Garden reach Ship Builders: GRSE Stock Hits Record High After Strong Q4 Performance

The GRSE Company Q4 results are robust and cheered by investors. Net revenue rose to 69% as Rs.1000 cr, Net profit doubled to Rs.112 cr and EBITA tripled to Rs.90.5 cr. The company has healthy order books in FY 2024. So Far FY24 net revenue increased to 40% and Net profit comes to 57%.

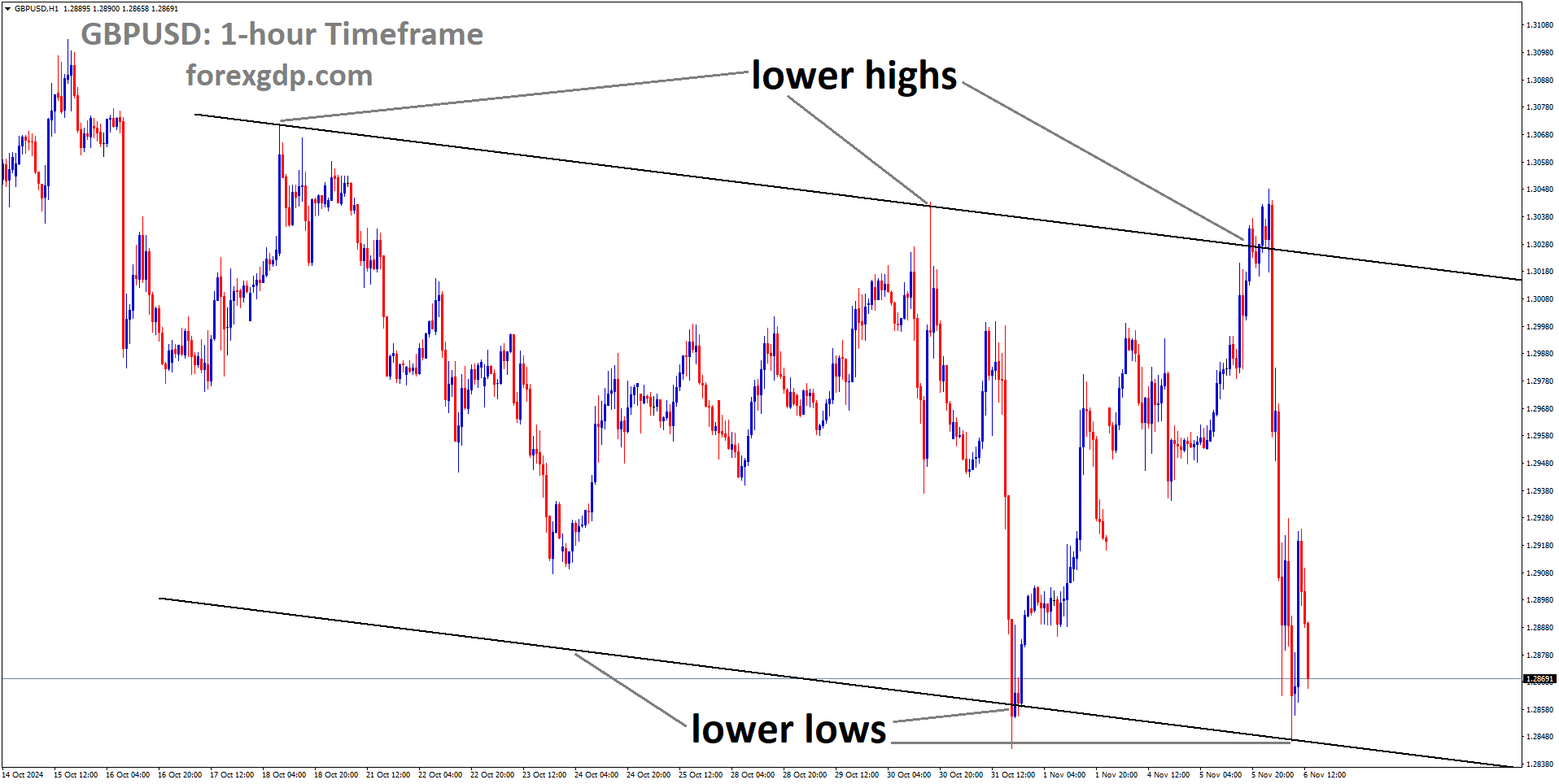

GARDEN REACH SHIPB Market price has broken Ascending channel in upside

This surge came as investors celebrated the company’s impressive fourth-quarter results.

During Q4, Garden Reach Shipbuilders witnessed a remarkable growth in revenue, crossing the Rs 1,000 crore mark, representing a 69 percent increase compared to the same quarter the previous year. The company’s net profit doubled to Rs 112 crore during the quarter on an annual basis.

Moreover, Garden Reach Shipbuilders’ EBITDA (earnings before interest, tax, depreciation, and amortization) more than tripled in Q4, reaching Rs 90.5 crore compared to Rs 20 crore in the corresponding period last year.

The management of Garden Reach Shipbuilders expressed satisfaction with the record-high revenue and profit achieved in the quarter. They also expressed optimism about sustaining this growth trajectory in the future.

Additionally, the company highlighted the robustness of its order book, with ongoing projects contributing significantly to revenue. Furthermore, Garden Reach Shipbuilders anticipates securing more orders in the near future. For FY24, the company reported a 40 percent increase in revenue and a 57 percent growth in net profit.

Power Grid: Power Grid Stock Drops 4% Despite Weak Q4, Morgan Stanley Sticks to Outperform

The Power Grid Corporation reported weak Q4 Results, Net profit declined to 3.6% as Rs.4166 cr from Rs.4323 cr in the past quarter, Net revenue declined to 2.5% as Rs.11978 cr from Rs.12286 cr in the past quarter. The Analysts and Brokerages like Morgan Stanley Upgraded this stock after the PAT rised 3% compared to previous quarter.

Power Grid Corp Market price is moving in Ascending channel and market has fallen from the higher high area of the channel

State-run Power Grid Corporation of India Limited (Power Grid) witnessed a sharp decline of over four percent in early trading on May 23 as investors reacted to the company’s lackluster earnings report for the quarter ending March.

The power major reported a 3.6 percent decrease in net profit for the March quarter, amounting to Rs 4,166 crore compared to Rs 4,323 crore in the corresponding period the previous year. Similarly, revenue declined by 2.5 percent to Rs 11,978 crore from Rs 12,286 crore in the previous fiscal year.

Despite the disappointment expressed by investors, international brokerage Morgan Stanley decided to maintain its overweight call on Power Grid. The brokerage retained a target price of Rs 296 per share, indicating a potential downside of around 10 percent from the previous session’s close.

Morgan Stanley noted that Power Grid’s results surpassed its estimates, with the earnings beat primarily driven by other income. The company’s consolidated adjusted profit after tax (PAT) was three percent higher than the brokerage’s estimates.

Analysts had anticipated muted Q4 results for Power Grid, with expectations of revenue and profits declining from the previous year’s high base. According to a Bloomberg consensus estimate of five brokerages, analysts predicted that Power Grid might report a revenue of Rs 10,594 crore for the quarter, down 18 percent year-on-year.

Over the past year, Power Grid shares have surged approximately 80 percent, outperforming the benchmark Nifty 50, which has risen around 23 percent during the same period.

RAMCO CEMENTS: Ramco Cements Q4 Weak on Cement Price Drop, Brokers Predict 11% Decline

The Ramco Cement delivered poor Q4 Results of FY24, Net profit declined to 20% as Rs.121 cr from Rs.152 cr in the past quarter, Net revenue increased by 4% as Rs.2687cr from Rs.2581 cr in the past quarter. Company net debt increased by Rs.470 cr in this quarter and totally Rs.4820 cr as Net debt so far.

RAMCO CEMENTS Market price is moving in Ascending channel and market has reached higher low area of the channel

Ramco Cements’ earnings report for the quarter ending March failed to impress brokerages as margins remained under pressure due to softening cement prices.

The cement manufacturer recorded a 20 percent decline in net profit, amounting to Rs 121 crore, down from Rs 152 crore in the corresponding quarter of the previous fiscal year, as cost pressures persisted.

Despite the decline in net profit, the firm’s net revenue saw a modest increase of four percent to Rs 2,687 crore during the quarter, up from Rs 2,581 crore in the year-ago period.

Cement volume is anticipated to recover post-elections, supported by robust demand from the housing and commercial segments.

However, brokerages expressed concerns and adjusted their target prices for Ramco Cements accordingly:

– Motilal Oswal reduced its target price from Rs 940 per share to Rs 870 per share while maintaining a neutral call. The brokerage expects the company’s volume growth to moderate to approximately 8 percent CAGR over FY24-26 compared to 29 percent over FY22-24.

– Emkay Global slashed its target price to Rs 865 per share from Rs 950 previously, citing concerns about deleveraging over the next couple of years. However, the brokerage upgraded its rating to add from reduce, noting that the recent stock correction already reflects near-term challenges.

– Jefferies lowered its target price to Rs 690 per share, implying an 11 percent downside, and maintained its underperform rating. The brokerage highlighted concerns about Ramco Cements’ consistently higher leverage, which is expected to continue weighing on investor sentiment.

Over the past year, Ramco Cements’ shares have declined by approximately 11 percent, while the frontline Nifty 50 index has risen around 23 percent during the same period.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!