The US Non-Farm Payroll (NFP) report is anticipated to show a decline of 184,000 jobs compared to the previous figure of 209,000. This reduction is attributed to the Federal Reserve’s decision to raise interest rates, which has resulted in slower job growth and subsequently impacted business profit earnings positively. Despite the decrease in job creation, the unemployment rate remains at a low level of 3.6%.

GBPUSD is moving in Ascending channel and market has reached higher low area of the channel

The US economy faces a critical juncture as it contends with the aftermath of a 25bps rate hike from the Federal Reserve, possibly the final move of the current cycle. With interest rates reaching 20-year highs, the upcoming July nonfarm payrolls report holds immense importance in assessing the resilience of the US economy. This report aims to provide a detailed analysis of the recent economic developments, the June jobs report’s impact on market sentiment, and the expectations for the July nonfarm payrolls report. Additionally, it explores the potential influence of the ISM PMIs on the US dollar and the overall focus on economic activity alongside inflation.

1) The Impact of the June Jobs Report

1.1 Unremarkable Nature of the June Jobs Report

The June nonfarm payrolls report exhibited a rather unremarkable performance, with job growth slowing to 209,000 from 306,000 in May.

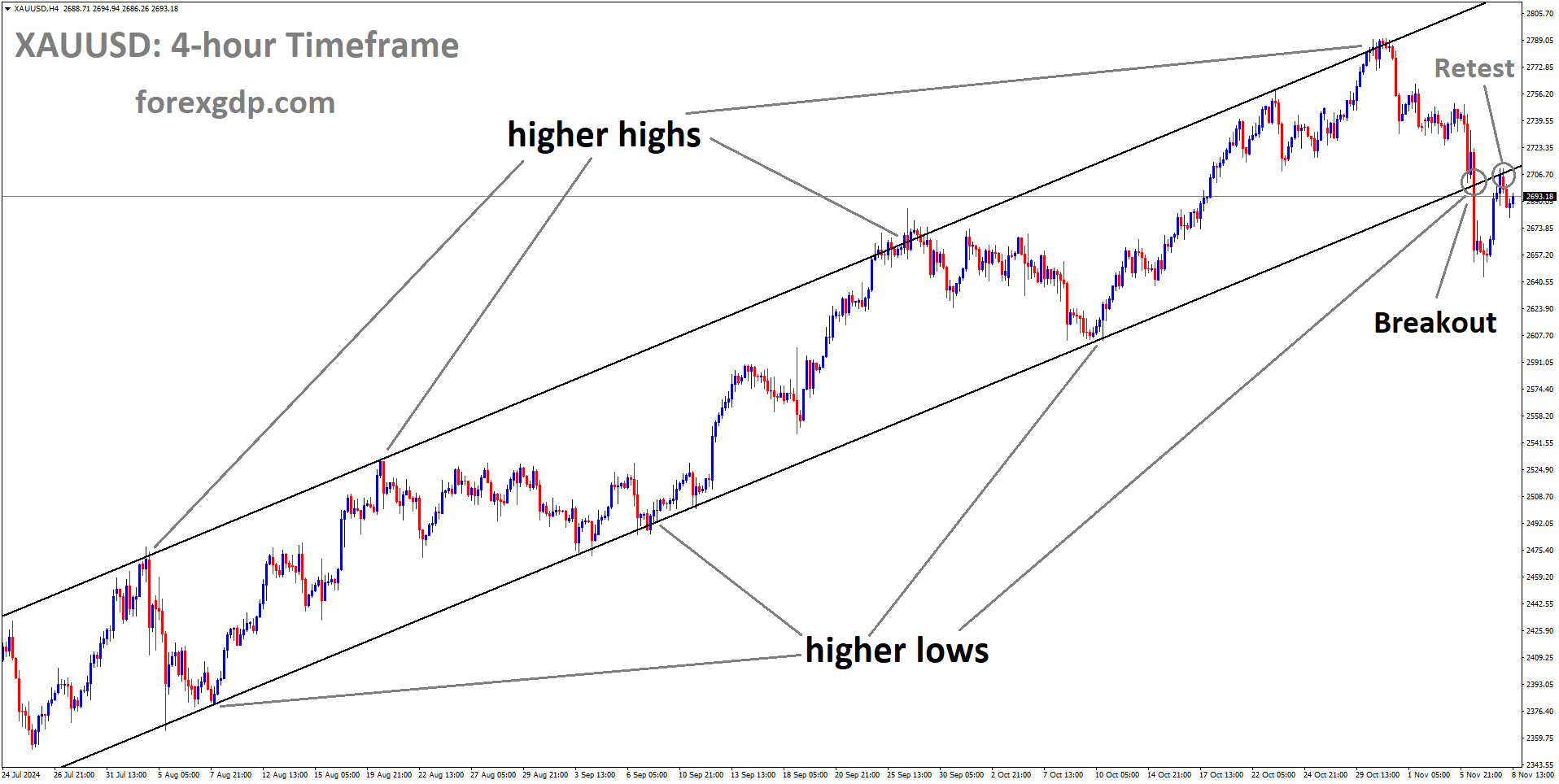

XAUUSD is moving in descending channel and the market has reached lower low area of the channel.

This slowdown was the slowest rate seen in over two years, raising concerns about the health of the labor market.

1.2 Taming the Froth in Yields

Despite the unremarkable nature of the report, it played a crucial role in subduing the excitement and frothiness in the market, particularly in the aftermath of the ADP payrolls report, which showed a remarkable jump of 497,000 jobs added during the month.

1.3 Impact on Market Sentiment

The June report, combined with the Federal Reserve’s recent rate hike, had varying effects on market sentiment. While it dampened some of the excessive enthusiasm, it also cast doubts on the pace of economic recovery and potential implications on future monetary policy.

2) Expectations for the July Nonfarm Payrolls Report

2.1 Projections for Job Growth

As the economy grapples with inflationary pressures and concerns about a wage-price spiral, economists forecast a modest rise of 184,000 nonfarm payrolls for July, a decline from the previous month’s figure of 209,000.

2.2 Unemployment Rate and Earnings Growth

USDCAD is moving in Descending channel and market has reached lower high area of the channel.

The unemployment rate is expected to remain steady at 3.6%, while average hourly earnings are projected to maintain their growth at slightly above 4% year on year.These figures will provide valuable insights into inflationary pressures and wage dynamics.

2.3 Weekly Jobless Claims

The gradual decline in weekly jobless claims during most of July suggests a positive surprise in the nonfarm payrolls report. However, the market’s reaction may be mixed, considering the implications for a potential rate hike in September.

3) Fed’s Stance and Economic Activity

3.1 Federal Reserve’s Open Options

With the Fed’s rate hike decision behind, market participants look to the upcoming jobs report for cues on the central bank’s stance for the September meeting.The report’s strength or weakness could influence the likelihood of further rate adjustments.

3.2 Employment Growth Trend

The US jobs market has been showing signs of losing momentum throughout the year.

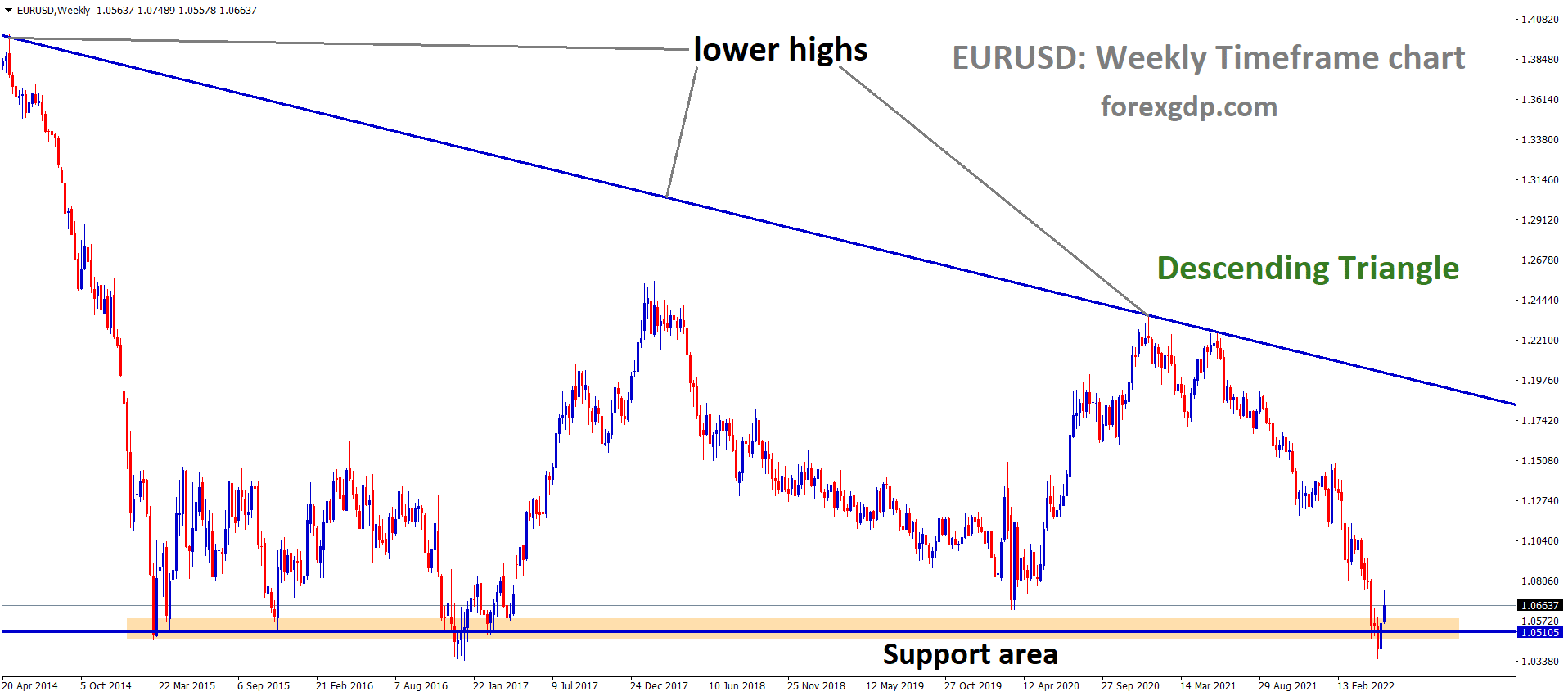

EURUSD is moving in a ascending channel and the market has fallen from the higher high area of the channel

The slowest pace of employment growth in two-and-a-half years in June might have persisted in July, raising concerns about the broader economic recovery.

4) Impact on the US Dollar: ISM PMIs

4.1 Importance of ISM PMIs

In addition to the nonfarm payrolls report, the market will closely monitor the Institute for Supply Management (ISM) Purchasing Managers’ Index (PMI) for the manufacturing and non-manufacturing sectors.

NZDUSD is moving in a descending channel and the market has reached the lower low area of the channel

These readings carry significant weight in shaping the US dollar’s movement.

4.2 Manufacturing vs. Services

While the US manufacturing sector has experienced recessionary pressures, the services economy has continued to expand, as seen from the unexpected bounce in the non-manufacturing PMI in June. The disparity in these sectors could lead to divergent expectations for the US dollar.

Conclusion

The July nonfarm payrolls report is poised to provide crucial insights into the resilience of the US economy amidst inflationary pressures and ongoing economic challenges. Market sentiment will be influenced by the report’s figures, with a focus on the Federal Reserve’s potential actions in the upcoming September meeting. Additionally, the performance of the US dollar will also be driven by the ISM PMI readings, reflecting the contrasting trends in the manufacturing and services sectors. As the Fed’s historic tightening campaign appears to be winding down, market participants will closely scrutinize economic indicators to navigate the evolving economic landscape.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/