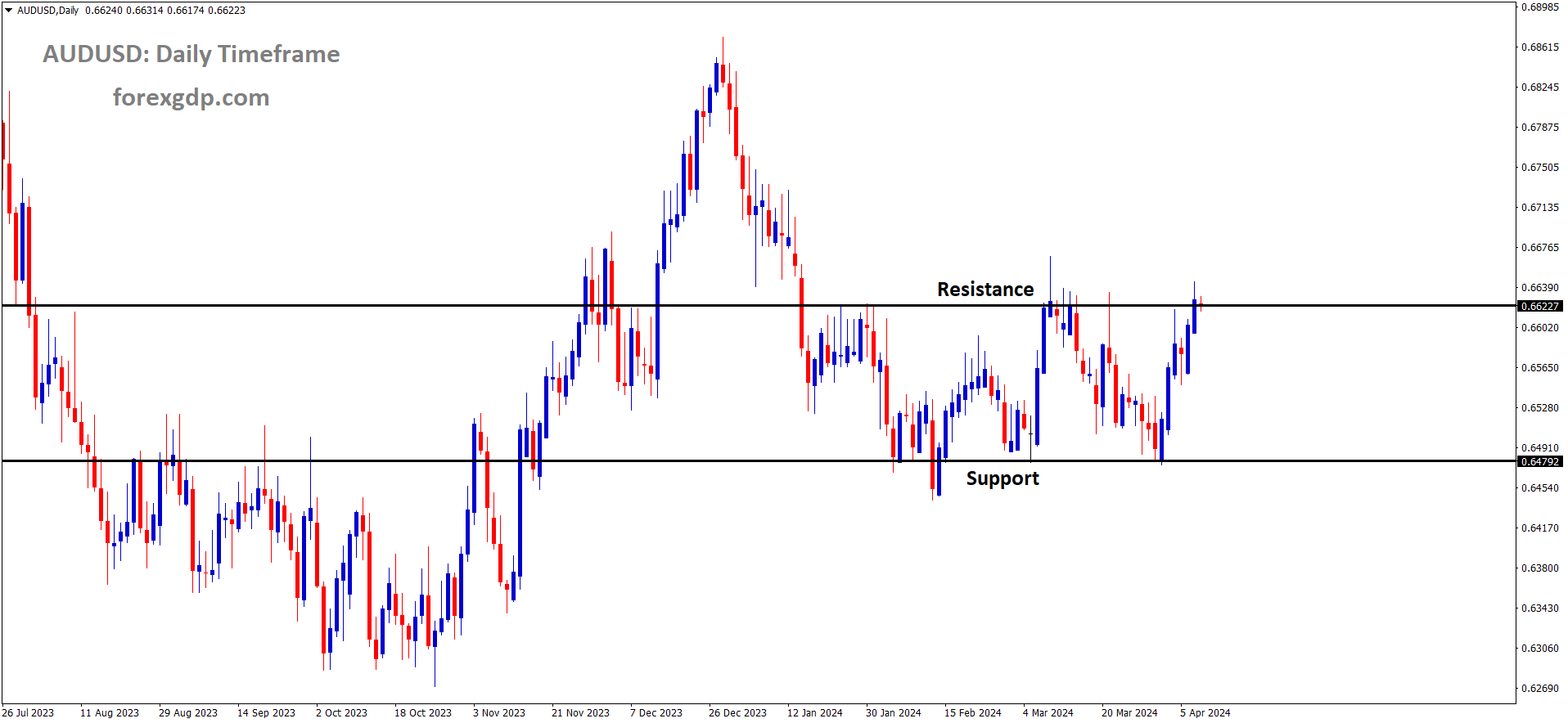

AUDUSD is moving in the Box pattern and the market has reached the resistance area of the pattern

AUDUSD – AUD Steadies, Awaits CPI Data Amid Stronger USD

The RBA is expected to cut the rates at September month is forecasted by Common wealth bank, increasing chances of rate holdings to September month stemming Australian Dollar move higher against counter pairs. Westpac consumer confidence April month came at -2.4% versus -1.8% decline in the previous month.

The Australian Dollar (AUD) endeavors to sustain its upward momentum for the third consecutive session on Wednesday. The AUD/USD pair hit a four-week peak at 0.6644 in the preceding session, propelled by a weakened US Dollar (USD) amidst declining US Treasury yields.

Investor sentiment towards the Australian Dollar strengthens as doubts emerge regarding the necessity of interest rate cuts by the Reserve Bank of Australia (RBA) in 2024. This skepticism arises from expectations of the Federal Reserve (Fed) maintaining its stance of higher interest rates.

The RBA has signaled a reluctance to consider further rate hikes, emphasizing the need for increased confidence in the inflation outlook before contemplating rate cuts. Attention now turns towards the release of the US Consumer Price Index (CPI) data and the Federal Open Market Committee (FOMC) Minutes later in the North American session.

In the financial landscape:

– Australia’s Westpac Consumer Confidence Index for April records a decline of 2.4%, compared to the previous decrease of 1.8%.

– Commonwealth Bank projects three 25 basis points (bps) interest rate cuts by year-end, starting from September.

– Westpac anticipates interest rate cuts to commence in September, while NAB and ANZ predict it won’t be until November.

– Federal Reserve Bank of Minneapolis President Neel Kashkari underscores the central bank’s commitment to combatting inflation, aiming to bring it back down to the target level of 2% despite the current rate hovering around 3%.

– According to the CME FedWatch Tool, the probability of a 25-basis point rate cut by the Fed in June slightly rises to 53.5%, while the likelihood of a rate cut in July decreases to 49.9%.

– The US headline CPI is forecasted to accelerate in March, with the core measure expected to show a moderation.

– Friday’s US Nonfarm Payrolls (NFP) report reveals a significant increase of 303K jobs in March, surpassing both expectations of 200K and the previous reading of 270K. US Average Hourly Earnings rise by 0.3% month-over-month in March, meeting expectations.

XAUUSD – GOLD Price Forecast: XAU/USD Surges Past $2,350, Investors Eye US CPI Data

The Gold prices surpassing $2350 today after the Israel Foreign minister Kat said if Iran do any retaliation on attacks we do severe attacks on them, other side Iran Supreme Leader said Israel will be punished severely in upcoming days due to Iran officers killed in Embassy in Syria. This fears of War consecutive makes Gold prices stemmed higher, central banks silently accumulating Gold for safer play during war times. China so far March month accumulation of 1.6lakhs troy ounces of Gold in its reserves.

XAUUSD Gold price is moving in an Ascending channel and the market has reached higher high area of the channel

During early European trading hours on Wednesday, XAU/USD extends its upward movement, reaching near $2,355. The surge in the price of gold is supported by expectations of rate cuts from the Federal Reserve (Fed) this year, increased central bank purchases, and escalating geopolitical tensions in the Middle East.

Israeli Foreign Minister Israel Kat issued a warning on Wednesday, stating that Israel would retaliate if Iran launched an attack from its territory. Earlier, Iran’s supreme leader had stated that Israel “must be punished” following an apparent attack on an Iranian consulate building in Syria last week, resulting in the deaths of two senior military commanders, according to Sky News. These escalating tensions in the Middle East could contribute to a rise in demand for safe-haven assets like gold.

Moreover, the consistent gold purchases by major central banks have propelled the yellow metal to nearly an all-time high. In March alone, China added 160,000 troy ounces of gold to its reserves, marking the 17th consecutive month of such acquisitions. Additionally, countries such as Turkey, India, Kazakhstan, and some Eastern European nations have also been purchasing gold this year, alongside China.

Gold traders will closely watch the release of the US Consumer Price Index (CPI) data for March and the Federal Open Market Committee (FOMC) Minutes scheduled for Wednesday. These events could offer insights into the trajectory of inflation and the Fed’s monetary policy direction. A stronger inflation reading might diminish expectations for Fed rate cuts in June, potentially capping the upside for gold. Conversely, softer inflation data could fuel speculation of rate reductions, lending support to XAU/USD.

EURUSD – holds steady before US CPI, ECB meeting

The ECB is expected to hold the rates at tomorrow meeting is economists view. ECB President Lagarde company is set to cut the rates at June month based on incoming data of inflation and GDP, Labour data.

EURUSD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

The economic calendar is relatively light on both sides of the Atlantic as investors gear up for the release of US inflation figures on Wednesday and the European Central Bank (ECB) monetary policy decision on Thursday.

The US Consumer Price Index (CPI) for March is expected to rise by 0.3% month-over-month, slightly lower than February’s 0.4% increase. Annually, CPI is projected to climb from 3.2% to 3.4%. Meanwhile, the core CPI, which excludes volatile food and energy prices, is forecasted to drop from 0.4% to 0.3% month-over-month and from 3.8% to 3.7% year-over-year.

On April 11, the ECB is anticipated to maintain its current interest rates, but there’s a growing likelihood that President Lagarde and the ECB policymakers may need to implement further easing measures come June to achieve a smooth economic transition.

This potential action could widen the interest rate differentials between the Eurozone and the US, possibly leading to additional downside pressure on the EUR/USD exchange rate.

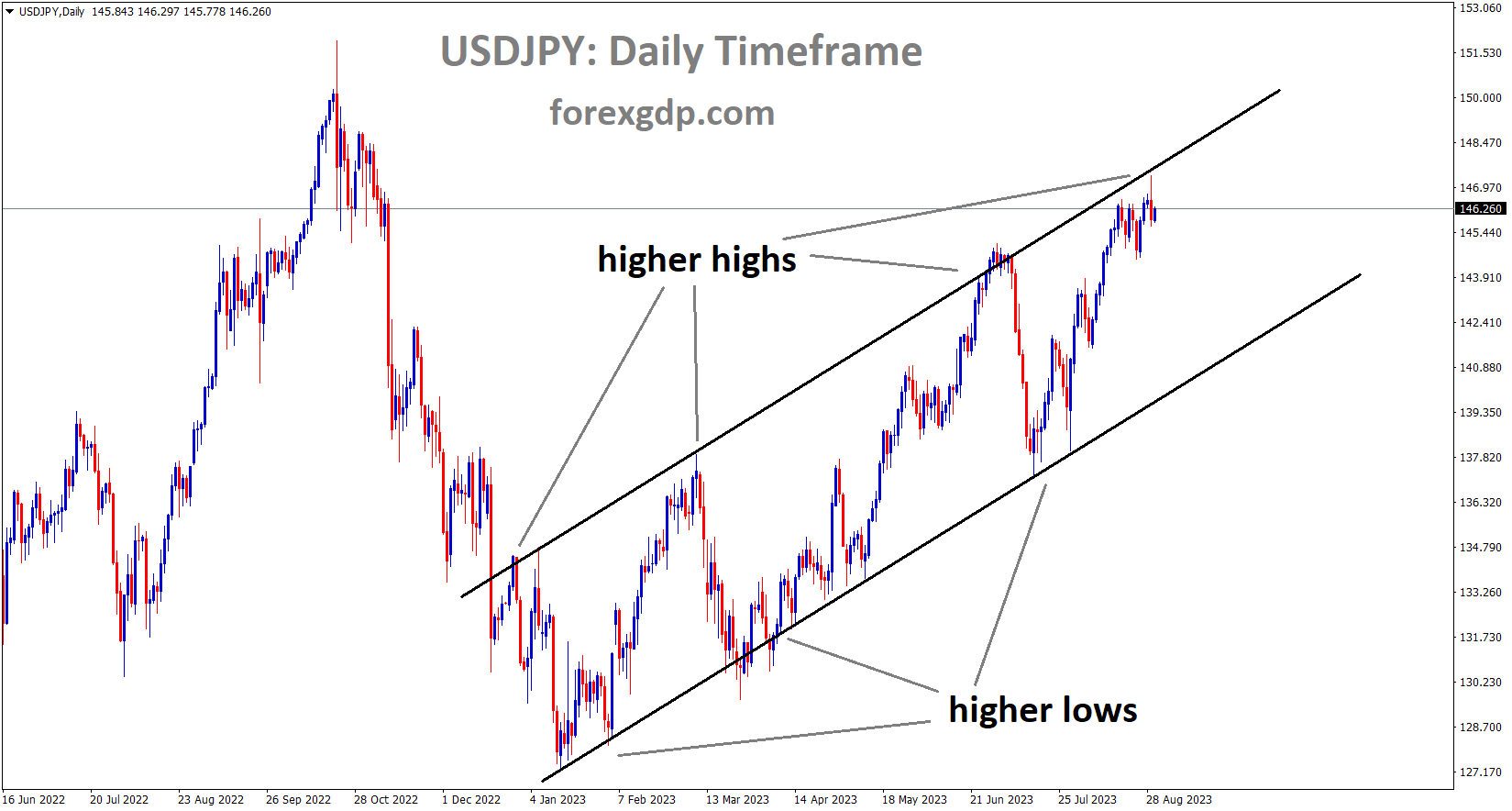

USDJPY – BoJ’s Ueda: Accommodative Conditions to Persist

The Bank of Japan Governor Ueda said at semi annual monetary policy meeting today, The central bank has to maintained the current accommodative stance for some times. Until wage hiked pushed inflation to trend upside we keep qualitative and quantitative easing measures taken.

USDJPY is moving in the Box pattern and the market has reached the resistance area of the pattern

We did not do change on every FX Moves in the market, this FX Moves relying on the Fundamentals and intervention also not say at this time. Import costs is higher when Japanese Yen weakness persists, if inflation tends to survive within 2% target we do not change the settings. We focussed on 2% above inflation and import costs to set to lower, we remove step by step stimulus from the economy. The message is down turn for Japanese Yen due to Dovish play on monetary policy settings.

In his Semiannual Report on Currency and Monetary Control released on Wednesday, Bank of Japan (BoJ) Governor Kazuo Ueda provided insights into the bank’s stance on economic activity, prices, and monetary policy. Ueda highlighted the expectation of maintaining accommodative financial conditions in light of the current economic outlook.

Ueda expressed confidence that the price stability target of 2 percent would be achieved in a sustainable manner by the end of the projection period outlined in the January 2024 Outlook Report. He noted that various data and anecdotal information from firms indicated a strengthening of the virtuous cycle between wages and prices.

Based on these observations, the Bank concluded that the policy framework of Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control and the negative interest rate policy had fulfilled their roles. Consequently, the Bank decided to adjust the monetary policy framework, setting the uncollateralized overnight call rate as the policy interest rate with the aim of maintaining it at around 0 to 0.1 percent.

Regarding the outlook for economic activity and prices, Ueda anticipated that accommodative financial conditions would persist for the foreseeable future. He emphasized the importance of supporting the economy’s momentum toward achieving the 2 percent inflation target, as trend inflation has yet to reach this level.

Ueda stressed the need to carefully monitor whether trend inflation would indeed progress toward 2 percent when determining the appropriate degree of monetary support. He cautioned against waiting for trend inflation to hit 2 percent before adjusting monetary policy, as it could heighten the risk of inflation overshooting and necessitate aggressive rate hikes.

Addressing foreign exchange (FX) movements, Ueda stated that the Bank would not alter monetary policy solely to address FX fluctuations. However, if FX movements led to significant increases in import prices or posed risks to trend inflation, the Bank might consider adjusting monetary policy accordingly.

Ueda also discussed the Bank’s objectives regarding the Japanese Government Bond (JGB) market, expressing a desire for market-based determination of yields. He indicated that the Bank would monitor market reactions to its policy shift in March and aim to gradually reduce the size of JGB purchases.

Furthermore, Ueda acknowledged the challenges posed by Japan’s prolonged deflation and low inflation in influencing public inflation expectations through the expansion of the monetary base.

USDCHF – Slides to 0.9000 Amid Positive Sentiment, Focus on US Inflation

The Swiss Franc is moving lower after the cease fire talks begins between Israel and Gaza . SNB like to cut the rates further due to inflation in the February month came at lower than previous month. Today US CPI will drive the further USDCHF in the market based on readings.

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Franc experiences a decline as market sentiment remains optimistic, leading traders to reduce their expectations of Federal Reserve (Fed) rate cuts at the upcoming June meeting. This shift comes as robust United States Nonfarm Payrolls (NFP) data bolsters confidence in the inflation outlook.

Positive sentiment is reflected in the opening of the S&P 500, indicating strong demand for risky assets. However, there is concern as 10-year US Treasury yields decrease to 4.37%, driven by worries that prolonged high interest rates could create imbalances in employment and inflation.

Chicago Federal Reserve President Austan Goolsbee’s recent remarks underscore the need for the central bank to consider the duration of elevated interest rates. Goolsbee warns that prolonged high rates could lead to a rise in the Unemployment Rate.

Amid this backdrop, the US Dollar Index (DXY) retreats to 103.90 amidst the prevailing positive market sentiment. Looking ahead, investors are eagerly awaiting the release of US consumer price inflation data for March, scheduled for Wednesday.

Projections suggest that both monthly headline and core inflation rates are expected to slow to 0.3% from 0.4% in February. Meanwhile, annual headline CPI is anticipated to accelerate to 3.4% from 3.2%, while core inflation is predicted to decelerate to 3.7% from 3.8%. This data will significantly impact market expectations regarding potential Fed rate cuts.

Regarding the Swiss Franc, investors anticipate further interest rate cuts by the Swiss National Bank (SNB) due to persistently low inflation, which consistently falls below the 2% target. The SNB initiated the global rate-cut cycle by unexpectedly announcing a dovish interest rate decision in the March meeting, reducing borrowing costs by 25 basis points (bps) to 1.5%.

USD INDEX – Ends neutral session ahead of CPI data

The US CPI data for the month of March is scheduled today and expected to rise from previous month readings. FED Members saying hawkish tone made favouring for US Dollar in the near term.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

Market activity remains subdued as the focal point of the week revolves around the imminent release of March’s US Consumer Price Index (CPI) data on Wednesday. Concurrently, diminishing US Treasury yields appear to be exerting downward pressure on the US Dollar, while minor data releases have failed to elicit significant market reactions.

The upcoming CPI figures are expected to further shape expectations regarding the Federal Reserve’s (Fed) monetary policy stance, with the likelihood of an easing cycle commencing in June. Despite two consecutive months of elevated inflation, the Fed recently revised its projections upward. However, Fed Chair Jerome Powell has reiterated a cautious stance, indicating a readiness to wait and observe before making any policy adjustments. Consequently, the US Dollar remains in a state of anticipation, awaiting potential shifts in monetary policy direction driven by incoming economic data.

In other market developments, the National Federation of Independent Business (NFIB) reported a decline in small business optimism, attributed largely to concerns over inflation and the labor market. Despite robust job growth in March, there are indications that continued monetary austerity could potentially lead to an uptick in unemployment rates.

Fed officials have moderated their previously hawkish tone, suggesting a more dovish or neutral stance on monetary policy. Market expectations for a rate cut have diminished, with the probability of a June cut falling to approximately 50% and a July cut dropping below 90%, marking the lowest levels since last October.

US Treasury yields have witnessed a decline, with the 2-year yield reaching 4.74%, while the 5-year and 10-year yields traded at 4.37% and 4.36%, respectively. The forthcoming CPI data release is anticipated to inject volatility into the bond market, shaping expectations for future Fed decisions.

Additionally, investors are keenly awaiting the release of the Federal Open Market Committee (FOMC) minutes from March’s meeting, scheduled for Wednesday. These minutes will offer further insights into the Fed’s discussions and deliberations regarding monetary policy.

GBPUSD – holds slight declines under 1.2700 pre-US CPI data

The UK Budget responsibility team projected UK Growth will be 0.80% this year. UK nation GDP is scheduled this week. US CPI is expected to come larger than expected makes GBP moving flat against USD.

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Investors are eagerly awaiting the release of the US Consumer Price Index (CPI) inflation data, coupled with speeches from Fed officials Bowman and Goolsbee later in the day.

Recent hawkish comments from some Federal Reserve (Fed) officials have drawn attention. Chicago Fed President Austan Goolsbee remarked on Monday that the recent jobs report was “quite strong,” prompting the central bank to consider how long it can maintain its current interest rate stance without harming the economy. Meanwhile, Minneapolis Fed President Neel Kashkari noted that while the labor market is no longer ‘red hot,’ it remains tight, expressing his belief that inflation will continue to ease.

According to the CME FedWatch Tool, financial markets have priced in nearly a 57% probability of a rate cut in June, while the likelihood of a July cut has dropped below 75%. The US March CPI data will be closely watched as it could influence the Fed’s future monetary policy decisions, especially after last month’s 3.2% year-over-year increase. Persistent inflation and robust US growth signals may bolster the Greenback in the short term.

Conversely, the latest UK Office for Budget Responsibility (OBR) forecast suggests that the UK economy is projected to grow by 0.8% this year due to a recovery in domestic demand. The country’s monthly Gross Domestic Product (GDP) report is scheduled for release on Friday. Should the GDP figure surpass expectations, it could slow down the easing cycle and lift the Pound Sterling (GBP) against the US Dollar (USD). Currently, markets are pricing in 75 basis points (bps) of rate cuts by the Bank of England (BoE) this year, potentially lowering the benchmark rate from its current level of 5.25% to 4.5%.

NZDUSD – RBNZ Keeps Interest Rate Steady at 5.50%

The RBNZ hold the rates at 5.5% for the 6th consecutive meeting in a row, they are focused to control the target of inflation to 2% by this year. 4.7% inflation sustaining now till the Q4 of 2023, it is the 2.5 years low of inflation. Last day Business confidence of Q1 slumped to 25% it is drastically fall in the Business firms view. So August month Rate cuts are expected from the RBNZ in the economists view.

NZDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

Following the conclusion of the April policy meeting on Wednesday, the Reserve Bank of New Zealand (RBNZ) announced its decision to maintain the Official Cash Rate (OCR) at 5.50%, aligning with market expectations.

In its Monetary Policy Statement (MPS) summary, the RBNZ highlighted the anticipated trajectory of the New Zealand economy. The committee reiterated the necessity of a restrictive monetary policy stance to alleviate capacity pressures and control inflation. Despite weak economic growth in New Zealand, the committee expressed confidence that persisting with the OCR at a restrictive level would facilitate a return of consumer price inflation to the target range of 1 to 3 percent within the current calendar year.

During the interest rate meeting, committee members discussed the effectiveness of the current monetary policy in curbing demand and alleviating capacity pressures to steer inflation back to target levels. They acknowledged the decline in business confidence and weakened expectations for activity and investment. While near-term business pricing intentions decreased, they remained elevated due to rising costs.

The committee recognized the support to aggregate consumer spending from continued strength in net migration and rising dwelling costs. Emphasizing the need for a sustained restrictive monetary policy, the members deliberated on the balance of risks, acknowledging the limited tolerance for prolonged deviation from the inflation target while inflation expectations and pricing intentions remained elevated.

Members also discussed the persisting risk of services inflation and the elevated goods price inflation. They noted the potential for a more rapid decline in inflation than expected due to ongoing restrictive monetary policy amid a backdrop of weak global growth.

Overall, the RBNZ’s decision to maintain the OCR at 5.50% reflects its commitment to managing inflationary pressures and fostering economic stability in New Zealand.

USDCAD – Holds Slight Decline, Awaits BoC Decision and US CPI

The bank of Canada is expected to keep the rates at 5.005 in the today meeting, So Canadian Dollar falling down against counter pairs, Israel- Gaza ceasefire talks under progress makes relief for Crude oil prices stands at $85. Any positive attainment of ceasefire talks will drive Canadian Dollar lower against counter pairs.

USDCAD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Market participants eagerly await the Bank of Canada’s (BoC) decision on interest rates, with prevailing expectations leaning towards the rate remaining unchanged at 5.0%. Additionally, attention is focused on the release of the US Consumer Price Index (CPI) data and the Federal Open Market Committee (FOMC) Minutes scheduled later in the North American session.

Crude oil prices face obstacles that potentially weigh on the Canadian Dollar (CAD). The ongoing impasse in Gaza ceasefire negotiations revives concerns regarding the security of oil supplies from the Middle East, offsetting the impact of a larger-than-anticipated increase in US Crude inventories. The price of West Texas Intermediate (WTI) oil hovers around $84.70 per barrel at the time of writing.

Federal Reserve (Fed) Bank of Minneapolis President Neel Kashkari reiterates the central bank’s commitment to combating inflation. Emphasizing the importance of returning the current inflation rate, which hovers around 3%, to the target level of 2%, Kashkari signals the Fed’s dedication to this goal.

Investors maintain a cautious outlook, anticipating potential policy adjustments influenced by incoming data. Strong labor market indicators from the previous week could prompt a more hawkish stance from the Federal Reserve if inflation surpasses expectations.

CRUDE OIL – WTI Slides to $84.70, Focus on Gaza Ceasefire Talks and US CPI

The Iran Navy leader said we are going to close the strait of Hormuz, it is the fifth volume of Sea transport of Oil channels, if it is closed then there will be a huge demand created in the market for Oil.

XTIUSD Crude Oil price is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

Western Texas Intermediate (WTI), the benchmark for US crude oil, is observed trading around $84.60. The commodity experiences a decline for the fourth consecutive day, with negative sentiment prevailing. This downturn is attributed to a notable increase in US crude stockpiles and profit-taking activities ahead of the imminent release of the US March Consumer Price Index (CPI) report and the Federal Open Market Committee (FOMC) Minutes scheduled later in the day.

Speculation regarding the Federal Reserve (Fed)’s interest rate policy intensifies following the recent US employment report released the previous week. The report has prompted discussions among investors about the possibility of the Fed delaying interest rate cuts this year. Market participants are closely monitoring the US CPI inflation data for March, as it holds potential implications for the inflation trajectory and the Fed’s monetary policy stance. Should the CPI data show a stronger-than-expected outcome, it could lead to a strengthening of the US Dollar (USD), consequently putting downward pressure on the USD-denominated WTI price.

Additionally, the WTI price faces selling pressure due to a larger-than-anticipated increase in US crude inventories. Data released for the week ending April 5 revealed a build-up of 3.034 million barrels, contrasting with the previous week’s decline of 2.286 million barrels. The American Petroleum Institute (API) had forecasted a rise in stocks by approximately 2.415 million barrels in its report on Tuesday.

Geopolitical developments further impact market sentiment. The leader of Iran’s Revolutionary Guard navy suggested the possibility of closing the Strait of Hormuz if deemed necessary. Given that a significant portion of the world’s oil consumption traverses through this strategic waterway daily, such remarks raise concerns about potential disruptions to oil supply. Consequently, this factor could limit the downside of WTI prices.

In the Middle East, negotiations for a ceasefire in the Gaza conflict continue. While Palestinian militant groups have indicated that the proposed ceasefire terms from Israel do not meet their conditions, they remain open to further consideration. Oil traders are monitoring these geopolitical tensions closely, as any escalation could heighten concerns about a tight oil market.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!