AUDUSD – Australian Dollar Drops on Unexpected Current Account Deficit

The Australian Current Account Deficit shows -A$4.9 Billion from A$2.7 Billion Surplus in the previous quarter and A$ 5.9 Billion Surplus is expected in Q1. The Australian economy faces trouble in the exports of Coal and Iron Ore Production, So Exports data fell by 1.5% in Q1 and Imports data grew by 4.5% in the Q1, The Australian Dollar little down after the data printed today.

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Australian Dollar (AUD) halted its three-day winning streak on Tuesday, likely due to Australia’s unexpected current account deficit of A$ 4.9 billion (USD 3.2 billion) in the first quarter. This shift from a downwardly revised surplus of A$ 2.7 billion in the previous quarter missed market expectations of an A$ 5.9 billion surplus.

In a media release from the Australian Bureau of Statistics (ABS), Grace Kim, ABS head of International Statistics, stated: “The current account deficit reflects a smaller trade surplus, driven by a rise in the imports of goods, while the net primary income deficit increased.” Imports of goods rose by 4.5% in Q1, driven by consumption goods, while exports of goods fell by 1.5%, reflecting reduced domestic coal and iron ore production.

The US Dollar (USD) edged higher as US Treasury yields improved, attributed to prevailing risk aversion. However, the Greenback may face challenges as Federal Reserve (Fed) officials indicated last week that the central bank could achieve its 2% annual inflation target without further interest rate hikes.

Investors are likely awaiting Australia’s Gross Domestic Product (GDP) data for the first quarter and China’s Caixin Services PMI for May, both set to be released on Wednesday. In the US, attention will be paid to the ADP Employment Change and ISM Services PMI reports.

Daily Digest Market Movers:

– Australian Dollar depreciates due to risk aversion

– The ISM Manufacturing PMI unexpectedly dropped to 48.7 in May, down from April’s reading of 49.2 and below the forecast of 49.6. The US manufacturing sector experienced its second consecutive month of contraction, marking the 18th in the last 19 months.

– Australia’s Judo Bank Manufacturing PMI, released on Monday, edged up slightly to 49.7 in May from 49.6 in April, marking the fourth consecutive month of declining conditions in the manufacturing sector.

– On Monday, the Caixin China Manufacturing PMI rose to 51.7 in May from 51.4 in April, marking the seventh consecutive month of expansion in factory activity and surpassing estimates of 51.5. Friday’s NBS PMI data showed that manufacturing activity fell to 49.5 in May from 50.4 in April, missing the market consensus of an increase to 50.5. Meanwhile, the Non-Manufacturing PMI declined to 51.1 from the previous reading of 51.2, falling short of the estimated 51.5.

– Last week, Atlanta Fed President Raphael Bostic remarked in an interview with Fox Business that he doesn’t believe further rate hikes should be required to reach the Fed’s 2% annual inflation target. Additionally, New York Fed President John Williams stated that inflation is still too high but should moderate over the second half of 2024. Williams doesn’t feel the urgency to act on monetary policy, per Reuters.

– According to a Bloomberg report, RBA Assistant Governor Sarah Hunter said at a conference in Sydney on Thursday that “inflationary pressures” are the key issue. “We’re very mindful of that.” Hunter also stated that the RBA Board is concerned about inflation remaining above the target range of 1%-3%, suggesting persistent inflationary pressure. Wages growth appears to be near its peak.

XAUUSD – Gold flat, downside limited

The Gold prices are moving higher after the US ISM Manufacturing PMI data came at 48.7 in the May month versus 49.2 printed in the April month. This NFP data is scheduled and Last week Core PCE index came at 2.8% YoY makes US Dollar weaker against Gold.

XAUUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

On Tuesday, the gold price (XAU/USD) shows a bearish trend during the European session, partially reversing Monday’s gains from a recent low. Despite the Federal Reserve’s anticipated rate cuts later this year, which have pushed the US Dollar to a near two-month low, gold hasn’t seen significant bullish movement.

Geopolitical risks continue to bolster the positive outlook for gold, suggesting that any declines could be considered buying opportunities. Traders remain cautious ahead of crucial US macroeconomic data and central bank events this week, including the Nonfarm Payrolls report on Friday, the Bank of Canada’s decision on Wednesday, and the European Central Bank meeting on Thursday.

Easing inflationary pressures and slowing economic growth have strengthened expectations for a Fed rate cut, which typically supports gold prices. Recent data from the US Bureau of Economic Analysis showed stable PCE Price Index figures, while the ISM Manufacturing PMI dropped, signaling a slowdown in economic activity. This has led to lower US Treasury bond yields and a weaker US Dollar, factors that usually boost gold.

In the short term, traders will focus on US economic data, including JOLTS Job Openings and Factory Orders due on Tuesday, and the ADP employment report on Wednesday. These events, along with central bank decisions, are expected to significantly influence the near-term direction of gold prices.

Despite these developments, gold’s bearish bias remains intact. However, persistent geopolitical risks and a dovish Fed stance are likely to limit further downside, making gold an attractive option for investors seeking stability amid uncertainty. The market’s attention is now on the upcoming data and events that will shape gold’s trajectory in the coming days.

EURUSD – near March peak at 1.0900+

The Euro pairs little stronger against counter pairs due to rate cuts expected this week from ECB. Yesterday US Domestic data gives negative reading than expected gives Boost for Euro pair against USD. Decreasing growth in the Euro zone makes way for rate cuts from ECB is expected.

EURUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Euro Firms Near March Highs, Awaits ECB Cues

The Euro (EUR) is trading near its highest level since March against the US Dollar (USD) but lacks strong momentum. Investors are cautious before committing to further gains ahead of the key European Central Bank (ECB) meeting on Thursday.

The recent EUR/USD rise is primarily driven by a weakening USD. Disappointing US manufacturing data on Monday fueled expectations of a Federal Reserve rate cut later this year, pushing down Treasury yields and undermining the Dollar. This has benefited the Euro, which currently sits just above the 1.0900 mark, a key resistance level.

However, market participants are hesitant to take aggressive long positions on the Euro. They are waiting for clues about the ECB’s monetary policy stance at its upcoming meeting. Investors will focus on comments from ECB officials and economic projections to gauge the likelihood of future rate hikes in response to rising Eurozone inflation. The ECB’s stance will be crucial in determining the Euro’s trajectory, especially before the release of the US Nonfarm Payrolls report on Friday.

Despite the caution, the underlying fundamentals suggest potential upside for the EUR/USD pair. Any significant dips could be viewed as buying opportunities. Technically, a sustained move above 1.0900 could further embolden bulls and validate a near-term positive outlook for the Euro. In the meantime, traders are watching German employment data and US economic releases (JOLTS Job Openings and Factory Orders) for short-term trading opportunities.

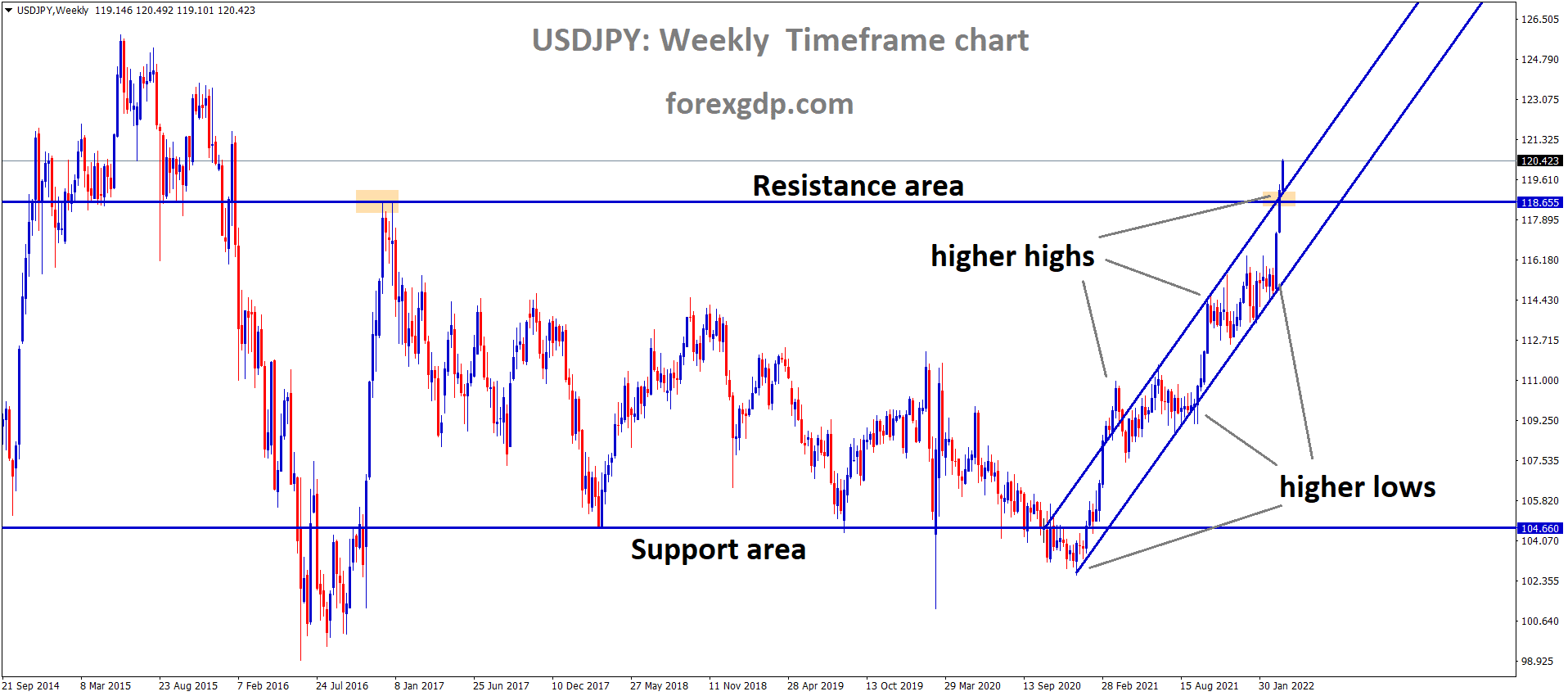

USDJPY – BoJ Deputy Governor: Easy money’s long-term economic impact needs attention.

The BoJ Deputy Governor Ryozo Himino said Long term Lower rates is helpful for economic productivity and Growth. Firms are easy to fix the prices based on Products and Wages of Labour cost.BoJ do rate hike until the inflation returned to 2% target.

USDJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Here’s a rewrite of the quotes by Ryozo Himino, Deputy Governor of the Bank of Japan:

Central bank policymakers need to be aware of the long-term risks of keeping interest rates too low, as it can hinder economic growth.

Businesses would have more flexibility in adjusting prices if both prices and wages were rising at a moderate and steady pace.

")

When interest rates are near zero, central banks can influence the economy by impacting foreign exchange rates, stock prices, and real estate prices.

The Bank of Japan is aiming for an inflation rate of around 2%, excluding temporary factors.

USDCHF – Rebounds Despite Swiss CPI Rise

The Swiss CPI inflation data came at 1.4% YoY in the May month versus same reading in the previous month. MoM data came at 0.30% MoM versus 0.40% printed in the April month. Slight decrease in the inflation expected SNB rate cuts in the June month. But SNB Chairman Thomas Jordan said FX Intervention will be there inorder to keep CHF higher.

USDCHF has broken the Descending triangle pattern in downside

Swiss Franc Slips on Cooler Inflation, But SNB Intervention Lurks

The Swiss Franc (CHF) weakened against the US Dollar (USD) on Tuesday, snapping a three-day losing streak for the USD/CHF pair. This follows the release of Switzerland’s Consumer Price Index (CPI) data:

Swiss Inflation Cools: Year-over-year inflation came in at 1.4%, lower than expected, raising hopes for a Swiss National Bank (SNB) rate cut later this month.

Monthly CPI Below Consensus: The monthly inflation figure of 0.3% also fell short of market expectations, further strengthening the case for a dovish SNB.

However, the CHF’s decline might be limited due to:

SNB Intervention Potential: SNB President Jordan has previously hinted at intervening in currency markets to control inflation, potentially supporting the CHF.

Focus Shifts to US Data and Potential Fed Rate Cuts

Despite the Swiss inflation data, the USD could still face pressure due to:

Steady US PCE Inflation: April’s PCE inflation data remained unchanged, potentially paving the way for a more dovish Fed.

Weaker US Manufacturing PMI: The May ISM Manufacturing PMI came in weaker than expected, increasing the likelihood of the Fed delaying rate hikes.

US Jobs Report on Watch:

Investors are now looking forward to the US Nonfarm Payrolls data on Friday.

A weaker-than-expected jobs report could further weaken the USD against the CHF.

Overall, the USD/CHF pair is experiencing a temporary reprieve due to the cooler Swiss inflation data. However, the potential for SNB intervention and upcoming US jobs data could still influence the currency pair’s direction.

USDCAD – vulnerable above 1.3600 before BoC

The Canadian Dollar plunging down ahead of BoC rate cut expected tomorrow. The easing Q1 GDP and inflation proving Canadian economy is slowdown than 2022 rate hike started. Oil prices are also down due to OPEC+ cuts, this is another drawback for Canadian Dollar.

USDCAD is moving in the Descending triangle pattern and the market has rebounded from the support area of the pattern

Softer US Dollar: The greenback dipped below the 104.00 support level on Monday due to disappointing US manufacturing data. The Institute for Supply Management (ISM) reported a contraction in manufacturing activity for the second month in a row, with the PMI falling to 48.7 (below expectations). This has fueled speculation of potential interest rate cuts by the Federal Reserve (Fed) later this year, weakening the USD.

Focus Shifts to US Services PMI and NFP: While the manufacturing data dampened USD sentiment, investors are now looking ahead to Wednesday’s US Services PMI release and the highly anticipated Nonfarm Payrolls (NFP) report on Friday. A strong NFP showing (estimated at 190,000 jobs added) could reverse the USD’s downward trend.

Looming BoC Rate Cut: The Bank of Canada (BoC) is expected to cut its interest rate by 25 basis points to 4.75% on Wednesday, as Canadian inflation cooled down in April. This dovish stance by the BoC, compared to the potentially hawkish Fed, could weigh on the CAD and benefit the USD/CAD pair. However, BoC Governor Tiff Macklem has emphasized that the rate decision will be data-dependent.

Key Factors to Watch:

US Services PMI (Wednesday): A strong reading could support the USD.

US Nonfarm Payrolls (NFP) (Friday): A stronger-than-expected report could significantly boost the USD.

BoC Rate Decision (Wednesday): A larger-than-expected rate cut (or dovish comments) could weaken the CAD.

The interplay of these factors will determine the fate of the USD/CAD pair in the coming days. If the BoC delivers a sizeable rate cut while US economic data disappoints, the recent USD weakness could extend, pushing the pair below 1.3600. However, a strong NFP report and a cautious BoC could trigger a USD rebound.

USD INDEX – USD steadies after PMI drop

The US Dollar moved down after the US ISM Data came at 48.7 in the May month versus 49.2 printed in the April month. Inflation price index came at 57 in the May month from 60.9 printed in the April month. Easing pricing pressures US Dollar moving down on the expectations of FED September rate cut.

USD INDEX is moving in an Ascending channel and the market has reached the higher low area of the channel

US Dollar Recovers After Monday’s Plunge, Key Data on Tap

The US dollar (USD) staged a tentative comeback on Tuesday after a steep selloff in the previous session. The greenback had fallen against its major rivals on Monday following disappointing economic data that fueled speculation of an interest rate cut by the Federal Reserve later this year.

The Institute for Supply Management (ISM) reported that its closely watched Manufacturing Purchasing Managers’ Index (PMI) dropped to 48.7 in May, down from 49.2 in April. This indicates a continued contraction in manufacturing activity, with the rate of decline accelerating. Additionally, the Prices Paid Index, a measure of input inflation within the manufacturing sector, fell to 57 from 60.9. This suggests that inflationary pressures are easing, potentially giving the Fed more room to maneuver on interest rates.

The weak data triggered a sharp decline in the USD Index, a measure of the dollar’s strength against a basket of six major currencies. The index fell to its lowest level since early April before recovering slightly in early Tuesday trading. It currently sits around 104.00.

The selloff in the dollar was compounded by a significant fall in US Treasury bond yields. The yield on the benchmark 10-year Treasury note plunged nearly 2.5% on Monday, reflecting investor expectations of a potential rate cut by the Fed.

Later today, the focus will shift to the release of additional US economic data. April’s Factory Orders and JOLTS Job Openings figures are expected to provide further insights into the health of the US economy and could influence market sentiment towards the dollar. Finally, US stock index futures are currently trading slightly lower, suggesting a cautious mood among investors.

GBPUSD – GBP Up on Weak US Data

The GBP is rose against USD after the US ISM PMI Data contraction in the May month, inflation prices pressures are down in the products. So Rate cut from FED is expected in the September month. BoE is expected to do in the August month after the UK elections this year.

GBPUSD is moving in the Symmetrical triangle pattern and the market has reached the top area of the pattern

GBP Up on Weak US Data, BoE Rate Cut Eyed

The British Pound (GBP) is strengthening against the US Dollar (USD) on Tuesday, buoyed by a weaker USD after the release of disappointing US manufacturing data.

Softer Dollar: The greenback came under pressure after the Institute for Supply Management (ISM) reported that the US manufacturing sector contracted at an accelerating pace in May. The ISM Manufacturing PMI dropped to 48.7 in May, down from 49.2 in April and below market expectations. This suggests a slowdown in the US economy, which is weighing on the USD.

Fed Rate Cut Expectations: The weaker PMI data has reinforced expectations that the Federal Reserve will cut interest rates this year. Traders are now pricing in nearly a 53% chance of a rate cut in September, up from 49% before the report. This shift in expectations is positive for the GBP, as it makes the USD less attractive to investors.

BoE Rate Cut Possibilities: The Bank of England (BoE) is also considering cutting interest rates, as UK inflation has eased recently. However, BoE policymakers are cautious due to concerns about slow progress in reducing inflation within the service sector. The outlook for BoE rate cuts remains uncertain, but it is a factor that could support the GBP in the coming months.

In the absence of major economic data releases from the UK this week, the GBP/USD is likely to be primarily driven by USD price dynamics. If the USD weakens further, the GBP could rise towards its multi-week highs near 1.2810.

NZDUSD – NZD Up Near 0.6200 on Weak US PMI

NZ Dollar moved higher after the US economy weaker data in manufacturing sector in the May month. RBNZ Hawkish stance on the monetary policy and no rate cut in this year until inflation target 2% to achieve said by RBNZ Deputy Governor Christian Hawkesby last week. This news also boosted Kiwi against counter pairs.

NZDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

NZD Climbs Near 0.6200 on Weak US Data, Awaits Key Events

The New Zealand Dollar (NZD) is strengthening against the US Dollar (USD), consolidating gains near 0.6190 early Tuesday in Asia. This rise is primarily driven by:

Weak US Data: Disappointing US manufacturing data released Monday significantly impacted the USD. The Institute for Supply Management (ISM) reported a contraction in manufacturing activity for the second consecutive month, with the PMI falling to 48.7 (below expectations). This has fueled speculation of potential interest rate cuts by the Federal Reserve (Fed) later this year, weakening the USD.

Increased Odds of Fed Rate Cuts: Following the weak data, investors are now pricing in a higher probability of a Fed rate cut in September. According to the CME FedWatch tool, the odds have climbed to nearly 53%, up from 49% before the data was released.

NZD Supported by External Factors:

Strong Chinese Manufacturing Data: The positive Chinese Caixin Manufacturing PMI for May boosted the NZD. As a major trading partner of China, New Zealand’s economy benefits from China’s growth.

Hawkish RBNZ Stance: Recent comments from Reserve Bank of New Zealand (RBNZ) Deputy Governor Christian Hawkesby suggesting a hold on interest rate cuts further strengthened the NZD. This contrasts with the Fed’s potentially dovish stance, creating a relative advantage for the NZD.

Upcoming Events in Focus:

US ISM Services PMI (Wednesday): A strong reading could support the USD and potentially weaken the NZD.

US Nonfarm Payrolls (Friday): A stronger-than-expected NFP report could significantly bolster the USD and put downward pressure on the NZD.

The NZD/USD pair is likely to remain sensitive to upcoming US economic data releases and the Fed’s monetary policy signals. If the US data continues to disappoint and the Fed strengthens its dovish stance, the NZD could extend its gains towards 0.6200 or higher. However, a positive surprise in the US data or a more cautious Fed could reverse the trend and weaken the NZD.

CRUDE OIL – Oil down as OPEC+ to ease cuts

The Oil prices are dropped after the OPEC+ allies agreed to output cut of 2.2Million Barrels perday upto June 2025. US announced yesterday they are going to purchase 3 million barrels per day for Strategic reserves for the US. This news is the support for Oil prices to drive flat not for plunging efforts.

XTIUSD Crude oil price is moving in the Descending channel and the market has reached the lower low area of the channel

Oil Prices Slide on OPEC+ Production Cut Easement, US Rate Hike Worries

Oil prices extended their decline on Tuesday, falling for the fifth consecutive day. West Texas Intermediate (WTI) crude oil dipped to around $73.90 per barrel, pressured by two key factors:

OPEC+ Production Cut Rollback: The Organization of the Petroleum Exporting Countries and allies (OPEC+) announced a plan to gradually ease their oil production cuts. This move will bring more oil back to the market, potentially exceeding demand and driving prices down. The cuts will be phased out over a year, starting in October with an initial increase of 500,000 barrels per day (bpd) and reaching a total of 1.8 million bpd by June 2025.

US Rate Hike Concerns: Despite easing inflation data, the Federal Reserve’s (Fed) commitment to raising interest rates continues to weigh on oil prices. Higher interest rates can weaken economic growth and dampen demand for oil.

Additional factors impacting the market:

US Strategic Petroleum Reserve Replenishment: The US announced the purchase of an additional 3 million barrels of oil for its Strategic Petroleum Reserve (SPR). While this move may temporarily support oil prices, it’s part of a gradual replenishment effort following a large sale in 2022.

The interplay of these factors is creating a bearish sentiment in the oil market, with prices potentially continuing their downward trend until a clearer picture emerges regarding global oil demand and the Fed’s monetary policy.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!