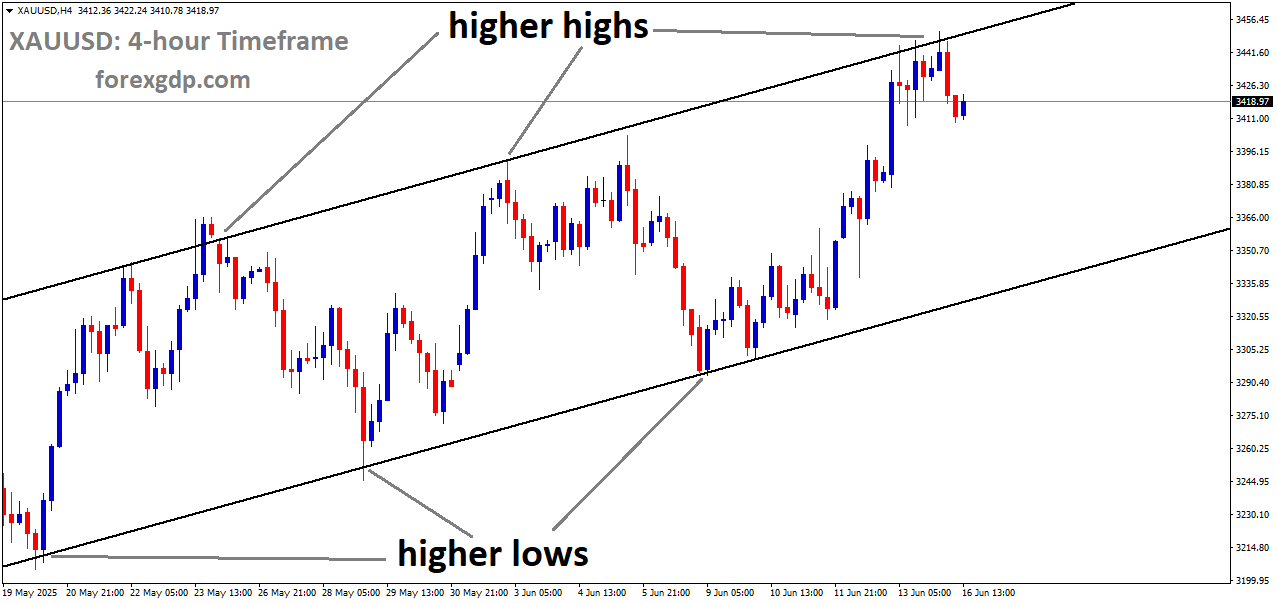

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Due to lower-than-expected US jobless reports, gold prices rose to $2000 yesterday. The likelihood of the US FED raising rates is lower than normal, and the US dollar falls against other currency pairs. The US collapse of medium-sized banks causes investors to lose confidence in the dollar and redirects their greed towards gold.

After the FOMC announced a dovish interest rate hike and hinted that its tightening campaign may be coming to an end, gold prices rose on Thursday amid a weaker U.S. currency. In late morning trading, the XAU/USD currency pair was up slightly by 1% to $1,986, edging closer to its 2023 highs and just above the psychological $2,000 level established on Monday. The Fed is now taking a much more cautious posture and projecting a less aggressive hiking cycle than it did just a few weeks ago, when Powell dropped a hawkish bombshell before Congress. This is a result of recent turmoil in the banking sector. In reality, the FOMC only anticipates raising borrowing costs once more this year, to 5.00-5.25%, a significant decrease from the highest rate of 5.70% that the market had earlier this month forecast.

It is likely to be positive for non-yielding assets, such as precious metals, that the terminal rate is within reach and that there is increasing speculation that the central bank will ease policy soon after. This suggests that gold may continue to rise over the medium term, particularly if financial instability reappears and poses a danger to the system. Technically speaking, if gold continues to progress in the ensuing sessions, the first ceiling to take into account is in the $2,000–$2,015 range. On sustained strength and a clear breakthrough, attention will turn to channel resistance at $2,050, then to $2,078, the high from the previous year. On the other hand, if buyers come back and cause a pullback, early support is found at $1,975/$1,965. The region of interest below that is at $1,920, and it continues at $1,900.

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has reached the lower low area of the channel.

Below is a collection of Japanese CPI predictions made by Four Banks.

Compared to 4.3% in January, Standard Chartered predicted 3.3% YoY growth.

ING projected 3.5% YoY compared to January’s 4.3%.

Compared to January’s 4.2%, SocGen predicted a 3.2% CPI YoY.

In contrast to January’s 4.2%, Citibank predicted 3.1%.

If today’s CPI results are lower than anticipated or higher than predicted, the Japanese Yen may strengthen.

The Federal Reserve continued to extend large amounts of credit to the financial system, which now includes official foreign borrowing, late Thursday, according to a Reuters report. Emergency lending to banks, which reached record levels the previous week, stayed high in the most recent week. The total size of its balance sheet increased from $8.7 trillion the previous week to $8.8 trillion as a result of borrowing from the Fed.Discount window borrowing, the Fed’s primary source of emergency credit to depository institutions, decreased from the $152.9 billion recorded last week to $110.2 billion as of Wednesday. The level reached last week increased from $4.6 billion on March 8 to smash the previous high of $112 billion established in the fall of 2008, the most dangerous time of the global financial crisis.

Additionally, the Fed stated that lending to foreign central banks and monetary authorities increased from zero on March 15 to $60 billion on Wednesday. Recently, a number of significant central banks declared they would use the Fed’s dollar liquidity as required. The Fed believes that the increase from last week has no impact on monetary policy, but it has been working since last summer to reduce the size of its stockpile of cash and bonds, which peaked at just short of $9 trillion during the summer. The Federal Reserve’s $142.8 billion credit to the Federal Deposit Insurance Corporation for handling the failing California banks increased further, reaching $179.8 billion, according to statistics from the Fed.

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern.

After oil prices continued to fall due to slowing global demand, the Canadian dollar continued to fall.

Due to the US and Swiss bank failures, credit is becoming more limited for households and businesses, which will result in a decline in fuel consumption.

The Bank of Canada is more likely to maintain rates low or unchanged if the CAD CPI came in lower than anticipated.

The USDCAD pair fails to take advantage of the previous day’s solid recovery from the 1.3630 area, or more than a two-week low, and oscillates in a constrained trading band through Friday’s early European session. Despite the pair’s present placement just above the 1.3700 level, several factors prevent any appreciable upward movement. Fears that escalating conflict in the Middle East could interrupt supply have led to a rebound in crude oil prices, particularly following a US airstrike on organisations with Iranian support. A headwind for the USD/CAD combination is created by the commodity-linked Loonie and the quiet price movement of the US Dollar as a result. The Greenback’s overnight recovery from its lowest level since February 2003 is not sustained by the Federal Reserve’s suggestion of a pause in interest rate increases.

Crude Oil Analysis

Crude Oil price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Recall that the US central bank increased interest rates on Wednesday by 25 basis points, as was generally expected, but sounded cautious about the outlook in light of the recent turmoil in the banking sector. This follows the sudden demise of two mid-sized US institutions, Silicon Valley Bank and Signature Bank, just recently. Additionally, the Fed reduced its median estimate for real GDP growth for 2023 and 2024, which keeps the yield on US Treasury bonds low and the USD weak. In addition to this, a generally upbeat atmosphere in the equity markets is considered to be another reason harming the safe-haven dollar. Nevertheless, growing market apprehensions that sluggish economic expansion will reduce fuel consumption should limit the rise in oil prices. The softer-than-expected Canadian consumer inflation reported on Tuesday, along with predictions that the Bank of Canada will hold off on raising interest rates further, should support the USDCAD pair.

Technically speaking, the two-way price movements within a well-known band seen since the start of the current week indicate uncertainty among traders regarding the near-term trajectory. Furthermore, before making aggressive directional bets on the USD/CAD pair, exercise some caution given the previously stated mixed fundamental backdrop. Additionally, investors appear uneasy ahead of crucial macroeconomic data coming later in the early North American session from the US and Canada. The release of Durable Goods Orders and the flash PMI prints, along with US bond yields and the general risk mood, will all have an impact on the USD demand on Friday’s US economic calendar. Traders will also observe data on Canadian monthly retail sales. In addition, the USD/CAD pair should receive a new boost from oil price dynamics on Friday, creating short-term trading chances.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

SNB A further rate increase is anticipated in June month, bringing the rate increase since COVID-19 to four months in a row and 50bps to 1.50%.

Thomas Jordan, the chairman of the SNB, stated that the bankruptcy of Credit Suisse does not imply that we were careless on our part; the problem was stopped as soon as it started. Credit Suisse received more liquidity from SNB, and FINMA and FED both contributed significantly more to this problem.

As it continues its four-day losing run early on Friday ahead of the important US data, the USDCHF makes a new intraday low near 0.9160. Thus, amid a slow end to the volatile week, the Swiss Franc (CHF) pair supports hawkish bias surrounding the Swiss National Bank (SNB) versus dovish bets on the Federal Reserve’s next move. As generally anticipated, the SNB increased its benchmark sight deposit interest rate on Thursday from 1.0% to 1.50%. The markets now anticipate that the final rate increase will occur in June as the SNB increases rates for the fourth consecutive meeting.

Thomas Jordan, the chairman of the SNB, stated that additional rate increases cannot be counted out in order to maintain price stability after the interest rate announcements. The decision-maker added that it would have been reckless to take a chance on a Credit Suisse bankruptcy while stating that the crisis has been stopped thanks to actions done by the federal government, FINMA, and SNB. Andrea Maechler, a member of the SNB governing board, also made a statement on Thursday, stating that the failure of Silicon Valley Bank had significantly raised tension on the financial markets. In other places, the Fed’s aggressive lending amid the banking crisis raises concerns about an expanding Fed balance sheet, which in turn prompts fresh calls from hawks for the US central bank to take action. The conflicting US statistics and the most recent Fed statement, however, seem to put the policy hawks on the defensive. Key market participants’ remarks, such as DoubleLine’s Gundlach’s recent reiteration of his dovish stance for the US central banks, may also pose a threat to the US Dollar.

It’s important to note that the Basel Committee on Banking Supervision’s Chair and US Treasury Secretary Janet Yellen’s remarks also influence the market’s attitude and put the USD/CHF bears on the defensive. The recent decline in yields, however, gives the pair sellers confidence. According to a recent article in The Financial Times, Pablo Hernández de Cos, the head of the world’s top financial regulator, has advocated for stricter regulations to prevent risks from spreading from so-called “shadow banks” to other components of the banking system. As an alternative, China and Russia may want to create a currency that isn’t the US dollar, according to US Treasury Secretary Janet Yellen, who also said that they should be ready to take additional deposit measures “if warranted.” However, in February, the US Chicago Fed National Activity Index (CFNAI) decreased to -0.19 from the previous month’s 0.23 and the 0.0 forecast. Furthermore, compared to the prior week’s 192K claims and the 203K market expectations, weekly initial jobless claims decreased to 191K for the week concluded March 18. It should be noted that the Kansas Fed Manufacturing Index for March increased to 3.0 from -9.0 prior and 6.0 expected, while US New Home Sales climbed 1.1% in February from 1.8% prior and 1.6% analysts’ estimates.

In light of this, the US 10-year and two-year Treasury note yields are still low by press time, at 3.38% and 3.78%, respectively, while the S&P 500 Futures find it difficult to mimic the gains made on Wall Street. Future US S&P Global PMI readings for March and Durable Goods Orders for February will be vital for traders of the USD/CHF pair to monitor for clear trends.

USD Index Analysis

US Dollar index has broken the Descending channel in upside.

The FED Powell statement that they have a plan for no rate change to do this month due to bank failure, but the economy condition to keep tight, that’s why we do rate change in this meeting, caused the US Dollar index to fall to a seven-week low.

Since the FED’s goal inflation rate is 2%, a rate hike is implemented at this meeting despite the fact that tight businesses and households will cause an economic recession.

The Federal Reserve has likely increased interest rates for the final time in its fight against inflation that is higher than its target rate, according to the most recent Fed Fund rate probabilities. Chair Powell claimed that the FOMC had considered leaving interest rates unchanged yesterday in light of the recent banking crisis, despite the fact that these probabilities are constantly shifting and inflation is still uncomfortably high and sticky. Chair Powell stated that the Committee will continue to watch the implications of new information for the economic outlook when determining the proper stance of monetary policy.

If risks arise that could obstruct the Committee’s objectives, the Committee would be prepared to modify the stance of monetary policy as necessary. While chair Powell continued to emphasise that the Fed’s 2% inflation goal would be the focus of monetary policy, he also noted that tighter credit conditions for individuals and businesses would have an impact on the economy. It is too soon to say how monetary policy should react because it is too soon to know the full extent of these impacts. Because of this, we no longer predict that ongoing rate increases will be necessary to control inflation; rather, we now predict that some extra policy firming may be necessary.

Traders now believe that US interest rates are at, or are very close to, their cycle peak, which has contributed to the US dollar weakening. Despite this small change in language, the Fed still has plenty of room to act if necessary. After the FOMC ruling, US Treasury yields decreased, with the rate-sensitive US 2-year trading back below 4%. The US dollar indicator is testing levels last seen almost two months ago as it drops back below 103. The dollar is attempting to recover some of its post-FOMC losses from Wednesday, but the chart still appears heavy and pointing downward. The most recent US unemployment applications are due later today, which will provide an update on the health of the labour market. At noon, the Bank of England will announce its most recent monetary policy, and the US dollar gauge will be impacted by any hawkish language or twists from the UK central bank.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to increased wage pressure and inflation rates, the ECB will implement large rate increases in the future months.

Fears of a bank failure and higher inflation are putting pressure on the US FED, Bank of England, and RBA to raise interest rates.

The ECB has already stated that there is sufficient liquidity to withstand any bank default or lending preference.

In the Tokyo session, the EURUSD pair is moving back and forth around 1.0830. The significant currency pair is anticipated to maintain its downward trajectory towards the 1.0800 level support. The US Dollar Index has demonstrated a substantial recovery, strengthening the shared currency pair’s tendency to the downside. After a recovery move on Thursday supported by Janet Yellen, the US Treasury Secretary, restoring investors’ trust and portraying some optimism in US equities, S&P500 futures have remained silent. As other western central banks imitate the Federal Reserve, the US Dollar Index has continued to rise, approaching 102.70.

In order to prevent a worsening of the banking problem, Fed chair Jerome Powell gave indications on Wednesday at the monetary policy meeting that the rate-hiking binge that has lasted a year would be coming to an end. Additionally, there is less room for rate increases now that they have hit a certain level. Similar to the Fed, the Reserve Bank of Australia and the Bank of England are considering pausing the rate-hiking trend. Due to the USD Index’s appeal as a secure haven, the market has recovered. In the meantime, as investors rejoiced that the Fed is halting rate increases sooner, demand for US government bonds increased further. The return given on 10-year US Treasury yields has been reduced below 3.4% due to increased demand for US bonds.

Future preliminary S&P Global Eurozone/US PMI releases will be closely monitored. Both countries are predicted to perform inconsistently. Contrary to other countries, the Eurozone still favours larger rate increases because there is still more room for the European Central Bank to manoeuvre. Additionally, because of strong wage constraints, core inflation is very stubborn. According to ECB policymaker Klaas Knot, rate increases are unlikely to end for the central bank, and they still believe that May’s policy rate increase is necessary.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The UK pound gained against the news after the Bank of England raised rates by 25 basis points yesterday.

In contrast to forecasts of 6.2%, the UK CPI is predicted to be 5.6% in 2023. As prices in the hospitality industry rise, inflation increases.

The Bank of England and the UK government are currently seeking additional rate increases to lower inflation in 2023.

The Bank of England increased interest rates by 25 basis points as anticipated, despite votes to maintain rates by BoE policymakers Tenreyro and Dhingra. The BoE expressed their opinion that the recent rise in inflation data may not be sustained and stated that Q2 CPI is likely to be lower than predicted in February due to longer energy price caps and lower wholesale prices. Unpredictable garment costs were blamed for February’s high core goods prices. The Central Bank predicts that wage growth will slow down more quickly than expected in February as businesses anticipate year-ahead inflation to be 5.6% for the three months ending in February 2023 rather than 6.2% for the three months ending in November 2022. If there were indications of more sustained price pressures, the BoE said that further tightening of monetary policy would be required.

Regarding the recent turmoil in the banking industry, the BoE believes that the UK banking system has strong capital and liquidity, which has contributed to its resilience during the fallout. The macroeconomic and inflation outlook will continue to be carefully watched by the MPC for any impacts on the credit conditions that people and businesses face. The MPC estimates that the recent support measures included in the spring budget could raise GDP by 0.3% over the ensuing years. However, the precise impact, especially in relation to supply and demand, will be evaluated prior to the May Monetary Policy Report. The Bank of England (BoE) came under significant pressure as a result of this week’s UK inflation data because the hospitality industry continues to experience especially sticky inflation. The Bank of England’s own Decision Maker Panel poll of businesses, which indicates that less aggressive price and wage increases are coming, is the only encouraging sign for the UK and the Bank of England with regard to inflation. Additionally, the official wage data finally seems to be steadily decreasing. The Decision Maker Panel data, which was published today, verified this and predicted that inflation would peak at 5.6% in 2023 rather than the 6.2% previously predicted. If the hospitality industry’s prices continue to rise noticeably, however, even this and reduced gas prices won’t be able to reduce inflation.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Australian PMI for March is less than 50.00, manufacturing gauge is 48.7 vs. 50.3 expected, and services PMI dropped from 50.7 to 48.2 in contraction.

Following the announcement of the news, the Australian Dollar fell against the US Dollar today.

While preparing for the weekly loss early on Friday, AUDUSD records its first daily loss in three days around 0.6670. The Australian couple thereby defends its risk barometer status as well as the negative activity statistics at home. Preliminary March S&P Global PMI readings for Australia fell below market expectations and earlier readings earlier in the day, entering the recession zone of under 50.00. On the other hand, the Services PMI fell to 48.2 from 50.7 previous readings and 49.7 market expectations, while the Manufacturing gauge fell to 48.7 from 50.3 expected and 50.7 prior. As a result, the Composite PMI decreased from 50.6 to 48.1. In other news, concerns over the Fed’s ballooning balance sheet prompt more hawkish calls for the US central banks, and the turmoil in the world financial system adds to the pressure, causing the US dollar to lick its wounds close to a seven-week low. However, despite recovering from a seven-week low the previous day, the US Dollar Index (DXY) remains bearish near 102.60 as of press time, while the rates on US 10-year and two-year Treasury bonds are still low at 3.39% and 3.80%, respectively. The S&P 500 Futures fail to replicate Wall Street’s positive actions while portraying the mood.

Along with the Fed’s wagers, remarks from the Basel Committee on Banking Supervision Chair and US Treasury Secretary Janet Yellen also influence the market’s sentiment and support AUD/USD sellers. Janet Yellen, the secretary of the US Treasury, stated on Thursday that “China and Russia may want to develop an alternative to the US dollar” and that she was ready to take additional deposit measures “if warranted.” On the other hand, the Financial Times reported that Pablo Hernández de Cos, the head of the world’s top financial regulator, has asked for stricter regulations to stifle risks that could spread from so-called “shadow banks” to other components of the banking system. Speaking of statistics, the US Chicago Fed National Activity Index fell to -0.19 in February compared to a 0.23 reading the month before and a 0.0 expectation. Furthermore, compared to the prior week’s 192K claims and the 203K market expectations, weekly initial jobless claims decreased to 191K for the week concluded March 18. It should be noted that the Kansas Fed Manufacturing Index for March increased to 3.0 from -9.0 prior and 6.0 expected, while US New Home Sales climbed 1.1% in February from 1.8% prior and 1.6% analysts’ estimates.

NZDUSD Analysis

NZDUSD is moving in an Ascending triangle pattern and the market has reached the higher low area of the pattern.

Due to the fact that inflation in the New Zealand economy has not decreased as of late, the RBNZ will increase rates once more at its upcoming meeting.

The growing trade imbalance causes New Zealand’s economy to see lower exports and higher imports. China’s return from COVID-19 is crucial for New Zealand’s export growth.

In the early Asian session, the corrective move below 0.6250 on the NZDUSD pair is beginning to show symptoms of exhaustion. Late on Thursday, the Kiwi commodity showed a downward movement after the US Dollar Index recovered from 102.00. Investors are cheering signs of a policy-tightening end that were recovered from Federal Reserve head Jerome Powell’s commentary, which is why the market tone is still positive. Investors took Fed Powell’s remark that some additional policy firming may be appropriate as good news. The Fed is probably just one rate increase away from reaching the terminal rate, but the fight against persistent US inflation will go on until the Consumer Price Index softens to 2%.

As US Treasury Secretary Janet Yellen stated that the government is “prepared for additional deposits actions if warranted,” S&P500 futures have carried forward their favourable move in early Asia. Participants in the market now feel more confident thanks to the expanding insurance coverage for investments. The US Dollar Index has recovered to almost 102.60, but it still faces challenging obstacles. Since the Fed is unwilling to consider rate cuts this year and since US banks are imposing strict credit conditions on consumers and businesses, the US inflation would be under double assault from now on. This would lead to a decline in demand, weaker economic activity, and a lowering of inflation.

Future S&P Global PMI (March) preliminary data will be closely monitored. The Manufacturing PMI is predicted to decrease from the previous report of 47.3 to 47.0. And the Service PMI, which had previously been released at 50.6, may decline to 50.5. Weaker-than-expected PMI data could have a bigger effect on the USD Index. The Reserve Bank of New Zealand’s (RBNZ) fight against inflation is far from over, so the New Zealand Dollar is anticipated to strengthen going forward. The RBNZ will likely increase rates again since New Zealand inflation hasn’t significantly slowed down yet.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/