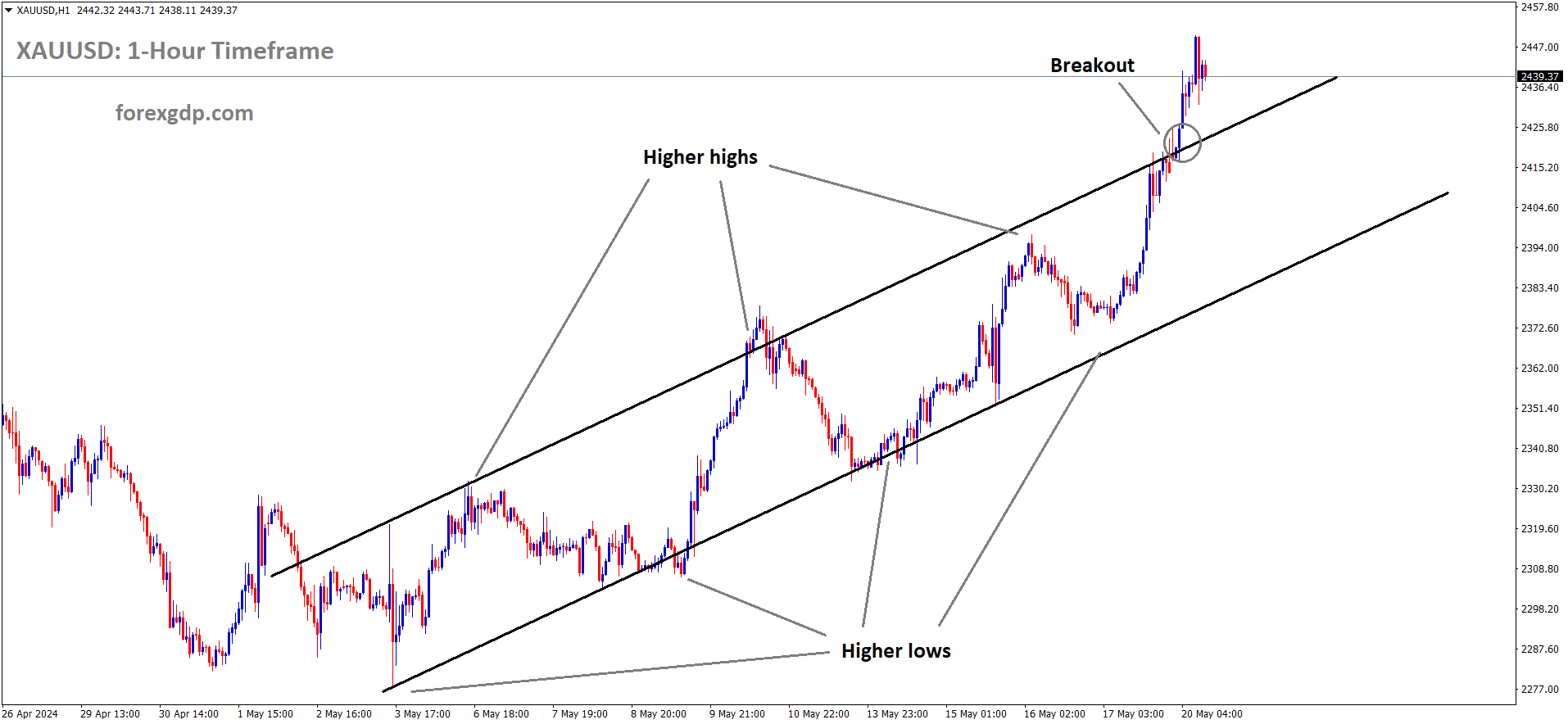

XAUUSD Gold price has broken Ascending channel in Upside

XAUUSD – Gold Hits Record High Amid Rising Geopolitical Tensions

The Gold prices are surged to Historical highs due to geopolitical tensions and China economy slowdown. China is buying 60K ounces of Gold in the April month so far it is the 18th straight month buying Gold from China Side. Additionally, Middle east nations also buy bullions for safety measures.

The gold price, represented by XAU/USD, surged on Monday, reaching a remarkable milestone near $2,450 during the European trading session. This surge came amid renewed optimism regarding potential interest rate cuts by the US Federal Reserve (Fed) and escalating geopolitical tensions in the Middle East. Additionally, the ongoing conflict between Russia and Ukraine contributed to an increased demand for safe-haven assets, further bolstering the appeal of gold.

As Monday progressed, market attention turned towards speeches from key Federal Reserve officials, including Bostic, Barr, Waller, Jefferson, and Mester. These speeches were anticipated to provide insights into the Fed’s future monetary policy direction. Any indications of a cautious approach or hawkish comments from these officials could potentially restrain the upward momentum of the precious metal.

In other developments, geopolitical risks and uncertainties in the Middle East remained in focus. Iranian state television reported concerning news regarding the crash site of a helicopter carrying Iran’s President Ebrahim Raisi, indicating no signs of life. Moreover, remarks from various Federal Reserve members, including Richmond Fed President Thomas Barkin and Cleveland Fed President Loretta Mester, highlighted the ongoing assessment of economic data and the appropriateness of current monetary policy.

Meanwhile, Fed Governor Michelle Bowman emphasized the restrictive nature of the current policy but expressed readiness to raise rates if inflation shows signs of stalling or reversing. Market expectations, as reflected by the CME FedWatch tool, indicated a 10% probability of a rate cut in June and nearly an 80% likelihood of a cut by September.

Additionally, the People’s Bank of China (PBoC) continued its streak of gold purchases, adding 60,000 troy ounces to its reserves in April, marking the 18th consecutive month of such acquisitions, according to official data released on Tuesday.

EURUSD – ECB’s Kazaks: Rate Cuts Likely to Commence in June

The ECB Policy maker Martin Kazaks said June month meeting will be decided when we have to start the rate cuts in the market. The Rate cuts has to handled in proper patience approach not in Rush manner. The data dependent and inflation must come back to 2% target then only we are doing in the right way of policy settings.

EURUSD has broken the Descending channel in upside

In a Bloomberg interview conducted on Monday, Martins Kazaks, a policymaker at the European Central Bank (ECB), expressed his outlook, stating, “it’s quite likely June will be when we start to cut rates.”

Kazaks emphasized the efficacy of a data-dependent approach thus far, implying that the ECB’s policy decisions have been suitably aligned with prevailing economic indicators.

Furthermore, he indicated reservations regarding the effectiveness of forward guidance as a policy tool in light of the elevated levels of uncertainty prevailing in the economic landscape.

Highlighting the central bank’s objectives, Kazaks outlined that the baseline scenario suggests a gradual approach towards achieving the ECB’s inflation target of 2%. This outlook provides the rationale behind considering rate cuts.

However, Kazaks emphasized the importance of a cautious and methodical approach, suggesting that any rate cuts should be implemented gradually without hastiness.

USDJPY – BoJ Survey: Japan Nearing Major Shift in Corporate Activity

The Survey conducted by Bank of Japan across Corporate sectors, The Big companies rises the sales prices to compensate the labor costs after the wage hike agreement. The Firms enjoying lower prices of yen is supported for its exports and accumulate more wealth as profit, if scenario continues then Japanese economy like to shrink than ever before.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Bank of Japan (BoJ) recently conducted a survey to evaluate the impact of its past monetary easing policies, revealing significant indications that Japan is on the verge of witnessing substantial shifts in corporate activity.

Key points from the survey include:

- Many companies expressed concerns about their ability to recruit sufficient workers if they restrain wage increases.

- A growing number of firms are beginning to pass on the rising costs of labor to their sales prices.

- Regardless of their size or sector, many companies indicated a preference for an economic environment where both wages and prices increase, as opposed to one where they remain stagnant.

- The BoJ’s monetary easing measures have supported capital expenditure and corporate business activities by maintaining low borrowing costs and enhancing fund availability.

- Some firms highlighted challenges in hiring personnel and heightened price competition as side-effects of the BoJ’s monetary easing policies.

- Major manufacturers identified fluctuations in foreign exchange rates as one of the impacts of the BoJ’s monetary easing on their operations.

- Big manufacturers emphasized the importance of exchange rate stability as the primary factor they seek from the BoJ’s monetary policy.

The potential broadening and sustainability of these shifts in corporate activity will be crucial in shaping Japan’s economic and price outlook moving forward.

USDCHF – climbs towards 0.9100 amid decrease in Swiss Industrial Production

The Swiss Industrial production by Volume is decreased to 3.1% in the Q1 Followed by 0.50% decline in the last quarter. Seasonally adjusted basis shows 1% decline in the Q1 Followed by 1.1% decline in the last quarter. The Swiss Franc is depreciated against counter pairs after the reading came.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Swiss Franc (CHF) weakened against the US Dollar (USD) following the release of lower-than-expected Swiss Industrial Production figures by Swiss Statistics.

The data revealed a notable decline of 3.1% in the volume of production in Swiss industries during the first quarter, marking a consecutive downturn from the upwardly revised 0.5% decrease observed in the previous quarter. This downward trend indicates a slowdown in industrial activity, with a seasonal adjustment showing a 1% drop in industrial production in Q1 compared to a revised 1.1% decline in the preceding quarter.

Meanwhile, the USD received support from the cautious stance of the Federal Reserve (Fed) regarding inflation and the possibility of rate adjustments in 2024, thus bolstering the USD/CHF pair.

Recent statements from Fed officials have echoed this sentiment. Atlanta Fed President Raphael Bostic emphasized the need for patience with interest rates, highlighting ongoing pricing pressure in the US economy. Similarly, Cleveland Fed President Loretta Mester suggested a prolonged period might be necessary to confidently gauge the inflation trajectory, advocating for the maintenance of a restrictive stance by the Fed.

However, higher-than-anticipated Initial Jobless Claims reported by the US Department of Labor on Thursday have fueled market expectations of a potential rate cut by the Federal Reserve in September. The number of Americans filing new claims for jobless benefits rose to 222,000 for the week ending May 10, surpassing the market consensus and indicating potential economic challenges ahead.

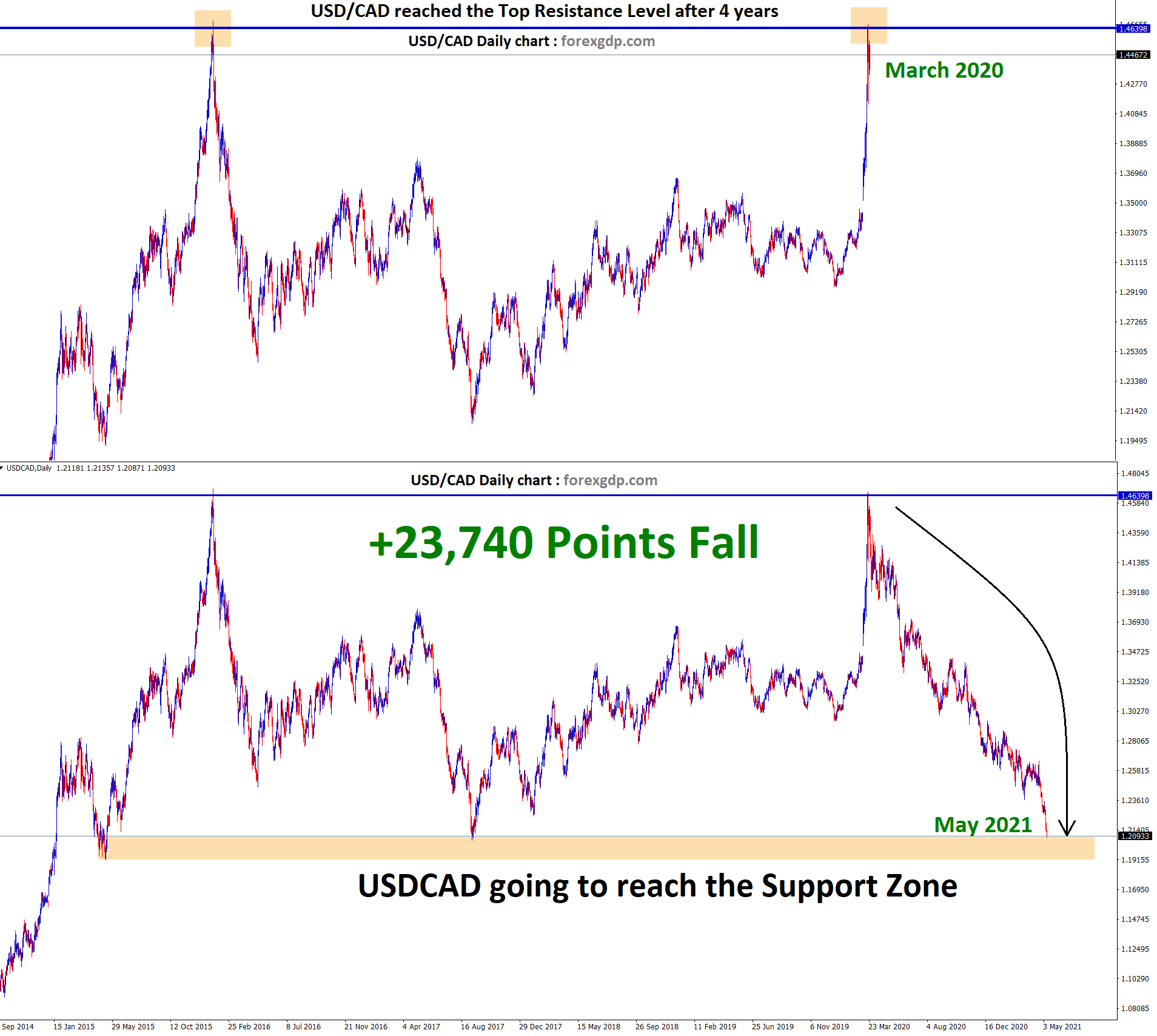

USDCAD – dips below 1.3610 ahead of Canadian CPI data

The Canadian CPI is expected at 2.8% YoY in the April month versus 2.9% YoY in the previous reading this week scheduled. The economists believed that BoC is started to cut the rates from June month due to inflation in Canadian economy comes to sufficient safety level.

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel

The USD/CAD pair continued its downward trend, hovering around 1.3605 during the early European trading hours on Monday. The depreciation of the US Dollar (USD), spurred by expectations of a potential Federal Reserve (Fed) rate cut, is exerting pressure on the pair. Traders are eagerly awaiting the release of the Canadian Consumer Price Index (CPI) inflation data, anticipated to show a decrease to 2.8% year-on-year (YoY) in April from the previous reading of 2.9% YoY.

Market sentiment suggests that the Bank of Canada (BoC) might initiate rate cuts as early as June or July, preceding any action by the Fed. However, the forthcoming CPI inflation report from Canada on Tuesday is expected to shed light on the BoC’s future rate decisions. A decline in inflation could potentially convince the central bank to implement interest rate cuts in the upcoming months. Presently, investors are estimating a nearly 40% probability of a BoC rate reduction in June, which could apply some downside pressure on the Canadian Dollar (CAD) and limit the USD/CAD pair’s decline.

Conversely, the Fed is anticipated to maintain its current interest rate until September, despite recent data showing subdued inflation in the United States. Notably, Cleveland Fed President Loretta Mester, known for her hawkish stance, affirmed that the Fed’s existing monetary policy stance aligns with the economic conditions. Moreover, Fed Governor Michelle Bowman emphasized that although the policy remains restrictive, she is open to raising rates if inflation exhibits signs of stagnation or reversal. This cautious approach by Fed officials is poised to provide support for the USD.

USD INDEX – USD Ends Week on Soft Note as Markets Digest Cautious Fed

The US Dollar loses it momentum of Gains last week due to weak CPI, Retail sales and increased initial Jobless claims. US Joe Biden put billions of Dollars increased Import tax on Chinese Goods makes another trade war tensions in the Two world biggest economies after the Trump Period.

USD INDEX is moving in the Box pattern and the market has fallen from the resistance area of the pattern

This import tax makes Exports of US Good will be lowered if China retaliation happened. So US Dollar moved down against counter pairs.

Despite this neutrality, the overall growth trajectory of the US economy in the second quarter, supported by the Federal Reserve’s (Fed) cautious approach to monetary policy, has provided some mild gains to the US Dollar as the week draws to a close.

The US economy has shown signs of robust growth in the second quarter, despite occasional softness in certain economic indicators. This overall positive growth outlook has influenced the cautious stance taken by Fed officials, who have refrained from implementing rate cuts. This cautious approach seems to be bolstering the strength of the Greenback and preventing significant downward pressure.

In the daily market movements, the DXY remains neutral as traders await further cues, particularly from the Fed, over the weekend. Earlier in the week, the release of April’s Consumer Price Index (CPI) and Retail Sales figures, along with an uptick in weekly Initial Jobless Claims, led to a slight depreciation of the US Dollar.

Various Fed officials have expressed their views on the current economic situation. Raphael Bostic, President of the Atlanta Fed, has expressed optimism regarding the progression of inflation in April but emphasized that the Fed is not yet ready to lower the policy rate. Loretta Mester, President of the Cleveland Fed, believes that the current monetary policy stance is appropriate as economic data continues to be evaluated. Thomas Barkin, President of the Richmond Fed, shares a similar sentiment, noting that inflation rates still have targets to meet.

According to the CME FedWatch Tool, market expectations indicate higher odds of the first rate cut occurring in September, reflecting the cautious sentiment prevalent in the markets regarding the future trajectory of Fed policy.

GBPUSD – Nears 1.2700 on Expectations of 2024 Fed Rate Cuts

The GBPUSD pair is moving higher against USD after the US Domestic data printed last week lower than expected numbers. This week GBP CPI data is scheduled for the April month and expected 2.7%, Already BoE Governor Andrew bailey said April month inflation data will reach our 2% target. So Investors hopes for this 2% target and 60bps rate cuts from BoE this year.

GBPUSD has broken the Descending channel in upside

The GBP/USD pair continues its upward trajectory, marking a second consecutive session of gains as it hovers around 1.2710 during Asian trading hours on Monday. This advancement is attributed to a weakened US Dollar (USD), which lends support to the GBP/USD pair. Notably, the US consumer inflation data for April, revealing a slowdown to 0.3%, has spurred speculation about potential rate cuts by the Federal Reserve (Fed) in 2024. However, the Fed remains cautious about inflation and the prospects of rate adjustments this year.

Market analysis via the CME FedWatch Tool indicates a slight uptick in the likelihood of the Federal Reserve implementing a 25 basis-point rate cut in September, rising to 49.0% from 48.6% a week prior. Such potential monetary policy easing by the central bank could undermine the US Dollar, thereby bolstering the GBP/USD pair.

Federal Reserve Board of Governors member Michelle Bowman’s recent remarks on Friday garnered attention, suggesting that the progression of inflation might not be as consistent as anticipated. She highlighted the temporary nature of last year’s observed inflation decline and the lack of further progress this year. Additionally, Richmond Fed President Thomas Barkin acknowledged the easing of inflation but underscored the prolonged timeline to achieve the Fed’s 2% target.

Meanwhile, in the United Kingdom (UK), market participants anticipate a potential 60 basis points (bps) interest rate cut by the Bank of England (BoE) in 2024, with initial expectations set for August. The forthcoming UK Consumer Price Index (CPI) data for April, scheduled for release on Wednesday, is projected to reveal an annual increase of 2.7%, according to FactSet estimates. This data is poised to significantly impact the performance of the Pound Sterling (GBP).

BoE Governor Andrew Bailey’s post-release commentary following March’s CPI data emphasized the anticipated convergence of UK inflation towards its 2% target in the coming month, noting a decline in inflation that aligns closely with the BoE’s February forecast.

AUDUSD – AUD Firm as Risk Sentiment Prevails; Market Awaits RBA Minutes

The China reported 2.3% YoY sales in the April month versus 3.1% printed in the March month and 3.8% expected. It is the 18th straight decline in the retail sales activity. Industrial Growth is accelerated to 6.7% YoY versus 4.5% printed in the March month and 5.5% is expected. China is prohibited General Atomics Aeronatics systems US Company from imports and exports in China makes retaliation on US, last week Biden imposed more tariffs on China.

AUDUSD has broken the Box pattern in upside

The Australian Dollar (AUD) continued its upward trajectory for the second consecutive session on Monday, buoyed by a weakening US Dollar (USD), which lent support to the AUD/USD pair. However, gains in the Aussie Dollar were tempered following the release of China’s interest rate decision. The People’s Bank of China (PBOC) opted to maintain the one-year and five-year Loan Prime Rates (LPR) at 3.45% and 3.95%, respectively. Traders are now eagerly awaiting the release of the Reserve Bank of Australia (RBA) Meeting Minutes scheduled for Tuesday.

Amidst these developments, the Australian Dollar may encounter hurdles as the yield on Australia’s 10-year government bond has dipped to approximately 4.2%, marking its lowest level in a month. This decline in bond yields comes on the heels of a softer-than-expected domestic jobs report for the first quarter. Sluggish wage growth has led market participants to revise down expectations of any interest rate hikes by the RBA. Australia’s Wage Price Index (QoQ) for the first quarter rose by only 0.8%, falling short of the market’s forecast of a 0.9% increase, representing the smallest uptick since late 2022.

The cautious stance maintained by the US Federal Reserve (Fed) towards inflation and the potential for rate adjustments in 2024 also influences market sentiment. Federal Reserve Board of Governors member Michelle Bowman’s recent remarks highlighted concerns about the pace of progress on inflation. She suggested that the decline in inflation witnessed in the latter part of last year was temporary, and there has been no significant further progress on inflation this year.

In the broader market context, recent announcements have impacted market dynamics. The Chinese Commerce Ministry’s decision to restrict General Atomics Aeronautical Systems, a US company, from certain import and export activities amid ongoing US-China trade tensions, has drawn attention. Economic developments in China hold particular significance for Australia, given their close trade relationship.

Furthermore, recent economic data releases have also influenced market sentiment. China’s Retail Sales for April increased by 2.3% year-over-year, falling short of expectations and signaling a slowdown in retail activity growth. Conversely, Industrial Production in China improved by 6.7% year-over-year, surpassing forecasts and indicating resilience in industrial output.

Additionally, developments in the US, such as the release of Initial Jobless Claims, which exceeded market expectations, and the deceleration of the Consumer Price Index (CPI) and Retail Sales figures for April, have also impacted market sentiment. Sarah Hunter, Chief Economist and Assistant Governor (Economic) at the Reserve Bank of Australia (RBA), addressed the REIA Centennial Congress, discussing strategies to address housing supply-demand imbalances in Australia, an issue of significant concern amidst rising prices and homelessness.

NZDUSD – Steady around 0.6150; RBNZ Expected to Maintain Unchanged OCR

The Economists believed that RBNZ will be hold the rates at 5.50% in this week meeting and it is the seventh straight hold on meeting if the rate is hold. The RBNZ is expected to keep the rates at higher until the inflation back to 1-3% target.

NZDUSD has broken the Descending channel in upside

During Asian trading hours on Monday, the NZD/USD pair maintains a position around 0.6130 as investors gear up for the upcoming policy meeting of the Reserve Bank of New Zealand (RBNZ) scheduled for Wednesday. Market consensus anticipates the RBNZ to uphold its Official Cash Rate (OCR) at the current level of 5.5%, extending a streak of unchanged rates for the seventh consecutive meeting. It is expected that policymakers will stress the necessity of maintaining a restrictive policy stance for an extended duration to steer inflation back within the targeted range of 1-3%.

Adding to the anticipation, the New Zealand Institute of Economic Research (NZIER) Monetary Policy Shadow Board has recommended the RBNZ to maintain the OCR unchanged in its forthcoming Monetary Policy Statement. This recommendation is rooted in ongoing apprehensions regarding persistent high inflation levels.

On the global front, the US experienced a moderation in consumer inflation, recording a 0.3% increase in April. This development has prompted speculation about potential rate cuts by the Federal Reserve (Fed) later in 2024. However, the Fed maintains a cautious stance regarding inflation and the likelihood of monetary policy adjustments in the current year.

According to data from the CME FedWatch Tool, there has been a slight uptick in the probability of the Federal Reserve implementing a 25 basis-point rate cut in September, with the likelihood increasing to 49.0% compared to 48.6% recorded a week earlier. Such potential easing measures by the central bank could potentially undermine the strength of the US Dollar, thereby providing support to the NZD/USD pair.

Federal Reserve Board of Governors member Michelle Bowman attracted attention on Friday with her remarks indicating that the progress on inflation might not unfold as steadily as initially anticipated. Bowman highlighted that the decline in inflation observed last year was temporary and that there hasn’t been significant further progress this year. Additionally, Richmond Fed President Thomas Barkin acknowledged that while inflation is showing signs of moderation, attaining the Fed’s 2% target will require additional time.

CRUDE OIL – WTI nears $79.70 after PBoC rate stability

The Crudeoil is moving higher after the PBOC left the rates at 1yr and 5yr at 3.45% and 3.95% respectively.The China real estate sector is tumbled last year and now the Government has injected 1 trillion Yuan ( $138 Billion) to overcome from Crisis, Local Government is ready to buy some apartments, lower the mortgage rules inorder to support the real estate crisis in the China.

XTIUSD Oil price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

This surge follows the decision of the People’s Bank of China (PBOC) to maintain its one-year and five-year Loan Prime Rates (LPR) at 3.45% and 3.95%, respectively. However, despite this positive momentum, crude oil prices face potential challenges in light of hawkish sentiments expressed by Federal Reserve (Fed) officials last week. Additionally, market attention is drawn to upcoming speeches by Fed members Bostic, Barr, Waller, Jefferson, and Mester scheduled for Monday.

On Friday, Federal Reserve Board of Governors member Michelle Bowman’s remarks regarding inflation’s uncertain progress captured headlines. She suggested that inflationary trends may not be as stable as previously anticipated, noting a lack of significant progress in inflation levels this year compared to the latter half of the previous year.

The previous week witnessed a 2% surge in WTI oil prices, buoyed by optimistic forecasts for increased demand from the United States (US), the world’s leading oil consumer. April’s US consumer inflation data, which revealed a modest 0.3% growth, raised speculations about potential Federal Reserve rate reductions in 2024. Such rate cuts could stimulate economic activity and subsequently boost energy demand. Moreover, lower US interest rates could depreciate the US Dollar (USD), potentially making oil more attractive to countries utilizing alternative currencies for trade.

Data from the US Energy Information Administration (EIA) indicated a 2.508 million barrel decrease in US crude stockpiles for the week ending May 10, marking the second consecutive week of decline and surpassing market expectations of a 1.350 million barrel decrease.

In China, April’s 6.7% year-on-year increase in industrial output signals a robust rebound in the country’s manufacturing sector, hinting at potential future demand growth. Additionally, Reuters reported “historic” measures announced by China on Friday to stabilize its property sector, including 1 trillion yuan ($138 billion) in additional funding from the central bank and relaxation of mortgage regulations. Moreover, local governments are expected to purchase “some” apartments to bolster the sector.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!