USD: JPMorgan research head says immigration is boosting US economy, ‘really underestimated’

FED is projected GDP for 2024 is 2.1% it is up from 1.6% predicted in December 2023. JP Morgan Brokerge company said 6 million immigration of population increased in past 2 years in the US. So Unemployment rate low level is a welcome one. US Dollar staying stronger for long term, This year election spending also in the table. Lowering rates will support economy to drive faster than now, inflation also keeps higher.

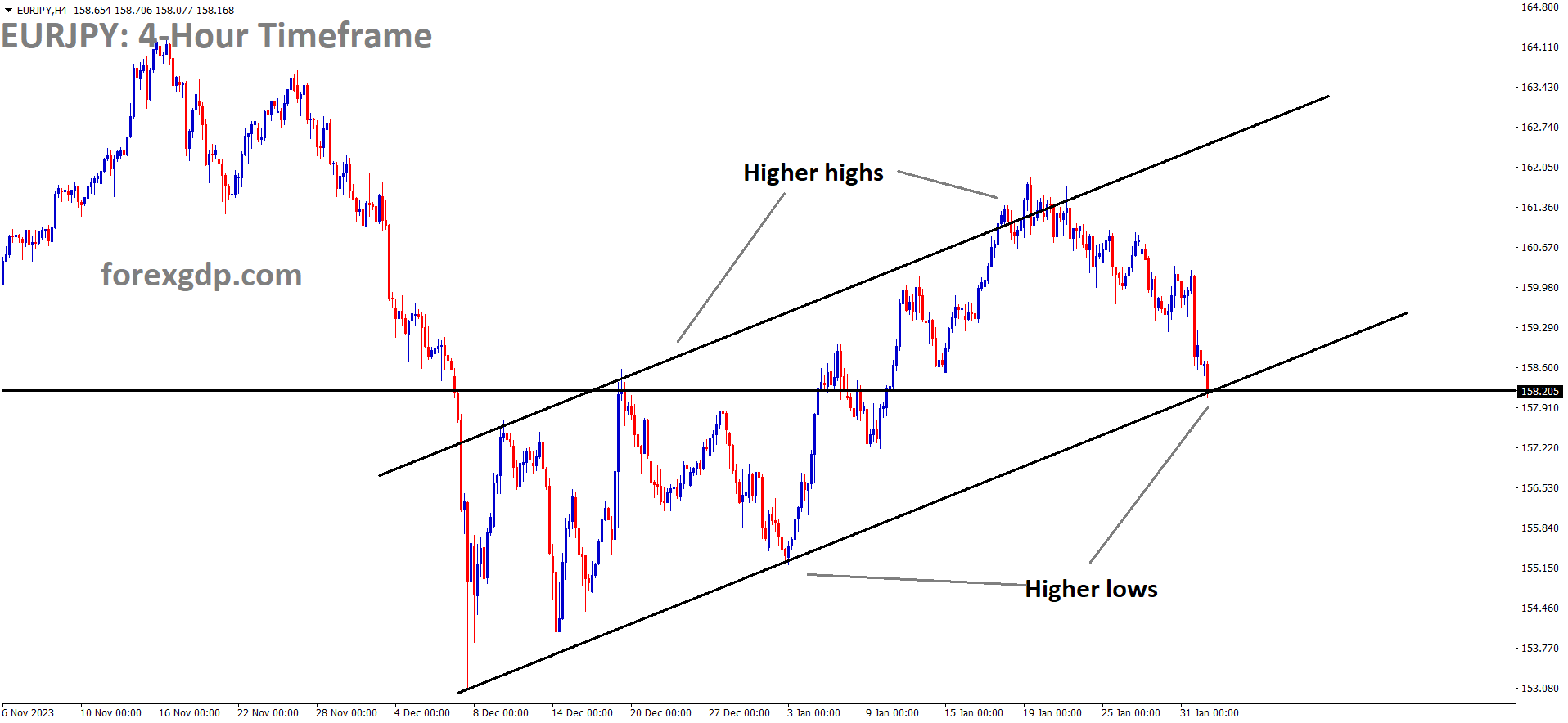

USDCHF is moving in Descending channel and market has reached lower high area of the channel

JPMorgan’s Joyce Chang highlights the underestimated role of immigration in bolstering the US economy amid global challenges. Despite the Federal Reserve’s revised GDP growth projection to 2.1% for 2024, indicating economic resilience, Chang emphasizes the positive impact of immigration on consumption and low unemployment rates.

Chang notes that the recent surge in immigration, contributing to a nearly 6 million increase in the US population, has significantly boosted consumption. This growth in population has played a crucial role in maintaining low unemployment figures.

While acknowledging the upward pressure on wages and housing costs, Chang warns that the Fed still faces challenges in controlling inflation. The Congressional Budget Office estimates consistent levels of net immigration, with projections indicating its ongoing contribution to economic growth.

Although immigration remains a contentious political issue, Chang argues that, economically, it’s beneficial, generating revenues that surpass expenses. She emphasizes that the US’s high fiscal deficit, energy independence, and sustained government spending further support its economic outlook.

In light of these factors, JPMorgan predicts a cautious approach from the Fed, with inflationary pressures likely to persist amid continued government spending and immigration, suggesting a “shallow” loosening cycle.

GBP: Upcoming: US & UK GDP

This week GBP Q4 GDP is projected to -0.20% in YOY and -0.30% in QoQ from 0.30% and -0.10% in the previous reading respectively. Already BoE made no rate cuts in this month meeting makes GBP plunged against USD. Data shows declining growth is expected after the higher rates persists in the UK economy.

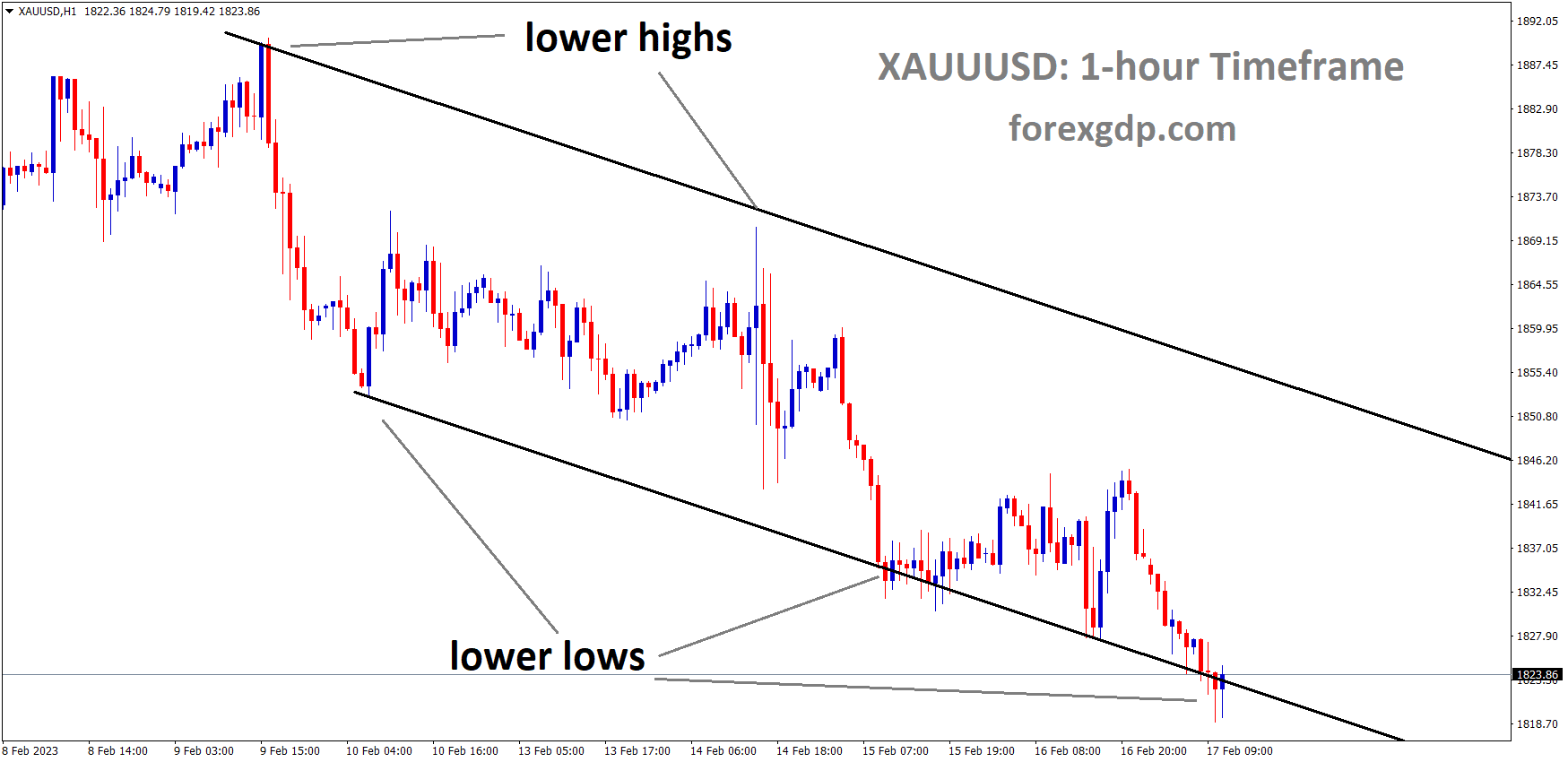

GBPUSD is moving in descending channel and market has reached lower low area of the channel

US & UK GDP

On Thursday, March 28th, both the US and UK will unveil their revisions for fourth-quarter GDP. In the US, GDP is forecasted to remain steady at 3.2%. While these figures may not significantly sway markets unless there’s a substantial revision, attention will be on the core PCE price index within the GDP data. The recent revision indicated a 2.1% increase in core PCE quarter on quarter (q/q). If there’s an upward adjustment, it could signal that inflation isn’t receding as fast as the Fed expects, potentially impacting short-term rates and strengthening the US dollar.

In the UK, the last GDP release showed a 0.3% contraction q/q and a 0.2% decline y/y. Any downward revisions might further weaken the pound, prompting markets to anticipate earlier rate cuts. The pound saw significant turbulence following the Bank of England’s recent rate decision, with GBP/USD edging closer to support at 1.263. A breach of this level could trigger a further decline toward 1.25.

USD: USD Weekly Forecast: Inflation Resurfaces

The FED is projected Core PCE index for 2024 is 2.5-2.6% from 2.4%-2.5% projected in the previous meeting. This week Core PCE index is the major support for FED rate cuts in upcoming meetings.

USD INDEX is moving in box pattern and market has rebounded from the support area of the pattern

Weekly Greenback Gain Driven by Yen Sell-Off; Fed Eyes June Rate Cut

The recent rise in the US Dollar (Greenback) was not solely fueled by an increase in US yields but also by a significant decline in the Japanese Yen, amplified by the Bank of Japan’s dovish stance earlier in the week.

Federal Reserve (Fed) Meeting Impact:

During the Federal Open Market Committee (FOMC) meeting on March 20, the Fed held its fed funds target range as expected but raised its core Personal Consumption Expenditures (PCE) projections for 2024. Despite inflation running above targets, the Fed is confident it will eventually stabilize. Chair Jerome Powell hinted at potential rate cuts later in the year.

Potential Rate Cuts:

Looking ahead, if US inflation drops faster in the coming months and the labor market cools further, the Fed may start its easing cycle sooner, possibly in May.

Market Focus:

Investors are awaiting the release of US inflation data, particularly the Personal Consumption Expenditures (PCE) figures. Other key data includes GDP growth, Durable Goods Orders, Initial Jobless Claims, and the Michigan Consumer Sentiment Index.

Currency Outlook:

Among G10 central banks, the Fed, European Central Bank (ECB), and possibly the Bank of England (BoE) are expected to ease rates, while the Reserve Bank of Australia (RBA) may follow later in the year. Despite the Bank of Japan’s recent rate hike, the Dollar is expected to remain strong against its counterparts, especially the Euro.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/