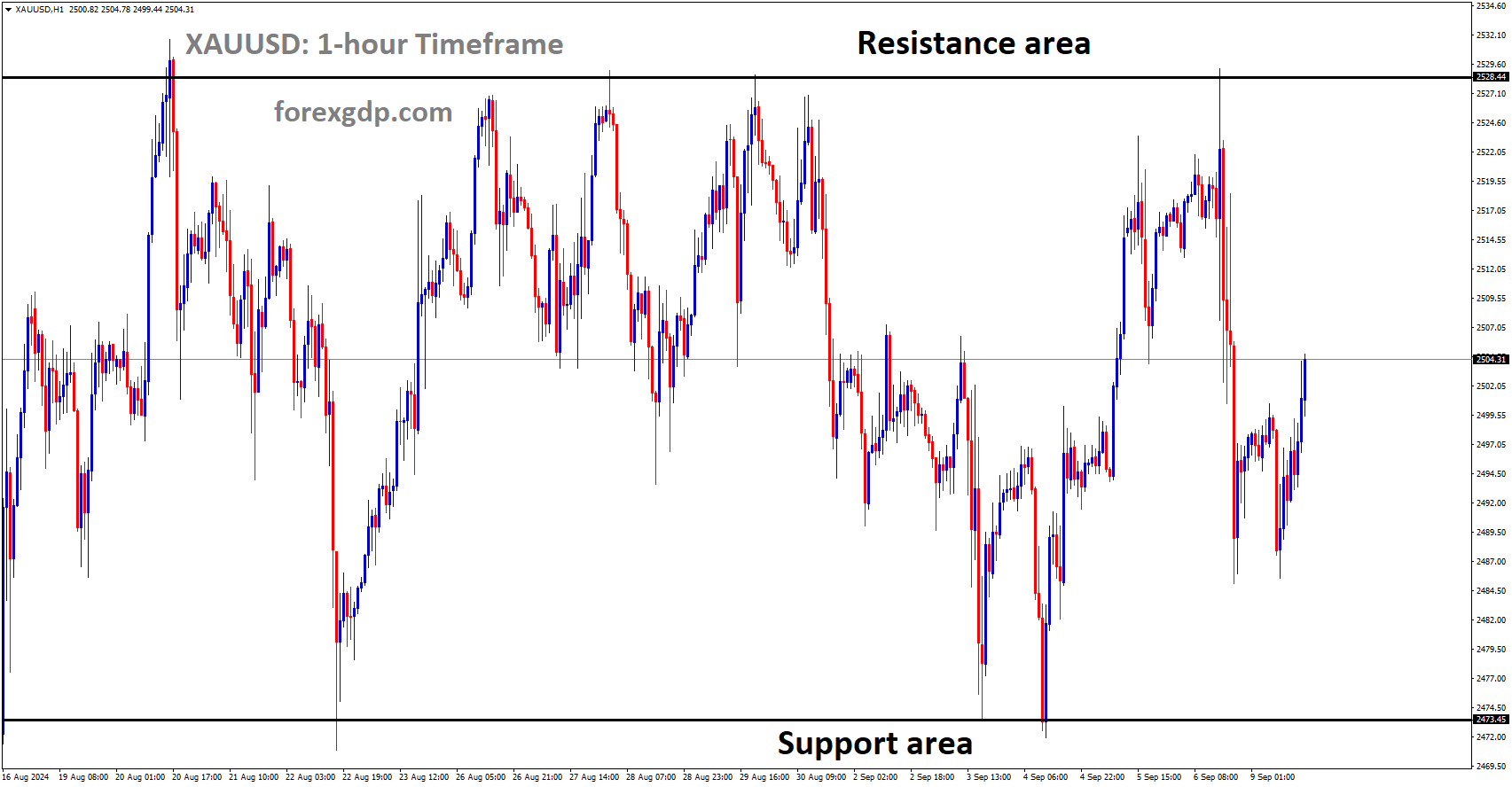

Gold: US PPI data forecast

Gold shows consolidation mode in the last two weeks due to new strain faced across Globes and waiting ahead of FOMC and PPI report.

XAUUSD Gold price is moving in an ascending triangle pattern and the market fell from the horizontal resistance area.

The UK announced face mask mandatory, and the US also joined with the same regulations to avoid Widespread Omicron variants.

And this week FOMC meeting will dictate how many numbers will be tapering and when rate hikes are going to happen in 2022.

The US PPI data for November is expected to be 9.2% YoY from 8.6% the previous month. So now all eyes are on the FOMC meeting and US PPI data this week.

And the Demand for yellow metal shows less on investors side because chances of rate hikes from Central banks to counter inflation are higher.

US Dollar: Moody’s View on FED action in 2022

USDJPY is moving the major descending triangle pattern and market falling from the top of the triangle pattern and the market reached the higher low area of the Ascending trendline.

Global Rating agency Moody’s view on US FED like to increase rates in the Second half of 2022 as tapering will end.

And If FED acts lazier for inflation, higher progress and then US Economy will face more inflation than expected. If FED acted too fast for tapering and rate hikes is also making insufficient funds to handle if the third wave gets severed.

So now FED action will be an intermediate stance to act well upon situation handling.

Once by March or June 2022, tapering will be complete as expected, rising interest rates in the second half of 2022 will be much better for the US Economy.

New York FED survey report and waiting on FOMC and PPI Data

The New York FED survey shows one-year median inflation survey increased to 6.0% in November from 5.7% in October.

But the Three-year Median inflation declined to 4.0% from 4.2%.

So, uncertainty surrounds short and medium-term inflation outlook.

The survey shows a wide gap difference between 2013 and 2021.

Earnings growth is expected to dim at 2.8% in November from 3.0% in October. Next year earnings growth will be 3.2% with rising inflation numbers.

And the one year home prices decreased to 5.0% from 5.7% as per the median survey.

EURO: ECB vs FED monetary policy has wide divergence

EURUSD is moving in the Descending channel and the market reached the lower high area of the channel.

ECB committee shows no rate hikes and no tapering in the near term as ECB Lagarde views.

But for FED, it was opposite to the point; FED Powell & CO said the speeding of tapering assets would be increased in coming quarters to cool off inflation data in the US.

This week FOMC meeting suggested at least more numbers of tapering will be announced as expected by Analysts.

ECB will reduce the asset purchases from PEPP’s compared to the second and third quarters as the decision expected in this week’s ECB meeting.

ECB Versus FED saw more deviation gap in interest rate decision and tapering instrument based on Covid-19 handling by respective Governments.

UK POUND: UK Unemployment rate came in good numbers

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

UK reported that people claiming unemployment-related benefits decreased by 49.8K in November against a 14.9k fall in the previous month.

UK Unemployment rate fell to 4.2% from 4.3% during three months to October.

And the Wage pressures are slightly going higher by year-end is all expected.

UK PM Johnson announced at least first dead from new strain in the UK. By considering this, they are more cautious on UK Economy and People to stay away from new variants by announcing more restrictions on the economy.

Bank of England failed to increase interest rates this week due to new variant lockdown and restrictions.

Canadian Dollar: Bank of Canada extended the 2% inflation mandate until 2026

USDCAD is moving in an ascending channel and the market has reached the previous horizontal resistance area of the channel

Bank of Canada set to extend the inflation mandate of 2% until 2026 from January 1, which was the deadline date.

Inflation hits 40 years high in Canada, so worries surround the Bank of Canada policy to hike rates expectations.

But the Canadian Dollar is nothing reacted to news flashed and going down after Oil prices declined.

And now Bank of Canada is waiting for absorbing the Jobs data, which was slack in recent years.

China reported the first Omicron cases, UK reported the First Omicron death, told by UK PM Johnson.

Japanese Yen: Bank of Japan announced to inject more funds to tackle short term interest rates

GBPJPY is moving in the Symmetrical triangle and market rebounding from the bottom area of the Symmetrical triangle pattern.

Bank of Japan announced it would like to deploy more funds to the market to counter rising short term interest rates.

And going to intervene in the money market and inject $97 billion via temporary Government bond purchases.

Buying Bonds worth 2 trillion Yen for immediate fund provision and another 7 trillion Yen for injection of funds.

So, the Japanese Government is making smart efforts to tackle new variants and the economy to stable up from pandemics.

Australian Dollar: NSW face cases from New strain is higher and FOMC and PPI data forecaste

AUDCHF is moving in the Descending channel and the market reaching the lower low area of the channel from the Top.

New South Wales facing cases increased to higher from lower numbers.

And Australian Dollar faced downward pressure as RBA Quietly unchanged interest rate and asset purchases per month.

And also, the US Posted a higher number of cases, but FED has the tool to increase the tapering numbers per month, But RBA won’t be acted fast, and it will hold in an accommodative stance.

China reported the first case from the Omicron variant, and the UK announced the First death from the omicron variant.

So, Traveller’s restrictions may be extended by the Australian Government or eased based on new cases spread in Major populated cities.

New Zealand Dollar: RBNZ Governor Speech forecast

GBPNZD is moving in an Ascending channel and the market reached the previous resistance area of the channel.

New Zealand Dollar posted losses as US Dollar performed well in recent months.

And Tomorrow, RBNZ Governor Orr’s speech will happen; any lagging of the Economy outlook or postponement of rate hikes will hammer New Zealand Dollar again.

Cases increased in Neighboring country Australia, now, so New Zealand may be faced soon from new variant. Some easing restrictions are now announced ahead of the Christmas holidays and New Year’s Eve.

New Zealand Q3 GDP will be announced this week, a weaker number expected due to more lockdown faced in the third quarter.

Swiss Franc: SNB trying to stable Swiss Franc prices higher

USDCHF is moving in the Descending triangle pattern and the market has reached the horizontal support area of the triangle pattern

SNB faces higher deposits from investors shows the highest in seven months in 2021.

So now SNB has to control the rise of Swiss Franc prices mainly against EURO, by rising Swiss franc prices during pandemic started in 2020.

This week SNB will decide whether to rate cut or buy more assets to tackle Swiss Franc proceeding higher.

And FED will act for tapering soon and complete in March 2022; After this, we can expect two rate hikes in 2022.

As FOMC and PPI data are scheduled this week US Dollar shows strong dominance against the Swiss Franc.

Don’t trade at your free time, instead trade the markets only when there are confirmed trade setups.

Get confirmed trade setups here: https://www.forexgdp.com/buy/