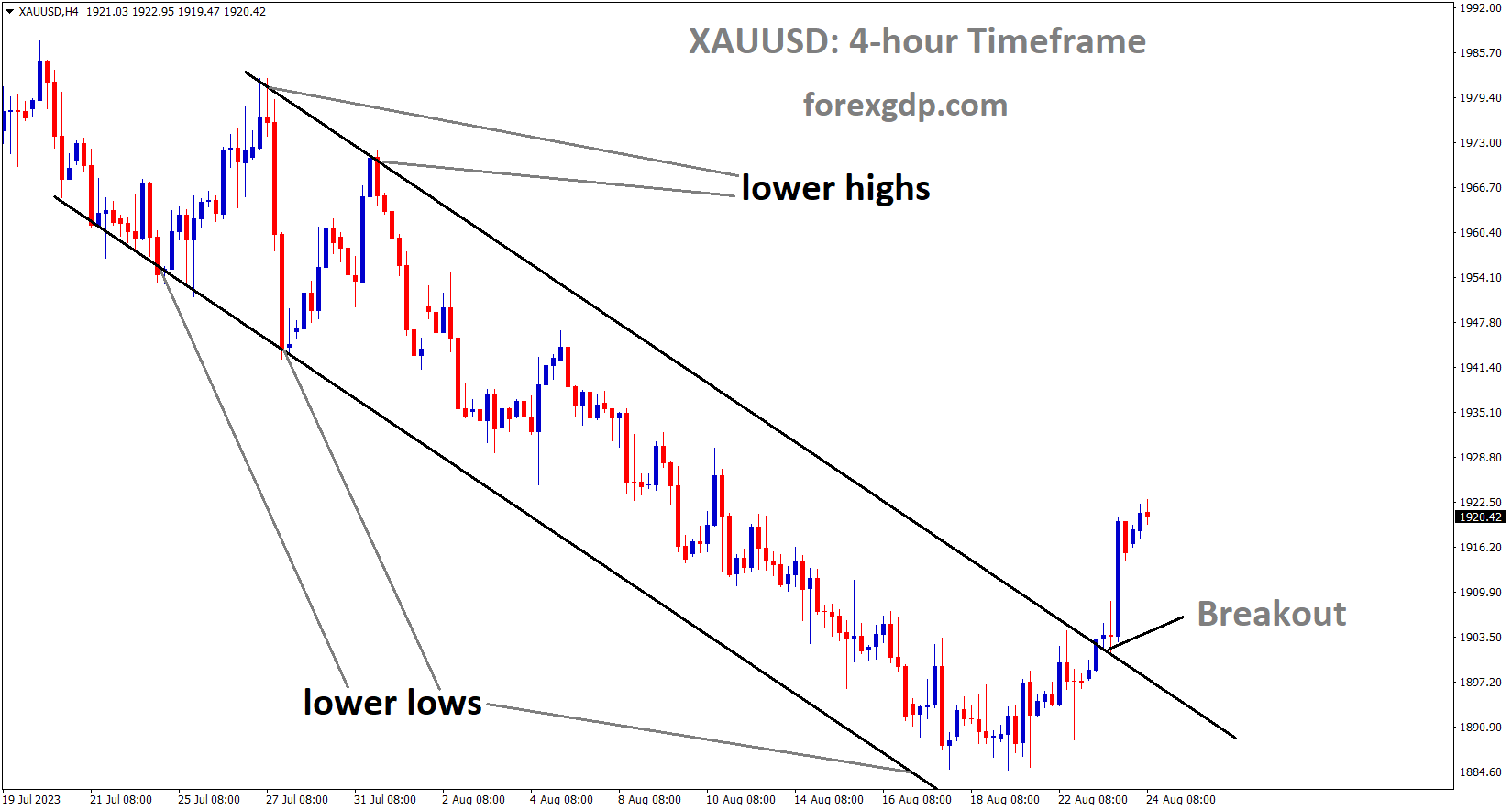

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD – Gold Nears $2,300 on Declining Safe-Haven Demand

The Gold prices are moving lowered after the Iran-Israel conflict is cooled down. Iran said nothing retaliation on Israel here after. So Calm down of the war fears makes buying of Gold is lowered in the recent 2 days.

The price of gold (XAU/USD) remains under significant selling pressure for the second consecutive day, hovering near its lowest level in over two weeks, around the $2,300 mark as the European session approaches on Tuesday. Despite the recent attack on US forces in the Middle East, investor sentiment remains optimistic amid hopes of a de-escalation in the Iran-Israel conflict. This sentiment, coupled with expectations of a potential delay in interest rate cuts by the Federal Reserve (Fed), has been a key factor dampening demand for the non-yielding yellow metal.

Additionally, the anticipation of a more hawkish stance from the Fed continues to support elevated US Treasury bond yields, bolstering the US Dollar (USD) and contributing to the downward pressure on gold prices. However, speculations persist that major central banks may implement interest rate cuts later this year, which could help mitigate further losses in the gold market. Traders are likely awaiting the release of key economic data this week, including the Advance US Q1 GDP report and the Personal Consumption Expenditures (PCE) Price Index, before committing to new directional positions.

Furthermore, Iran’s indication that it does not intend to retaliate against the limited-scale missile strike by Israel on Friday has further diverted investor flows away from safe-haven assets like gold. Stronger-than-expected US payroll data, coupled with signs of rising consumer price inflation and hawkish commentary from Federal Reserve officials, have led investors to scale back their expectations for US interest rate cuts. Present market projections suggest that the Fed may commence its rate-cutting cycle in September, with only 34 basis points or less than two rate cuts expected in 2024, compared to the three projected by the central bank.

The yield on the benchmark 10-year US government bond remains near a five-month high, acting as a tailwind for the US Dollar and exerting additional pressure on the XAU/USD pair. Moreover, concerns about slowing global economic growth have raised prospects for synchronized interest-rate cuts by major central banks in the latter half of this year, potentially lending support to the commodity.

Traders are also looking forward to the release of flash global PMI prints on Tuesday, alongside the Advance US Q1 GDP report and the US Personal Consumption Expenditures (PCE) Price Index later in the week, which are expected to provide further clarity and potentially drive market movements.

EURUSD – German PMI Manufacturing Beats Expectations

The German Manufacturing PMI rose to 42.2 in the April month from 41.9 printed in the March month and 42.8 is expected. This is the highest level in two months. EURUSD moved higher after the data printed.

EURUSD has broken the Descending triangle pattern in downside

According to the preliminary business activity report published by the HCOB survey on Tuesday, Germany’s manufacturing sector exhibited signs of improvement in its contraction during April. Meanwhile, the services sector outperformed expectations.

Specifically, the HCOB Manufacturing Purchasing Managers’ Index (PMI) in the Eurozone’s economic powerhouse climbed to 42.2 this month, surpassing the anticipated figure of 42.8. This marks a positive uptick from March’s reading of 41.9 and represents the highest level observed in the manufacturing PMI in the past two months.

USDJPY – BoJ’s Ueda: Flexibility Preferred Over Firm Policy Commitments

The BoJ Ueda said Wage negotiations are very much impacted on Japanese Economy, In March Month Wage hike approval from Union is the Top of the scope in the changes of monetary policy settings. Now we wait for data dependent approach on changing the monetary policy settings. So we need some time for applying the wage hikes in the consumer spending and then raise for inflation in the economy, then we adjust the monetary policy settings, we do not expected over forecast of the economy day by day.

USDJPY has broken the Box pattern in upside

Bank of Japan (BoJ) Governor Kazuo Ueda provided insights on Tuesday regarding the ongoing Japanese wage negotiations and their potential impact on the central bank’s policy decisions.

Ueda highlighted the significance of annual wage negotiations as a crucial factor in shaping the BoJ’s policy framework. These negotiations, he emphasized, have consistently held importance in the central bank’s consideration of economic variables when formulating policy strategies.

In determining policy directions, Ueda stressed the BoJ’s comprehensive approach, which encompasses not only wage negotiations but also a wide array of economic indicators. He noted that the decision to adjust policy in March was influenced by favorable outcomes in wage negotiations, coupled with robust performance across various sectors of the economy.

The governor emphasized the dynamic nature of policy formulation, indicating that the BoJ’s approach to wage negotiation outcomes may vary depending on prevailing economic conditions. He acknowledged the challenge of determining the optimal timing for policy adjustments, underscoring the importance of gathering sufficient data before making informed decisions.

Ueda emphasized the BoJ’s preference for flexibility in policy implementation, expressing a reluctance to overly commit to specific policy stances. This approach allows the central bank the necessary leeway for adjustments as economic conditions evolve.

Overall, Ueda reiterated the BoJ’s commitment to its price stability mandate, highlighting the reliance on trends in inflation and a data-dependent approach in shaping future policy initiatives.

USDCHF – Stays Above 0.9100, Focus on US PMI Data

The Swiss Franc calmed after the Middle east tensions calmed. Any surge in the tensions of the middle east will make surge in the safe haven flows of Swiss Franc in the market. Swiss ZEW Survey is scheduled this week and SNB Chairman Thomas Jordan speech scheduled this week.

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

During the early European session on Tuesday, the USD/CHF pair continued to trade on a stronger note, hovering around 0.9125 for the second consecutive day. This uptrend is attributed to the prevailing risk-on sentiment in the market, fueled by diminishing concerns about wider tensions in the Middle East. The improved outlook has provided some support to the US Dollar (USD) against the Swiss Franc (CHF).

Investors are eagerly awaiting the release of the US preliminary S&P Global Purchasing Managers Index (PMI) data for April on Tuesday, which is expected to provide fresh impetus to the market.

In recent developments, the Fed Bank of Chicago reported on Monday that the National Activity Index improved to 0.15 in March from the previous reading of 0.09. However, this data release had minimal impact on the Greenback. Instead, the USD gained momentum following hawkish remarks from US Federal Reserve (Fed) policymakers, leading to expectations that the central bank might delay any potential rate cuts. This sentiment bolstered the USD against the CHF.

Looking ahead, market participants are closely monitoring the US preliminary Gross Domestic Product Annualized for the first quarter (Q1) and March’s Personal Consumption Expenditures Price Index (PCE), scheduled for later this week. These events are expected to provide insights into the possibility of policy easing by the Fed. Upbeat data from these reports could further strengthen the USD and potentially limit the upside of the USD/CHF pair.

On the geopolitical front, ongoing tensions in the Middle East could drive safe-haven flows, benefiting the CHF. Additionally, market attention will be on the Swiss ZEW Survey for April, set to be released on Wednesday, and Swiss National Bank (SNB) Chairman Jordan’s speech scheduled for Friday. These events are anticipated to influence the trajectory of the USD/CHF pair in the coming days.

USDCAD – Soft Below 1.3700 Before US PMI Data

The Canadian Industrial producer price index came at 0.80% in the March month versus 1.1% printed in the previous month. Canadian retail sales data is scheduled this week and expected to come at 0.1% from -0.30% printed in the previous month. Oil prices are come down makes downward pressure to Canadian Dollar against counter pairs.

USDCAD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The USD/CAD pair continues its decline, trading around the 1.3695 level, despite the backdrop of lower crude oil prices. However, the downward momentum of the pair may face limitations due to robust US economic indicators and hawkish remarks from the Federal Reserve (Fed). Market participants are eagerly awaiting the release of the US S&P Global Purchasing Managers Index (PMI) data, with upcoming events including US Gross Domestic Product (GDP) and US Core Personal Consumption Expenditures (PCE) later in the week.

Several Fed policymakers have expressed consensus on maintaining current borrowing costs, citing the slow progress on inflation alongside the resilience of the US economy. New York Fed President John Williams emphasized a lack of urgency to adjust interest rates, highlighting the strength of the economy. Similarly, Chicago Fed President Austan Goolsbee noted that the Fed’s current monetary policy stance aligns with the robustness of US economic data. The prevailing narrative of higher interest rates for a prolonged period in the USD might bolster the greenback against its counterparts, with the Core US PCE potentially offering further insights into the inflationary landscape.

On the Canadian dollar (CAD) front, data from Statistics Canada indicated that Canadian Industrial Produce Prices met market expectations, decreasing by 0.8% month-over-month (MoM) in March, following an upwardly revised figure of 1.1% in the previous month. Concurrently, the decline in WTI prices exerts downward pressure on the Loonie, considering Canada’s status as the largest oil exporter to the United States. Anticipated events include the release of Canada’s Retail Sales data on Thursday, with expectations of an improvement to 0.1% MoM in February from a decline of 0.3% in January.

USD INDEX – USD steady on calm Monday

The US Dollar moved calm after the calming tensions of the middle east countries. Oil prices are coming down after the conflict ceasefire. September month rate cut from FED is higher on the poll of 85% and June month rate cut is 15% expected. Due to Hawkish speech from FED Members makes FED rate cut is vanishing each month depending on strong economic data printing.

USD Index is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The currency’s resilience is attributed to a combination of factors, including robust domestic economic indicators and persistent inflationary pressures, which have led to a more hawkish stance by the Federal Reserve (Fed).

The underlying strength of the US economy, characterized by rising yields and robust growth, contributes to the stability of the US Dollar. Some Fed officials have begun to entertain the idea of a rate hike, citing a lack of progress on inflation. Consequently, market expectations for the initiation of an easing cycle have been postponed. In the upcoming week, the release of key economic data, including Personal Consumption Expenditures (PCE) and Durable Goods for March, as well as Gross Domestic Product (GDP) estimates for the first quarter, alongside April’s S&P Purchasing Managers’ Index (PMI), are likely to influence sentiments regarding the Fed’s future monetary policy decisions.

Market analysts anticipate that a hawkish shift from the Fed, combined with increased US Treasury supply, could further drive up US Treasury bond yields, potentially leading to additional gains for the Greenback as investors adjust to the Fed’s evolving stance. Currently, market expectations assign a 15% probability of a rate cut in the upcoming June meeting, with higher probabilities for rate cuts in subsequent months. In the bond market, yields show a slight decline, with the 2-year yield at 4.97%, the 5-year yield at 4.64%, and the 10-year yield slightly lower at 4.61%.

GBPUSD – Near 1.2350, Awaiting UK, US PMI Data

The BoE Deputy Governor Dave Ramesdan said inflation is cooling in the UK economy and BoE do rate cuts before earlier. BoE is projected to do rate cuts in the August month and 2 rate cuts in this year. GBP is moving lower against USD after the rate cut hopes is more stronger as 60% in the near term.

GBPUSD is moving in the Symmetrical triangle pattern and the market has reached the higher low area of the pattern

The GBP/USD pair maintains a defensive stance, hovering near 1.2350, marking its lowest level since mid-November during the early Asian session on Tuesday. Concurrently, the USD Index (DXY) consolidates its recent gains above 106.10, as market participants await the release of preliminary S&P Global Purchasing Managers Index (PMI) data from both the US and UK for April.

Federal Reserve (Fed) policymakers have reached a consensus regarding the slow but persistent decrease in US inflation, emphasizing that inflation remains elevated. Consequently, the central bank is not rushing towards implementing interest rate cuts. Atlanta Fed President Raphael Bostic has indicated that interest rates will need to be maintained at a “restrictive level,” suggesting the possibility of easing only “at the end of 2024.” Similarly, Chicago Fed President Austan Goolsbee has suggested a prolonged timeline for rate cuts, citing that progress on inflation has “stalled.” The prevailing hawkish stance of the Fed on interest rates throughout this year has bolstered the US Dollar (USD), exerting downward pressure on the GBP/USD pair.

On Monday, the Chicago Fed National Activity Index demonstrated improvement, rising to 0.15 in March from 0.09 in the preceding reading, as reported by the Fed Bank of Chicago. Market focus now shifts to the release of April PMI reports, anticipated later on Tuesday. Projections suggest that both manufacturing and services PMI figures are expected to exhibit improvement for April. Any outcomes surpassing market expectations could potentially provide a boost to the Greenback, thereby limiting the upside potential of the GBP/USD pair.

Conversely, interest rate futures are currently fully priced in for a quarter-point interest rate cut by the Bank of England (BoE) in August, with expectations for two rate cuts by the year’s end. The growing speculation surrounding an earlier-than-anticipated interest rate cut by the UK central bank exerts downward pressure on the Pound Sterling (GBP). Last week, BoE Deputy Governor Dave Ramsden indicated that progress on UK inflation, coupled with a pessimistic economic outlook, could prompt the BoE to commence its rate-cutting cycle sooner than previously envisaged. Investors have priced in a 60% probability of a June rate cut, emphasizing market sentiment towards this potential monetary policy shift.

AUDJPY – Dips Despite Positive Aussie PMI, Focus on Monthly CPI

The Australian Judo Bank composite PMI data came at 53.6 in April month from 53.3 printed in the previous month. Services index expansion hopes for Second quarter after the reading came at 24-month high.The China has imposed 43.5% tariffs on import duty on US products like Propionic Acid, it is used for Food, seeds, and medical manufacturing products.

AUDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Australia’s Judo Bank Composite Purchasing Managers Index (PMI) surged to a 24-month high of 53.6 in April, indicating an accelerated expansion in the Australian private sector during the second quarter, particularly driven by the services sector. This improvement from the previous month’s 53.3 suggests robust growth prospects for the Australian economy.

Conversely, the Japanese Yen (JPY) faces challenges stemming from the expanding yield gap between Japan and many other major countries. This dynamic prompts traders to borrow JPY and invest in higher-yielding assets elsewhere, contributing to downward pressure on the currency.

In line with this, Bank of Japan (BoJ) Governor Kazuo Ueda reiterated the central bank’s commitment to raising interest rates if trend inflation accelerates toward its 2% target. However, Ueda also highlighted the difficulty in predicting the ideal timeframe for the BoJ to gather sufficient data before considering a policy change.

Market indicators reveal mixed sentiments across both economies. Australia’s Judo Bank Manufacturing PMI rose to an eight-month high of 49.9 in April, while Services PMI declined slightly to 54.2. On the other hand, Japan’s Jibun Bank Manufacturing PMI improved to 49.9, surpassing expectations, and Services PMI rose to 54.6.

Amidst these developments, China’s monetary policy decisions are also poised to impact the Australian market. The People’s Bank of China (PBoC) is expected to decrease the Medium-term Lending Facility (MLF) rate, aiming to lower funding costs. Additionally, China has imposed a new tariff on imports of propionic acid from the United States, potentially affecting various sectors.

Traders are closely monitoring upcoming economic data, particularly the Monthly Consumer Price Index and quarterly RBA Trimmed Mean CPI from Australia, expected to provide insights into inflation trends and potential monetary policy adjustments.

NZDUSD – Holds Above 0.5900 with Focus on Fed, US PMI, Kiwi Trade Balance

The NZDUSD is moving higher after the Middle East tensions are calm down. No Retaliation measures from Iran is the welcome one for Middle east countries. China is going to reduce the medium term lending rate makes NZ Dollar positive for the current stance.

NZDUSD is moving in the Symmetrical triangle pattern and the market has reached the higher low area of the pattern

During the Asian session on Tuesday, the NZD/USD pair experienced a slight downturn, hovering near the 0.5920 level. The New Zealand Dollar (NZD) received a boost from an improved risk appetite, contributing to the resilience of the NZD/USD pair. This positive sentiment stemmed from diminished geopolitical tensions in the Middle East, notably highlighted by a recent statement from an Iranian official indicating no immediate plans for retaliation against Israeli airstrikes.

However, despite the favorable market sentiment, the upside potential for the NZD/USD pair appears limited due to a hawkish tone surrounding the Federal Reserve’s (Fed) interest rate outlook for June. According to the CME FedWatch Tool, the probability of interest rates remaining unchanged in the June meeting has risen to 84.4%, up from the previous week’s 78.7%.

Furthermore, statements from Federal Reserve officials indicate a more hawkish stance regarding the trajectory of interest rates in June, potentially bolstering the US Dollar (USD). For instance, Chicago Fed President Austan Goolsbee remarked on Friday that progress on inflation had “stalled,” suggesting that the Federal Reserve’s current restrictive monetary policy is appropriate. Atlanta Fed President Raphael Bostic hinted that the US central bank would refrain from cutting interest rates until the end of the year.

On the economic front, the China Securities Journal hinted on Tuesday at the possibility of the People’s Bank of China (PBoC) reducing the Medium-term Lending Facility (MLF) rate on May 15 to lower funding costs. Given the strong trade ties between China and New Zealand, such a move could potentially influence New Zealand’s market dynamics and consequently impact the Kiwi Dollar.

Looking ahead, market participants will likely keep a close watch on New Zealand’s monthly Trade Balance NZD data for March scheduled for release on Wednesday. Additionally, ANZ-Roy Morgan Consumer Confidence figures for New Zealand are expected on Friday. In the United States (US), attention will be on the S&P Global Purchasing Managers Index (PMI) on Tuesday, with expectations of improvements in both the manufacturing and services sectors for April.

CRUDE OIL – WTI Oil below $82 on Middle East Calm, Hawkish Fed

The Crude Oil prices are moved lowered after the middle east tensions are calm down. China Growth is expected at 4.9% in 2024, it is up from 4.2% in the previous foreacast by ANZ Economists.

Crude Oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

China is suffering from Real estate crisis and weigh down the imports of Oil due to economy slowdown, this is also concerns for the Oil prices to come down.

Western Texas Intermediate (WTI), the US crude oil benchmark, is currently trading around $82.00 on Tuesday, maintaining a downward trajectory. This decline comes amid easing concerns over escalating tensions in the Middle East. The market is closely watching for cues from the preliminary US S&P Global Purchasing Managers Index (PMI) data for April and the API Weekly Crude Oil Stock report later in the day.

The recent statements from Iranian Foreign Minister Hossein Amirabdollahian indicating Iran’s reluctance to retaliate against Israel’s actions have contributed to the calm in the region. Despite Israel’s retaliatory strike, the overall silence from both sides suggests efforts to de-escalate tensions. However, any unforeseen escalation between the two nations could potentially provide support to WTI prices, preventing further downside.

Furthermore, the increase in US crude oil inventories, surpassing market expectations in recent weeks, continues to weigh on WTI prices. Additionally, hawkish comments from the Federal Reserve (Fed) have strengthened the US Dollar (USD), posing as a headwind for oil prices. Chicago Fed Austan Goolsbee’s remarks last week highlighted the Fed’s confidence in maintaining its current monetary policy stance in light of strong labor market conditions and persistent inflation pressures.

On the flip side, optimism surrounding Chinese demand offers a glimmer of hope for WTI prices. China, being the world’s largest oil importer, is expected to bolster its economy through fiscal and monetary stimulus measures. ANZ economists anticipate a growth rate of 4.9% for China’s economy in 2024, up from 4.2% previously projected. However, concerns persist regarding the fragility of the Chinese property sector, which could potentially dampen economic prospects and weigh on WTI prices in the future.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!