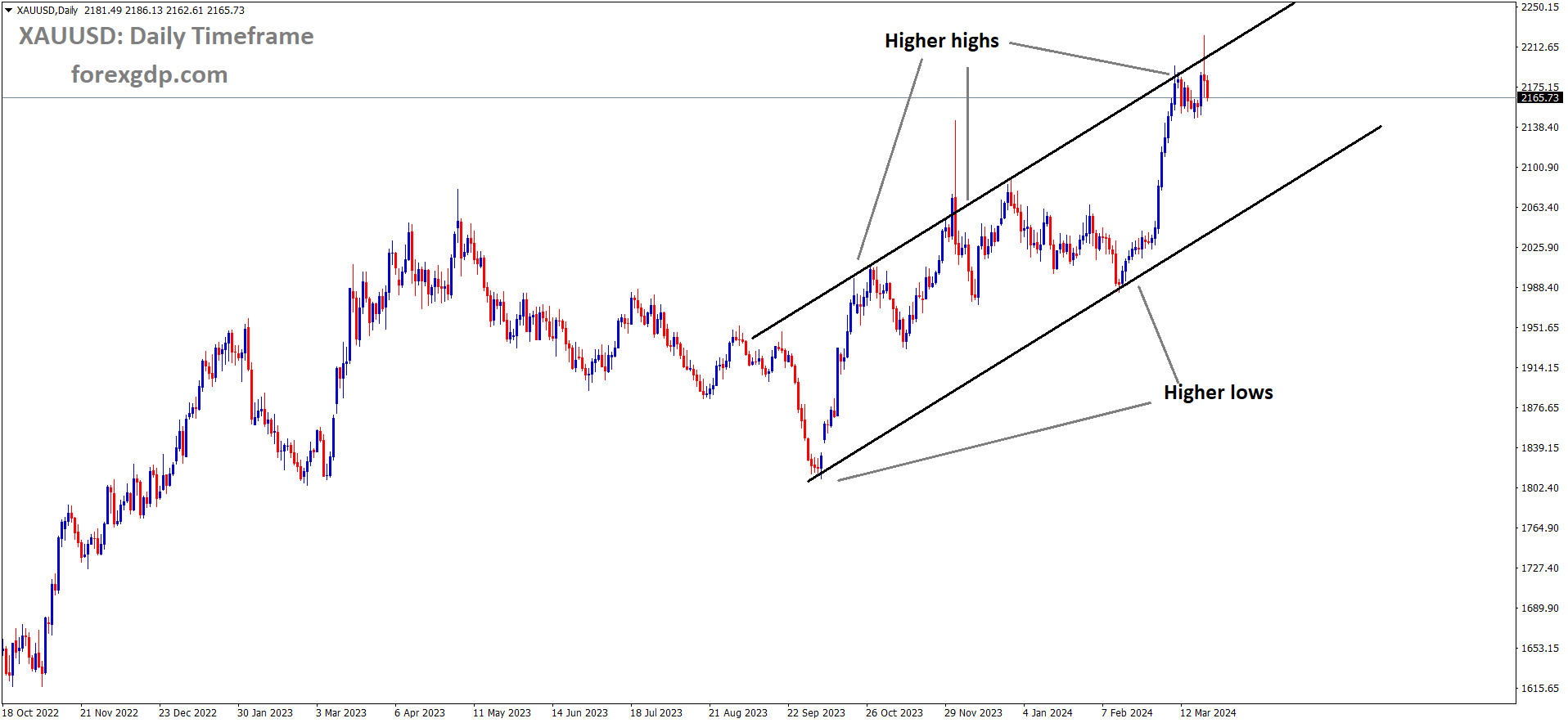

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

XAUUSD – GOLD Price Stays Weak with Modest USD Strength, Bearish Sentiment Weak

The Gold prices are falling after the US Secretary of State Anthony Blinken said ongoing talks of Ceasefire between Gaza and Israel is narrowing, it is positive for Investors confidence. So Fears are away from the market makes Gold prices moved lower against USD.

Gold (XAU/USD) remains subdued, trading around $2,175 amid modest USD strength and optimistic US economic outlook. The US Dollar’s solid bounce from a one-week low, along with elevated US Treasury bond yields and positive global financial markets, undermines the safe-haven metal.

However, any significant decline in gold prices is limited due to the Federal Reserve’s projection of a less restrictive policy stance, including a potential 75 basis point interest rate cut this year. This could lower US bond yields, capping gains for the USD and supporting non-yielding gold prices.

Market focus shifts to Fed Chair Jerome Powell’s speech during the early North American session for further direction. US bond yields and broader risk sentiment will also influence gold price dynamics, offering short-term trading opportunities.

Despite current pressures, XAU/USD is poised to end the week positively for the fourth time in five weeks.

Additionally, the Federal Reserve’s upgraded economic growth projection, higher core inflation forecast, and lower unemployment rate outlook support elevated US Treasury bond yields, potentially boosting the USD. However, expectations of a less restrictive policy may limit USD upside.

On the economic front, US Initial Jobless Claims fell to 210K, signaling a strengthening labor market. Positive developments in ceasefire talks in Gaza also boost investor confidence.

Powell’s speech is awaited for insights into future policy decisions, providing fresh impetus to XAU/USD trading.

EURUSD – Returns to Consolidation Levels After Brief Rally

The Euro currency moved lower against USD after the mixed bag of Euro zone data printed.

EURUSD has broken the Ascending channel in downside

EURUSD has broken the Ascending channel in downside

German manufacturing PMI came at five month low of 41.6, Services PMI came at 49.8. US Side having strong Manufacturing, Services PMI data reading printed last day.

EUR/USD Retreats to Familiar Levels Amid Mixed Data

On Thursday, the EUR/USD pair plunged by three-quarters of a percent, settling near 1.0850, retracing its Wednesday rally driven by the Fed’s actions. This movement indicates a return to familiar consolidation levels, marking a whipsaw effect rather than a sustained break in market sentiment.

The Euro (EUR) faced early downward pressure on Thursday after mixed European Purchasing Managers Index (PMI) figures. German Manufacturing PMI hit a five-month low of 41.6, while the Services PMI exceeded expectations at 49.8, inching closer to positive territory.

![]()

In the US, March’s S&P Global Composite PMI slightly declined to 52.2, with the Services PMI falling more than anticipated to 51.7.

Friday’s agenda includes German IFO Expectations, expected to improve slightly, and a series of Federal Reserve board member speeches, headlined by Fed Chairman Jerome Powell.

USDJPY – Japan’s February CPI rises to 2.8% YoY from 2.2% prior

The Headline CPI data of Japan came at 2.8% in February month from 2.2% printed in Previous month. This reading came above the BoJ target of inflation 2%. Just two days back hiked 10bps by BoJ, inflation reading come well above 2% target. Wage hike increased and coming months personal consumption will be increased then inflation also increased with Wage hikes pressures.

USDJPY is moving in an Ascending trend line and the market has reached the higher low area of the trend line

In February, Japan’s CPI rose to 2.8% YoY from January’s 2.2%, as per the latest data from the Japan Statistics Bureau. Excluding fresh food, the National CPI reached 2.8% YoY in January, aligning with market expectations.

USDCHF – Climbs Below 0.9000 on Strong Dollar, SNB Rate Cut

USDCHF climbed higher after the SNB do rate cuts of 25bps last day. First central bank was initiated steps for rate cuts after the inflation reading come to under 2% target of SNB.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Next week Swiss ZEW survey ( March) and Swiss Q1 bulletin of 2024 is scheduled.

USD/CHF Rises Below 0.9000 as SNB Cuts Rates

During the early European session on Friday, the USD/CHF pair gained momentum below the 0.9000 psychological level. The Swiss Franc (CHF) experienced selling pressure following a surprise rate cut by the Swiss National Bank (SNB), reducing its main interest rate by 25 basis points to 1.50%.

At present, USD/CHF is trading at 0.8990, marking a 0.15% increase for the day.

The SNB’s decision to lower interest rates to 1.50% came after Swiss inflation fell to 1.2% in February, below the SNB’s target range of 0-2%. This unexpected rate cut exerted downward pressure on the CHF, benefiting the USD/CHF pair.

Meanwhile, the US Federal Reserve (Fed) kept its benchmark interest rate unchanged, maintaining its outlook for three rate cuts this year. Fed Chairman Jerome Powell emphasized that despite upside surprises in US inflation data for January and February, the overall narrative remains that inflation is gradually returning to its 2% target.

Recent data showed that the US S&P Global Manufacturing PMI exceeded expectations, rising to 52.5 in March, while the Services PMI decreased to 51.7, slightly below estimates. The Composite PMI for March stood at 52.2.

Investors are anticipating Federal Reserve Chair Jerome Powell’s speech on Friday for insights into inflation and monetary policy. Additionally, upcoming releases next week include the Swiss ZEW Survey for March and the SNB Quarterly Bulletin for Q1 2024, alongside US Gross Domestic Product Annualized (GDP) for Q4.

USDCAD – Weak Above 1.3500, Awaits Canadian Retail Sales

The Canadian retail sales data for the month of February is scheduled today and expected -0.40% reading today. The BoC Governor did not take immediate rate cuts based on the recent data cycle. He has to conclude atleast 2 quarters data to fix the rate cut in the monetary policy settings.

USDCAD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

USD/CAD Dips Above 1.3500, Eyes on Canadian Retail Sales

During early Asian trading hours on Friday, the USD/CAD pair trades weaker above the 1.3500 mark, standing at 1.3523, down 0.05% for the day. The decline in the US Dollar below 104.00 adds pressure to the pair.

The Federal Reserve (Fed) held interest rates steady at its March meeting and maintained its projection for three rate cuts this year. Fed Chair Jerome Powell emphasized that a strong job market wouldn’t prevent the central bank from cutting rates.

On Thursday, the US S&P Global Manufacturing PMI rose to 52.5 in March, surpassing expectations, while the Services PMI eased to 51.7, slightly below consensus. Canadian Retail Sales data for January, expected to decline by 0.4% MoM, is awaited on Friday.

Regarding the Loonie, the Bank of Canada (BoC) indicated potential rate cuts this year if the economy follows projections, but the timing remains uncertain. BoC Governor Tiff Macklem emphasized the importance of not moving too quickly.

Later on Friday, speeches by Fed Chair Jerome Powell and Michael Barr are anticipated.

USD INDEX – Greenback Rises on Solid Labor Data, Mixed PMIs

US Manufacturing PMI data came at 52.5 in February from 52.2 in January, services PMI data came at 51.7 from 52.3. The Initial Jobless claims data came at 210K versus 215K printed in last week. The Composite PMI data came at 52.5 from 52.2 in the last month.US Dollar soaring against counter pairs after the positive data readings printed.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

USD Index Up 0.50% at 103.80, Rebounding from Wednesday’s Losses

The US Dollar Index (DXY) is trading at 103.80, up 0.50%, recovering most of Wednesday’s losses. The Greenback strengthened on mixed S&P preliminary PMIs from March and robust weekly Jobless Claims.

The prevailing expectation is for an easing cycle to commence in June, with the timing of subsequent cuts dependent on incoming data. Despite recent high inflation figures, the Federal Reserve revised its inflation projections upward. However, Fed Chair Jerome Powell assured that the central bank would not overreact, adopting a more dovish stance towards rates. The Dot Plot indicated that the median rate prediction by year-end remains at 4.6%.

In other news, S&P Global’s initial Purchasing Managers Survey for March revealed a slight decrease in Services PMI but an increase in Manufacturing PMI. Initial Jobless Claims for the week ending March 15 were lower than expected at 210K.

Post-FOMC, US Treasury bond yields are on the rise, with the 2-year yield at 4.59%, the 5-year at 4.25%, and the 10-year at 4.27%.

GBPUSD – UK Retail Sales Flat at 0% MoM in February vs. -0.3% Expected

The UK Retail sales for the month of February came at no growth versus -0.30% expected and 3.6% printed in January month. Core retail sales came at 0.20% versus -0.10% expected and 3.4% in January month. GBP moved lower after the lower retail sales data printed today.

GBPUSD is moving in the Box pattern and the market has fallen from the resistance area of the pattern

UK Retail Sales Unchanged in February: ONS

According to the Office for National Statistics (ONS), UK Retail Sales remained stagnant in February, in contrast to an expected -0.3% decline and the 3.6% increase recorded in January.

Core Retail Sales, excluding auto motor fuel sales, edged up by 0.2% MoM, surpassing expectations of -0.1% and the 3.4% figure from January.

Annual Retail Sales in the UK fell by 0.4% in February, better than the expected -0.7% decrease, while Core Retail Sales also declined by 0.5% during the month, compared to the forecasted -0.9% and the previous 0.5%.

AUDUSD – AUD Weakens Amid Stronger USD, Eyes on Fed Chair Powell

The Australian Dollar moved lower after the stronger data printed from Australian economy last day and FED Powell monetary settings favoured for Australian Dollar. The news impact made higher Australian Dollar against counter pairs last 2 days. JUDO Bank Services PMI shows 53.5 from 53.1 and Composite PMI increased to 52.4 from 52.1.

AUDUSD is moving in the Descending channel and the market has reached the lower low area of the channel

The Australian Dollar (AUD) experienced a decline for the second consecutive session on Friday. This decline was attributed to the strengthening of the US Dollar (USD) following mixed data from the S&P preliminary Purchasing Managers Index (PMI) and robust weekly Jobless Claims from the United States (US).

Furthermore, the Australian Dollar faced downward pressure due to the decline in the ASX 200 Index. Despite a positive performance on Wall Street, where all three major benchmarks set record highs, the Australian equity market experienced losses, particularly in energy and consumer stocks.

Meanwhile, the US Dollar Index (DXY) continued to extend its gains, despite lower US Treasury yields. However, the US Dollar encountered challenges due to the Federal Reserve’s (Fed) reaffirmation of expectations for three interest rate cuts in 2024. The prevailing consensus suggests the start of an easing cycle in June, with the timing of the next cut contingent upon incoming data.

Additionally, key economic indicators from various regions were reported. Notably, Australian Employment Change for February surged to 116.5K, surpassing expectations, while the Unemployment Rate dropped to 3.7%, lower than anticipated. In the US, the preliminary Judo Bank Services PMI rose to 53.5, but the S&P Global Services PMI showed a slight decrease. Manufacturing PMI exceeded expectations, while Initial Jobless Claims for the week ending on March 15 were below expectations.

Moreover, the People’s Bank of China (PBoC) kept its interest rate unchanged, while the Federal Open Market Committee (FOMC) maintained interest rates at 5.5% during Wednesday’s policy meeting. The dovish stance signaled by US Federal Reserve (Fed) Chair Jerome Powell in the post-meeting press conference exerted additional downward pressure on the Greenback.

In the US housing sector, Building Permits and Housing Starts both showed increases in February, while the preliminary US Michigan Consumer Sentiment Index for March decreased slightly.

NZDUSD – Drops Near 0.6020 on Strengthening Greenback

The NZ Trade balance data in February month came at $-11.99 billion compared to $-12.62 billion. Exports surged to $5.89 billion from $4.81 bilion, imports rose to $6.11 billion from $5.9 Billion. This data hopes for RBNZ to cut the rates earlier this year not wait for 2025.Already Q4 recession data of GDP is printed this week.

NZDUSD has broken the Ascending channel in downside

NZD/USD Slips Near 0.6020 Amid Stronger USD

On the second consecutive session, NZD/USD continues its downward trend, hovering near 0.6020 during Asian trading hours on Friday. The strengthening US Dollar (USD) amid mixed US data contributes to this decline.

While the S&P Global Services PMI declined slightly to 51.7 in March, below the expected 52.0, Manufacturing PMI rose to 52.5, exceeding expectations. However, Composite PMI saw a minor dip to 52.2 from the previous 52.5.

Despite lower US Treasury yields, the US Dollar Index (DXY) remains robust. Challenges arise from the Federal Reserve’s (Fed) confirmation of three interest rate cuts in 2024, with an easing cycle expected to begin in June.

In February, New Zealand’s Trade Balance improved to $-11.99 billion year-on-year, with both exports and imports increasing from January. This improvement comes amidst speculation that the Reserve Bank of New Zealand (RBNZ) may consider cutting its official cash rate this year, prompted by an unexpected recession in Q4 of 2023.

XTIUSD – WTI Nears Weekly Low, Stays Below Mid-$80s

The Crude Oil prices are remain flat after the investors confidence on cease fire talks is narrowing between Israel and Gaza as per US Secretary of state Anthony Blinken said in the statement. The OPEC+ will cut 2.2 million barrels per day is possible due to Ukraine attacked Russia Oil Refineries.

XTIUSD Crude Oil price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

WTI Near Weekly Low Amid USD Strength and Supply Concerns

West Texas Intermediate (WTI) crude oil prices hover near the weekly low around $80.30 during the Asian session on Friday, facing continued selling pressure for the third consecutive day.

US Secretary of State Antony Blinken’s remarks on narrowing gaps in Gaza ceasefire talks, coupled with USD strength driven by upbeat US economic prospects, contribute to the downward pressure on USD-denominated commodities, including crude oil. However, concerns over supply disruptions, including Ukrainian drone strikes on Russian oil refineries and OPEC+ production cuts, cushion the downside. Additionally, expectations of a stronger US economy and potential recovery in China may support oil prices, urging caution among bearish traders.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/