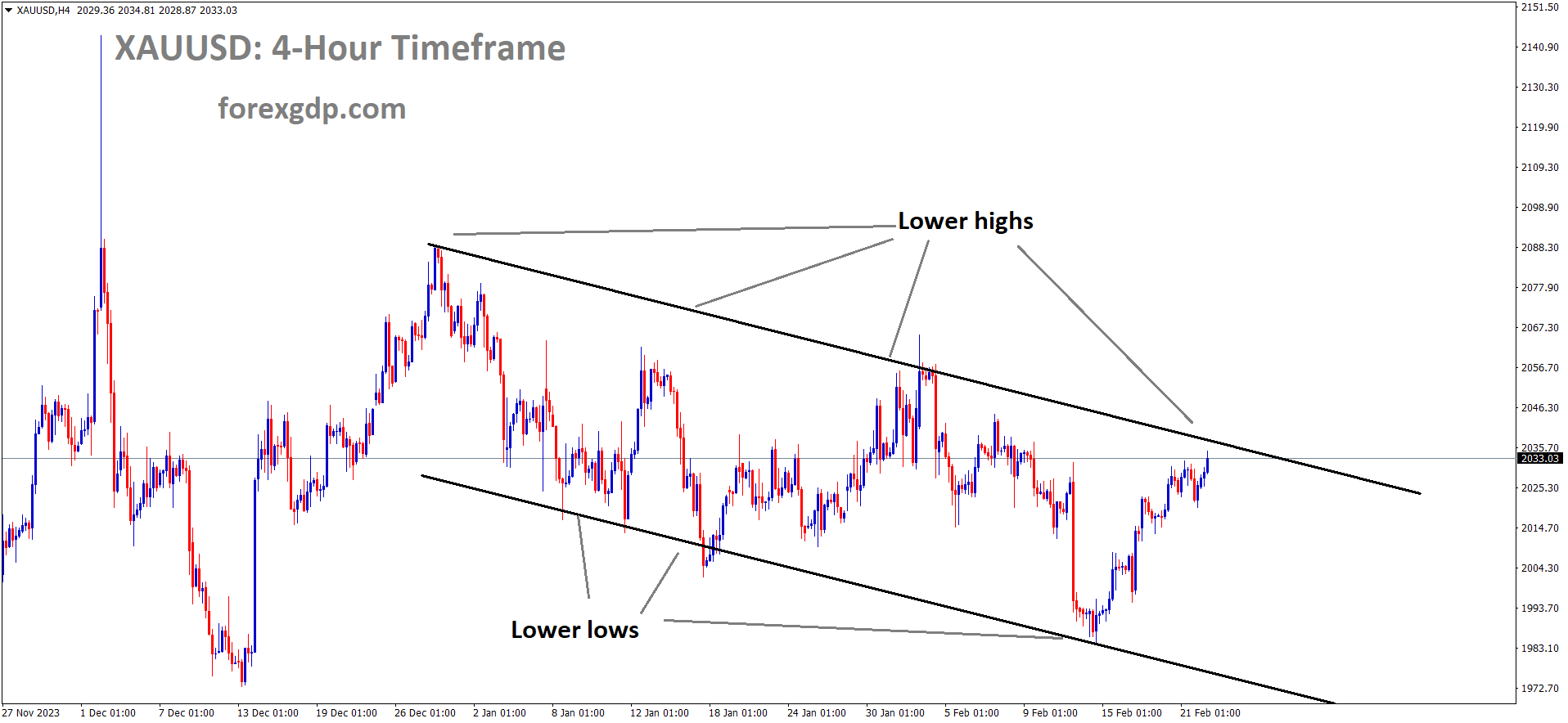

XAUUSD – Gold Prices Drop on Firm US Yields, Strong USD After Solid US Data

The Gold prices are moved down after the US Manufacturing, Composite, Services PMI reading in the Positive numbers against previous month reading. US Manufacturing PMI data came at 51.7 in the June month versus 51.3 in the previous month.US Composite PMI data came at 54.6 in the June month versus 54.5 in the previous month.US Services PMI data came at 55.1 in the June month versus 54.8 in the previous month. Another side US Existing home sales came at down when compared to April month data.

XAUUSD is moving in Ascending channel and market has reached higher low area of the channel

Mixed signals from the US economy have created uncertainty. S&P Global’s June Purchasing Managers Index (PMI) readings surpassed expectations and outperformed May’s data. However, the housing sector showed signs of weakness, with Existing Home Sales for May falling short of expectations and declining compared to April’s figures.

US economic data released throughout the week has highlighted ongoing uncertainty. Indicators like Industrial Production, S&P Flash PMIs, and Retail Sales showed improvement, although Retail Sales were lower than the previous month. On the downside, the housing market continued to struggle, and unemployment claims were higher than expected. This mixed economic picture has kept alive the possibility of a Federal Reserve rate cut in September.

The CME FedWatch Tool indicates a 59.5% probability of a 25-basis-point rate cut by the Fed in September, up from 57.5% on Thursday. Additionally, the December 2024 fed funds rate futures contract suggests a 36-basis-point cut by the end of the year.

Key market movers include:

– US Treasury bond yields remained steady, with the 10-year Treasury note yield flat at 4.261%.

– S&P Global Manufacturing and Services Flash PMIs for June exceeded expectations, with the Manufacturing PMI rising to 51.7 from 51.3 and the Services PMI increasing to 55.1 from 54.8.

XAUUSD is moving in box pattern and market has rebounded from the support area of the pattern

– US Existing Home Sales in May fell to 4.11 million from 4.14 million in April, representing a -0.7% contraction.

– Fed officials advised caution regarding interest rate cuts, emphasizing that decisions would be data-dependent. Despite a positive CPI report last week, policymakers stated the need for more consistent data before considering any rate changes.

– Fed Chair Jerome Powell commented that the Fed remains “less confident” about the progress on inflation, even though the CPI report indicated ongoing disinflation.

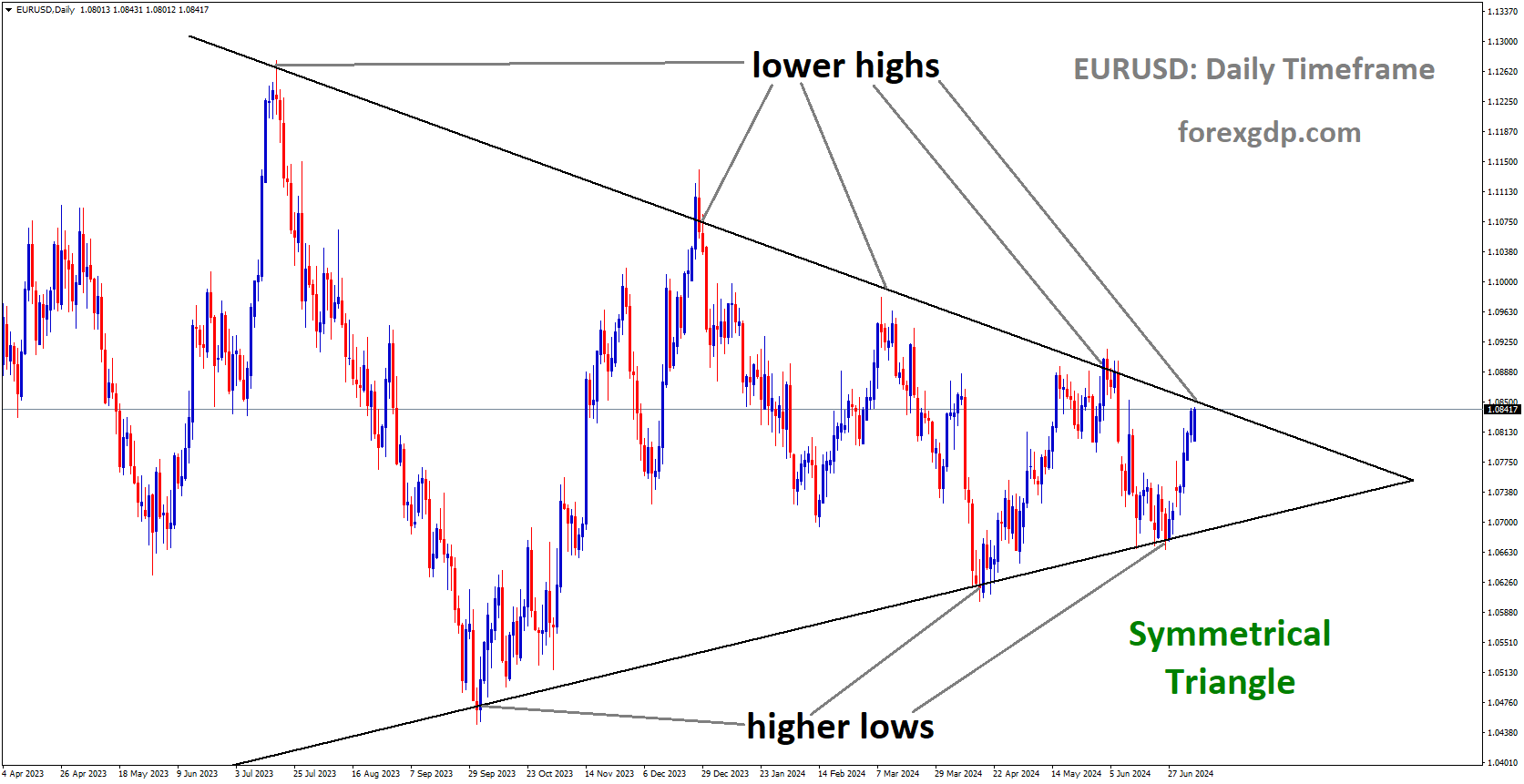

EURUSD – German Economy Minister: EU Tariffs on China Not Punitive

The Germany Economy minister Robert Habeck said EU Tariffs on China EV Vehicles is not the punishment offence tariffs, we did level between EU EV vehicles and China EV Vehicles in the European Market. China said we do supportive for our EV player companies all over the world, we did 350 GW renewable energy sources in 2023, nearly Global half of the World. Germany said Coal is used as highest CO2 emission still used by China, India and Indonesia. We have to control the CO2 emissions to help more renewable energy resources around the world.

EURUSD is moving in Descending channel and market has fallen from the lower high area of the channel

In a recent dialogue between German Economy Minister Robert Habeck and Chinese officials in Beijing, Habeck clarified that the proposed European Union tariffs on Chinese goods, particularly electric vehicles (EVs), are not intended as punitive measures. His visit marked the first by a senior European official since the EU proposed substantial tariffs on Chinese-made EVs due to concerns over what the EU sees as excessive subsidies.

During discussions, Habeck emphasized that the EU’s approach differs from that of countries like the United States, Brazil, and Turkey, who have imposed punitive tariffs in similar situations. Instead, the EU’s actions aim to ensure fair competition by addressing subsidies that Chinese companies may have received unfairly from Beijing.

Habeck stressed that the European Commission had conducted a thorough nine-month investigation into whether Chinese companies had benefited unfairly from subsidies. Any resulting countervailing duties, according to Habeck, are meant to compensate for these advantages rather than punish China.

The proposed EU tariffs, set to take effect by July 4 with an investigation continuing until November 2, could potentially lead to definitive duties lasting up to five years.

Despite the trade tensions over EVs, the meeting between Habeck and Chinese officials also focused on broader cooperation, particularly in climate change and the green transition. Both Germany and China acknowledged their joint responsibility to combat global warming, highlighting their memorandum of understanding signed in June last year for cooperation on these critical issues.

While China has made significant strides in renewable energy, installing nearly 350 gigawatts of new capacity in 2023 alone, concerns remain about its heavy reliance on coal, which still supplies almost 60% of its electricity. This reliance underscores challenges in transitioning to cleaner energy sources despite China’s ambitious renewable energy goals.

In response to Habeck’s concerns about coal expansion, Zheng Shanjie of China’s National Development and Reform Commission defended the construction of coal-fired power plants as essential for energy security, availability, and cost considerations. However, Habeck urged for a reevaluation of China’s energy strategy, emphasizing the need to integrate renewables more effectively into the energy mix to reduce overall carbon emissions.

The dialogue highlighted both cooperation and contention between Germany and China, underscoring their shared commitment to climate action amid ongoing economic and environmental challenges.

USDJPY – Surges Above 159 on US Dollar Rebound, Japanese Disinflation

The Japan Headline inflation rate came at 2.8% in the May month compared to 2.5% in the previous month. The Bank of Japan ready to do rate hikes if inflation rate came at 2% target. Yen depreciation only solved by rate hikes from the BoJ. So USDJPY surpassed 159 level this week, FX intervention is any time possible to control the Yen depreciation as per BoJ members said.

The USD/JPY pair is currently seeing a rally driven by several factors, primarily centered around the dynamics of the US Dollar (USD) and the Japanese Yen (JPY).

USDJPY has broken box pattern in upside

Firstly, the US Dollar’s strength has been bolstered by rising US Treasury yields. Recent increases in yields, such as the 2-year bond yield rising 3 basis points to 4.74% and the 10-year Treasury yield increasing 4 basis points to 4.26%, have contributed significantly to the USD’s upward momentum. This rise in yields followed hawkish remarks from Federal Reserve (Fed) officials, particularly from Fed Bank of Richmond President Tom Barkin. Barkin emphasized that while rate cuts are anticipated, the Fed requires clearer inflation signals before implementing them, reaffirming a data-dependent approach.

Conversely, the Japanese Yen has weakened due to recent economic data, particularly the Japanese inflation figures for May. The data revealed a decline in core inflation, with any gains primarily attributed to increases in energy prices rather than broad-based inflationary pressures. This weakening inflationary environment in Japan has dampened prospects for the Bank of Japan (BoJ) to consider raising interest rates, despite the headline Consumer Price Index (CPI) rising to 2.8% from 2.5% due to utility bill increases following the withdrawal of government subsidies.

Looking ahead, economists at Capital Economics anticipate that underlying inflation in Japan, excluding food and energy, could fall below the BoJ’s 2% target soon. This expectation suggests that while a rate hike might occur at the BoJ’s upcoming July meeting, subsequent rate increases may be postponed as inflation slows further than initially anticipated by the central bank.

In summary, the USD/JPY pair’s recent movements reflect a combination of USD strength driven by rising yields and hawkish Fed commentary, contrasted with JPY weakness stemming from cooling inflation in Japan, posing challenges for the BoJ’s monetary policy decisions in the near term.

USDCHF – Soars Above 0.8900 as SNB Cuts Rates

The Swiss Franc is depreciated against counter pairs after the SNB cut the interest rates 25bps to 1.25% from 1.50% in this week meeting. Swiss Zone inflation reading, GDP,Retail sales are down and under the control of SNB Goals.

The Swiss Franc (CHF) experienced significant depreciation on Thursday following the Swiss National Bank’s (SNB) decision to cut interest rates for the second time this year. The SNB reduced rates from 1.50% to 1.25% during the European session, aiming to counteract the recent strengthening of the Swiss Franc against other currencies, particularly the US Dollar (USD).

USDCHF is moving in Descending channel and market has rebounded from the lower low area of the channel

The move above the 0.8900 mark occurred swiftly after the SNB’s announcement, indicating market reaction to the easing measures intended to curb CHF appreciation.

SNB Chairman Thomas Jordan emphasized that the Swiss Franc had strengthened significantly in recent weeks, prompting the central bank’s proactive stance. Jordan also noted that the SNB stands prepared to intervene in the foreign exchange (FX) market if necessary, although the rate cuts are seen as a primary tool to influence currency values.

Looking ahead, market analysts and Reuters suggest that the SNB could potentially implement further rate cuts in September, depending on economic conditions and the CHF’s exchange rate movements. This preemptive strategy aims to avoid excessive appreciation of the Swiss Franc without resorting to direct market interventions, which can be less predictable in their effectiveness.

Meanwhile, in the United States, economic indicators such as the Initial Jobless Claims report highlighted a cooling labor market, with more individuals filing for unemployment benefits than anticipated. Additionally, the US housing sector showed further signs of deterioration, fueling expectations among traders that the Federal Reserve (Fed) may opt for multiple rate cuts in the near future to stimulate economic growth and mitigate risks.

In summary, the USD/CHF pair’s rally above 0.8900 following the SNB’s rate cut underscores the central bank’s efforts to manage currency appreciation pressures, while also reflecting broader market expectations of potential monetary policy easing by the Federal Reserve in response to weakening economic indicators.

USDCAD – Canadian Dollar Cools Despite Retail Sales Beat

The Canadian Dollar moved upside against counter pairs after the Canada retail sales came at robust upside since July 2022 in the April month. Core retail sales up by 1.8% YoY versus -0.80% contraction last month. Raw material prices fell by 1.0%, Industrial produce prices came at flat.

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

On Friday, the Canadian Dollar (CAD) struggled to maintain its recent gains against the US Dollar (USD), faltering after a strong US Purchasing Managers Index (PMI) report lifted the Greenback broadly. Despite a positive start to the week, where the CAD enjoyed a five-day winning streak against the USD, it faced pressure as US economic indicators outperformed expectations.

Canada reported mixed economic data: core Retail Sales surged impressively by 1.8% month-on-month (MoM) in April, surpassing expectations of 0.7% following a revised decline in the previous month. However, the Raw Material Price Index fell by 1.0% in May, more sharply than the anticipated 0.6% decline, and Industrial Produce Prices remained flat, missing the forecast of a 0.5% increase.

In contrast, US economic data showed strength with the S&P Global Manufacturing PMI rising to 51.7 in June, surpassing expectations of a decline from the previous month. Similarly, the Services PMI increased to 55.1, exceeding forecasts and highlighting robust expansion in the US economy.

Looking ahead to the coming week, the focus for the Canadian Dollar will be on Bank of Canada (BoC) Governor Tiff Macklem’s public appearance on Monday, followed by the release of Canada’s Consumer Price Index (CPI) inflation data on Tuesday, including the BoC’s core CPI print. These releases are expected to provide further insights into the Canadian economic outlook and potential implications for monetary policy.

Overall, while the CAD has maintained some of its strength against the USD over the week, ongoing economic data and central bank developments will likely influence its performance in the near term amidst global economic uncertainties.

USD Index – USD Rises After Strong June Preliminary PMIs

US Dollar moved gains after the US Manufacturing, Composite, Services PMI reading in the Positive numbers against Previous month reading. US Manufacturing PMI data came at 51.7 in the June month versus 51.3 in the previous month.US Composite PMI data came at 54.6 in the June month versus 54.5 in the previous month.US Services PMI data came at 55.1 in the June month versus 54.8 in the previous month.

USD Index Market price is moving in Ascending channel and market has rebounded from the higher low area of the channel

On Friday, the US Dollar, as measured by the US Dollar Index (DXY), extended its gains, driven primarily by strong Purchasing Managers Index (PMI) figures for June released by S&P Global.

The US economic outlook shows signs of disinflation, though Federal Reserve (Fed) officials have expressed caution about initiating easing cycles too quickly. Their remarks aim to keep market expectations balanced. If the mixed signals from the economy persist, they could potentially hinder further gains in the USD.

Daily Digest Market Movers: US Dollar Rides High on Strong PMIs

– US S&P Global Composite PMI for June: Increased slightly from 54.5 in May to a flash estimate of 54.6, indicating healthy expansion in private sector business activity in the US.

– US S&P Global Manufacturing PMI: Rose from 51.3 to 51.7, showing continued growth in the manufacturing sector.

– US S&P Global Services PMI: Increased from 54.8 in May to 55.1, beating analysts’ estimates and highlighting robust performance in the services sector.

Rate Cut Probability

– According to the CME Group’s FedWatch Tool, the probability of a rate cut at the September 18 meeting stands at around 65%.

These strong PMI figures reflect solid economic activity and have contributed to the recent strength of the US Dollar. However, the cautious stance of Fed officials and ongoing economic uncertainty could influence future movements.

GBPUSD – Ends Week Lower Amid Steep Bearish Turnaround

The UK Retail sales Jumped to 2.9% MoM, 1.3% YoY in Core side, Annual headline retail sales Jumped to 2.9% MoM and 1.2% YoY. The GBP pairs slight rebounded against counter pairs after the uptick reading from the Downtick reading printed in the last month.US Services , Manufacturing and composite PMI ticked higher reading printed in the evening makes GBP dragged down against USD.

GBPUSD has broken Ascending channel in downside

The Bank of England’s decision to hold rates midweek failed to bolster confidence in the British Pound (GBP), while a late-week rise in US Purchasing Managers Index (PMI) data dampened overall market risk appetite, thereby strengthening the US Dollar (USD) as the trading week concluded.

In the UK, Retail Sales rebounded strongly in May, increasing by 2.9% month-on-month (MoM), surpassing expectations of a decline to 1.5% following the previous month’s revised contraction of -1.8%. However, UK PMI data presented a mixed picture: the S&P Global/CIPS Manufacturing PMI for June edged up to 51.4, slightly exceeding the forecast of 51.3 but still reflecting modest expansion. In contrast, the Services PMI fell sharply to a seven-month low of 51.2, missing expectations of a rise to 53.0 from 52.9.

Looking ahead, the UK economic calendar appears light for the coming week, with Sterling traders anticipating Friday’s Gross Domestic Product (GDP) report for further guidance. Meanwhile, in the US, early-week economic releases are expected to be mid-tier, with the highlight being the US GDP update scheduled for Thursday. Strong US economic data releases last week have reduced expectations of an imminent rate cut by the Federal Reserve (Fed), bolstering demand for the safe-haven USD towards the end of the trading week.

Overall, market sentiment remains cautious with focus on upcoming economic indicators that could influence GBP/USD dynamics amidst evolving global economic conditions and central bank policies.

AUDUSD – Australian Dollar Ends Week with Losses Amid Weak PMIs

The Australian Dollar moved down after the Australian PMI data came at weaker numbers in the June month. Manufacturing PMI data came at 47.5 from 49.2, Services PMI came at 51.0 from 52.5, and Composite PMI came at 50.6 from 52.1. RBA Governor Michelle Bullock said there are no rate cuts this year, rate hikes is more in order to control the inflation to target of 2%.

AUDUSD is moving in box pattern and market has rebounded from the support area of the pattern

Selling pressure intensified in Asian markets due to soft preliminary Purchasing Managers Index (PMI) data from Judo Bank in Australia. This weakness was compounded by elevated US Treasury yields and optimistic PMI figures from S&P in the US, which bolstered the US Dollar.

Despite indications of economic fragility in Australia, persistently high inflation has prompted the Reserve Bank of Australia (RBA) to delay potential rate cuts, potentially mitigating losses for the Australian Dollar. The RBA is positioned among the last G10 central banks expected to initiate rate cuts, a factor that could support the Aussie’s stability.

Daily Digest Market Movers: Australian Dollar Navigates Weak Data, Awaits Clarity

– Australia’s June Preliminary PMI Data: Showed weakening across sectors:

– Manufacturing PMI dropped to 47.5 from May’s 49.7

– Services PMI decreased to 51.0 from 52.5

– Composite PMI fell for a third consecutive month to 50.6 from 52.1 in May.

– US Economic Performance: Continued to demonstrate robust growth in private sector activity, with the S&P Global Composite PMI improving slightly to 54.6.

– RBA’s Stance on Monetary Policy: Governor Bullock emphasized discussions on potential rate hikes, dismissing near-term rate cut considerations due to persistent inflation exceeding targets. The RBA remains committed to taking necessary actions to bring inflation back within target ranges.

– Market Expectations:

– Anticipation of nearly 50 basis points of easing by December 2025, with potential rate hikes in August and September not ruled out by the RBA.

– The Federal Reserve signals only one rate cut in 2024, while markets continue to hope for a cut in September.

These dynamics underscore the contrasting economic conditions influencing currency movements, particularly impacting the Australian Dollar against the backdrop of global economic data and central bank policies.

NZDUSD – Surges to 0.6150 as New Zealand Exits Recession

NZ Dollar Jumps to higher after the Q1 GDP came at 0.20% QoQ versus 0.0% printed in the last quarter. Annual Basis expanded by 0.30% versus -0.20% contraction in the last quarter. Consumer confidence decline to 82.2 reading from 93.2 printed in the last month. Now NZ exits recession after the strong Q1 GDP numbers printed.

NZDUSD is moving in box pattern

New Zealand’s economy showed resilience with a 0.2% quarter-on-quarter growth in Q1, rebounding from stagnation in the previous quarter. Annually, GDP expanded by 0.3% in Q1, contrasting with a 0.2% contraction in the preceding quarter. This positive GDP surprise lifted the New Zealand Dollar (NZD) as it signaled the country’s exit from recession.

In contrast, Westpac New Zealand’s Consumer Confidence Survey reflected a downturn in sentiment to 82.2 for Q2, down from 93.2 previously.

The USD faced pressure following a disappointing US Retail Sales report last week, which heightened expectations of Federal Reserve (Fed) interest rate cuts in the coming months. Currently, markets are pricing in a 67% probability of a 25 basis points rate cut in September, up from 61% previously, according to the CME FedWatch tool. Boston Fed President Susan Collins mentioned the possibility of one or two rate cuts later this year, emphasizing the Fed’s cautious stance amid volatile inflation readings.

XTIUSD – Crude Oil Retreats from Fresh Highs on EIA Natural Gas Buildup

The Crudeoil reported higher gains in the market during higher stock piles reported by EIA administration in the US. EIA reported 71 Billion Cubic Feet Natural gas reserves by the week end June 14. Now totalling 3054 Billion Cubic feet in the reserves of the US.

XTIUSD has broken Descending channel in downside

West Texas Intermediate (WTI) US Crude Oil initially rose to a weekly high early on Friday but later retreated into negative territory after the Energy Information Administration (EIA) reported that US Crude Oil production remains near record levels and there was a larger-than-expected increase in Natural Gas reserves.

The EIA’s report indicated a significant 71 billion cubic feet (Bcf) increase in natural gas storage, bringing total US reserves to 3,045 Bcf for the week ending June 14. This marked a multi-month high, following the previous week’s build-up of 74 Bcf, which was anticipated to decrease more steeply to just 69 Bcf.

The filling up of natural gas reserves ahead of peak summer cooling demand suggests reduced prospects for significant increases in Crude Oil demand. This expectation dampens hopes for a substantial drawdown in Crude Oil inventories over the summer months.

Additionally, on Friday, US Purchasing Managers Index (PMI) figures for June exceeded expectations, reinforcing the view that the Federal Reserve (Fed) is unlikely to accelerate its pace of interest rate cuts in 2024. This development has led Crude Oil markets to reassess near-term bullish expectations, as investors increasingly rely on hopes of rate cuts to alleviate lending and financing costs.

Overall, the combination of robust natural gas reserves and strong economic indicators has tempered immediate optimism in the Crude Oil market, prompting a cautious outlook amidst evolving global economic conditions and Fed policy considerations.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!