investors interpreted the rise in jobless claims as a potential signal of weakness in the US economy, heightening expectations for Fed intervention through interest rate cuts. According to the CME’s FedWatch Tool, market participants are currently pricing in nearly a 70% probability of at least a quarter-point rate cut at the Fed’s September rate-setting meeting. Additionally, there is a 67% likelihood of a second rate cut by the end of 2024, as indicated by rate traders.

Despite the growing anticipation of Fed rate adjustments, comments from Fed officials have adopted a cautious tone. San Francisco Fed President Mary C. Daly emphasized on Thursday that there remains considerable uncertainty surrounding the inflation outlook in the coming months. Furthermore, Daly highlighted that recent fluctuations in employment data appear to pose minimal risks, indicating a tempered approach towards monetary policy adjustments.

USDJPY – Suzuki: Will Act as Necessary on FX

The Japan Finance minister Shunuchi Suzuki said FX Intervention will do if necessary came. We continuously monitor the FX Moves in the market. No comments on FX Intervention data. FX Related developments on-going in the Government side.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Japanese Finance Minister Shunichi Suzuki addressed on Friday his commitment to closely monitoring movements in the foreign exchange (FX) market. He emphasized his readiness to undertake essential actions if deemed necessary to address FX-related developments.

Suzuki reiterated his stance by stating that he is closely observing FX movements and refrained from making direct comments on FX levels. However, he assured that he stands prepared to implement any required measures concerning foreign exchange matters.

The minister emphasized his willingness to take necessary actions as required, indicating a proactive approach towards managing FX dynamics. He reiterated his commitment to promptly implementing appropriate measures related to foreign exchange, without hesitation, if the situation demands.

USDCAD – BoC: Canada’s Financial System Still Strong

The BoC Governor Tiff Mackhlem said Canada Financial system is resilient and Higher rates is still needed to counter the Financial stress in the economy. Global tensions makes Financial stress in the Canadian economy and overall credit performance is Good in the Canada Banking system.

USDCAD is moving in the Descending channel and the market has fallen from lower high area of the channel

The BoC Senior Deputy Governor Carolyn Rogers said Small Business firms are more affected by higher rates, NBFCs doing more leverages for Trading purposes it will harm the Business risks. Overall Credit performance of Banks are really good.

On Thursday, the Bank of Canada (BoC) released its Financial System Review (FSR), providing insights into the current state of Canada’s financial landscape.

BoC Governor Tiff Macklem emphasized the resilience of Canada’s financial system, despite potential volatility in global markets due to shifting expectations regarding the timing and extent of rate cuts. Macklem cautioned that financial institutions are still adjusting to higher rates and potential shocks, which poses risks to financial stability. He also noted that some indicators of financial stress have increased, and the valuations of certain financial assets appear overstretched, heightening the risk of a significant correction that could lead to system-wide stress.

Senior Deputy Governor Carolyn Rogers highlighted that while the financial health of large businesses remains robust, smaller businesses are exhibiting signs of financial strain. However, evidence suggests that households are capable of servicing debt even at higher rates. Rogers noted a rise in insolvency filings among smaller firms, possibly reflecting a normalization after years of below-average filings as pandemic support measures come to an end. Additionally, in the non-bank financial sector, some firms are leveraging more to fund trading activities, rendering them more susceptible to significant market fluctuations. Despite these challenges, the overall credit performance of Canadian banks remains strong.

USDCHF – Swiss Analysis: Ukraine Summit Shifts Toward Western Embrace

The Ukraine Peace summit is going to held in Switzeraland in June 1-15 days. Last time invitation to Russia did not take part in this summit in January 2024. So This time also expected same reaction from Russia. Switzeraland is staying in the neutral stance only and bringing the peace between Ukraine and Russia through this summit as per Western nations view. But Russia said Swiss is not right to take part for mediator because Swiss Joined with EU and US stay against Russia on Sanctions process. Public preferred Swiss has to stay neutral and not to go with one side of Support on Western nations against Russia.

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel

Switzerland’s upcoming Ukraine peace summit, initially seen as a significant endeavor by the neutral nation to mediate a major international conflict, is now spotlighting the country’s evolving alignment with Western Europe over Russia, according to both proponents and critics within Switzerland.

Key Points:

– Despite Switzerland’s long-standing tradition of neutrality, its economic and security interests are increasingly converging with Western Europe, particularly amid the ongoing Ukraine conflict.

– Russia has not been invited to the June 15-16 summit at a lakeside resort near Lucerne, with Switzerland hosting at the request of Ukrainian President Volodymyr Zelenskiy.

– The summit aims to mitigate risks from Russia’s actions and isolate the country, rather than achieving immediate peace.

– While the Swiss government insists on its neutrality, it strongly condemns Russia’s aggression against Ukraine and supports solidarity with Ukraine and its people.

– The conference will address global issues such as nuclear safety, freedom of navigation, food security, and humanitarian concerns.

– Russia’s absence from the summit is justified by its lack of interest in participating, according to Switzerland, despite calls for its involvement in the process.

– Swiss efforts to include Russian allies from the Global South, such as China, highlight the potential to pressure Moscow to compromise.

– European support for the summit is growing, with leaders like German Chancellor Olaf Scholz confirming their attendance.

– Despite Switzerland’s historical neutrality, its economic ties and geographic location align it more closely with Western Europe, prompting calls for stronger alignment with Western powers.

– While the majority of Swiss citizens support neutrality, there is also increasing backing for taking a clear stand in foreign conflicts and closer ties with NATO.

– Critics argue that neutrality is outdated and risks isolating Switzerland, while proponents view it as vital for the country’s prosperity and independence.

– The Swiss Peoples’ Party (SVP) has initiated a referendum to embed neutrality in the constitution, reflecting ongoing debates about Switzerland’s role in international affairs.

USD INDEX – Forex Today: Cooling US Labor Market Keeps Dollar on Edge

The US Dollar moved flat against counter pairs after the US Labour Market cooled more than expected in the US Initial Jobless claims benefits. Next week US April month inflation reading will be projections for FED meeting in the September rate cut or not. Until US Dollar moved by FED speakers in the news.

USD INDEX is moving in an Ascending channel and the market has reached the higher low area of the channel

On Friday, May 10, the US Dollar (USD) saw a modest recovery during the Asian trading session. However, the currency’s near-term outlook remains uncertain, given the recent indications of strain in the United States (US) labor market. Higher-than-anticipated Initial Jobless Claims (IJC) for the week ending May 3 have underscored the challenges faced by the labor market in coping with the Federal Reserve’s (Fed) restrictive policy framework.

The US Dollar Index (DXY), which measures the value of the Greenback against a basket of six major currencies, experienced a slight rebound after declining to 105.00. Market participants are now closely watching for the release of April’s US inflation data scheduled for Wednesday. This data will offer crucial insights into whether the Fed might commence interest rate reductions starting from September.

Until the release of the inflation data, investors will be guided by the comments and speeches of Fed officials regarding interest rate policies. These statements will play a significant role in shaping the trajectory of the US Dollar in the coming days.

GBPUSD – UK Preliminary GDP: Q1 Growth Surpasses Expectations

The UK Q1 GDP QoQ came at 0.60% expansion versus 0.30% contraction in the previous quarter and 0.40% is expected. YoY data came at 0.20% expansion versus -0.20% contraction in the previous quarter and 0.0% is expected. GBP moving higher after the upbeat data printed in the Quarter GDP.

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The UK economy exhibited significant growth momentum in the first quarter (Q1) of 2024, expanding by 0.6% quarter-on-quarter (QoQ), according to the preliminary estimate released by the Office for National Statistics (ONS) on Friday. This marks a notable turnaround from the 0.3% contraction recorded in the previous quarter. Market analysts had anticipated a more modest expansion of 0.4% for the reported period.

On an annual basis, the UK Gross Domestic Product (GDP) recorded a growth rate of 0.2% year-on-year (YoY) in Q1 2024, compared to a contraction of -0.2% in the fourth quarter (Q4) of 2023. This performance surpassed market expectations, which had forecasted no growth (0%) in the same period.

AUDUSD – AUD Steady Near Psychological Level, Focus on US Consumer Sentiment

The Common Wealth Bank predicted the AUDUSD pair will move by 0.69 in the end of 2024 and it is down from 0.71 as previous forecasted. Inflation for Q1 dropped to 3.6% from 4.1% printed in the previous quarter. MoM data printed at 3.5% from 3.4% expected. So RBA expressed concerns over the rate cuts in the near term. RBA Projected 2-3% target of inflation range in 2025 and Mid -2026.

AUDUSD is moving in the Box pattern and the market has reached resistance area of the pattern

On Friday, the Australian Dollar (AUD) witnessed a retracement from its recent gains, following a notable rally observed on Thursday. This rally was primarily fueled by a weakening US Dollar (USD) in response to lackluster US Initial Jobless Claims data, which hinted at a potentially more dovish stance from the Federal Reserve (Fed). The downward pressure on the Aussie Dollar stemming from the Reserve Bank of Australia (RBA)’s relatively less hawkish stance was somewhat offset by the higher-than-expected inflation data.

In Australia, the inflation rate for the first quarter dipped to 3.6% from the previous quarter’s 4.1%, marking the fifth consecutive quarter of deceleration. However, it exceeded expectations by reaching 3.4%. Furthermore, the Monthly Consumer Price Index (YoY) for March surged to 3.5%, surpassing the anticipated reading of 3.4%. The RBA acknowledged the stall in recent progress in inflation control and maintained a stance of keeping options open.

The US Dollar Index (DXY), which measures the USD’s performance against six major currencies, attempted a rebound on the sentiment of the Fed prolonging higher interest rates. Nevertheless, the decline in US Treasury yields may exert pressure on the Greenback, consequently supporting the AUD/USD pair.

In the United States, the preliminary Michigan Consumer Sentiment Index for May is scheduled for release on Friday, with expectations for a slight decrease. This index serves as a gauge of consumer sentiment across various aspects, including personal finances, business conditions, and buying conditions. Additionally, Chinese Consumer Price Index (CPI) data is anticipated on Saturday, potentially influencing the Australian Dollar given the close trading ties between Australia and China.

Furthermore, market observations indicate that the Commonwealth Bank of Australia (CBA) has revised down its forecasts for the Australian Dollar at the end of 2024, citing factors such as the interest rate gap and elevated US Treasury bond yields. Moreover, RBA Governor Michele Bullock emphasized the importance of vigilance regarding inflation risks, while Societe Generale expressed concerns over the RBA’s economic growth optimism. On the US front, Federal Reserve Bank officials continue to underscore the need for moderation in economic activity to achieve inflation targets, while also signaling a steady outlook for interest rates in the near term.

NZDUSD – dips under 0.6000 post Business NZ PMI.

The Businesses in the NZ Manufacturing Activity for the month of April came at 48.9 it is well above the March month reading of 46.8 and it is well below the February month reading of 49.1. This is the 14th month contraction in the Business dull activity in the NZ economy due to higher rate surviving in the NZ, China is slowdown in the economy, China CPI data is anticipated as 0.10% in the April month due on Saturday this week.

NZDUSD has broken the Descending channel in upside

The New Zealand Dollar/US Dollar (NZD/USD) pair, after a two-day uptrend, experienced a reversal, settling around 0.6020 during Friday’s Asian trading session. This shift occurred following the release of the Business NZ Performance of Manufacturing Index (PMI), which assesses business activity within New Zealand’s manufacturing sector.

Although the PMI data for April showed improvement, with a seasonally-adjusted figure of 48.9 compared to March’s 46.8, it remained below February’s 49.1. Despite the manufacturing sector remaining in contraction for 14 consecutive months, there are indications of gradual improvement.

In the upcoming session, market attention is directed towards the Chinese Consumer Price Index (CPI) data for April, with expectations of a 0.1% increase, a release that could impact New Zealand’s market due to the close economic ties between the two countries.

The US Dollar Index (DXY), which measures the performance of the US Dollar (USD) against six major currencies, is striving for a rebound, fueled by sentiments of the Federal Reserve (Fed) maintaining elevated interest rates for a prolonged period. However, the USD encountered resistance due to diminished US Treasury yields, influenced by disappointing US Initial Jobless Claims data released on Thursday.

According to the US Bureau of Labor Statistics (BLS), the number of individuals filing for unemployment benefits surpassed expectations, with Initial Jobless Claims for the week ending May 3 rising to 231,000, exceeding estimates of 210,000 and surpassing the previous week’s reading of 209,000.

Looking ahead, market participants await the preliminary Michigan Consumer Sentiment Index for May, with forecasts indicating a slight decline. This index, which surveys consumer sentiment in the US, encompasses three primary areas: personal finances, business conditions, and buying conditions.

CRUDE OIL – WTI Rises Above $79.20 on Optimistic Chinese Demand

The China import Oil data for the month of April surged to 5.45% when compared to the previous month. The World two biggest economies demand for Oil supports the Oil prices to surge in the market. US EIA said week ending May 03 shows 1.4 million Barrels in reserve when compared to 7.3 Million Barrels in reserve last week.

XTIUSD Oil price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

On Friday, Western Texas Intermediate (WTI), the benchmark for US crude oil, is trading around $79.30, experiencing an upward movement. This increase is attributed to growing optimism regarding demand in the two largest crude-consuming nations globally, namely China and the United States.

China’s official statistics released on Thursday revealed a 5.45% rise in crude oil imports for April compared to the same period last year, signaling a promising uptick in demand. This positive development in China’s trade balance data has contributed to the upward momentum in WTI prices, as noted by Tina Teng, an independent market analyst.

Furthermore, on Wednesday, a reduction in oil inventories further bolstered WTI prices. According to the Energy Information Administration (EIA), crude inventories in the US declined by 1.4 million barrels for the week ending May 3, following a significant build of 7.3 million barrels in the previous week. This decrease aligns with market expectations, which projected a similar decline of 1.4 million barrels.

Geopolitical tensions in the Middle East have also played a role in supporting WTI prices. Israeli forces deployed tanks and engaged in gunfire near populated areas of Rafah on Thursday, prompted by President Joe Biden’s statement indicating a potential withholding of weapons from Israel in the event of a major invasion of the southern Gaza city. Such uncertainties in the region raise concerns about potential disruptions to oil supply, thereby boosting WTI prices.

However, the appreciation of the US Dollar (USD), fueled by the Federal Reserve’s (Fed) hawkish stance, may exert some pressure on USD-denominated oil prices in the near term. San Francisco Fed President Mary Daly highlighted on Thursday the challenges posed by uncertainty surrounding the inflation outlook, suggesting that policy projections remain challenging until more clarity is attained.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!