XAUUSD Gold price is moving in an Ascending triangle pattern and the market has reached the higher low area of the triangle pattern

XAUUSD – Gold Bounces Back Despite Fed’s Hawkish Stance

The Gold prices are down after the US Domestic data of PMI readings came at higher than expected last day. China Private sector imported 543 Tonnes of Gold in Q1 2024 and 189 Tonnes from PBoC bank purchased in Q1 2024. Indian exchanged Old Gold to New Jewels in the market due to higher rates prevailing moments.

Gold (XAU/USD) managed to regain some lost ground on Friday despite the prevailing strength of the US Dollar (USD). However, the upside potential for the yellow metal may be constrained by diminishing expectations of a rate cut by the US Federal Reserve (Fed) in September. Nonetheless, geopolitical tensions in the Middle East could provide support for gold as investors seek safe-haven assets.

Investor focus will remain on Fed communication, with Fed Governor Waller scheduled to speak on Friday. Any further hawkish commentary from Fed officials could exert downward pressure on gold prices. It’s important to note that higher interest rates typically weigh on gold, as they increase the opportunity cost of holding the precious metal. Additionally, market participants will be closely monitoring the release of US Durable Goods Orders and the Michigan Consumer Sentiment Index.

In market developments:

– US Initial Jobless Claims decreased by 8,000 to 215,000 for the week ending May 18, surpassing expectations and the previous week’s reading.

– The flash US S&P Global Manufacturing PMI rose to 50.9 in May from 50.0 in April, while the Services PMI increased to 54.8, both exceeding forecasts.

– The US S&P Global Composite PMI surged to 54.4 in May, beating expectations and reaching its highest level since April 2022.

– Atlanta Fed President Raphael Bostic expressed concerns about upward inflation pressure, suggesting the need for the Fed to exercise patience to prevent overheating the economy.

– China’s private sector imported 543 tonnes of gold in Q1 2024, with the People’s Bank of China (PBoC) adding another 189 tonnes to its reserves during the same period.

– Gold imports to India are expected to decline by approximately 20% in 2024 due to high prices, encouraging retail customers to exchange old jewelry for new products.

EURUSD – German Q1 Growth Confirmed at 0.2% by Stats Office

The Germany Economy is expanded in First Quarter of 2024 as 0.20% compared to -0.40% decline in the last quarter. The Construction area is concentrated by 2.7% up in this quarter, Government spending lower to 0.40% than previous quarter. Exports area contribute to 1.1% in this Quarter compared to last quarter.

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The German economy exhibited a growth of 0.2% during the initial three months of 2024, as confirmed by the statistics office in its report released on Friday, validating preliminary data.

Ruth Brand, the president of the statistics office, remarked, “After a decline in GDP towards the end of 2023, the German economy initiated 2024 with positive growth.”

Despite a downturn in inflation, household consumption failed to rebound in the first quarter, experiencing a decrease of 0.4% compared to the previous quarter. Concurrently, government expenditure also recorded a 0.4% decline from the previous quarter, as indicated by the data.

Following a subdued performance in the latter half of 2023, investment in construction witnessed a significant rise of 2.7% from the previous quarter. However, investment in machinery and equipment witnessed a slight dip of 0.2%.

Foreign trade made positive contributions to the economic landscape as well. Notably, exports of goods and services in the first quarter exhibited an increase of 1.1% compared to the previous quarter.

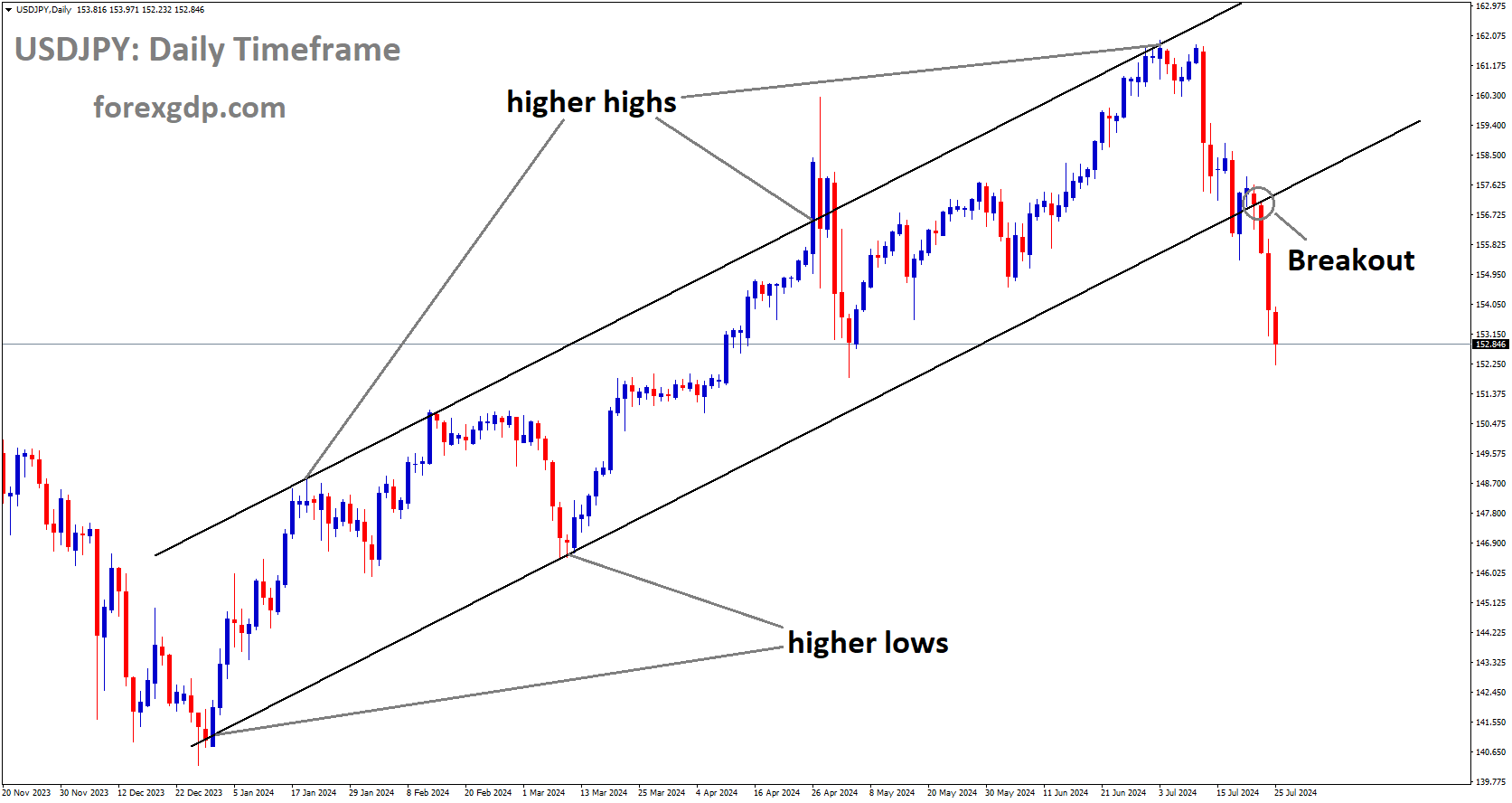

USDJPY – Yen Steady, Dollar Firm Ahead of Consumer Sentiment

The Japan CPI Data annually came at 2.5% in the April month when compared to 2.7% in the last month. Core CPI Data came at 2.2% when compared to 2.6% in the March month. Japan Government Bond 10 Yr Yield surpassed 1% and expected another rate hike from BoJ. Japan Manufacturing index came at 50.5 in the May month from 49.6 printed in the April month, Service PMI fell into 53.6 from 54.3 in the April month. JPY weakness persistence in the market due to weak CPI Figures once again.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Japanese Yen (JPY) continued its downward trajectory on Friday following the release of softer National Consumer Price Index (CPI) data by the Statistics Bureau of Japan. The annual inflation rate for April dipped to 2.5% from 2.7% in the previous month, marking the second consecutive month of moderation but remaining above the Bank of Japan’s (BoJ) 2% target. This sustained inflation exerts pressure on the central bank to consider further policy tightening measures.

The Bank of Japan has stressed the importance of achieving a virtuous cycle of sustained and stable attainment of its 2% price target, alongside robust wage growth, as crucial for policy normalization. Meanwhile, market participants anticipate that the persistent weakness of the JPY could prompt the BOJ to expedite its next interest rate hike to mitigate the impact on the cost of living, according to Reuters.

On the other hand, the US Dollar (USD) strengthened on hawkish sentiments surrounding the Federal Reserve (Fed), which intends to maintain higher policy rates for an extended period. This sentiment was bolstered by the better-than-expected Purchasing Managers Index (PMI) data from the United States (US) released on Thursday. Investors are closely monitoring the Michigan Consumer Sentiment Index on Friday to glean insights into consumer perceptions regarding financial and income situations in the United States.

In addition to these market movements, recent developments include:

– Japan’s Core CPI (YoY), excluding fresh food but including fuel costs, rose 2.2% in April as anticipated, marking a second consecutive monthly slowdown from March’s 2.6%.

– The S&P Global US Composite PMI surged to 54.4 in May from April’s 51.3, surpassing market forecasts of 51.1. The Service PMI recorded robust output growth, reaching 54.8, while the Manufacturing PMI edged up to 50.9.

– The likelihood of the Federal Reserve implementing a 25 basis-point rate hike in September decreased to 46.6% from 49.4%.

– The Bank of Japan announced no change in the amount of Japanese government bonds (JGB) compared to the previous operation.

– Escalating tensions ensued following Lai Ching-te’s assumption of office as Taiwan’s new president, with reports indicating increased fighter jet deployment and simulated strikes by China in the Taiwan Strait and surrounding areas.

– Japan’s Manufacturing Purchasing Managers Index (PMI) rose to 50.5 in May from April’s 49.6, surpassing expectations. However, the Services PMI dipped slightly to 53.6.

– Japan’s 10-year government bond yield surpassed 1% this week for the first time since May 2013, driven by growing speculation of further policy tightening by the Bank of Japan in 2024.

USDCAD – CAD falls below 1.3750 before Canadian Retail Sales release

The Canadian Dollar moved lower against counter pairs ahead of Canada Retail sales scheduled today. This Week Canadian CPI fell near to 2% target level makes BoC happy with earlier rate cuts preparations. 53% chances of 25bps rate cut in the June month meeting is expected by Poll results.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The pair is bolstered by a stronger US Dollar (USD) driven by positive US PMI data, with investors eagerly awaiting Canadian Retail Sales figures and US Durable Goods Orders for potential market shifts. Moreover, Fed’s Waller is scheduled to deliver a speech later in the day, adding to market anticipation.

In the US, private sector business activity surged in May, surpassing April’s performance, as reported by S&P Global. The flash US Composite Purchasing Managers Index (PMI) exceeded expectations, rising to 54.4 from April’s 51.3. Both Manufacturing PMI and Services PMI showed notable improvements, with May’s figures surpassing estimates and previous readings. These positive PMI reports have lifted the USD Index (DXY) above the key 105.00 level, providing further support to the USD/CAD pair.

Conversely, the Canadian Dollar (CAD) faces pressure from declining crude oil prices, given Canada’s status as a major oil exporter to the US. Additionally, speculations that the Bank of Canada (BoC) might lower interest rates before the US Federal Reserve could weaken the Loonie against the USD. Market sentiment suggests a 53% likelihood of a 25 basis points (bps) rate cut by the BoC in June, with full pricing for a July rate cut.

USDCHF – Swiss Q1 Employment Increases by 1.8%

The Swiss Q1 Employment data came at 1.8% up from the previous quarter, Full time Employment came at 1.4%, Employees joined the companies rose to 0.60%. Companies showing Job Vacancies lower to 9.7% YoY and 12300 vacancies so far.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

According to a report released by the Federal Statistical Office of Switzerland on Friday, total employment in the country increased by 1.8% in the first quarter of 2024 compared to the corresponding period in the previous year. When measured in terms of full-time equivalents, job numbers rose by 1.4%.

After seasonal adjustments, the number of employees in Swiss companies showed a 0.6% increase compared to the previous quarter.

Additionally, Swiss companies reported a year-on-year decrease of 9.7% in job vacancies, with the total number of vacancies reaching 12,300.

USD INDEX – Forex Today: USD Gathers Weekly Strength Ahead of Mid-tier Data

The US Manufacturing PMI data came at 50.9 in the May month versus 50.0 is printed in the last month. Composite PMI came at 54.4 from 51.3 printed in the April month, Services PMI data printed at 54.8 in the May month from 54.4 printed in the last month. The expansion in the all regions of PMI data in the US economy moved US Dollar higher against counter pairs.

USD INDEX is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The US Dollar (USD) rode the wave of positive Purchasing Managers’ Index (PMI) data from the United States on Thursday, maintaining its upward trajectory for the fourth consecutive day. The USD Index closed on a positive note, buoyed by the robust economic indicators. Looking ahead, investors are eyeing the release of Durable Goods Orders data for April and the revised University of Michigan Consumer Sentiment Survey for May from the US economic calendar as potential market movers before the weekend.

The S&P Global Composite PMI surged to 54.4 in May’s preliminary estimate, up from 51.3 in April, signaling a continued expansion in business activity with an accelerating pace. Both the Manufacturing and Services PMIs showed improvement, with figures reaching 50.9 and 54.8, respectively. Despite experiencing a slight dip during European trading hours, the USD Index quickly regained momentum, surpassing the 105.00 mark for the first time in 10 days. As Friday begins, the index remains steady, holding near its closing level from Thursday.

GBPUSD – UK Retail Sales Fall 2.3% MoM in April, Surprising Expectations

The UK retail sales for the month of April came at -2.3% MoM versus -0.40% decline expected and -0.20% decline in the last month, Core Retail sales came at -2.0% MoM versus -0.60% in the March. YoY decline to -2.7% in the April month versus 0.40% increase in the March month and Core YoY data declined to -3.0%. GBP Down after the Retail sales figues tremendous sharp fall in the market.

GBPUSD is moving in the Symmetrical triangle pattern and the market has reached the lower high area of the pattern

According to the latest data released by the Office for National Statistics (ONS) on Friday, retail sales in the UK experienced a notable decline in April. Specifically, retail sales dropped by 2.3% over the month, a significant deviation from the expected decrease of 0.4%. This decline follows a smaller decrease of 0.2% recorded in March.

When excluding auto motor fuel sales to analyze core retail sales, the situation remained bleak. Core retail sales fell by 2.0% month-on-month in April, compared to a decline of 0.6% in March and against market expectations of a decrease of 0.6%.

On an annual basis, retail sales in the United Kingdom saw a substantial decrease of 2.7% in April compared to the previous month’s increase of 0.4%. Similarly, core retail sales experienced a decline of 3.0% in April, contrasting with the previous month’s flat growth. Both of these figures fell short of market expectations.

AUDUSD – AUD slips as USD strengthens; Focus on Consumer Sentiment

The China conducted more Fighter Jets operations in the Taiwan strait near Taiwan Islands creating Geopolitical tensions and Australian Dollar dropped after the tension begins. The Australian inflation expecations for the 12 months forecasts in the May month dropped to 4.1% from 4.6% printed in the April month. Services, Composite and Manufacturing PMI data came at lower than expected in the May month created pressures on Australian Dollar in the market.

AUDUSD has broken the Ascending channel in downside

The Australian Dollar (AUD) saw a downward trend for the fourth consecutive session on Friday, potentially driven by risk aversion. The AUD/USD pair experienced a decline as the US Dollar (USD) strengthened, buoyed by hawkish sentiment surrounding the Federal Reserve (Fed) maintaining higher policy rates for a prolonged period.

The Australian Dollar faced pressure as the Consumer Inflation Expectation, reflecting future inflation over the next 12 months, decreased to 4.1% in May from 4.6% in April, marking the lowest level since October 2021. This raised concerns about inflation persisting above the target for an extended duration. The recent Reserve Bank of Australia (RBA) meeting minutes revealed policymakers’ challenge in determining potential changes in the cash rate.

The USD extended its gains following the release of higher-than-anticipated Purchasing Managers Index (PMI) data from the United States (US) on Thursday, raising concerns about prolonged elevated interest rates and driving Treasury yields higher. Furthermore, the latest Federal Open Market Committee (FOMC) Minutes highlighted Fed policymakers’ concerns regarding the persistent nature of inflation, which exceeded earlier expectations at the beginning of 2024.

Investors are closely monitoring US Durable Goods Orders on Friday, providing insights into the value of orders received by manufacturers for durable goods intended to last three years or more. Additionally, the Michigan Consumer Sentiment Index will offer perspectives on consumer attitudes concerning financial and income situations in the US.

In the Australian equity market, the ASX 200 Index rebounded, trading around 7,740 on Friday. However, Australian equities faced pressure amid lower commodity prices as stronger-than-expected US PMI data raised concerns that the Federal Reserve might sustain higher interest rates for an extended period.

Preliminary data from Thursday indicated that Australian private sector activity remained expansionary for the fourth consecutive month in May. The preliminary Judo Bank Composite Purchasing Managers Index (PMI) moderated slightly to 52.6 in May from April’s 53.0, signaling a marginal growth slowdown. The Judo Bank Australia Services PMI was 53.1 in May, down from April’s 53.6, marking the fourth straight month of expansion but at a slower pace. The Manufacturing PMI remained unchanged at 49.6 in May, indicating continued deterioration in manufacturing conditions for the fourth consecutive month.

Reuters reported Chinese state media’s indications on Thursday of China’s deployment of numerous fighter jets and simulated strikes in the Taiwan Strait and around groups of Taiwan-controlled islands. Any geopolitical tensions in the region may impact the Australian market, given China and Australia’s close trade partnerships.

NZDUSD – RBNZ’s Silk: Worried About Near-Term Inflation Risks

RBNZ Assistant Governor Karen Silk stated that inflation is currently higher in the New Zealand economy. The RBNZ forecasts that inflation will fall within the 1-3% target range by the end of 2024, but it is expected to slow down further in the second half of 2025.

NZDUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

For the first quarter of 2024, non-tradable inflation is at 5.8%, while the RBNZ projects it will average 5.3% this year and decrease to 2.8% by mid-2026. As long as inflation remains high, no rate cuts are projected for this year, with potential cuts planned for the second half of 2025.

Following Assistant Governor Silk’s hawkish remarks, the New Zealand Dollar strengthened against other currencies.

Reserve Bank of New Zealand Assistant Governor Karen Silk stated early Friday that she is “concerned about near-term inflation risks.”

Silk further explained that the bank has adjusted its modeling after underestimating the strength of domestic inflation.

CRUDE OIL – WTI Oil Faces Pressure Around $77 Amid Fed’s Hawkish Tone

The June 01 OPEC+ meeting is scheduled, On the last meeting April meeting Oil rich nations shows nochange in the Voluntary output cuts of 2.2 Million Barrels per day. This meeting also same resemblance expected from the analysts side. The Norway, Spain and Ireland going to Acquire Palestinian under their custody to protect people in Gaza from the Israel war crime activity against Gaza Civilians.

XTIUSD Oil price is moving in the Descending channel and the market has reached the lower low area of the channel

West Texas Intermediate (WTI) crude oil futures, traded on the New York Mercantile Exchange (NYMEX), are poised to end the week on a bearish note. Oil prices have been on a downward trend for the fifth consecutive trading session as of Friday. Throughout the week, the commodity has faced downward pressure, largely attributed to the Federal Reserve (Fed) maintaining a hawkish stance on interest rates despite expectations of a decline in the United States Consumer Price Index (CPI) report for April.

Fed policymakers remain cautious about the prospects of a sustainable decline in inflation, particularly given the robustness of the labor market. They have indicated that any consideration for rate cuts would require greater confidence in the return of inflation to the targeted 2% rate.

Minutes from the Federal Open Market Committee (FOMC) meeting in May revealed that while some policymakers advocate for further monetary tightening to ensure price stability, Fed Chair Jerome Powell and the majority do not foresee additional rate hikes in the near term.

The Fed’s hawkish stance on interest rates tends to negatively impact oil prices. Higher interest rates restrict liquidity in the economy, leading to reduced consumer spending and economic activity, ultimately affecting overall oil demand.

The upcoming OPEC meeting scheduled for June 1 will likely serve as a significant catalyst for oil prices. During this meeting, member countries will discuss supply policies. In the previous meeting on April 13, OPEC nations opted to maintain the existing voluntary oil output cut of 2.2 million barrels per day.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!