USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

USDCAD – CAD Slips Below 1.3650, Focus on Canadian CPI Data

The Canadian CPI For the month of April is expected at 2.7% YoY versus 2.9% printed in the last month. Monthly basis, expected reading is 0.50% MoM versus 0.60% printed in the March month. Lower CPI reading if printed today makes BoC to do rate cuts 2-3 times in this year before FED rate cut.

Market participants are eagerly awaiting remarks from additional Federal Open Market Committee (FOMC) members. Additionally, all eyes are on the upcoming release of the Canadian Consumer Price Index (CPI) inflation report for April.

Market expectations anticipate a further moderation in CPI inflation figures, both on an annual and monthly basis, which could potentially influence the Bank of Canada (BOC) to consider interest rate cuts in the following month. Analysts project that the Canadian central bank may opt for 2-3 rate cuts before the Federal Reserve implements its first rate cut, potentially exerting downward pressure on the Loonie and providing a boost to the USD/CAD pair. Forecasts suggest that Canada’s CPI inflation is likely to ease to 2.7% year-on-year (YoY) in April from the previous reading of 2.9%, while the monthly CPI inflation is expected to decrease to 0.5% month-on-month (MoM) in April from 0.6% in March.

Furthermore, the decline in crude oil prices is adding selling pressure on the commodity-linked Canadian Dollar (CAD), given that Canada is a prominent exporter of oil to the United States.

Conversely, US Federal Reserve (Fed) officials maintain a cautious stance regarding the timing of their easing cycle, emphasizing the importance of maintaining higher interest rates for prolonged periods to ensure confidence in achieving inflation targets. This cautious approach by the Fed may bolster the Greenback and limit the downside potential of the USD/CAD pair in the near term.

XAUUSD – Gold Price Loses Momentum on Renewed USD Demand

The FED Vice Chair Michael Barr said Current policy is more restrictive until inflation come to our target of 2%, FED Policy maker Philip Jefferson said 2% target of inflation is near by and once reached then we do rate cut in the policy settings. Atlanta FED President Raphale Bostic said current policy is enough for controlling inflation in the market, rate cuts is not necessary at the current stance. US Hawkish members speech on rate hike makes US Dollar stronger against Gold yesterday.

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices (XAU/USD) experienced a loss in momentum on Tuesday, retracting from previous record highs. The market lacked fresh catalysts amid a relatively quiet session devoid of significant top-tier economic data, potentially restricting the precious metal’s upward movement. However, underlying factors such as increased bets on interest rate cuts by the US Federal Reserve (Fed), persistent geopolitical tensions, and robust demand from central banks and Asian buyers may offer some support to gold.

Traders are closely monitoring Fedspeak, with several Fed officials, including Waller, Williams, Barr, Bostic, Collins, and Mester, scheduled to deliver speeches later on Tuesday. The release of the FOMC Minutes on Wednesday will be a focal point. Additionally, the hawkish tone from Fed officials could bolster the US Dollar, consequently exerting downward pressure on USD-denominated gold.

In recent developments, gold achieved a record high on Monday, reaching $2,450, while silver prices approached 12-year highs. Gold has exhibited an 18% increase year-to-date, with silver recording a 35% gain. Remarks from Fed Vice Chair Michael Barr emphasized the need for the central bank to allow its restrictive policy more time to take effect. Additionally, Fed policymaker Philip Jefferson noted that while inflation is easing, it is not doing so as rapidly as anticipated. Atlanta Fed President Raphael Bostic echoed similar sentiments, highlighting that policy remains restrictive and that it will take time for the central bank to gain confidence in inflation reaching the 2% target.

Investor sentiment indicates a 76% probability of a 25 basis-point rate cut by the Fed in September, with expectations of two cuts by year-end, according to the CME FedWatch Tool.

EURUSD – steady before ECB Lagarde, Fed Minutes

The ECB is expected toreduce the borrowing costs in the June month meeting from the ECB members expected. ECB Board Member Isabel Schnabel said reducing rates will impact the economy more and economy recovered from bottom. Patience in the rate cut is needed due to risk aversion in the furture. This week ECB President Lagarde speech and FOMC meeting minutes is scheduled.

EURUSD has broken the Descending channel in upside

With no significant US data releases, investors are turning their attention to statements from Federal Reserve (Fed) officials. Meanwhile, all eyes are on the upcoming events, including a speech by European Central Bank (ECB) President Christine Lagarde and the release of minutes from the recent Federal Open Market Committee (FOMC) meeting, scheduled for Wednesday.

Following last week’s US inflation report, Fed officials expressed confidence that inflation is on track to meet the 2% target. Fed Vice Chair Philip Jefferson emphasized the need for cautious evaluation of incoming economic data and outlook. Michael Barr, Vice Chair of the Atlanta Fed, noted that disappointing first-quarter inflation data did not provide the Fed with enough confidence to support easing monetary policy.

Market expectations suggest the Fed will maintain interest rates at its June meeting. However, traders are pricing in a 76% probability of a 25 basis-point rate cut by September, with the possibility of two cuts by the year-end, according to the CME FedWatch Tool.

On the European front, the ECB is anticipated to consider lowering borrowing costs in its June meeting. ECB board member Isabel Schnabel suggested a potential rate cut in June but cautioned against further reductions due to uncertainty surrounding the economic outlook. Analysts believe the monetary policy divergence between the ECB and Fed may impact the Euro’s strength and pose challenges for the EUR/USD pair.

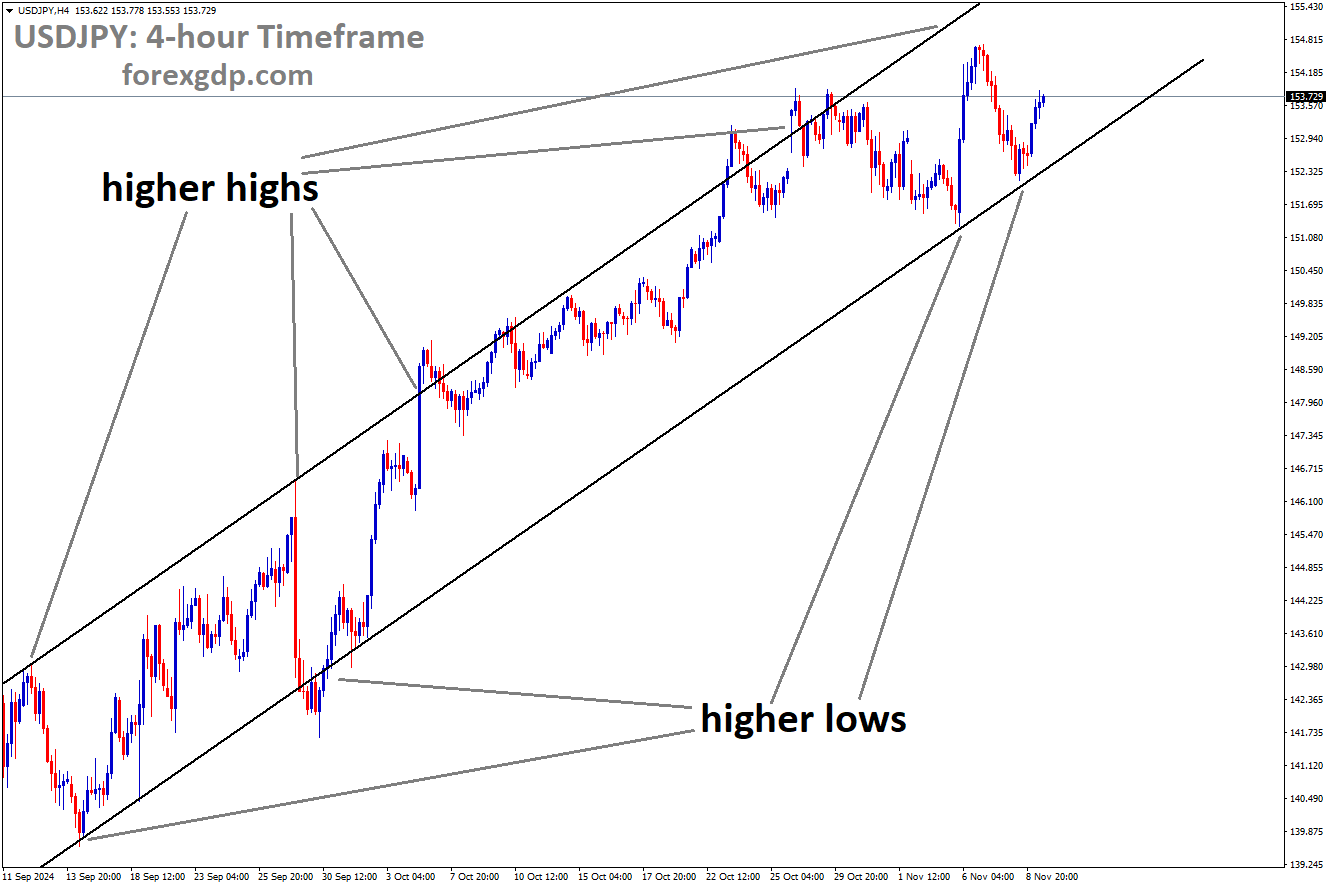

USDJPY – JPY rebounds on weaker USD, decreased US bond yields

The Japanese Yen weakness in the market is higher and is more concerned by Japan Finance Minister Shunuchi Suzuki today. Rates are lower is supported for 90% of Firms to do business in the profit manner, but 70% of Business firms said lower rates makes import cost higher and labour cost also higher. The BoJ Governor Ueda said at last meeting BoJ did not end the purchasing of Bonds in the market, they know when to stop buying purchases in the market. Lowering rates is support for counter currencies to strengthed against JPY.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Japanese Yen (JPY) ended its three-day decline on Tuesday, with the USD/JPY pair facing potential hurdles due to the significant interest rate gap between Japan and the United States (US). The JPY’s weakness against the backdrop of potential earlier interest rate hikes by the Bank of Japan (BoJ) has supported the USD/JPY pair.

Japanese Finance Minister Shunichi Suzuki voiced concerns about the negative impacts of the weak JPY, emphasizing market discussions on long-term rates and appropriate national debt policies. There are expectations for wage increases to outpace inflation, with close monitoring of foreign exchange (FX) movements.

The US Dollar (USD) traded steadily, buoyed by higher US Treasury yields and cautious sentiment from the US Federal Reserve (Fed) regarding inflation and potential rate adjustments in 2024.

Daily Digest Market Movers: Japanese Yen under pressure due to hawkish Fed

A recent Bank of Japan (BoJ) survey revealed that approximately 70% of firms reported drawbacks from the BoJ’s lengthy monetary easing measures, citing a weak JPY that raised import costs. However, around 90% of firms also acknowledged benefits, including low borrowing costs. Exchange rate stability emerged as a key factor desired by Japan’s large manufacturers.

The yield on the 2-year Japanese government bond stands at 0.34%, suggesting anticipated policy rate increases to 0.25% in the second half of the year and 0.5% next year.

Loretta Mester, President of the Federal Reserve Bank of Cleveland, indicated a shift in her stance, no longer supporting three rate cuts in 2024. She emphasized upward inflation risks and the need for more data gathering before policy adjustments.

The probability of a 25 basis-point rate cut by the Federal Reserve in September has slightly risen to 49.6%, compared to 48.6% a week earlier, according to the CME FedWatch Tool.

Market sentiment suggests the possibility of the BoJ reducing bond purchases at the June policy meeting. BOJ Governor Kazuo Ueda indicated no immediate plans to sell the central bank’s ETF holdings.

USDCHF – Maintains Positive Sentiment Near 0.9100

The 10 Year Bond Yield rate soared to 0.70%, SNB may be maintain the rates at current level is possible expected from the investors side, buying Bond markets. But SNB has do alternate to this expected levels and do 25bps rate cut in the March month. This week Labour data and SNB Chairman Jordan speech is scheduled.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The bullish momentum in the USD/CHF pair is primarily attributed to the strengthened US Dollar (USD) sentiment. Notably, Swiss markets remain closed due to the Whit Monday bank holiday.

However, concerns arise from the recent easing of US consumer inflation and labor market data, fueling speculations about potential rate cuts by the Federal Reserve (Fed) in 2024. According to the CME FedWatch Tool, the probability of the Federal Reserve implementing a 25 basis-point rate cut in September has slightly increased to 49.0%, up from 48.6% a week earlier. Such potential monetary policy easing by the Fed could undermine the strength of the US Dollar and restrain the upward movement of the USD/CHF pair.

Fed officials have maintained a cautious approach toward interest rates, highlighting that a singular decline in inflation does not instill confidence that price pressures will consistently revert to the targeted 2% rate. Market participants eagerly await the release of the Federal Open Market Committee (FOMC) minutes scheduled for Wednesday, anticipating insights into policymakers’ emphasis on prolonging higher interest rates.

Meanwhile, on the Swiss front, the yield on the 10-year Swiss government bond has marginally increased to approximately 0.7%. This uptick in Swiss yield typically signals the likelihood of the Swiss National Bank (SNB) maintaining its current interest rates, potentially bolstering the Swiss Franc (CHF). In a surprising move, the SNB slashed interest rates for the first time in nine years in March, reducing the key interest rate by 25 basis points to 1.50%, positioning itself as the first major central bank to implement monetary policy easing.

Traders await further insights into the Swiss economy, particularly from the Employment Level data released by Swiss Statistics later in the week. Additionally, Swiss National Bank (SNB) Chairman Thomas Jordan is scheduled to deliver a speech on communication, monetary policy, and public impact at the Swiss Media Forum in Lucerne, Switzerland, on Friday.

USD INDEX – Yellen: Global Economy Resilient Despite Geopolitical Challenges

The US Secretary Janet Yellen said The European central banks must have vigilant in Russia sanctions then only we reduce the power of Russia in the war against Ukraine. But some countries did not follow the sanctions like China, UAE and Turkey, it is more concerning for the US. After 2023 Swiss Bank collapse, Global Financial conditions are lower and is emerging from bottom. Stay Vigilance on Private lenders on Real estate and NBFCs investments.

USD INDEX is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

On Tuesday, US Treasury Secretary Janet Yellen commented that the “global economy remains resilient in the face of the challenging geopolitical landscape.”

Yellen emphasized the importance of European banks stepping up compliance measures and focusing on thwarting Russian evasion attempts. She urged European banks to ensure strict adherence to sanctions compliance policies, particularly in high-risk jurisdictions.

Furthermore, Yellen stated that efforts are ongoing to explore new methods to diminish Russia’s revenues and disrupt its procurement of goods for the conflict in Ukraine. She highlighted concerns about evasion of US-Russian sanctions, particularly through channels in China, UAE, Turkey, and Europe.

Yellen noted that banks have strengthened compliance measures in response to US warnings regarding secondary financial institution sanctions. These actions by the global financial sector have contributed to impeding Russia’s ability to acquire battlefield goods.

Regarding global financial conditions, Yellen mentioned that conditions have eased since the banking sector turmoil in 2023, with risks being broadly balanced. However, she emphasized the importance of remaining vigilant regarding elevated corporate debt, leverage, liquidity mismatches in the non-bank sector, and strains in commercial real estate.

GBPUSD – GBP holds steady above 1.2700, awaits UK inflation

The UK CPI Data for the month of April is expected to 2.1% from 3.2% printed in the last month, Core CPI is expected at 3.6% from 4.2% printed in the last month. This expected reading will give way for rate cuts in the UK economy as per BoE Deputy Governor Broadbent said yesterday.

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The Pound Sterling (GBP) stands firm, trading slightly above 1.2700 during Tuesday’s European trading session. Market attention is fixed on the upcoming release of the United Kingdom Consumer Price Index (CPI) data for April and the forthcoming Federal Open Market Committee (FOMC) minutes from the May meeting, scheduled for publication on Wednesday.

The US Dollar Index (DXY), a measure of the dollar’s strength against a basket of major currencies, remains stable near 104.60 as investors await fresh signals regarding the Federal Reserve’s (Fed) potential interest rate adjustments. Investors are keenly awaiting insights from the FOMC minutes to discern policymakers’ perspectives on the interest rate trajectory.

Given the significant shifts in the US inflation landscape since the last Fed meeting, the impact of the FOMC minutes on the market sentiment may be subdued. April witnessed a decline in inflation as anticipated, indicating a resumption in the disinflationary trend after a stagnant period in the first quarter. As the previous Fed meeting occurred before the latest inflation data release, the forthcoming communication from Fed officials is anticipated to carry a notably hawkish tone regarding interest rates.

Despite the decline in US inflation in April, Fed officials remain cautious about the sustained return of price pressures to the desired 2% level. Fed Vice Chair for Supervision, Michael Barr, underscored the disappointing first-quarter inflation figures, emphasizing the need for a patient approach towards monetary policy adjustments.

In the daily market movement report:

The Pound Sterling experiences upward momentum, maintaining its position within Monday’s trading range and holding firm above the critical support level of 1.2700 against the US Dollar. GBP demonstrates strength against other major currencies, ahead of the impending release of UK CPI data for April.

Economists anticipate a significant drop in headline inflation to 2.1% from the previous reading of 3.2%, as reported by the UK Office for National Statistics (ONS). The core CPI, excluding volatile items, is projected to decelerate to 3.6% from 4.2% in March. Additionally, monthly headline inflation is expected to exhibit slower growth of 0.2% following a sharp increase of 0.6% in March.

The anticipated decline in UK inflation is expected to bolster investor confidence in the trajectory towards the desired 2% inflation target. This could heighten expectations of imminent interest rate cuts by the Bank of England (BoE). Speculation is divided between the June or August meetings for potential policy adjustments by the BoE.

Market sentiments favor the likelihood of the BoE initiating interest rate cuts during the summer, spurred by dovish remarks from BoE Deputy Governor Ben Broadbent on the interest rate outlook. Broadbent’s comments on Monday suggested that if economic conditions align with forecasts indicating a need for less restrictive policy, a Bank Rate cut could be on the horizon over the summer months.

AUDUSD – RBA Minutes: Rate Hike Considered

Today RBA Meeting minutes for the May month Monetary meeting outcome is, Board members difficult to take decision either Rule in or Rule out for cash rate dependent on incoming data. Inflation will stay higher for Longer until 2026, Labour conditions are tightened, Consumer spending is lower, Financial conditions is remained restrictive, Over tightened will take economy to recession mode, So rate hike or hold for some times based on incoming data is the board outcome today.

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Reserve Bank of Australia (RBA) published the Minutes of its May monetary policy meeting on Tuesday, highlighting that the board members considered whether to raise rates and judged the case for maintaining steady policy as stronger. Additional details of the RBA Minutes suggest that the board agreed it was difficult to either rule in or rule out future changes in the cash rate, according to Reuters.

Key takeaways:

– The board considered whether to raise rates but judged the case for steady policy as stronger.

– The board agreed it was difficult to either rule in or rule out future changes in the cash rate.

– The flow of data had increased the risks of inflation staying above target for longer.

– The board expressed limited tolerance for inflation returning to target later than 2026.

– Staff forecasts were considered sound and presented a credible path back to target.

– The board noted that forecasts were predicated on a noticeably higher path for the cash rate.

– A rate rise could be appropriate if forecasts proved overly optimistic.

– Risks around the forecasts were judged to be balanced.

– Importantly, inflation expectations remained well anchored.

– It was considered reasonable to look through short-term variation in inflation to avoid “excessive fine-tuning.”

– The labor market had proved tighter than expected, while consumer demand was weaker.

– Financial conditions in Australia were judged to be restrictive.

– Risks to global growth had become more balanced, with the outlook for the US and China revised upward.

NZDUSD – dips close to 0.6100 amid RBNZ rate expectations

The RBNZ is expected to keep the rates at 5.50% in the Tomorrow meeting due to Members are voting for Hold inorder to inflation comeback to 1-2% target. 2 Year inflation expecations falling to lower point in the second half of 2024 survey, So RBNZ may do rate cuts from starting of 2025 is expected. China measures of real estate bring back policies is helpful for Kiwi exports and China economy struggling from lower portion.

NZDUSD has broken the Descending channel in upside

Market participants are eagerly anticipating the upcoming policy meeting of the Reserve Bank of New Zealand (RBNZ) scheduled for Wednesday. It is widely expected that the RBNZ will opt to maintain its Official Cash Rate (OCR) at the current level of 5.5%, marking the seventh consecutive meeting without any changes. Analysts anticipate policymakers to underscore the importance of sustaining a restrictive monetary policy stance for an extended period to steer inflation back within the target range of 1-3%.

Recent data revealing a decline in the country’s 2-year inflation expectations to their lowest level in nearly three years during the second quarter has fueled speculation that the RBNZ might contemplate rate cuts later in 2024.

Support for the New Zealand Dollar (NZD) could stem from China’s recent announcement of a comprehensive package aimed at bolstering its struggling property market. The Chinese finance ministry intends to raise 1 trillion Yuan by issuing bonds with maturities ranging from 20 to 50 years to facilitate larger stimulus measures. These measures include the relaxation of mortgage regulations and encouragement for local governments to purchase unsold homes. Given the close trade ties between New Zealand and China, this development may uplift sentiment in Kiwi markets.

Meanwhile, the US Dollar (USD) remains relatively stable, with no significant economic data releases from the United States (US) at present. The Greenback continues to receive support from higher US Treasury yields. The US Federal Reserve (Fed) maintains a cautious stance regarding inflation and the potential for rate cuts in 2024.

According to the CME FedWatch Tool, there has been a slight increase in the probability of the Federal Reserve implementing a 25 basis-point rate cut in September, rising to 49.6% from 48.6% a week ago.

CRUDE OIL – WTI Dips Below $79.00 on Fed Officials’ Hawkish Remarks

The Crudeoil prices are moving flat after the Canada announced Transmountain pipeline is ready for manufacturing Oil nearly 590K barrels per day, it will supply from Alberta to Canada Pacific Coast. Longer delay of this production now comes to active is positive for Oil supply but negative for Oil prices soaring in the market. OPEC+ meeting conducted in the June 1 for voluntary cut of 2.2 Million Barrels per day decision.

XTIUSD Oil price is moving in the Descending channel and the market has fallen from the lower high area of the channel

During the Asian session on Tuesday, the price of West Texas Intermediate (WTI) crude oil extended its decline to approximately $78.90 per barrel, influenced by recent developments in the Middle East. Despite events such as the death of Iran’s President Ebrahim Raisi in a helicopter crash and emerging health concerns surrounding Saudi Arabia’s King Salman bin Abdulaziz, these occurrences do not seem to be significantly impacting the market sentiment.

Crude oil prices faced downward pressure as investors assessed recent hawkish statements from Federal Reserve (Fed) officials, notwithstanding the cooling US consumer inflation data from the previous week. Federal Reserve Vice Chair Michael Barr, in a statement reported by Reuters on Monday, indicated that the Fed is well-positioned to maintain its current policy stance and observe economic developments.

In an interview with Bloomberg, Loretta Mester, President of the Federal Reserve Bank of Cleveland, expressed her revised view that three rate cuts in 2024 may no longer be appropriate. Mester highlighted the upward risks to inflation and emphasized the importance of gathering additional data on inflation given the robustness of the economy.

According to the CME FedWatch Tool, there has been a slight increase in the likelihood of the Federal Reserve implementing a 25 basis-point rate cut in September, rising to 49.6% from 48.6% a week earlier.

Meanwhile, in Canada, the expanded Trans Mountain pipeline (TMX) commenced commercial operations this month after overcoming numerous regulatory delays and construction challenges. The TMX expansion will facilitate the transportation of an additional 590,000 barrels per day (bpd) from Alberta to Canada’s Pacific coast.

Investor focus now shifts to the upcoming meeting of the Organization of the Petroleum Exporting Countries and its allies (OPEC+) scheduled for June 1. During this meeting, decisions will be made regarding output policies, including whether to extend voluntary production cuts of 2.2 million barrels per day implemented by certain member countries.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!