XAUUSD – Gold Rises Despite Strong US Dollar and Weak Data

The Gold prices are moving higher after the US Michigan Consumer sentiment for the month of May came at 67.4 from 77.2 printed in the last month and 76 is expected rate. This is the six month lower reading in the consumer sentiment. Next week, inflation rate for the April month is expected to 3.5% from 3.2% in the Current state. Over a 10 year period, Inflation is expected to 3.1% from 3.0% in the current projection.

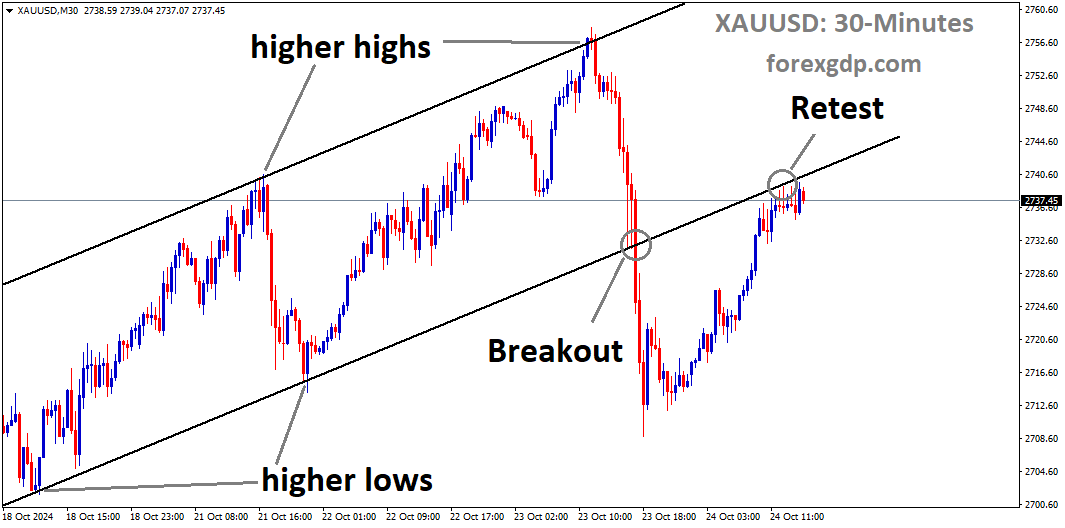

XAUUSD is moving in Descending channel and market has fallen from the lower high area of the channel

Gold prices experienced a notable surge during the latter part of the North American trading session on Friday, climbing by over 1% despite the persistence of high US Treasury bond yields. This upward movement in gold occurred in the wake of a University of Michigan (UoM) survey revealing a significant downturn in consumer sentiment, marking its lowest level in six months.

The XAU/USD pair reached $2,369 after rebounding from daily lows of $2,343. The release of Friday’s sentiment data, coupled with recent weaker labor market indicators since the beginning of May, painted a somber picture for the US economy. Although concerns about a substantial economic slowdown remained subdued, investors seeking refuge drove both the precious metal and the US Dollar higher.

Federal Reserve officials continued to make statements throughout the day. Atlanta Fed President Raphael Bostic maintained a hawkish stance, suggesting that the Fed is likely to enact only one rate cut in 2024. Later, Fed Governor Michelle Bowman emphasized the importance of maintaining policy stability and expressed no inclination towards rate cuts for the remainder of the year. Lorie Logan from the Dallas Fed dismissed the notion of interest rate reductions.

Minneapolis Fed President Neel Kashkari recently stated his preference for adopting a “wait and see” approach regarding future monetary policy decisions.

Looking ahead, next week’s US economic calendar will feature the release of crucial inflation figures, retail sales data, building permits statistics, and additional speeches from Fed officials.

In a daily market roundup, gold prices were observed to decline amidst lower US Treasury yields and a strengthening US Dollar. The yield on the US 10-year Treasury note reached 4.504%, marking an increase of nearly five basis points (bps) from its opening level. The US Dollar Index (DXY), tracking the performance of the Greenback against a basket of six major currencies, rose by 0.12% to 105.32.

The University of Michigan Consumer Sentiment Index experienced a significant decline in May, dropping from 77.2 in April to 67.4, failing to meet analysts’ expectations of 76. Joanne Hsu, Director of the UoM Survey, highlighted the statistical significance of the 10-point drop, marking the lowest consumer sentiment level recorded in approximately six months.

Furthermore, there was an escalation in inflation expectations, with the one-year outlook rising from 3.2% to 3.5% in May. Expectations for a 10-year period also saw a slight increase from 3.0% to 3.1%.

Soft labor market indicators, as evidenced by last month’s US employment report and unemployment claims data, may exert pressure on the Fed. Officials acknowledged that the risks associated with achieving the Fed’s dual mandate of maximum employment and price stability have become more balanced over the past year.

Following the data release, the probability of Fed rate cuts towards the end of 2024 increased from around 33 basis points (bps) to 34 bps.

EURUSD – Falls on Dollar Rebound Post-Fed Rate-Cut Speculation

The ECB Policy Maker and Greece Governor Yannis Stournaras said three more rate cuts in this year and first rate cut is expected from July month is possible. In Contrary, ECB Governing Council member and Austrian Governor Robert Holzmann said there is no reason for rate cuts in this year and inflation has to come down to our target have long time. So no worry for Rate cuts at this time in his view. The Euro zone GDP expanded 0.30% in January- March Quarter from 0.10% is expected.

EURUSD is moving in Descending channel and market has reached lower high area of the channel

EUR/USD encounters downward pressure near the 1.0800 level during Friday’s American session, struggling to maintain its strength amidst expectations of potential interest rate cuts by the European Central Bank (ECB).

Investors are anticipating that the ECB might initiate a downward adjustment in borrowing rates starting from June. However, there is a division among ECB policymakers regarding the extension of the rate-cutting cycle beyond the June meeting. Some policymakers argue for additional interest rate cuts post-July, aiming to stimulate price pressures in the economy.

Yannis Stournaras, an ECB policymaker and the Governor of the Bank of Greece, indicated in a recent interview that he foresees three rate cuts within this year. He suggested the possibility of a rate cut in July, particularly noting the economic rebound observed in the first quarter, which makes a scenario of three cuts more likely than four. The Eurozone economy demonstrated growth of 0.3% in the January-March period, surpassing expectations of a 0.1% expansion.

In contrast, Robert Holzmann, a member of the ECB Governing Council and the Governor of the Austrian central bank, expressed reservations about implementing rate cuts too swiftly or aggressively. He emphasized a cautious approach in this regard.

This week, the movement of EUR/USD has been influenced by market sentiment, with limited impact from significant economic data releases from both the Eurozone and the United States. However, investors will closely monitor the US Consumer Price Index (CPI) data for April scheduled for release next Wednesday.

In a daily market summary:

– EUR/USD encounters notable selling pressure near the key resistance level of 1.0800 as the US Dollar stages a recovery.

– Speculation mounts regarding the Federal Reserve (Fed) potentially initiating interest rate cuts in September, driven by signs of cooling in the US labor market.

– Recent data from the US Department of Labor indicates a significant rise in Initial Jobless Claims, surpassing expectations and highlighting concerns about labor market weakness.

– Sluggish Nonfarm Payrolls (NFP) for April and a slowdown in job openings in March further fuel doubts about the resilience of the US job market.

– The uncertain labor market conditions have bolstered expectations for Fed interest rate cuts in September, with traders pricing in a 71% chance of rate reduction, up from 66% recorded earlier.

– Minneapolis Fed Bank President Neel Kashkari suggested that the weakening job market could justify a rate cut, although he remains inclined towards maintaining the current interest rate framework throughout the year. Concerns persist about the stagnation of inflation below the Fed’s target of 2% amidst a robust housing market.

USDJPY – Rises After Weak US Consumer Report

The USDJPY pair moved flat after the US Michigan consumer sentiment data came at lower than expected and six month lower reading. Coming week US inflation rate for the month of April is expected to 3.5% from 3.2% printed in the March month, 10 Year inflation forecast to 3.1% from 3.0%.The BoJ Members said FX intervention is necessary when the prices are going beyond our expectations, no rate hikes from BoJ is worry for JPY weakness.

USDJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

During the North American trading session, the USD/JPY pair made significant gains, spurred by disappointing results from the University of Michigan (UoM) Consumer Sentiment survey, which indicated a growing pessimism among American consumers about the state of the economy. Despite these concerns, the pair was seen trading at 155.83, marking a 0.24% increase.

Key developments surrounding USD/JPY after UoM Consumer Sentiment survey, with focus on upcoming US inflation data:

The UoM Consumer Sentiment Index experienced a notable decline in May, dropping from 77.2 in April to 67.4, missing analysts’ expectations of 76. Joanne Hsu, Director of the UoM Survey, highlighted the significance of this 10-point decrease, stating that it represents the lowest sentiment reading recorded in approximately six months. The survey revealed rising worries among Americans regarding inflation, unemployment, and interest rates.

Inflation expectations for the short-term (one year) surged from 3.2% to 3.5% in May, while expectations for the longer term (ten years) saw a slight increase from 3.0% to 3.1%.

Following the release of this data, the yield on the US 10-year Treasury note climbed by four basis points (bps) to reach 4.498%. Concurrently, the US Dollar Index (DXY) strengthened by 0.14%, reaching 105.35. Concerns about a potential economic downturn were reignited as the UoM survey suggested a possible weakening of consumer spending in the near future.

In addition to the data release, statements from two Federal Reserve officials garnered attention. Fed Governor Michelle Bowman emphasized the importance of proceeding with caution and prudence in monetary policy decisions. Meanwhile, Lorie Logan, from the Dallas Fed, expressed the view that it is premature to consider implementing rate cuts at this stage.

Looking ahead, the US economic calendar for the upcoming week includes key releases such as inflation figures, retail sales data, building permits statistics, and speeches from Federal Reserve officials. These events are expected to provide further insights into the state of the US economy and may influence the trajectory of the USD/JPY pair.

USDCAD – Canadian Dollar Rises on Surprising Job Additions

The Canadian Employment Job Numbers added 90.4 K in the April Month versus 18K expected and -2.2K declined in the March month, Unemployment rate rises to 6.1% in the April versus 6.2% in the previous month. Wage Growth decreased to 4.8% in the April month versus 5.0% printed in the March month. The data shows strong Job Growth and Slower Wage growth but Bank of Canada may delay the rate cuts from June to September is possible. So Canadian Dollar rallied against counter pairs after the upbeat readings of Job data.

USDCAD is moving in Descending Triangle and market has rebounded from the support area of the pattern

The Canadian Dollar (CAD) experienced a notable surge on Friday, buoyed by robust job additions in the Canadian economy, surpassing analysts’ expectations by a significant margin. However, the CAD’s upward momentum was tempered by prevailing risk-off sentiment in the market, with investors showing a preference for the US Dollar amidst concerns regarding hawkish rhetoric from the Federal Reserve and disappointing US consumer sentiment data.

In April, Canada witnessed its most substantial net job gains since February 2023, with nearly 100,000 jobs added to the economy, significantly exceeding forecasts. Despite this positive development, the unemployment rate in Canada remained unchanged at 6.1%. Meanwhile, both consumers and policymakers in the United States expressed concerns about prolonged and elevated inflation levels, which diverged from the expectations of market participants anticipating rate cuts. This cautious sentiment contributed to subdued risk appetite in the market, limiting the CAD’s gains.

In a daily market summary:

– Canada recorded a net addition of 90.4 thousand jobs in April, surpassing the forecast of 18 thousand and reversing the previous month’s decline of 2.2 thousand.

– The Canadian Unemployment Rate remained stable at 6.1%, outperforming market expectations of a slight increase to 6.2%.

– The University of Michigan’s US Consumer Sentiment Index for May declined to 67.4, marking its lowest level in six months.

– Consumer inflation expectations for the next five years, as per the UoM survey, rose to 3.1%, indicating anticipation of continued price growth among US consumers.

– The dampened consumer sentiment and persistent inflation expectations undermined market hopes for potential rate cuts, leading investors to seek refuge in the safe-haven US Dollar.

– Comments from Federal Reserve officials, downplaying the likelihood of rate cuts in 2024, failed to provide significant support to market sentiment.

USDCHF – Stagnates Around 0.9050 Amid Fed’s Dovish Tone

The Swiss Government 10 year Bond yield lower to 0.70% threshold level and it is negative for Foreign investors to invest in Switzerland Bonds due to lower Yields. Swiss Bank Reserves shows CHF 720 Billion in the April month from CHF 716 Billion in the March Month. The reading is higher since November month have CHF 642 Billion, it is the 6th month higher reading in the foreign reserves in the SNB. The SNB Focus is less on Bolstering Swiss Franc and Full focus shifted to lowering the inflation rate. The Unemployment rate came at 2.3% in the April month from 2.4% in the March month. This is the 4 month lowest reading the Swiss zone.

USDCHF is moving in Ascending channel and market has reached higher low area of the channel

During the European trading session on Friday, the USD/CHF pair lingered around the 0.9060 mark amidst prevailing negative sentiment, primarily influenced by the recent weak US labor market data released on Thursday. This data release has sparked discussions about a potential shift in the Federal Reserve’s (Fed) monetary policy stance towards a less hawkish outlook, consequently dampening US Treasury yields and exerting pressure on the US Dollar (USD).

According to the latest data from the US Bureau of Labor Statistics (BLS), the number of individuals filing for unemployment benefits surpassed expectations, with Initial Jobless Claims for the week ending May 3 rising to 231,000. This figure exceeded market estimates of 210,000 and represented an increase from the previous week’s reading of 209,000.

Amidst this backdrop, the US Dollar Index (DXY), which measures the performance of the USD against a basket of six major currencies, hovered around the 105.20 level. Concurrently, the 2-year and 10-year US Treasury yields stood at 4.81% and 4.44%, respectively, at the time of the report.

Meanwhile, in Switzerland, banks remained closed on Friday due to the observance of the Ascension Day holiday. The yield on the 10-year Swiss government bond dipped below the 0.7% threshold, nearing a new monthly low. This decline in bond yields mirrored a global trend and rendered Swiss assets less appealing to foreign investors, resulting in decreased demand for the Swiss Franc (CHF).

Earlier in the week, data from the Swiss National Bank (SNB) revealed that foreign exchange reserves increased to CHF 720 billion in April from CHF 716 billion in the previous month. This marked the fifth consecutive monthly rise since reaching a near seven-year low of CHF 642 billion in November. The SNB’s focus has shifted away from intentionally strengthening the Swiss Franc, as the central bank has intensified its efforts to combat inflation.

Additionally, data released by the State Secretariat for Economic Affairs indicated a decline in the seasonally adjusted Swiss Unemployment Rate to 2.3% month-on-month in April from 2.4% in March, marking the lowest level in four months.

USD INDEX – Barkin: Inflation to Reach 2% with Time and Policy

The RichMond Fed President Thomas Barkin said FED has to wait for patience inorder to inflation will come to target of 2%. Demand is Solid and not in excess demand situation now. The Inflation underway progress and gradually decline to 2% in the Year end. Until No push for rate hikes or Cuts approach from FED side is expected from Investors side.

USD Index Market price is moving in Ascending channel and market has reached higher low area of the channel

Federal Reserve (Fed) Bank of Richmond President, Thomas Barkin, made headlines on Friday as he reiterated the Fed’s commitment to a cautious and deliberate approach aimed at gradually reducing inflation to the central bank’s desired target level.

In his statement, Barkin emphasized several key points:

- Patient Approach : Barkin underscored the need for a patient and deliberate strategy in the current economic environment.

- Inflation Target : He expressed confidence that, given the right policy measures and sufficient time, inflation would eventually reach the Fed’s target of 2%.

- Solid Demand : Barkin noted that while demand remains robust, the economy is not experiencing overheating.

- Sustainability of Inflation Progress : He expressed optimism regarding the sustainability and broadening of progress in inflation.

Barkin’s remarks reflect the Fed’s ongoing assessment of economic conditions and its commitment to using appropriate policies to achieve its inflation objectives while ensuring the overall stability of the economy.

GBPUSD – Pill of BoE Emphasizes Persistent Inflation Components

The BoE Chief economist Huw Pill said Rates are kept at 5.25% this time is sufficient for the economy, we have to lookout persistent components of Inflation not the headline rate. Whenever the components of inflation will be down then automatically inflation come to our target of 2%. BoE Forecasts inflation rate did not mean to rate hike or rate cuts in the monetary policy settings. Never Too early rate cuts or too delay rate hikes will support the inflation to come lower, we have to control the main components of inflation triggering tool, then only we achieve the sustained inflation target of 2%.

GBPUSD is moving in Descending channel and market has reached lower high area of the channel

Huw Pill, the Chief Economist of the Bank of England (BoE), made notable statements on Friday. He echoed the sentiment of the majority of the BoE’s Monetary Policy Committee (MPC), which decided on Thursday to maintain interest rates at 5.25%. However, Pill indicated a growing conviction that the conditions for rate cuts would soon materialize.

Here are the key points from his remarks:

- Emphasis on Persistent Inflation Components : Pill stressed the importance of focusing on the persistent components of inflation rather than solely on the headline rate.

- Signal for Potential Rate Cuts : The MPC has communicated a relatively clear indication that the bank rate could be lowered once there is sufficient evidence of a downward trajectory in the persistent components of inflation.

- Caution Against Narrow Focus : Pill cautioned against solely concentrating on the upcoming BoE meeting, suggesting that such a narrow focus might be unwise.

- Medium-Term Inflation Forecasts : He highlighted that the BoE’s medium-term inflation forecasts do not necessarily provide a signal regarding rate adjustments at the next meeting or the subsequent ones.

Pill’s statements reflect a nuanced perspective on the factors influencing the BoE’s monetary policy decisions, emphasizing the importance of considering various inflation indicators and adopting a broader outlook beyond immediate meetings.

AUDUSD – AUD Steadies Near Psychological Level, Focus on US Consumer Sentiment

The Australian Dollar moved higher after the US Domestic data experiencing lower gains against the expected readings. The Q1 inflation rate is 3.6% from 4.1% in the previous quarter and 3.4% is expected, it is the 5th consecutive fall in the inflation reading. Monthly basis fall to 3.5% from 3.4% is expected.The RBA Governor Michelle Bullock said inflation will return to 2-3% target range in second half of 2025 and start of 2026 year, until the rates has to sustain in this level.

AUDUSD is moving in box pattern and market has reached resistance area of the pattern

On Friday, the Australian Dollar (AUD) experienced a retracement from its recent gains, following a surge on Thursday primarily driven by a weakening US Dollar (USD) due to disappointing US Initial Jobless Claims data. The market interpreted this data as signaling a more dovish stance from the Federal Reserve (Fed), which helped alleviate some pressure on the Aussie Dollar despite the Reserve Bank of Australia (RBA)’s less hawkish tone, particularly in light of higher-than-expected inflation figures.

Australia’s inflation rate moderated to 3.6% in the first quarter from 4.1% in the previous quarter, marking the fifth consecutive quarter of deceleration. However, it surpassed market expectations of 3.4%. Additionally, the Monthly Consumer Price Index (YoY) for March surged to 3.5%, exceeding the projected reading of 3.4%. The RBA acknowledged that recent progress in curbing inflation has halted and maintained a stance of flexibility regarding monetary policy.

Meanwhile, the US Dollar Index (DXY), measuring the USD against a basket of major currencies, attempted to rebound amid sentiment that the Fed might maintain higher interest rates for an extended period. However, declining US Treasury yields could counteract this, applying downward pressure on the Greenback and supporting the AUD/USD pair.

In the United States, the preliminary Michigan Consumer Sentiment Index for May is scheduled for release on Friday, with expectations of a slight decline. This index measures consumer sentiment across personal finances, business conditions, and buying conditions, potentially influencing market sentiment. Additionally, Chinese Consumer Price Index (CPI) data is anticipated on Saturday, with potential implications for the AUD due to Australia’s significant trade relationship with China.

In other news:

– The Commonwealth Bank of Australia (CBA) revised down its AUD forecasts for the end of 2024, citing factors such as the interest rate gap and elevated US Treasury bond yields, which bolster the USD.

– The ASX 200 Index rose on Friday, recovering recent losses, buoyed by a strong performance on Wall Street.

– The US Bureau of Labor Statistics (BLS) reported an increase in Initial Jobless Claims for the week ending May 3, surpassing expectations.

– RBA Governor Michele Bullock emphasized the importance of monitoring inflation risks and stated that current interest rates are positioned to guide inflation back towards the target range.

– Societe Generale expressed concerns about Australia’s economic growth outlook, anticipating potential downturns.

– Federal Reserve Bank of Boston President Susan Collins emphasized the need for moderation in the US economy to achieve the Fed’s inflation target, while Minneapolis Fed President Neel Kashkari hinted at a prolonged period of steady rates.

NZDUSD – China’s Consumer Prices Up 3rd Consecutive Month, Indicating Demand Recovery

The China CPI index came at 0.30% in the April month from 0.10% printed in the March month and 0.20% is expected rise. Core CPI data came at 0.70% in the April month from 0.60% printed in the March month. The Overall CPI Index is 0.10% rise against 0.10% fall is expected and 0.10% drop in the March month. The Consumer demand is playing higher due to Imports rise in the April month and Producer prices are falling in the other side. Healthy CPI makes NZ Dollar will move higher in the upcoming weeks due to imports are higher in the China it will benefit for NZ and Aussie economies to build their export revenues.

NZDUSD is moving in Descending channel and market has reached lower high area of the channel

In April, China’s consumer prices continued their upward trend for the third consecutive month, contrasting with a further decline in producer prices. This suggests a strengthening in domestic demand, a welcome sign for Beijing as it grapples with economic challenges.

The latest data, released by the National Bureau of Statistics on Saturday, revealed that consumer prices edged up by 0.3% year-on-year in April, compared to a 0.1% increase in March and exceeding a forecasted rise of 0.2% in a Reuters poll. Xu Tianchen, a senior economist at the Economist Intelligence Unit, noted that excluding food and energy prices, the core inflation data indicated a resurgence in demand, particularly in the services sector. Core inflation grew by 0.7% in April, up from 0.6% in March.

Moreover, the overall consumer price index (CPI) increased by 0.1% from the previous month, surpassing expectations of a 0.1% decline. This reversal from March’s 1% drop underscores the potential revival in consumer spending.

However, challenges persist for Chinese policymakers. Cooling factory and services activities, coupled with a persistent housing crisis, pose threats to sustained economic recovery. Municipal debt, amounting to $13 trillion, weighs heavily on local governments, potentially leading to price hikes by utility companies to offset fiscal strains.

Zhou Maohua, a macroeconomic researcher at China Everbright Bank, acknowledged the positive signs of recovering domestic demand but emphasized the need for balance, as reflected in the continued pressure on the industrial manufacturing sector.

Meanwhile, the producer price index (PPI) dropped by 2.5% year-on-year in April, although it moderated from the previous month’s 2.8% decline. This prolonged period of decline underscores challenges in the industrial sector.

In response, China’s central bank signaled flexibility in monetary policy to promote a moderate recovery in consumer prices and consolidate economic rebound. The Politburo’s commitment to utilizing policy tools underscores the importance of sustained support to achieve the economic growth target of approximately 5% for 2024.

CRUDE OIL – WTI Rises Above $79.20 on China Demand Optimism

The Crudeoil prices are gained on Friday after the China trade surplus data and Oil imports data came at higher than expected in the April month. The Two Biggest economies US and China demand for Oil is the Whole world supplying makes the price increase for Oil prices. The Middle East tensions on the other sides and supply constraint from OPEC+ countries is various forms of problems to Oil supply in the Market.

XTIUSD is moving in Ascending channel and market has reached higher low area of the channel

Western Texas Intermediate (WTI), the benchmark for US crude oil, is currently trading around $79.30 on Friday, experiencing an upward trend fueled by optimism surrounding increasing demand in China and the United States, the world’s largest consumers of crude oil.

China’s official statistics revealed a notable uptick in crude oil imports, rising by 5.45% in April compared to the same period last year, signaling a positive trajectory in demand. Tina Teng, an independent market analyst, attributed this improvement in demand to the encouraging data on China’s Trade Balance, further boosting WTI prices.

Additionally, a decrease in oil inventories in the United States contributed to the positive momentum for crude oil. According to the Energy Information Administration (EIA), crude inventories in the US declined by 1.4 million barrels during the week ending May 3, reversing the previous week’s build-up of 7.3 million barrels. This reduction in stocks aligned with market expectations, further supporting WTI prices.

Geopolitical tensions in the Middle East also played a role in driving up WTI prices. Israeli forces intensified their presence and engagement near built-up areas of Rafah following statements from President Joe Biden regarding potential consequences for Israel’s military actions. These ongoing uncertainties in the region raised concerns about potential disruptions to oil supply, bolstering WTI prices.

However, the appreciation of the US Dollar (USD), supported by the hawkish stance of the US Federal Reserve (Fed), poses a potential limitation to the upside of USD-denominated oil in the near term. San Francisco Fed President Mary Daly emphasized the challenges of projecting policy decisions amidst uncertainty over the inflation outlook until the Fed gains more clarity.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!