GOLD – Slumps to $2,150.00 Amid US Inflation Reacceleration

Gold prices dipped in the market due to strong PPI numbers and CPI data rose in this week. FED said strong industrial production numbers in February month. So FED Mostly do rate hold in this week widely expected than rate cuts. So Gold prices may be go down if upcoming US Domestic data inthis week like Services PMI, Manufacturing PMI numbers came at higher in March month.

XAUUSD is moving in Descending Triangle and market has reached support area of the pattern

Gold Retreats from $2,180 as US Inflation Delay Eases Fed’s Policy Expectations

Gold spot pulled back from the $2,180 region on Friday, marking consecutive negative sessions as hopes for the US Federal Reserve’s easing cycle were postponed. Strong US economic data pushed back expectations for Fed easing, with hotter-than-expected inflation figures supporting Fed Chair Jerome Powell’s stance to maintain patience and stick to current monetary policy.

The XAU/USD is trading at $2,157.66, down 0.20%, reflecting a risk-off sentiment on Wall Street despite gold typically benefiting from such conditions. US Treasury yields rose after Thursday’s Producer Price Index (PPI) data, keeping XAU/USD pressured during the European and late trading sessions.

Despite upbeat US economic data, gold remained under pressure. Industrial Production improved in February, and University of Michigan Consumer Sentiment showed continued optimism about the economic outlook among Americans.

The XAU/USD holds steady as the US 10-year Treasury bond yield increases by one basis point to 4.308%, while the US Dollar Index (DXY) rises 0.09% to 103.45.

In economic news, Industrial Production increased by 0.1% MoM, surpassing January’s -0.5% contraction, while the University of Michigan Consumer Sentiment preliminary reading came in at 76.5, slightly below estimates. The Producer Price Index (PPI) showed strength, with a 1.6% YoY increase, and Retail Sales rose by 0.6%, missing estimates but showing improvement compared to the previous month.

XAUUSD has broken descending channel in upside

Amidst reaccelerating inflation, expectations for Fed easing have diminished. Fed Chairman Jerome Powell, during last week’s testimony, emphasized the Fed’s cautious approach, suggesting policy adjustments would depend on incoming data indicating sustained progress toward the Fed’s inflation target.

According to the CME FedWatch Tool, expectations for a May rate cut have decreased to 11%, while June stands at 64%, highlighting uncertainty surrounding future Fed actions. The Fed’s next meeting is scheduled for March 19-20.

EURUSD – Euro Expected to Depreciate by Year-End – NBF

The National Bank of Canada projected EURUSD pair is moving in the range bound 1.0750-1.1000 in the past 2 months. Based on FED monetary policy and ECB Monetary policy divergence makes Euro weaker against USD this year. Comparing to US, Euro zone is most comfortable with inflation reading, Jobs, Manufacturing areas. So as per our view, Euro will be depreciate towards USD this year due to Policy rate cuts.

EURUSD is moving in Ascending channel and market has reached higher low area of the channel

EUR/USD Shows Limited Movement, but Volatility Expected Ahead – NBF

While EUR/USD has exhibited some movement in the first two months of the year, it remains relatively rangebound between the 1.0750 and 1.1000 levels. Analysts at the National Bank of Canada assess the pair’s outlook, foreseeing potential volatility in the coming quarters, particularly as the policy paths of both the Federal Reserve and the European Central Bank become clearer.

Despite this anticipated volatility, they predict a depreciation of the common currency towards the end of the year.

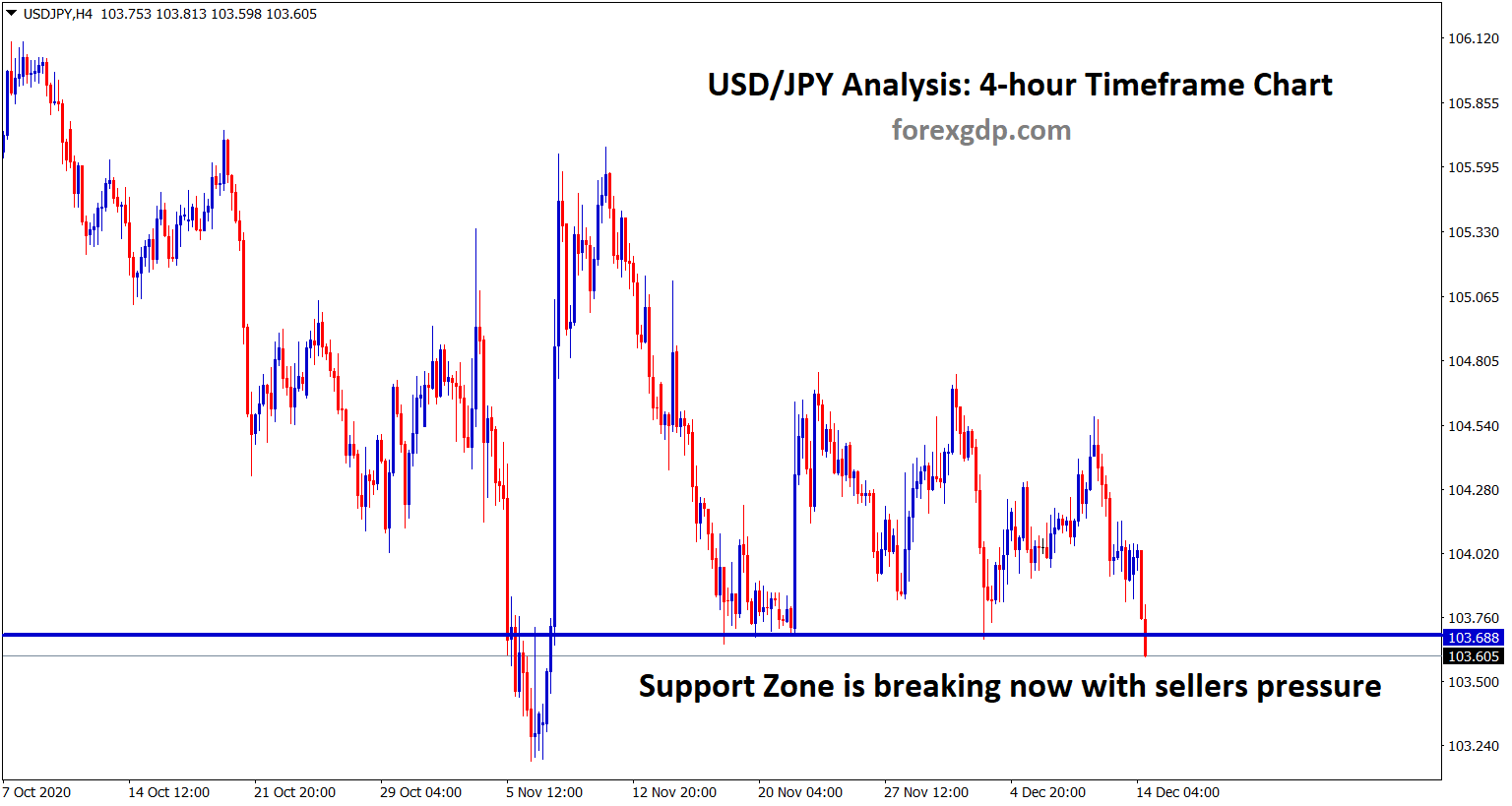

USDJPY – Nordea: JPY Won’t Strengthen as Long as Fed and ECB Keep Rates Steady

The Bank of Japan monetary policy meeting is scheduled this week, rate hikes in upcoming April month announcement is widely expected in this meeting. Wage hikes for Japan workers is 5% approved by Companies and it is largest hike in the last 3 decades. So inflation to 2% target will be achieved in coming days, But BoJ took baby steps of rate hikes in the market. So FED and ECB rate cuts only boost the JPY in the market, not BoJ rate hike will push up the JPY Market, As per Nordea economists told.

USDJPY is moving in Ascending channel and market has reached higher high area of the channel

Nordea Economists: BoJ Hikes Could Aid JPY, but Fed Rate Cuts Needed for Significant Strength

The Japanese Yen (JPY) could see some relief with the Bank of Japan (BoJ) beginning its rate hikes, driven by recent high wage growth. However, economists at Nordea suggest that for a more substantial strengthening of the JPY, significant rate cuts by the Federal Reserve (Fed) are necessary.

As the BoJ initiates its rate hike cycle, signaled by wage growth surpassing 5% for the largest workers union, the JPY may experience slight relief. Wage growth, reaching its highest level in three decades, coupled with inflation exceeding 2%, indicates an end to Japan’s negative interest rate era. Nonetheless, Nordea doesn’t anticipate a vigorous rate hiking cycle from the BoJ.

Nordea predicts that the BoJ will proceed cautiously with rate hikes to maintain inflation dynamics around 2%. Consequently, they argue that substantial JPY strengthening won’t occur unless the Fed and European Central Bank (ECB) adjust rates significantly.

USDCHF – US Dollar Gains Slightly Ahead of Fed Decision

The 5 Year inflation expectations in the US is 2.9%, Industrial production for the month of February came at 0.10% it is improved from -0.50% in January. The Economists expected May month cut is 10% and June month rate cut is 65% . So US Dollar is reversed from lows in this week after the Strong US Data readings are printed. Upcoming week US Data readings based market will be determined.

USDCHF is moving in box pattern and market has rebounded from the support area of the pattern

US Dollar Gains Ground Ahead of Fed Decision

The US Dollar Index (DXY) rises slightly to 103.40 on Friday, rebounding from December lows amidst increasing US Treasury yields following hot inflation data. Strong economic indicators and a cautious Federal Reserve (Fed) stance suggest potential for further USD recovery. Attention turns to the updated Federal Open Market Committee (FOMC) forecast next week, expected to provide additional support for the USD.

Despite ongoing inflation concerns, the timing of the easing cycle, anticipated in June, remains dependent on incoming data. Mixed labor market indicators have tempered inflation worries. The upcoming FOMC Dot Plot could recalibrate market expectations.

In other news, the University of Michigan reports a decline in March Consumer Expectations index to 74.6, while Consumer Sentiment holds at 76.5. Industrial Production for February sees a modest improvement at 0.1%. US Treasury yields climb, with the 2-year yield at 4.71%, the 5-year at 4.13%, and the 10-year at 4.29%.

Expectations for no rate cuts from the Fed next week prevail, with attention focused on the Fed’s ability to ensure a smooth economic transition. Projections for a May rate cut stand at 10%, while the likelihood of a cut in June is around 65%. Market watchers await insight into whether officials maintain a vision of three cuts in 2024.

USDCAD – Strengthens Above 1.3500 Amid Fed Policy Focus

The Interenational Energy Agency raise the oil consumption target of 2024 to 110K BPD this week. So Canada is the largest exporter of oil to US, So Canadian Dollar remain stronger against counter pairs, but lower against USD due to US Strong domestic data presence and FED rate cuts delaying fears.

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

USD/CAD Holds Above 1.3500 Amid Fed Policy Focus

In Friday’s European session, the USD/CAD pair maintains its strength above the key level of 1.3500. The Loonie’s sideways movement follows a recent rebound driven by decreased expectations of a Federal Reserve interest rate cut in the upcoming June policy meeting.

Fed policymakers are closely monitoring inflation trends, aiming for sustained decreases to reach the desired 2% rate. However, recent data, including the US Producer Price Index (PPI) for February, has shown stubborn inflation, particularly due to rising gasoline and food prices.

Investors are now turning their attention to the Fed’s policy decision, expecting interest rates to remain unchanged between 5.25% and 5.50%. The release of the dot plot and economic projections in Wednesday’s announcement will be closely watched for further market insights.

Meanwhile, oil prices have slowed down after a two-day rally, although broader strength persists following the International Energy Agency’s upward revision of its 2024 oil demand forecasts by 110K bpd. This is significant for Canada, a major oil exporter to the US, as higher oil prices typically support the Canadian Dollar.

EURNZD – ECB’s Rehn: Discussion Begins on Easing Monetary Policy Restrictions

ECB Policy maker Olli Rehn said ECB is started to doing reduce the restrictive monetary policy settings, whether we release the pedal from the break due to more inflation easing seen in the market. We are discussing to do rate cuts appropriate to the inflation easing in the coming months.

EURNZD is moving in Descending Triangle and market has rebounded from the support area of the pattern

ECB’s Olli Rehn Discusses Interest Rate Outlook:

Key Points:

– Initiating discussions on easing the restrictive aspect of monetary policy.

– Focus on determining the suitable timing for interest rate cuts.

– Suggests gradual adjustment if inflation trends downwards, signaling a cautious approach to easing monetary policy.

GBPCHF – Swiss Franc Faces Downside Risks Amid Inflation Divergence from SNB Forecasts

The Swiss Franc is going to depreciate in the upcoming days due to inflation is lower in Swiss zone and with in SNB target of 0-2%. Latest inflation data for February month came at 1.2%, Producers and Imports prices declined to -2.0%, it is the tenth consecutive month decline in the import price history. SNB most probably rate cuts will be do in this week meeting is widely expected by economists side.

GBPCHF is moving in Descending channel and market has reached lower high area of the channel

Swiss Franc Flat Amid Concerns of Diverging Inflation from SNB Forecasts

The Swiss Franc (CHF) remained largely unchanged at the close of the trading week, with minimal fluctuations in its major pairs. However, the fundamental outlook for the CHF appears unfavorable as Swiss inflation continues to decline, deviating from official projections. This could prompt the Swiss National Bank (SNB) to consider easing policy, which typically exerts downward pressure on the currency by reducing foreign capital inflows.

Recent macroeconomic data reveals that Swiss Producer and Import Prices continued their deflationary trend in February, marking the tenth consecutive month of deflation at minus 2.0% (compared to negative 2.3% in January), according to the Federal Statistical Office.

Swiss Franc Vulnerable as Inflation Undercuts SNB Forecasts

The Swiss Franc faces further vulnerability as Swiss inflation appears poised to fall short of official forecasts. Headline inflation in Switzerland rose by 1.2% year-on-year in February, down from 1.3% in January, and increased by 0.6% month-on-month, up from 0.2% in January. These figures indicate that inflation is lagging behind the SNB’s projections, which anticipated a rise from the 1.4% registered in November, as stated in the SNB’s December policy statement.

The SNB implemented a rate hike of 0.25% in June 2023 to counter the threat of higher inflation. However, with inflation decreasing faster than expected, there’s a risk of interest rate cuts, which would negatively impact the Swiss Franc by reducing foreign capital inflows. Furthermore, inflation running well below the SNB’s 1.9% forecast for 2024 increases the likelihood of a policy change. The SNB’s next policy meeting is scheduled for March 21.

SNB Concerned About Overvalued Swiss Franc

SNB Chairman Thomas Jordan has voiced concerns about the Swiss Franc’s excessive strength, particularly its adverse effects on Swiss businesses, especially exporters. This concern is evident in data from Switzerland’s Foreign Exchange Reserves (CHFER), indicating a recovery in Forex reserves in 2024, suggesting that the SNB may be selling Swiss Francs to depreciate the exchange rate.

GBPUSD – GBP Hits Weekly Low Amid Gloomy Market Sentiment

The GBP inflation data for the month of February is scheduled this Wednesday before BoE Monetary policy meeting. This reading will give the direction of BoE whether rate cuts or rate hold in the upcoming meetings. January month 0.20% economy growth after the technical recession happened in second half of 2023 is remarkable growth for GBP.

GBPUSD is moving in Descending channel and market has reached lower low area of the channel

GBP Dips on Gloomy Sentiment as USD Strengthens Ahead of Fed Meeting

In Friday’s European session, the Pound Sterling (GBP) faces downward pressure amidst bleak market sentiment, reducing the appeal of risk-sensitive assets. The GBP/USD pair hits a weekly low near 1.2730, with the US Dollar gaining strength on expectations that the Federal Reserve (Fed) will maintain interest rates between 5.25% and 5.50% in the upcoming June policy meeting.

Uncertainty looms over the UK’s economic outlook, potentially prompting Bank of England (BoE) policymakers to reconsider prolonged high-interest rates. Despite a slight uptick in January, the UK economy’s technical recession in the second half of 2023 remains a concern.

Looking ahead, the Pound Sterling’s performance will hinge on UK’s February inflation data, scheduled for release before the BoE’s interest-rate decision. Market expectations for BoE rate cuts, likely in the third quarter according to a Reuters poll, will be influenced by this data. Additionally, public inflation expectations for both the short and long term remain significant factors.

AUDUSD – Dips Further on Weak Chinese Data

The Chinese Housing price index fell down to -1.4% in February month versus -0.70% in January month. China using Iron Ore usage fell down to 25% for producing Steel for construction of Buildings. US Factory gate inflation rate is soared to 1.6% from 1.1% expected and 1.0% previous reading, this news also downturn the Australian Dollar against USD.

AUDUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

AUD/USD Slips on Weak Chinese Data

AUD/USD is down nearly 0.2% on Friday, extending Thursday’s decline as negative Chinese housing and lending data weigh on market sentiment. The downturn in Chinese house prices, coupled with a decrease in new loans and lower-than-expected money supply, reflects ongoing challenges in the country’s property sector.

This slump in Chinese data has a direct impact on Australia’s export-driven economy, particularly on commodities like Iron Ore, which has seen a significant drop in prices since the beginning of 2024.

Moreover, AUD/USD faced additional pressure on Thursday following robust US macroeconomic data, including a higher-than-expected rise in the US Producer Price Index, signaling persistent inflationary pressures.

This diminishes the likelihood of an early interest rate cut by the Federal Reserve, further dampening the outlook for AUD/USD.

Overall, these factors contribute to a negative sentiment for the pair, prompting a notable decline in its value post the Thursday data release.

NZDUSD – Dips to 0.6100 on Rising Safe-Haven Demand Amid Fed Rate Expectations

The Q4 NZD GDP is scheduled this week, already NZ economy is under stagnant, Q3 GDP came at -0.30% decline, if Last quarter of GDP came at negative reading it will be impactful for NZ Dollar downturn in the market.

NZDUSD is moving in box pattern and market has reached resistance area of the pattern

NZD/USD Plummets to 0.6100 Amid Diminished Fed Rate Cut Expectations

In Friday’s early American session, the NZD/USD pair sharply declines to the key support level of 0.6100 as market hopes for a Federal Reserve (Fed) interest rate cut in the June policy meeting fade. This reduction in expectations significantly impacts the demand for risk-sensitive assets.

The S&P 500 opens bearishly as investors seek refuge in safe-haven assets due to uncertainty surrounding the Federal Reserve’s upcoming monetary policy decision, scheduled for announcement on Wednesday. The Fed is anticipated to maintain interest rates within the 5.25%-5.50% range, with focus primarily on the dot plot and economic projections. The US Dollar Index (DXY) remains range-bound around 103.80, while 10-year US Treasury yields climb to 4.31%.

Projections for a Fed rate cut are now shifting to the July monetary policy meeting, as consumer and producer prices continue to exceed expectations in February. This scenario presents challenges for the Fed to justify rate cuts. Fed policymakers emphasize that rate adjustments will only be considered if there is confidence in sustained inflation returning to the 2% target.

Meanwhile, the New Zealand Dollar’s trajectory will be influenced by the release of Q4 Gross Domestic Product (GDP) data for 2023, scheduled for later next week. Forecasts suggest stagnation in the NZ economy, potentially indicating a technical recession if the economy contracts in the final quarter of 2023, following a 0.3% contraction in Q3 2023.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/