XAUUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

XAUUSD – Gold Price Struggles Amid Fed’s Hawkish Stance and Stronger US Dollar

The Gold prices are moving in the Flat after the China paused the Gold purchases in this month as per Survey shows. So Far $72.80 Million Troy ounces of Gold are bought by China, US Domestic data moving downwards makes Gold to upside pressures.

The Federal Reserve’s recent hawkish stance on interest rates, signaling only one potential rate cut in 2024, continues to weigh on the precious metal, which offers no yield. This stance is a significant headwind for gold. Additionally, a generally positive risk sentiment and a slight uptick in the US Dollar further limit the upside for gold.

Market sentiment still reflects expectations that the Fed might initiate rate cuts sooner than later, driven by easing inflationary pressures in the US. This has pushed US Treasury bond yields down to their lowest levels since April, potentially restraining significant gains for the US Dollar and providing some support to gold, which is denominated in USD. Moreover, ongoing geopolitical tensions in the Middle East and political uncertainties in Europe caution against aggressive bearish bets on XAU/USD, as these factors historically support safe-haven assets.

Recent economic data underscored these dynamics: the Producer Price Index (PPI) for final demand in May showed a 2.2% year-on-year increase, slightly below expectations and April’s figures. Core PPI, excluding volatile items, rose by 2.3% annually, indicating moderate inflationary pressures. In contrast, the Consumer Price Index (CPI) earlier in the week indicated stable consumer prices, while initial jobless claims in the US rose more than anticipated.

Adding to the geopolitical landscape, a snap election call in France has added to broader political uncertainties, further supporting the safe-haven appeal of gold amidst ongoing conflicts such as Russia’s actions in Ukraine and turmoil in the Middle East.

Looking ahead, investors are eyeing the preliminary release of the Michigan US Consumer Sentiment Index, which could influence short-term trading dynamics for the USD and potentially impact gold prices on the final trading day of the week.

EURUSD – Steady Below 1.0750 Amid Stronger US Dollar and Political Uncertainty in France

The Euro pairs are moving down against counter pairs due to France President Emmanuel Macron said for election to conduct to prove who is the more majority after the Far Right party wins in the Parliament vote on last week. Euro zone CPI data is moderate and no consecutive rate cuts is not seen in the market as per ECB Members view.

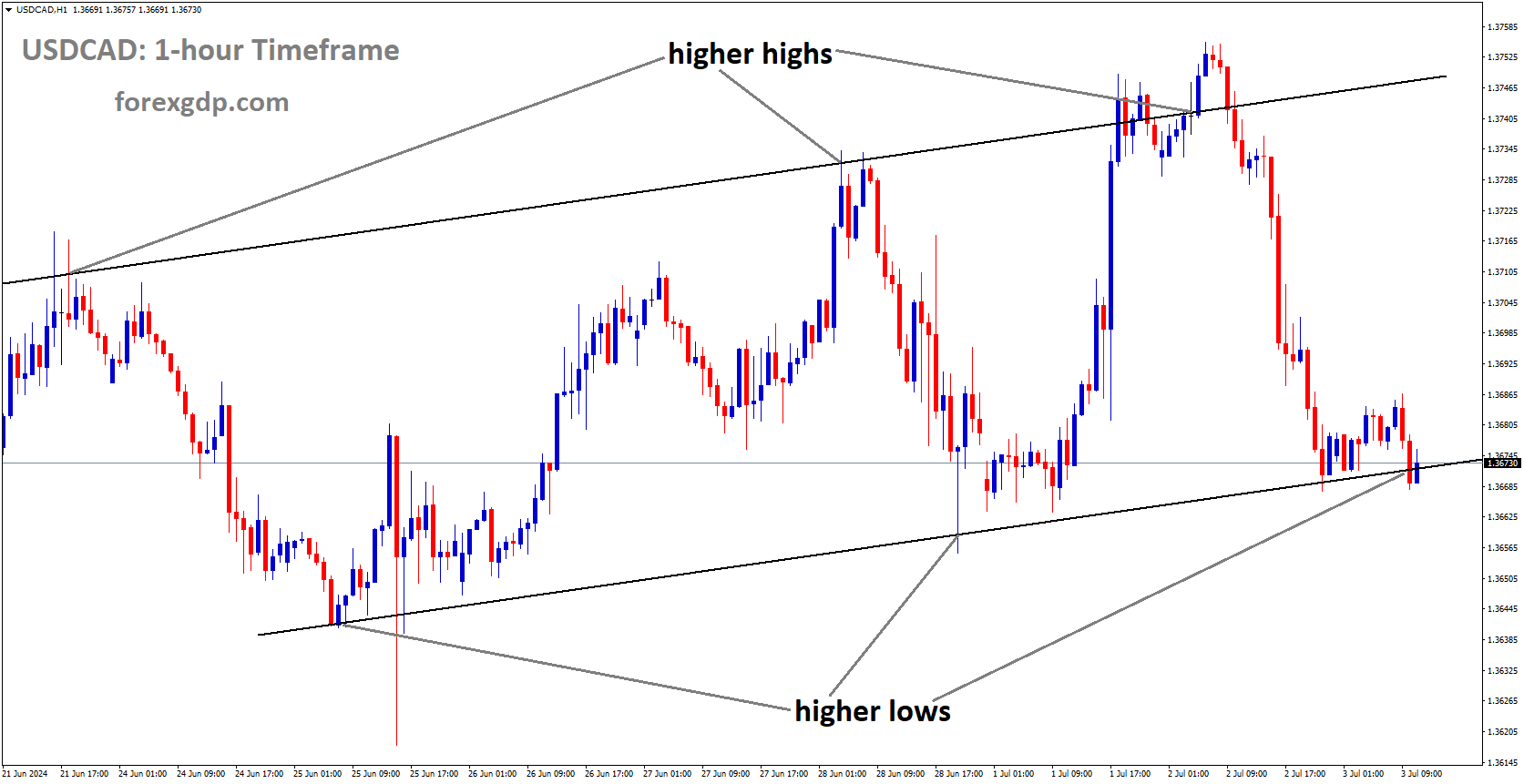

EURUSD has broken the Ascending channel in the downside

The EUR/USD pair traded flat around 1.0735 during Friday’s early Asian session. Market sentiment remained cautious due to uncertainties stemming from European parliamentary elections. Particularly notable was the situation in France, where President Emmanuel Macron dissolved parliament following a defeat by the far-right National Rally, potentially paving the way for increased political volatility.

Investor focus also turned to upcoming events, including a speech by ECB President Christine Lagarde and the release of the preliminary US Michigan Consumer Sentiment report for June. The European Central Bank (ECB) had recently cut interest rates by 25 basis points during its June meeting, aligning with market expectations. This move reduced the ECB’s key rate to 3.75%, following a previous record rate of 4% since September 2023. Financial markets have already priced in another rate cut this year, with economists predicting two additional cuts by the end of 2024, as reported by Reuters.

On the other side of the Atlantic, recent US economic indicators painted a mixed picture. The US Producer Price Index (PPI) for May showed weaker-than-expected results, with a year-on-year increase of 2.2%, down from April’s revised figure of 2.3%. Similarly, the core PPI, excluding food and energy prices, rose by 2.3% year-on-year, below both consensus forecasts and the previous month’s reading of 2.4%. Meanwhile, US Initial Jobless Claims for the week ending June 6 exceeded expectations, rising to 242,000 from the previous week’s 229,000, and surpassing the consensus estimate of 225,000.

Despite the softer US economic data, the US Dollar (USD) maintained strength against its counterparts. This resilience was underpinned by the Federal Reserve’s (Fed) indication that it anticipates only a single 25 basis points rate cut towards the end of 2024. Fed Chair Jerome Powell emphasized that while some progress had been made towards inflation targets, substantial improvements would be necessary before further rate adjustments. This stance from the Fed supported the USD, despite the disappointing economic releases.

In summary, the EUR/USD pair’s trading dynamics were influenced by cautious market sentiment amidst European political uncertainties and the ECB’s recent rate cut, juxtaposed with US economic data and the Fed’s cautious approach to monetary policy adjustments.

USDJPY – Bank of Japan Maintains Interest Rate and Bond-Buying Programme

The Bank of Japan hold the rates at 0.10% and no changes in the Bonds buying program of JPY 6 Trillion. So JPY pushed down after the no changes made in this meeting. BoJ Board members told outlook of July 2024 report will decided the trim of Bond Buying program schedule. Inflation is moderately higher, private consumption is higher, Automakers struggle in the shipments, So industrial production much more affected.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

After concluding its two-day monetary policy review meeting on Friday, the Bank of Japan (BoJ) board members decided to maintain the key interest rate at 0%.

This decision aligned with market expectations.

The BoJ maintained rates for the second consecutive meeting in June, following a hike in March—the first since 2007.

However, the BoJ did not alter its extensive monthly Japanese government bonds (JGB) buying programme, which amounts to JPY6 trillion ($38.14 billion).

Summary of the BoJ Policy Statement:

– The BoJ will conduct JGB purchases in accordance with the decision made at the March policy meeting.

– The decision on JGB purchases was made by an 8-1 vote.

– The BoJ decided to reduce bond buying to allow long-term interest rates to fluctuate more freely.

– A specific bond buying reduction plan for the next 1-2 years will be decided at the next policy meeting.

– The BoJ will hold a meeting with bond market participants to discuss today’s policy decision.

– BoJ board member Nakamura dissented on the decision regarding JGB purchases.

– Nakamura believed the bank should decide to reduce JGB purchases after reassessing developments in economic activity and prices in the July 2024 outlook report.

– Despite his dissent, Nakamura supported the idea of reducing the BoJ’s purchase amount of JGBs.

– Uncertainties surrounding domestic economic and financial developments remain high.

– Japan’s economy has shown moderate recovery, despite some areas of weakness.

– Inflation expectations have risen moderately.

– Financial conditions have been accommodative.

– Private consumption has remained resilient.

– Although private consumption has been strong, the impact of price rises persists, and auto sales continue to be affected.

– It is necessary to closely monitor developments in financial and forex markets.

– Underlying CPI inflation is expected to rise gradually.

– Industrial output has been relatively flat overall.

– Industrial output has recently been suppressed by the suspension of production and shipment at some automakers.

USDCHF – Maintains Strong Position Around 0.8950 Amid Fed’s Hawkish Stance

The Swiss PPI data for the month of May came at -0.30% versus 0.60% printed in the last month and 0.50% is expected. PPI Decreased data is favor for SNB to hold the rates at the current levels is possible on the June 20th meeting.

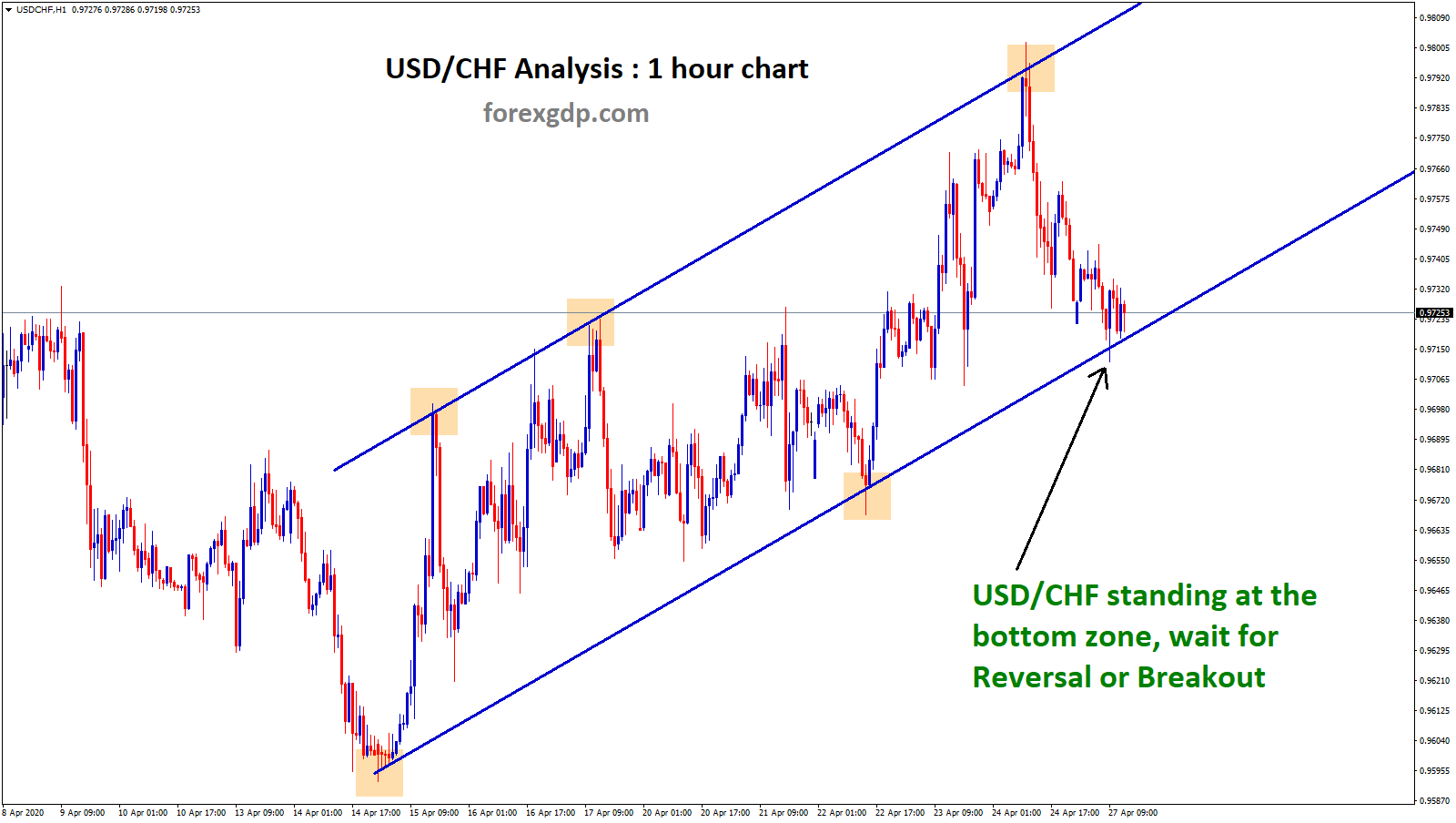

USDCHF is moving in the Descending channel and the market has rebounded from the lower low area of the channel

This recovery was driven by a stronger US Dollar, supported by a Federal Reserve projection suggesting only one potential rate cut in 2024, which boosted investor sentiment.

Market focus turned to upcoming events such as the preliminary US Michigan Consumer Sentiment report and a speech by Fed Bank of Chicago President Austan Goolsbee later in the day, expected to provide new market direction.

Thursday’s US economic data showed the Producer Price Index (PPI) rose 2.2% year-on-year (YoY) in May, slightly below expectations and April’s revised figure of 2.3%. The core PPI also moderated to 2.3% YoY, lower than both the prior reading and market forecast of 2.4%. Despite these softer economic indicators, the Federal Reserve’s hawkish stance, outlined in its dot plot, underpinned the USD by signaling a single 25 basis points rate cut by late 2024.

In contrast, Switzerland reported a decline in Producer and Import Prices by 0.3% month-on-month (MoM) in May, following a 0.6% increase in April, missing expectations of a 0.5% rise. The Swiss National Bank (SNB) is expected to maintain interest rates unchanged in June, potentially strengthening the Swiss Franc (CHF). Moreover, ongoing geopolitical tensions in the Middle East could bolster safe-haven demand, further supporting the CHF in the near term.

USDCAD – BoC’s Kozicki: BoC Plans to End Quantitative Tightening in 2025

The Bank of Canada Deputy Governor Sharon Kozicki said Quantitative easing measures are taken from Tightening measures, rate cuts are possible if the inflation data cooled in the coming months. We have the Vigilant measures on the monetary policy settings in the upcoming days.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Bank of Canada (BoC) Deputy Governor Sharon Kozicki emphasized on Thursday that the central bank is on course to conclude its quantitative easing (QE) program, transitioning towards a phase of quantitative tightening. Kozicki highlighted that the process of unwinding QE has proceeded smoothly thus far. She indicated a cautious approach going forward, suggesting that any future applications of QE would need to meet rigorous criteria before being considered as a tool in the central bank’s monetary policy arsenal.

Key Points:

- Quantitative Tightening Progress: The BoC’s move from QE to quantitative tightening has been managed without disruption.

- Potential for Rate Cuts: Kozicki indicated that if inflation continues to moderate, there could be room for further reductions in interest rates. However, decisions on interest rates are being approached on a meeting-by-meeting basis, indicating a data-dependent stance.

- High Bar for QE: Kozicki stressed that the threshold for reintroducing QE measures is set very high. This suggests that significant economic or financial developments would be necessary to warrant a return to QE.

- Timeline for QE Conclusion: The BoC anticipates completing its quantitative tightening phase by sometime in 2025, marking a milestone in its post-pandemic monetary policy normalization efforts.

Overall, Kozicki’s comments underscore the BoC’s cautious optimism regarding economic recovery and inflation dynamics. The central bank remains vigilant in its approach to managing monetary policy tools, balancing between supporting economic growth and ensuring price stability amidst evolving global economic conditions.

USD INDEX – US Dollar Holds Ground Following Fresh PPI Readings and Jobless Claims

The US Dollar moved downside after the US PPI data came at lower than expected in the May month. US PPI Data came at 2.2% in the May month and Core PPI data came at 2.3% in the May month. Continuous CPI and PPI data fell down in the US economy shows FED soon do rate cuts in the September month onwards.

USD INDEX is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Federal Open Market Committee (FOMC) affirmed its economic outlook with unchanged activity revisions but upgraded forecasts for Personal Consumption Expenditures (PCE), reflecting a US economy showing mixed signals. These include indications of easing inflationary pressures juxtaposed against a robust labor market, factors that influenced the Fed’s decision to revise down its anticipated rate cuts for 2024.

The DXY’s movement was particularly responsive to Wednesday’s dot plot update, revealing that the median expectation among Fed officials now points to just one rate cut in 2024, a reduction from earlier projections of three cuts as of March. This adjustment recalibrated market expectations, which had previously factored in one to two rate cuts, thereby extending the timeline for potential monetary policy easing.

Regarding economic indicators, the Producer Price Index (PPI) for final demand in May rose by 2.2% year-on-year, falling short of the market’s forecast of 2.5%. Similarly, the core PPI, excluding volatile components, increased by 2.3%, also below expectations. Concurrently, the weekly Initial Jobless Claims data for the week ending June 8 showed an uptick to 242,000, exceeding initial estimates of 225,000 and the previous week’s figure of 229,000.

These developments underscore a nuanced economic landscape where inflation pressures are moderating while labor market conditions remain resilient. The DXY’s ascent above 105.00 reflects investor reactions to these factors, positioning the US Dollar favorably amidst evolving expectations of Fed policy and economic performance.

GBPUSD – Pound Sterling Falls Further Against US Dollar on Fed’s Hawkish Outlook

The BoE is like to keep the rates at the next week meeting is more possible due to Wage inflation is stood higher in the market. Unemployment rate is higher but wages of labour is not decreased in the UK. So BoE is expected to kept the rates at current level from economists view.

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

This upward momentum in the USD was driven by the Federal Reserve’s (Fed) hawkish stance on interest rates, which overshadowed softer-than-expected US Consumer Price Index (CPI) and Producer Price Index (PPI) reports for May.

According to Thursday’s US PPI release, the headline PPI declined by 0.2% month-on-month, largely due to lower gasoline prices, while the core PPI, which excludes volatile food and energy prices, remained flat. These cooler inflation readings suggest that the core Personal Consumption Expenditure Price Index (PCE), favored by the Fed, may also show easing inflationary pressures. Consequently, market expectations for early rate cuts by the Fed have risen, with the CME FedWatch Tool indicating a 65% probability of a rate cut decision in September, up from 50.5% a week ago.

During Wednesday’s Fed meeting, policymakers revised their outlook to project only one rate cut this year, down from three previously anticipated, reflecting concerns about slower progress in inflation reduction. Fed Chair Jerome Powell, in the post-meeting press conference, noted the encouraging softness in May’s inflation report but emphasized the need for sustained declines in price pressures over several months to support rate cut decisions. Powell also assured that the Fed stands ready to act swiftly if labor market conditions deteriorate.

Looking ahead, the Pound’s near-term outlook remains uncertain as investors shift focus to the Bank of England’s (BoE) upcoming monetary policy meeting. Expectations are for the BoE to maintain its interest rate at 5.25%, with attention centered on the number of policymakers favoring a rate cut. While May saw Deputy Governor Dave Ramsden and policymaker Swati Dhingra vote for a rate reduction, BoE Governor Andrew Bailey has emphasized that the current inflation progress, while positive, does not yet warrant a rate cut.

Ahead of the BoE decision, market participants will scrutinize the upcoming UK CPI report for May, scheduled for release on Wednesday, to gauge inflation trends. Despite headline inflation nearing the BoE’s 2% target, concerns persist over service sector inflation driven by wage growth, complicating the central bank’s policy outlook. Recent UK employment data indicated steady growth in Average Earnings, reflecting wage inflation above levels conducive to achieving the BoE’s inflation goals.

AUDUSD – Australian Dollar Falls as US Dollar Extends Gains on Hawkish Fed

The Australian Dollar moved down against USD after the US PPI data came at lower than expected in the May month. Employment change for the May month is increased to 39.7K from 30.5K increase is expected in the Australia. RBA ready to do rate hikes if inflation not come to 2% target.

AUDUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

The Australian Dollar (AUD) faced downward pressure against the US Dollar (USD) on Friday, influenced by the USD’s strength driven by higher US Treasury yields. The AUD/USD pair attempted to recover earlier losses following a Reuters poll indicating that the Reserve Bank of Australia (RBA) is likely to maintain its current interest rates in June. The poll, encompassing 43 economists, indicated a strong consensus (90%) for stable interest rates over the next quarter, with a potential decrease of 25 basis points to 4.10% projected by the end of 2024. Moreover, a majority (63%) of economists foresee interest rates falling to 4.10% or below by the year’s end, contrasting with a minority (35%) expecting no change.

The US Dollar (USD) remained resilient despite softer-than-expected US economic data, including a mild increase in the Producer Price Index (PPI) and higher Initial Jobless Claims. The Federal Open Market Committee (FOMC) revised its outlook, now anticipating only one rate cut in 2024, down from three projected in March, which bolstered the USD’s strength and weighed on the AUD/USD pair.

Market participants awaited the release of the preliminary US Michigan Consumer Sentiment index for further insights into consumer confidence and the broader economic outlook.

In Australia, recent economic data showed positive signs with Employment Change surpassing expectations in May, registering a rise of 39.7K employed individuals compared to the anticipated 30.0K increase. The Unemployment Rate also improved to 4.0%, down from April’s 4.1%.

Looking forward, the RBA’s decision-making will likely hinge on inflation trends, as hinted by RBA Governor Michele Bullock’s remarks indicating readiness to adjust rates if the Consumer Price Index (CPI) does not return to its target range of 1%-3%.

Overall, the AUD faces headwinds from a strong USD supported by FOMC policy expectations, while domestic economic data and RBA’s cautious stance on inflation continue to influence its trajectory.

NZDUSD – Extends Decline to Around 0.6150 on Firmer US Dollar and Disappointing New Zealand PMI Data

The NZ Manufacturing index data for the May month came at 47.2 it is the 15th consecutive fall in the market against 48.9 printed in the April month. RBNZ will do rate cuts in the February 2025 if the readings are easing to Goal of target.

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The NZD/USD pair continued its decline to around 0.6155 during Friday’s Asian session, largely influenced by a stronger US Dollar (USD) and disappointing New Zealand PMI data. The USD gained strength after the Federal Reserve signaled a single 25 basis points rate cut by the year-end, a stance reinforced by Fed Chair Jerome Powell’s remarks emphasizing the need for favorable inflation indicators before any monetary easing, as reported by the BBC.

In contrast, US economic data released Thursday showed softer-than-expected figures, with the Producer Price Index (PPI) rising 2.2% year-over-year in May, below April’s 2.3% and forecasts of 2.5%. The core PPI also missed expectations, increasing by 2.3% year-over-year versus the anticipated 2.4%. Moreover, initial jobless claims surged to 242,000 for the week ending June 6, surpassing both market expectations of 225,000 and the previous week’s 229,000, marking the highest level in ten months.

On the New Zealand front, the Performance of Manufacturing Index (PMI) extended its contraction for the 15th consecutive month, dropping to 47.2 in May from April’s 48.9, as reported by Business NZ. This prolonged contraction underscores ongoing weakness in the New Zealand manufacturing sector, exerting downward pressure on the New Zealand Dollar (NZD). Analysts at ANZ anticipate that the persistently weak economic data may prompt the Reserve Bank of New Zealand (RBNZ) to initiate rate cuts sooner than previously anticipated, with expectations now leaning towards rate reductions starting in February 2025.

Looking ahead, market participants await the preliminary US Michigan Consumer Sentiment report and remarks from Fed Bank of Chicago President Austan Goolsbee later on Friday, which could provide further direction to the USD and the NZD/USD pair amidst ongoing economic uncertainties and central bank policy outlooks.

CRUDE OIL – WTI Holds Above $77.50 on Optimistic Demand Forecasts

The Rise in the Oil prices by the EIA projected 1.10Million Barrels per day demand in the 2024 from 0.90Million Barrels per day previous projections. Russia said May month production is higher than OPEC+ commitment, coming months we tightening the Oil production as per agreement levels.

XTIUSD Crude oil price is moving in the Descending channel and the market has reached the lower high area of the channel

This upward movement in oil prices is primarily attributed to optimistic projections regarding global crude demand for the remainder of the year.

Earlier in the week, Reuters reported that the Energy Information Administration (EIA) revised its 2024 forecast for global oil demand growth upward to 1.10 million barrels per day (bpd), up from the previous estimate of 900,000 bpd. Additionally, the Organization of the Petroleum Exporting Countries (OPEC) maintained its 2024 outlook, foreseeing robust growth in global oil demand, driven by anticipated increases in travel and tourism activities in the latter half of the year.

However, Russia’s energy ministry disclosed on Thursday that its oil production in May exceeded the agreed quotas set by the OPEC+ alliance. The ministry acknowledged this excess production and pledged corrective actions in June to align with the agreed production targets, according to Reuters.

Meanwhile, during its June meeting on Wednesday, the Federal Open Market Committee (FOMC) opted to keep its key lending rate unchanged in the range of 5.25% to 5.50%. This decision was widely anticipated. Higher interest rates can potentially constrain economic growth, subsequently impacting oil demand negatively.

Concurrently, yields on US Treasury bonds for 2-year and 10-year terms stood at 4.71% and 4.26%, respectively, at the time of reporting. A stronger US Dollar tends to make oil more expensive for buyers holding other currencies, potentially dampening global oil demand.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!