XAUUSD – Gold prices decline as robust US Dollar and elevated US Treasury yields prevail

The Gold prices are moving flat ahead of US Q1 GDP data and US Core PCE index data is scheduled this week. Continuous buying Global banks due to Geopolitical tensions makes handsome for Gold prices in the market over the long term view. Current stance of US Data is main driver for Gold prices in the near term. Next 12-18 Month expected recession in the US economy due to election prospects and Government changing fears.

XAUUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

Gold prices experience a significant decline on Wednesday as a result of increasing US Treasury yields, which heighten demand for the US Dollar following hawkish remarks by a Federal Reserve (Fed) official.

The negative sentiment extends to Wall Street, with US yields across various tenors rising between four and six basis points. Minnesota Fed President Neel Kashkari’s comments from the previous day contribute to the cautious tone, as he suggests that rate hikes have not been ruled out, and any potential cuts would likely occur twice by the end of 2024.

Meanwhile, economic data remains relatively limited on Wednesday, with the US Conference Board reporting a modest improvement in consumer confidence for May. However, concerns about a potential recession in the next 12 to 18 months linger among Americans, according to Dana Paterson, The Conference Board’s Chief Economist.

Looking ahead, market participants anticipate the release of April’s Personal Consumption Expenditures (PCE) Price Index, a crucial measure of inflation favored by the Fed. Projections indicate a 2.8% year-on-year increase in the core figure and a 0.3% month-on-month rise in the headline PCE.

In summary, gold prices decline notably as US Treasury yields climb, bolstering the US Dollar’s strength. Fed officials’ hawkish rhetoric adds to the cautious sentiment, while upcoming economic releases, including the second estimate of Q1 2024 Gross Domestic Product (GDP) and Initial Jobless Claims, are closely monitored for further market direction.

EURUSD – Slips Below 1.0800 as Fed Rate-Cut Prospects for September Diminish

The ECB is going to do rate cuts in the June month is more possible due to Euro zone inflation ticking downwards in the past months. This month CPI is expected to 2.5% from 2.4% YoY in the past month and Core CPI data is expected to 2.8% YoY versus 2.7%. US Q1 GDP and Core PCE index is scheduled this week for supporting US Dollar against Euro currency.

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The pair faces considerable pressure as the US Dollar (USD) gains strength amidst a cautious market atmosphere.

Investors are flocking to the US Dollar amid expectations that the Federal Reserve (Fed) is unlikely to pursue interest rate cuts in the near future. Fed policymakers have indicated their preference for observing a sustained slowdown in inflation before considering any adjustments to interest rates.

While the likelihood of further rate hikes by the Fed diminishes, the possibility remains on the table should progress in combating disinflation stall. Investors await the release of the United States core Personal Consumption Expenditure Price Index (PCE) data for April, scheduled for Friday. This data is poised to significantly impact speculations regarding Fed rate cuts in September, with projections indicating steady growth in both annual and monthly core PCE inflation readings.

EUR/USD experiences a sharp decline below the psychological barrier of 1.0800, driven by expectations of a weakening Euro against the US Dollar. Market sentiment suggests that the European Central Bank (ECB) is poised to initiate interest rate reductions starting from its June meeting, while the timing of any rate cuts by the Fed remains uncertain.

With Eurozone’s core inflation already dipping to 2.7%, and the service disinflation process resuming, ECB policymakers appear comfortable with the prospect of policy normalization from June onwards. Speculation surrounding the ECB’s rate-cutting trajectory beyond June will influence the Euro’s future movements, with current expectations pointing towards further rate cuts this year.

Investors eagerly anticipate the preliminary Eurozone inflation data for May, set to be released on Friday. These figures will offer insights into the ECB’s potential adjustments to key borrowing rates. Projections suggest a strengthening pace of annual Harmonized Index of Consumer Prices (HICP) to 2.5% from the previous reading of 2.4%, while the annual core HICP is expected to accelerate to 2.8% from 2.7% in April.

USDJPY – JPY Climbs Amid Speculation of BoJ Rate Hike, Tokyo Inflation Concerns

The Japanese Yen slight increase in the market ahead of Tokyo CPI is scheduled tomorrow. Japan Median inflation index shows 1.1% in the April from 1.3% in the March month. Services PPI index shows 2.8% in the April from 2.3% is expected, it is highest level since March 2015.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Japanese Yen (JPY) rebounded on Thursday, reversing recent declines, following remarks made by Bank of Japan (BoJ) board member Seiji Adachi on Wednesday. Adachi emphasized the gradual reduction of bond purchases to ensure that long-term yields accurately reflect market signals. Moreover, he suggested that a potential interest rate hike might be appropriate if a weaker JPY leads to heightened inflation, as reported by Reuters.

Market sentiment has shifted, with traders increasingly anticipating another interest rate hike by the Bank of Japan (BoJ). Investors are now closely monitoring the release of Tokyo’s inflation data scheduled for Friday, considering it a pivotal indicator of nationwide price trends.

Hawkish comments from Minneapolis Fed President Neel Kashkari further fueled concerns about possible rate hikes, sustaining the significant yield gap between the US and Japan. This environment continues to support JPY carry trades, where investors leverage the low-interest Japanese Yen to invest in higher-yielding US Dollar assets.

The US Dollar (USD) strengthened due to elevated US Treasury yields, partly influenced by heightened risk aversion ahead of the release of US Gross Domestic Product Annualized (Q1) data on Thursday. Additionally, market participants are awaiting the release of the Core Personal Consumption Expenditures (PCE) Price Index data on Friday, which are expected to provide insights into the Federal Reserve’s potential stance on interest rate adjustments.

In other news:

– Federal Reserve Bank of Atlanta President Raphael Bostic stated on Thursday that the path of inflation is expected to be uneven, and a decrease in inflation breadth would strengthen confidence in the necessity of a rate cut.

– The Fed Beige Book report, covering the period from April to mid-May, revealed slight growth in national economic activity, with mixed conditions across industries and districts. The report indicated slight employment growth, moderate wage growth, and modest price increases as consumers resisted further price hikes.

– Neel Kashkari, President of the Federal Reserve Bank of Minneapolis, suggested the possibility of a rate hike, expressing doubts about the disinflationary trend and projecting only two rate cuts.

– The US Housing Price Index (MoM) for March underperformed expectations, posting a 0.1% increase compared to the expected 0.5%.

– Japan’s Weighted Median Inflation Index rose by 1.1% in April, representing a slowdown from the 1.3% increase recorded in March.

– Japan’s Corporate Service Price Index (CSPI) posted a year-over-year reading of 2.8% in April, surpassing expectations and marking its fastest rate of increase since March 2015.

– Japan’s Finance Minister Shun’ichi Suzuki highlighted the importance of stable currency movements aligned with fundamentals, stating close monitoring of foreign exchange (FX) movements without commenting on currency intervention.

USDCHF – Nears 0.9100 as Swiss GDP Beats Expectations

The Swiss franc is appreciated after the Q1 GDP data came at 0.50% QoQ compared to 0.30% QoQ , Annualised data came at 0.60% YoY in Q1 when compared to 0.50% YoY last time. The Swiss trade surplus data came at $ 4316 Million in the April month from $3767 Million in the past month.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

This decline was attributed to the Swiss Franc (CHF) gaining traction following the release of Switzerland’s Gross Domestic Product (GDP) report for the first quarter (Q1) of 2024, which surpassed expectations. Currently, the USD/CHF pair is trading 0.32% lower for the day.

According to data revealed by the State Secretariat for Economic Affairs (SECO) on Thursday, the Swiss economy demonstrated continued expansion in Q1. Switzerland’s GDP exhibited a quarter-on-quarter (QoQ) growth of 0.5% in Q1, surpassing both the estimated and previous readings of 0.3% expansion. On an annual basis, the GDP figure for Q1 stood at 0.6% year-on-year (YoY), exceeding the market consensus of 0.5%. This positive GDP reading provided support to the CHF and pushed the USD/CHF pair to weekly lows.

In addition to the GDP data, the Federal Office for Customs and Border Security (FOCBS) reported that Switzerland’s trade surplus increased to $4,316 million in April from $3,767 million in March.

Furthermore, escalating geopolitical tensions in the Middle East have led to increased demand for safe-haven assets like the Swiss Franc (CHF). The BBC reported on Wednesday that Israel’s military has taken control of the Philadelphi Corridor, a strategically significant buffer zone along the Gaza-Egypt border, thereby asserting control over Gaza’s entire land border.

Regarding the USD, hawkish statements from Federal Reserve officials and stronger-than-expected US economic data have raised expectations that the US central bank may postpone interest rate cuts this year. Fed Atlanta President Bostic expressed optimism on Wednesday that the elevated price pressures witnessed during the COVID-19 pandemic would decline over the next year. However, he noted that the Fed still has work to do to address significant price growth seen over recent years.

Financial markets are currently pricing in a 50% possibility that the Fed will maintain interest rates in September, according to the CME FedWatch Tool. This wait-and-see approach by the Fed could provide some support to the Greenback and limit downside pressure on the USD/CHF pair.

Investor focus will now shift to the second estimate of the US Gross Domestic Product (GDP) for Q1 2024, expected to expand by 1.3%, which will be released on Thursday.

USDCAD – Approaches Weekly High Around 1.3740 Amid Strong US Dollar

The Canadian Dollar is moving down ahead of Q1 GDP data is scheduled tomorrow and is expected 2.2% on Annual basis expansion. US Core PCE Index is expected to expanded at 2.8% YoY and 0.30% MoM. The BoC is going to do rate cut in the June month if Q1 GDP Looms in the market tomorrow.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The robust demand for the US Dollar is fueled by a sharp decline in traders’ expectations for the Federal Reserve (Fed) to implement interest rate cuts during the September meeting.

Investor sentiment remains risk-averse amid concerns about the Fed potentially delaying rate cuts until the last quarter of the year. This sentiment is reflected in significant losses observed in S&P 500 futures during the Tokyo session, indicating a marked decrease in investors’ risk appetite. The prospect of prolonged higher interest rates by the Fed is favorable for yields on interest-bearing assets. Although 10-year US Treasury yields have slightly declined to 4.61%, they remain close to a nearly four-week high.

Meanwhile, investors eagerly await the release of the United States core Personal Consumption Expenditure Price Index (PCE) data for April, which is expected to significantly influence speculation regarding Fed rate cuts in September. This crucial inflation data is scheduled for publication on Friday, with analysts estimating steady growth in both annual and monthly core PCE inflation readings, at 2.8% and 0.3% respectively.

On the Canadian Dollar front, investors are awaiting the release of Gross Domestic Product (GDP) data for various timeframes, also scheduled for Friday. On a month-on-month basis, the Canadian economy is projected to have stagnated after expanding by 0.2% in February. For the first quarter of the year, the economy is forecasted to have grown by 2.2% on an annualized basis. Weak GDP figures could increase the likelihood of the Bank of Canada (BoC) initiating interest rate cuts starting from the June meeting.

USD INDEX – Bostic: Price Gain Breadth Supports Cut Confidence

The Atlanta FED President Raphael Bostic said inflation trend is down and we need to do rate cuts if inflation towards 2% target. Labour market is very tight but not meet our expected area. So US economy is doing well right situation and rate cuts is needed for expansion of economy in the coming months.

USD INDEX is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

On Thursday, Federal Reserve Bank of Atlanta President Bostic expressed his views on inflation and its implications for monetary policy. Bostic emphasized that the trajectory of inflation is expected to be irregular, indicating a potentially turbulent journey ahead. He noted a downward trend in general inflation, cautioning that the path toward achieving the Fed’s target of 2% inflation is not guaranteed. Despite acknowledging a tight job market, Bostic pointed out that it’s not as constrained as it once was.

Of particular significance was Bostic’s observation regarding the breadth of price gains, which he deemed to be still substantial. However, he also highlighted that a reduction in the breadth of inflationary pressures would bolster confidence among policymakers for implementing a rate cut.

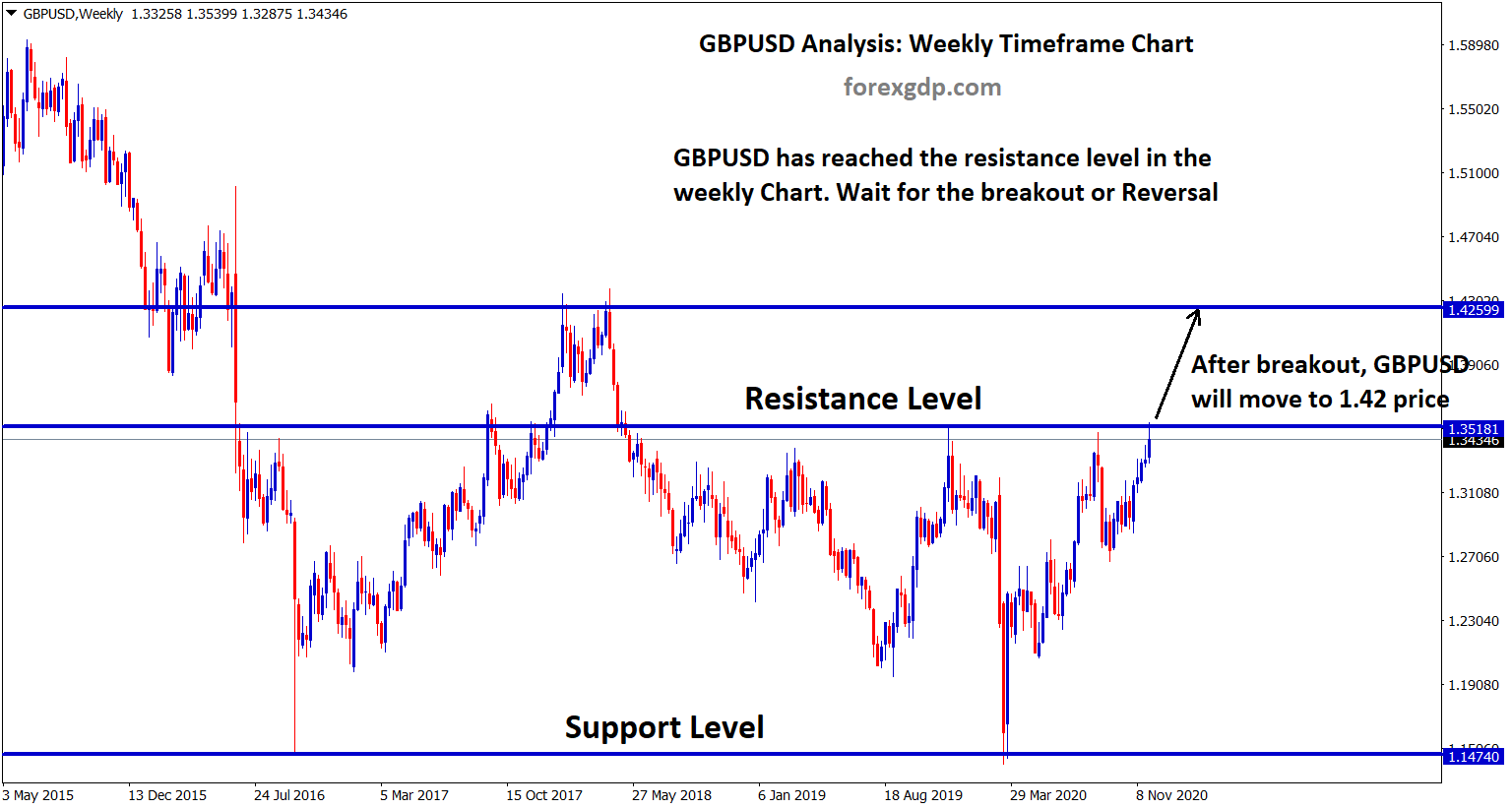

GBPUSD – remains below 1.2700 amid stronger USD and elevated US yields

The IMF Expected BoE to do 2-3 rate cuts this year and this mark moved down GBP against counter pairs. Inflation is steady down in the April month makes possible rate cut in the near month from BoE. July month UK Election causes Political moves in the market.

GBPUSD is moving in the Symmetrical triangle pattern and the market has fallen from the top area of the pattern

This decline is attributed to the prevailing strength of the US Dollar (USD), supported by higher US yields and reduced expectations of a Federal Reserve (Fed) rate cut in September.

In recent weeks, Fed officials have adopted a cautious stance regarding the inflation outlook, leading traders to revise down their expectations of monetary easing this year. According to the CME FedWatch Tool, markets are now indicating a 50% probability of the Fed maintaining interest rates in September. This cautious sentiment, coupled with robust US economic data, has bolstered the Greenback in recent trading sessions.

Market participants are eagerly awaiting the release of the second estimate of the US Gross Domestic Product (GDP) for Q1 2024 on Thursday, which is anticipated to show a growth rate of 1.3%. A stronger-than-expected GDP reading could further boost the USD, exerting downward pressure on GBP/USD. Additionally, scheduled releases such as the US weekly Initial Jobless Claims, Goods Trade Balance, Pending Home Sales, and speeches by Fed officials Raphael Bostic, John Williams, and Lorie Logan could influence market sentiment.

Meanwhile, speculation is growing that the Bank of England (BoE) may initiate interest rate cuts at its August meeting due to a softer UK inflation outlook. The International Monetary Fund (IMF) has projected two to three rate cuts by the BoE. With limited high-impact economic data releases from the UK, political uncertainty surrounding upcoming elections may impact the Pound Sterling (GBP). Concerns regarding political instability could undermine the GBP’s performance and limit the upside potential for the GBP/USD pair in the near term.

AUDUSD – RBA’s Hunter Concurs with Treasury’s Inflation Forecast

The RBA Chief Economist Sarah Hunter said I am totally agree with Treasury forecast on inflation this year and RBA is doing on right track on controlling inflation in the Australian Economy. Wages are higher and Consumer spending is more what we expected, So rate hikes are continue in the coming months in order to stabilize the inflation with in the target levels.

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

Sarah Hunter, Chief Economist of the Reserve Bank of Australia (RBA), stated on Thursday that the bank aligns with the inflation forecast presented by the Treasury.

Hunter elaborated that the Consumer Price Index (CPI) data confirmed strength in certain price sectors, indicating a robust economic environment. She emphasized that the RBA Board is diligently monitoring inflation to ensure it remains within the desired range, underscoring the importance of maintaining stability in inflation rates.

Furthermore, Hunter noted that wages growth appears to be nearing its peak, suggesting a potential stabilization in labor market conditions. This observation adds another dimension to the RBA’s assessment of economic trends and factors influencing inflation dynamics.

NZDUSD – NZ 2024 Budget: Treasury Predicts Sub-3% Inflation by Q3 2024, 2% by 2026

The NZ Budget released today and said Operating balance is NZ$ -11.07Billion before losses and gains in the Fiscal year 24-25 from NZ$ -9.32 Billion. This operating balance will come to surplus by FY-27-2028 year. GDP this year forecasted to 1.7% from 1.5% last year. Nearly 43.1% in GDP to Debt ratio in the NZ down from 43.5% in the last year. Unemployment rate is forecasted to 5.2% in this year and inflation will down in Q32024 to below 3% and come to 2% in the 2026. GDP is like to contract in 1H 2024 and then expanded by 2H 2024.

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

New Zealand’s Finance Minister, Nicola Willis, unveiled the government’s annual Budget report for 2024, outlining key projections and targets for the upcoming fiscal period. Here are the significant highlights from the Budget:

– The operating balance before gains and losses for the fiscal year 2023/24 is forecasted to be NZ$-11.07 billion, compared to NZ$-9.32 billion in the Half-Year Economic and Fiscal Update (HYEFU).

– The Gross Domestic Product (GDP) growth for the fiscal year 2024/25 is estimated at 1.7%, an increase from the HYEFU projection of 1.5%.

– The government anticipates a return to operating balance before gains and losses (OBEGAL) surplus in the fiscal year 2027/28, as opposed to the HYEFU expectation of 2026/27.

– Net debt for the fiscal year 2023/24 is forecasted to be 43.1% of GDP, slightly lower than the HYEFU projection of 43.5%.

– The unemployment rate is expected to remain at 5.2% in the fiscal year 2024/25, consistent with the HYEFU forecast.

– The government is committed to achieving a surplus in the OBEGAL by the fiscal year 2027/28.

– Tax relief initiatives will be fully funded through savings and revenue-generating measures.

– The Treasury predicts a contraction in New Zealand’s GDP in the first half of 2024, followed by growth in the second half of the year.

– Inflation is projected to decrease to below 3% in the third quarter of 2024, with further decline to 2% expected around 2026.

In addition to the Budget announcement, New Zealand’s Debt Management Office (DMO) disclosed plans to increase gross bond issuance for the fiscal year 2024/25 to NZ$38 billion, up from NZ$36 billion as indicated in the half-year update. The total gross bond issuance planned for the four years up to June 2028 now stands at NZ$126 billion, reflecting an increase from NZ$114 billion projected in the half-year update.

CRUDE OIL – WTI Near $79.00 Before Key US Economic Releases

The Oil stock is expected to decrease in the May 24 ending report from US EIA firm and API Already reported 6.4 Million barrels down from 2.4 Million Barrels surplus last week. The OPEC+ meeting is conducted on June 01 and expected to 2.2 Million barrels per day cut in this meeting.

XTIUSD Crude oil price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Traders are closely monitoring the upcoming release of the US crude oil stocks change report by the Energy Information Administration later today. Market projections suggest that US energy firms may draw down approximately 1.9 million barrels of crude from storage in the week ending May 24, following a previous addition of 1.825 million barrels in the preceding week. Notably, the API Weekly Crude Oil Stock report for the prior week indicated a significant decrease of 6.49 million barrels, contrasting with the 2.48 million barrels added in the week prior.

Furthermore, traders are eagerly awaiting the upcoming meeting of the Organization of the Petroleum Exporting Countries (OPEC) and its allies, including Russia (OPEC+), scheduled for June 2. During this meeting, member producers will deliberate on the extension of voluntary output cuts of 2.2 million barrels per day into the latter half of 2024. It is widely anticipated that the group will opt to maintain these supply cuts, which could impact crude oil prices.

In addition, hawkish remarks from Minneapolis Fed President Neel Kashkari have heightened concerns about potential rate hikes. Kashkari hinted at the possibility of a rate hike, expressing doubts about the prevailing disinflationary trend. These remarks, coupled with rising Treasury yields, driven by investor risk aversion ahead of the release of US Gross Domestic Product Annualized (Q1) data on Thursday and the Core Personal Consumption Expenditures (PCE) Price Index data scheduled for Friday, have bolstered the strength of the US Dollar. Consequently, oil prices may face downward pressure as the US Dollar strengthens, making oil more expensive for countries purchasing it with other currencies.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!