Honasa Consumer: Mamaearth Parent’s Stock Soars 7% on Record Q4 Profit

The Honasa consumer parent company of Mama Earth product reported net profit of Rs.30 cr from the loss of Rs.160 cr in the last quarter. The Revenue grew by 21.46% as Rs.471.09 cr compared to Rs.387.45 cr in the last quarter. EBITA Margin increased by 7.85%, Sales grow by 23.3% quarterly and 31.6% in the Annually.

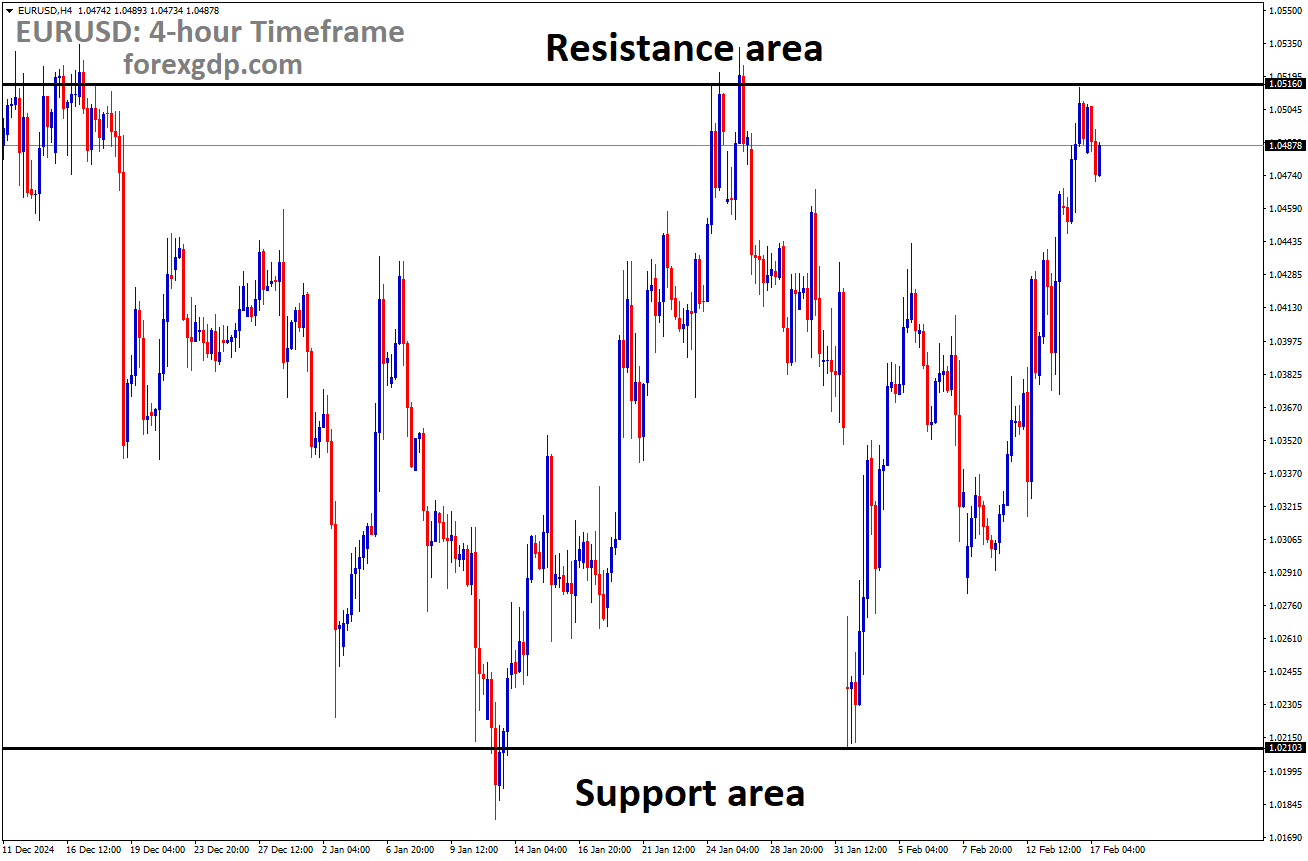

HONASA CONSUMER Market price is moving in box pattern and market has rebounded from the support area of the pattern

Shares of Mamaearth parent company, Honasa Consumer, rose 7 percent in early trade on May 24, following the announcement of their highest-ever quarterly net profit for the January-March quarter of FY24.

The company reported a net profit of Rs 30 crore for Q4 FY24, a significant turnaround from a loss of Rs 160 crore in the same period the previous year, which included an exceptional loss of Rs 155 crore.

Revenue grew by 21.46 percent to Rs 471.09 crore in the March quarter, compared to Rs 387.85 crore a year ago. The company’s EBITDA margin also expanded by 780 basis points, further boosting investor sentiment.

The company attributed its continued growth momentum and increased profitability in Q4 to network expansion, with FMCG outlets growing to 1,88,377 across India as of March 2024, representing a 34 percent year-on-year increase.

“Despite industry headwinds, Honasa has demonstrated remarkable resilience and growth for the quarter and fiscal, with robust like-for-like sales growth of 23.3 percent for the quarter and 31.6 percent annually,” said Chairman and CEO Varun Alagh.

INDIGO: IndiGo’s Strong Q4 Results Lead to Target Price Hikes; Up to 18% Upside Seen

The Indigo Airlines company reported Robust Q4 Net profit as Rs.1894 cr as 106% YoY rise and Revenue from operations up by 26% as Rs.17825.30 cr and EBITA profit rose to Rs.4412.3cr from 2966.5 cr in the last quarter. Margin expanded to 24.8% in this quarter from 20.9% in the last quarter. This quarter mostly comes from Lowering the Fuel Jet costs, Bulk purchases of Aircraft engines and materials from Direct OEM suppliers, increased Air Travel from customers.

INTERGLOBE AVIATIO Market price is moving in Ascending channel and market has reached higher high area of the channel

The low-cost airline InterGlobe Aviation, operating as IndiGo, reported earnings above expectations for the quarter ending in March 2024, leading to multiple target price hikes as analysts maintain a bullish outlook.

The company achieved a robust 106 percent year-on-year growth in net profit, reaching Rs 1,894 crore, driven by strong demand for air travel, significant capacity additions, low jet fuel costs, and increased yields, though partially offset by aircraft on the ground (AoG).

IndiGo has strategically placed bulk orders for aircraft and engines, enabling it to secure favorable terms with original equipment manufacturers (OEMs). The airline focuses on limited, high-demand point-to-point destinations, which contributes to its lowest cost structure in the competitive industry, according to Nuvama Institutional Equities.

In Q4 FY24, IndiGo’s revenue from operations increased by 26 percent year-on-year to Rs 17,825.30 crore. The carrier’s EBITDAR (earnings before interest, tax, depreciation, amortization, and rent) rose to Rs 4,412.3 crore from Rs 2,966.5 crore a year earlier, with its margin expanding to 24.8 percent from 20.9 percent.

Morgan Stanley issued an ‘overweight’ rating on IndiGo, raising the target price to Rs 5,142 per share. The brokerage noted that the airline’s Q4 EBITDA exceeded estimates by 10 percent but expects flat revenue per available seat kilometer (RASK) year-on-year due to rising inflationary pressures.

IndiGo is set for significant changes, including loyalty programs, business class services, and long-haul international flights, which align with evolving consumer preferences despite potential near-term cost pressures, Morgan Stanley said.

Jefferies maintained a ‘hold’ rating on IndiGo but increased the target price to Rs 4,150 per share. The impressive Q4 performance was driven by a 7 percent year-on-year increase in yields, offsetting cost pressures. IndiGo also announced plans to launch business class services by the end of 2024, surprising investors.

The company benefits from a constrained capacity environment, leading to favorable yields and spreads. However, Jefferies believes the stock’s strong performance already reflects these positive factors.

Analysts at Emkay Global highlighted that IndiGo’s management expects Q1 FY25 capacity growth of 10-12 percent year-on-year, despite AoG remaining in the mid-70s. RASK is expected to be flat year-on-year in Q1 FY25, with potential cost pressures on maintenance and airport charges.

IndiGo is introducing a customized business class offering by August 2024, with international expansion remaining a key strategy. Emkay retained a ‘buy’ rating with a target price of Rs 5,000.

“IndiGo has been delivering best-in-class performance, gaining market share. Despite being largely domestic-focused, IndiGo has among the best aircraft utilization levels,” said Nuvama, maintaining a ‘buy’ rating and raising the target price by 21 percent to Rs 5,192.

Key risks for IndiGo stock

Nuvama analysts identified policy and regulatory framework uncertainty as a concern for IndiGo. An adverse taxation structure could increase business costs, impacting profitability.

An economic slowdown could pressure demand for corporate and leisure travel, affecting load factors and profitability due to the high operating leverage in the airline industry. Capacity constraints at major Indian airports like Mumbai, Chennai, and Kolkata could also limit growth. Rising competition from Air India and higher oil prices are potential negative triggers for the stock.

Emkay Global noted additional risks, including adverse currency and fuel prices, economic slowdown, stake sales, and operational issues.

VODAFONE IDEA: Vodafone Idea Stock Soars 9% on UBS Upgrade; Analysts Predict 80% Upside

The UBS Preffered the Vodafone Idea stock to upgrade due to AGR Case appearing in the Supreme court this week, if this appeal favors for Vi Company then $5 Billion Tax waiver for this company shows increase in the profit in the coming quarters. $3 Billion from Spectrum Tax and $2 Billion from AGR dues.

VODAFONE IDEA Market price is moving in Ascending channel and market has fallen from the higher high area of the channel

The international brokerage forecasts a potential 70-80 percent rally in Vi’s stock, anticipating relief measures such as a reduction in Adjusted Gross Revenue (AGR) by the Supreme Court or equity conversion, coupled with government moratoriums. These measures are deemed highly likely, especially given the government’s objective of maintaining three viable private telecommunications companies.

UBS currently sets Vi’s target price at Rs 18, considering a 50 percent probability of AGR dues waiver. While other potential relief measures like spectrum due cancellation or deferral are acknowledged, they are considered less probable and hence not included in the base price target calculations.

“VIL is most leveraged to any such relief, yet the stock is trading at a similar 11 times FY26e EV/Ebitda as Airtel and Jio. We believe risk-reward is attractive going into any such announcement and upgrade to Buy,” UBS stated.

Vi’s annual payment to the government is projected to exceed $5 billion from FY26 onwards, comprising $2 billion for AGR and $3 billion for spectrum. Analysts estimate that 50-75 percent of AGR dues could potentially be canceled for Vi, based on details from the curative petition filed by telcos on the AGR case.

“Assuming AGR dues are completely waived, our DCF value could increase to Rs 24 per share, against Rs 12 when there are no waivers,” UBS added.

Analysts at UBS suggest that the stock market anticipates a 15-20 percent mobile price increase in the next 1-2 years, particularly as Vodafone Idea’s follow-on public offer (FPO) concludes and Bharti Airtel and Reliance Jio prioritize return on invested capital (ROIC) over market share gains.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!