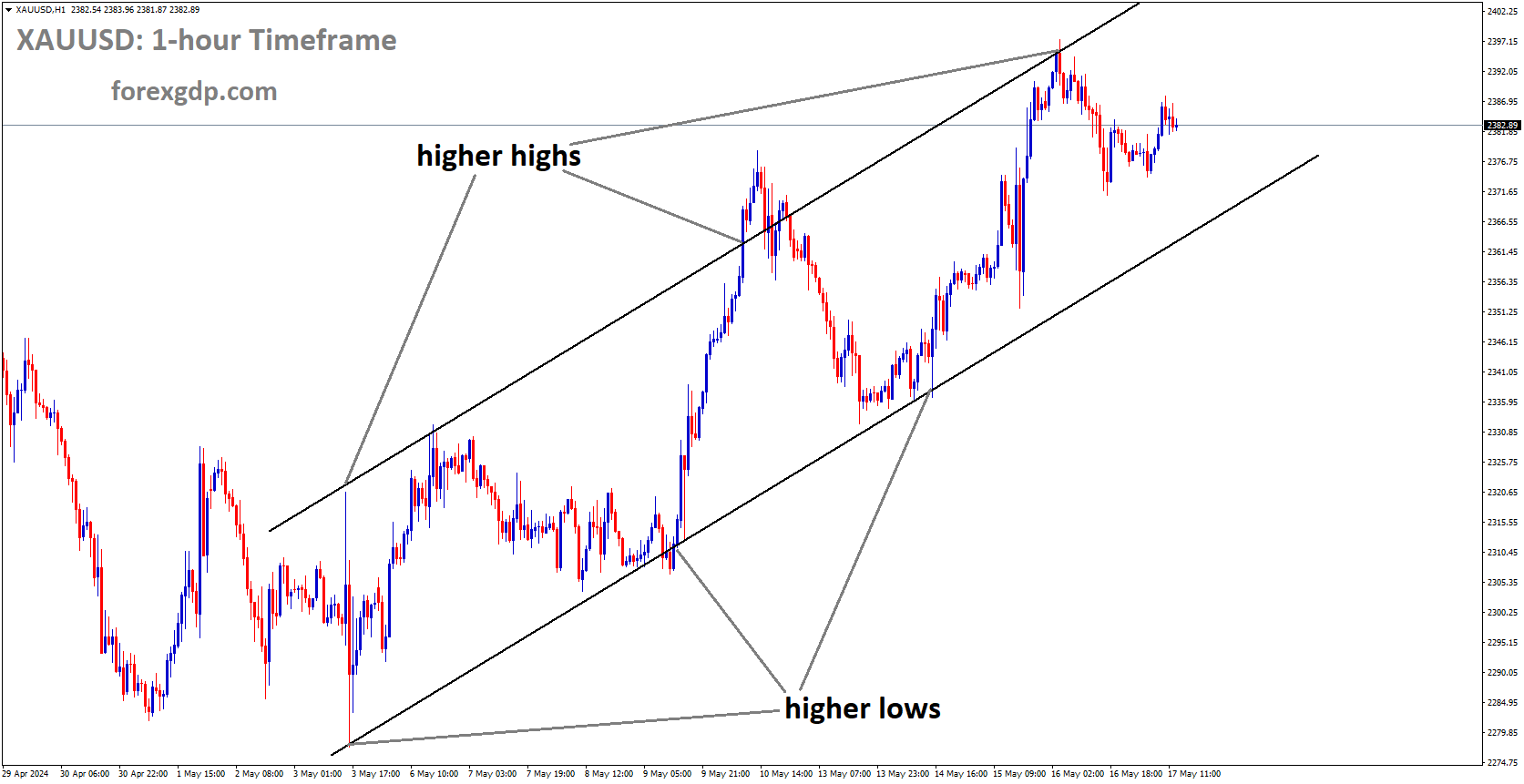

XAUUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

XAUUSD – Gold Prices Surge Amid Fed Rate Cut Hopes Despite USD Strength

Gold prices climbed on Friday, even as the USD strengthened. The increase in gold’s value was driven by softer-than-expected US inflation data, which bolstered expectations for potential rate cuts from the Federal Reserve (Fed). This optimism is beneficial for gold, as lower interest rates tend to decrease the opportunity cost of holding non-yielding assets.

However, on Thursday, Fed officials conveyed a cautious outlook, suggesting that high borrowing costs might be maintained for an extended period. This stance indicates that the Fed is not eager to reduce interest rates this year. Elevated interest rates generally support the USD, potentially putting downward pressure on gold prices by making it less attractive to investors.

With no major economic reports from the US, market participants are turning their attention to speeches from Fed officials Kashkari, Waller, and Daly later on Friday. These speeches are expected to provide insights into the Fed’s future monetary policy direction.

Recent US economic data has shown mixed results. Initial Jobless Claims for the week ending May 11 rose to 222,000, slightly above the forecast of 220,000 and up from 232,000 the previous week. In April, Housing Starts increased by 5.7% month-over-month to 1.36 million units, while Building Permits fell by 3% to 1.44 million units.

Atlanta Fed President Raphael Bostic noted signs of cooling inflation in the latest Consumer Price Index (CPI) report but emphasized the importance of monitoring data from May and June to ensure inflation does not reverse. Cleveland Fed President Loretta Mester mentioned that while current policies are well-positioned, it is premature to declare that progress on inflation has stalled. Richmond Fed President Tom Barkin stressed the need to keep borrowing costs high for longer to ensure inflation aligns with the Fed’s target, particularly pointing to persistent high prices in the services sector.

Financial markets have adjusted their expectations based on these developments. The probability of a Fed rate cut in September has risen to 75%, up from 65% earlier in the week. The CME FedWatch Tool also indicates expectations of a full 25 basis point rate cut by the end of the year.

In conclusion, while gold prices have shown resilience despite a stronger USD, the future trajectory of gold will largely depend on upcoming Fed communications and economic data. The mixed signals from recent economic reports and Fed officials suggest that market participants should be prepared for potential volatility in the near term.

EURUSD – ECB June Rate Cut Expectations Rise, Impacting EUR/USD

The EUR/USD currency pair experienced a slight decline on Thursday as the US Dollar broadly recovered from earlier losses in the week. Despite this dip, the pair remains significantly up for the trading week. This late-week movement reflects investor uncertainty regarding the Federal Reserve’s (Fed) stance on potential rate cuts, prompting many to retain their holdings in the safe-haven USD.

EURUSD is moving in Descending channel and market has reached lower high area of the channel

EURUSD is moving in Descending channel and market has reached lower high area of the channel

Market speculation around a June rate cut by the European Central Bank (ECB) has intensified. Traders have started to price in this possibility, especially after ECB Governing Council member and Governor of the Latvian central bank, Martins Kazaks, announced on Thursday that a June rate cut is a distinct possibility. The ECB’s cautious approach in recent public appearances has added to the speculation. Next week’s focus will shift to the release of Purchasing Manager’s Index (PMI) figures from both the EU and the US, which are expected to provide further market direction.

Meanwhile, Federal Reserve officials continue to dominate investor focus. Multiple policymakers from the US central bank provided insights on Thursday, with their overall tone being notably cautious. This aligns with the Fed’s strategy to temper market expectations for imminent rate cuts. Currently, the CME’s FedWatch Tool indicates that rate markets are pricing in a 70% probability of at least a quarter-point cut from the Fed in September, with a 90% chance of two total rate cuts by the end of the year.

Looking ahead to Friday, several significant speeches are scheduled, which are likely to influence market sentiment further. ECB Vice-President Luis de Guindos, along with Federal Reserve officials Neel Kashkari, Christopher Waller, and Mary Daly, are set to speak. These appearances will be closely watched as they round out the trading week and potentially set the tone for the upcoming economic data releases and central bank decisions.

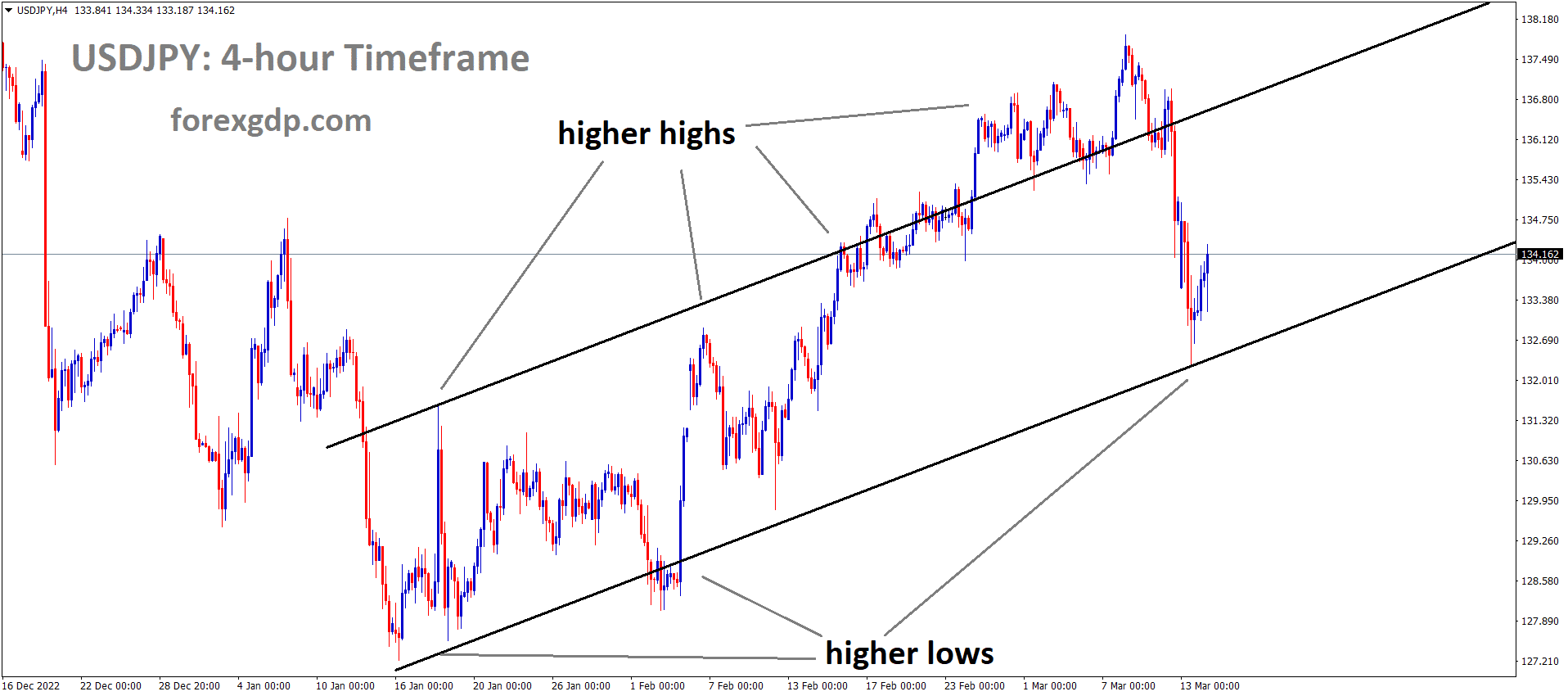

USDJPY – Climbs Amid BoJ Bond-Buying and Fed’s Cautious Stance

During the Asian session on Friday, the USD/JPY pair appreciated as the Japanese Yen (JPY) encountered renewed pressure. This development was driven by the Bank of Japan’s (BoJ) decision to maintain its bond-buying amounts from the previous operation, avoiding a surprise cut to debt purchasing that some market participants had anticipated earlier in the week.

USDJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

Speculations on BoJ’s Future Policy Decisions

There is growing speculation among traders that the BoJ might consider reducing its bond-buying activities at its policy meeting in June. This speculation is fueled by recent statements from BoJ Governor Kazuo Ueda, who noted that there are currently no plans to sell the central bank’s holdings of exchange-traded funds (ETFs). This cautious approach has left room for potential policy adjustments in the near future.

Insights from Former BoJ Economist on Interest Rate Hikes

In a recent interview with Bloomberg, former BoJ chief economist Toshitaka Sekine suggested that the Bank of Japan could raise its benchmark interest rate up to three times within the year. Sekine highlighted that the central bank has significant leeway to adjust its current monetary policy, which he described as “excessively” easy. He indicated that the first rate hike could occur as early as June, provided economic conditions support such a move.

")

US Dollar Strengthens Amid Fed’s Cautious Stance

The US Dollar Index (DXY), which tracks the performance of the US Dollar (USD) against six major currencies, showed strength after rebounding from a multi-week low recorded on Thursday. This recovery is attributed to the Federal Reserve’s (Fed) cautious stance on inflation and interest rate cuts. The Fed has signaled that it remains vigilant about inflationary pressures and is not in a hurry to reduce interest rates within the current year.

Fed Officials Emphasize Patience and Continued Vigilance

On Thursday, during an event in Jacksonville, Atlanta Fed President Raphael Bostic emphasized the importance of patience with interest rates, pointing out that significant pricing pressures persist within the US economy. Similarly, Cleveland Fed President Loretta Mester remarked that it might take longer than previously anticipated to confidently determine the trajectory of inflation. She advocated for maintaining a restrictive monetary policy stance for an extended period to ensure inflation is firmly under control.

These comments from Fed officials suggest that the central bank is prepared to maintain its current policy framework, which supports a strong US Dollar. The cautious approach from both the BoJ and the Fed reflects ongoing concerns about economic stability and inflation, influencing currency movements and market expectations.

USDCAD – Rises Amid Fed’s Cautious Stance and Mixed U.S. Data

USD/CAD pair maintained positive momentum during the early Asian trading session on Friday. This rise is driven by renewed demand for the US Dollar (USD), spurred by the Federal Reserve’s commitment to keeping interest rates high.

USDCAD is moving in Descending channel and market has rebounded from the lower low area of the channel

Federal Reserve’s Interest Rate Outlook

Federal Reserve officials have reiterated their cautious stance on interest rates. Atlanta Fed President Raphael Bostic observed cooling inflation signs but emphasized the need to monitor May and June data to prevent a resurgence. Cleveland Fed President Loretta Mester highlighted the importance of additional data to confirm that inflation is trending toward the Fed’s 2% target.

Richmond Fed President Tom Barkin stressed the necessity of maintaining high borrowing costs to ensure inflation targets are met, particularly noting higher prices in the services sector. The CME FedWatch Tool indicates that financial markets now see a nearly 70% chance of a Fed rate cut in September, up from 65% earlier in the week.

Mixed U.S. Economic Data

Recent U.S. economic data presented a mixed picture. The latest report from the US Bureau of Labor Statistics showed that weekly Initial Jobless Claims rose to 222,000 for the week ending May 11, slightly above market expectations of 220,000 but down from the previous week’s 232,000. Housing Starts increased by 5.7% month-over-month to 1.36 million in April, while Building Permits decreased by 3% month-over-month to 1.44 million. These mixed indicators had little impact on the USD, as market participants focused on the Fed’s policy direction.

Canadian Dollar and Oil Price Influence

In Canada, Manufacturing Sales fell by 2.1% month-over-month in March, following a 0.9% increase in February, as reported by Statistics Canada. This decline was sharper than the expected 1.4% drop. Nonetheless, the recent rebound in oil prices could bolster the commodity-linked Canadian Dollar (CAD), potentially capping further gains for the USD/CAD pair. As Canada is the largest oil exporter to the United States, fluctuations in oil prices significantly influence the CAD’s value.

USDCHF – Declines Amid Anticipations of Fed Rate Cuts

The USD/CHF pair is experiencing a continued decline during the European session on Thursday. This drop is driven by the weakening US Dollar, which is under pressure due to rising expectations of multiple rate cuts by the Federal Reserve (Fed) in 2024.

USDCHF is moving in Ascending channel and market has reached higher low area of the channel

The dovish sentiment surrounding the Fed has been reinforced by recent economic data from the United States. The Consumer Price Index (CPI) for April showed a modest increase of 0.3% month-over-month, falling short of the anticipated 0.4%. Additionally, Retail Sales data for the same period remained flat, also missing the expected 0.4% growth. These figures suggest a slowing economy, which has led to increased speculation that the Fed will lower interest rates to stimulate growth.

Further adding to the dovish outlook, Minneapolis Federal Reserve Bank President Neel Kashkari remarked that the Fed should maintain policy rates at their current level for an extended period to better assess the underlying inflation trends. His comments underscore the cautious approach the Fed is likely to take in the coming months.

On the Swiss economic front, there has been a slight improvement in Producer and Import Prices, which decreased by 1.8% year-over-year in April. This is a smaller decline compared to the previous month’s 2.1% drop, marking the twelfth consecutive period of decrease but at the slowest rate since December 2023. This data points to persistent deflationary pressures in Switzerland’s economy.

Looking ahead, traders are eagerly awaiting the release of the Swiss Industrial Production data for the first quarter, scheduled for Friday. This report is expected to provide fresh insights into the state of the manufacturing sector in Switzerland, covering the output of factories and other industrial entities. The findings will be closely analyzed for indications of economic health and potential future trends in the Swiss economy.

USD/CHF pair’s downward trend is driven by growing expectations of Fed rate cuts, supported by weak US economic data and cautious remarks from Fed officials. Meanwhile, improvements in Swiss economic indicators and upcoming industrial production data are key factors that traders are monitoring for future market direction.

USD Index – Rises as Pound Sterling Steadies Ahead of UK Inflation Data

Pound Sterling (GBP) is holding steady in Friday’s London session after a recent surge to a monthly high. Investor attention is now turning to the upcoming UK Consumer Price Index (CPI) data for April, set to be released on Wednesday. This data is expected to play a pivotal role in shaping the Bank of England’s (BoE) next steps regarding interest rates.

USD Index market price is moving in box pattern and market has fallen from the resistance area of the pattern

Market expectations are divided between a possible rate cut in June or August. BoE Governor Andrew Bailey has hinted that UK inflation might soon approach the 2% target, consistent with the BoE’s forecasts from February. He suggested that the next CPI release could show a significant drop, influenced by the UK’s unique household energy pricing system.

Despite the recent rally, the Pound’s upward momentum has paused amid growing market caution. This shift is partly due to hawkish remarks from Federal Reserve (Fed) officials, who have dismissed the likelihood of immediate rate cuts, even as US inflation is expected to decline in April.

On Thursday, several Fed policymakers emphasized that the current interest rate levels are appropriate for the current economic conditions. They argued that a single decline in inflation does not confirm a sustained disinflation trend, which had stalled earlier this year. Consequently, market expectations for a rate cut have been pushed to September, with the CME FedWatch tool indicating a 68% probability, down from 73% following the recent inflation data.

The Fed’s stance on maintaining higher interest rates has provided a boost to the US Dollar. The US Dollar Index (DXY), which tracks the Greenback against six major currencies, rebounded after dipping to a monthly low on Thursday. However, the index remains on track to close the week in negative territory.

Meanwhile, concerns about the US labor market persist. The Department of Labor reported on Thursday that Initial Jobless Claims for the week ending May 10 were higher than expected, totaling 222,000 and surpassing the forecast of 220,000. Although this was a decrease from the previous week’s eight-month high of 232,000, it highlights ongoing weaknesses in the job market.

Pound Sterling remains steady as investors await critical UK inflation data, which will influence the BoE’s interest rate decisions. At the same time, the US Dollar is recovering thanks to the Fed’s hawkish stance, despite lingering concerns about the labor market’s strength.

GBPUSD – Gains Capped by Expectations of BoE Rate Cuts Before Fed

The GBP/USD pair is experiencing a slight upward trend as of Friday. This movement is influenced by various economic signals from both the US Federal Reserve (Fed) and the Bank of England (BoE).

GBPUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

Federal Reserve officials have recently indicated that it might take longer than anticipated to reach their inflation targets. This has led to a consensus on the necessity of keeping interest rates elevated for an extended period. Such a stance aims to ensure that inflation is adequately controlled before considering any rate cuts.

Megan Greene of the BoE has expressed the need for more comprehensive data indicating a reduction in price pressures before the BoE can justify lowering interest rates. Her comments reflect a cautious approach, emphasizing the importance of solid evidence before making policy changes.

Early in the Asian trading session on Friday, the GBP/USD pair posted modest gains. The Federal Reserve’s careful approach to discussing inflation and the potential for rate cuts this year has been a significant point of interest. Investors are keenly awaiting further insights from speeches by Fed officials Kashkari, Waller, and Daly later in the day.

Several Fed officials have reiterated the need to maintain high borrowing costs until there is substantial evidence that inflation is decreasing. For instance, Raphael Bostic, President of the Federal Reserve Bank of Atlanta, highlighted the necessity of patience regarding interest rates, noting persistent pricing pressures within the US economy. Similarly, Loretta Mester, President of the Cleveland Fed, indicated that confidence in the inflation trajectory might take longer to establish, suggesting that the Fed should continue its restrictive stance for a longer period. This cautious tone from Fed policymakers has bolstered the US Dollar, exerting pressure on the GBP/USD pair.

Additionally, the US Department of Labor reported on Thursday that new claims for jobless benefits increased to 222,000 for the week ending May 11. This figure was higher than the market consensus of 220,000 but lower than the previous reading of 232,000, indicating a mixed but slightly worsening labor market situation.

On the British side, the BoE recently emphasized the need for more substantial evidence that inflation will remain low before considering policy easing. Megan Greene, a BoE policymaker, stated that while inflation appears to be moving in the right direction, more data is required before the central bank can start cutting rates. This stance suggests that the UK central bank may be more cautious compared to the Fed, potentially weighing on the Pound Sterling (GBP) and capping the near-term upside for the GBP/USD pair.

AUDUSD – AUD Declines on China Slowdown and Bond Yield Drop

The Australian Dollar (AUD) continues to experience a decline for the second consecutive session, influenced significantly by mixed economic data from China released on Friday. This decline is compounded by pressure from Australia’s recent employment figures, which have painted a mixed picture and raised concerns in the financial markets. Australia’s economic fortunes are closely tied to China’s due to their substantial trade relationship, making any economic changes in China particularly impactful on the Australian market.

AUDUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

One of the critical factors contributing to the Australian Dollar’s decline is the drop in the yield on Australia’s 10-year government bond, which has fallen to approximately 4.2%, its lowest level in a month. This decline in bond yields follows a domestic jobs report that revealed slower-than-expected wage growth during the first quarter. The unexpected slowing in wage growth has led market participants to discount the likelihood of any imminent interest rate hikes by the Reserve Bank of Australia (RBA). The bond market’s reaction reflects concerns over the strength of Australia’s economic recovery and the central bank’s future policy actions.

In contrast, the US Dollar Index (DXY), which measures the performance of the US Dollar (USD) against six major currencies, has shown a rebound from a recent multi-week low. The Federal Reserve (Fed) continues to maintain a cautious stance regarding inflation and the potential for rate cuts in 2024. This cautious approach has provided some support to the US Dollar. Investors are closely watching speeches from key Fed officials, including Minneapolis Fed President Neel Kashkari and San Francisco Fed President Mary Daly, for further insights into the central bank’s policy direction.

China’s latest economic data has been a mixed bag. Retail Sales in China increased by 2.3% year-over-year in April, down from March’s 3.1% and below the expected 3.8%. This marks the 15th consecutive month of growth in retail activity but represents the slowest gain in this sequence. On the other hand, Industrial Production in China showed a more robust improvement, rising by 6.7% year-over-year, surpassing the anticipated 5.5% and the previous month’s 4.5%. These mixed signals from China add to the uncertainty facing the Australian Dollar, given the significant trade links between the two countries.

In the United States, key Federal Reserve officials have been emphasizing the need for patience regarding interest rates. On Thursday, Atlanta Fed President Raphael Bostic stressed that substantial pricing pressures persist in the US economy, indicating that the central bank should maintain its restrictive monetary stance. Similarly, Cleveland Fed President Loretta Mester suggested that it might take longer than anticipated to confidently determine the inflation trajectory, further reinforcing the need for a cautious approach.

Australia’s Wage Price Index (QoQ) increased by 0.8% in the first quarter, falling short of the market’s forecast of a 0.9% rise. This quarter’s increase is the smallest since late 2022. Additionally, annual pay growth slowed slightly to 4.1%, down from the previous 4.2%, and below market expectations. These figures highlight the ongoing challenges in Australia’s labor market and the potential implications for the broader economy.

In a related development, Sarah Hunter, Chief Economist and Assistant Governor (Economic) at the Reserve Bank of Australia, addressed the REIA Centennial Congress on Thursday. During her speech, Hunter discussed various potential strategies to address the imbalance between housing supply and demand growth. This issue is critical in Australia, where escalating prices, rents, and homelessness pose significant challenges to economic stability and social cohesion.

In the United States, the Consumer Price Index (CPI) decelerated to 0.3% month-over-month in April, coming in lower than the expected 0.4% reading. Retail Sales also flattened, falling short of the anticipated 0.4% increase. These data points suggest that inflationary pressures may be easing somewhat, but the overall economic outlook remains uncertain.

On the fiscal front, the Australian Budget for 2024-25 has returned to a deficit after recording a surplus of $9.3 billion in 2023-24. The Australian government aims to tackle headline inflation and alleviate cost-of-living pressures by allocating billions to reduce energy bills and rent, alongside initiatives to lower income taxes. Treasurer Jim Chalmers has expressed his expectation that the current headline inflation rate of 3.6% will return to the RBA’s target range of 2-3% by the end of the year. If this scenario unfolds, the central bank may consider cutting interest rates earlier than markets had anticipated.

Meanwhile, Federal Reserve Chair Jerome Powell has anticipated a continued decline in inflation. On Tuesday, Powell expressed less confidence in the disinflation outlook compared to previous assessments. He also highlighted that Gross Domestic Product (GDP) growth is expected to reach 2% or higher, attributing this positive forecast to the strength of the labor market. These remarks underscore the complex interplay of factors shaping the economic landscape in both the US and Australia.

NZDUSD – NZD/USD Declines as USD Recovers and Fed Maintains Caution

NZD/USD pair witnessed a downturn during the Asian trading session on Friday, primarily due to a significant rebound in the US Dollar. This resurgence followed the USD hitting multi-week lows the previous day, leading to an extension of losses for the New Zealand Dollar.

NZDUSD is moving in Descending channel

Federal Reserve’s Outlook on Economic Conditions

The Federal Reserve continues to adopt a cautious stance concerning the economic outlook, especially regarding inflation and the future trajectory of interest rates. Fed Bank of Atlanta President Raphael Bostic emphasized the importance of patience in monetary policy, citing ongoing substantial pricing pressures in the economy. Likewise, Cleveland Fed President Loretta Mester pointed out the challenges in accurately predicting the inflation path, suggesting that a restrictive monetary policy might be necessary for a longer duration.

U.S. Labor Market Update

The latest data from the US Department of Labor highlighted an increase in Initial Jobless Claims. For the week ending May 10, claims reached 222,000, slightly above expectations but less than the prior week’s total of 232,000. This data provides insight into the employment trends that are closely monitored by market participants and policymakers.

Support from New Zealand’s Economic Indicators

In New Zealand, the first quarter showed promising signs with an increase in the Producer Price Index (PPI) for both inputs and outputs. PPI inputs matched expectations with a 0.7% rise, while outputs exceeded forecasts, posting a 0.9% increase. This performance, particularly higher than expected output prices, suggests potential upward support for the NZD.

Major Contributors to PPI Changes

Significant increases in the cost of electricity and gas, which surged by 8.8% quarter-on-quarter, were the primary drivers of the rise in output prices. Similarly, input prices were heavily influenced by a notable 11.6% increase in energy costs. Insurance costs also played a substantial role, contributing a 5.0% increase to the PPI inputs. These factors are crucial in understanding the pressures within the New Zealand economy that could affect monetary policy and currency valuation.

XAGUSD – Silver Prices Climb as Jobless Claims Boost Fed Rate Cut Expectations

silver prices experienced an uptick, driven by higher-than-expected Initial Jobless Claims, which intensified speculations about a possible rate cut by the Federal Reserve (Fed) in September. Despite these expectations, Fed officials conveyed a cautious outlook, suggesting that elevated interest rates might persist due to ongoing pricing pressures within the US economy. Concurrently, the US Dollar gained strength as the Fed signaled a wary stance on potential rate cuts in 2024.

XAGUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

Silver prices rebounded from recent losses, trading around per troy ounce during the Asian trading hours on Friday. Investors became cautious following the US Department of Labor’s report released on Thursday, revealing that Initial Jobless Claims rose to 222,000 for the week ending May 10. This figure surpassed the market consensus of 220,000, although it was a slight decrease from the previous week’s 232,000. The unexpected increase in jobless claims fueled dovish expectations, prompting market participants to anticipate a Fed rate cut in September.

On Thursday, Atlanta Fed President Raphael Bostic highlighted the necessity for patience regarding interest rates, noting substantial pricing pressures within the US economy. Bostic emphasized that it is crucial to observe inflation trends over a more extended period before making any policy changes. Similarly, Cleveland Fed President Loretta Mester indicated that it might take longer than anticipated to confidently determine the inflation trajectory. She advocated for maintaining a restrictive monetary stance to ensure inflation is kept in check.

These comments from Fed officials underscore a cautious approach to monetary policy, suggesting that while there is hope for rate cuts, the Fed remains committed to addressing inflation concerns. The cautious stance has supported the US Dollar, as higher interest rates typically strengthen the currency by making it more attractive to investors.

In the absence of significant economic data from the US, market participants are closely monitoring speeches from Fed officials for insights into the future direction of the Fed’s monetary policy. Later on Friday, speeches from Minneapolis Fed President Neel Kashkari and San Francisco Fed President Mary Daly are anticipated to provide further guidance. Their remarks are expected to offer valuable hints about the Fed’s policy outlook and potential timing for any adjustments.

In conclusion, while silver prices have shown resilience in response to rising jobless claims and the potential for a Fed rate cut, the future trajectory will largely depend on forthcoming economic data and the Fed’s communications. The mixed signals from recent economic reports and Fed officials suggest that market participants should prepare for potential volatility in the near term.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!