XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

XAUUSD – Gold price weakens as investors tread cautiously ahead of crucial US economic data.

The Gold prices are moved lower after the Middle east tensions calm down in the market, US Domestic data proved stronger last day in the core durable goods orders. US Dollar may be weak in the second quarter of 2024 due to rate hikes impact in the US economy will see in Second half of 2024.Q1 GDP and Core PCE index in the March month is scheduled this week.

Gold price (XAU/USD) faces resistance as it attempts to climb back above the $2,320 level in the early New York session on Wednesday. The precious metal continues to struggle for short-term momentum as safe-haven demand subsides amid easing tensions in the Middle East. Investors are exercising caution regarding bullions ahead of the release of key economic indicators from the United States, including the Q1 Gross Domestic Product (GDP) and the core Personal Consumption Expenditure Price Index (PCE) data for March, scheduled for Thursday and Friday, respectively.

Market participants are closely eyeing these data releases as they will provide insights into the timing of potential interest rate adjustments by the Federal Reserve (Fed). The US core PCE Inflation, which is the Fed’s preferred measure of inflation, is anticipated to have increased moderately by 0.3% in March, with annual figures expected to soften to 2.6% from the 2.8% recorded in February. A higher-than-expected inflation reading could prompt a significant sell-off in gold prices.

US inflation indicators, including the Consumer Price Index (CPI) and wage growth, have remained elevated in the first quarter. Continued signs of persistent price pressures would support the Fed’s stance of maintaining interest rates at current levels for an extended period, which historically diminishes the appeal of gold relative to the US Dollar and bond yields.

In the daily market overview, the bearish sentiment surrounding gold persists as safe-haven demand wanes following the easing of Middle East tensions. Although the precious metal experienced some relief after a decline to $2,300, its recovery was limited by a weakened US Dollar in response to the release of weak S&P Global preliminary PMI data for April. Both Manufacturing and Services PMI figures showed declines, with Manufacturing PMI even dropping below the 50.0 threshold, indicating a contraction in the sector.

Despite short-term fluctuations, the outlook for gold remains influenced by Fed policymakers’ views on the appropriateness of the current monetary policy framework, supported by robust labor demand and persistent price pressures. As investors await further economic data, particularly the US core PCE Price Index for March, speculation regarding the timing of potential Fed interest rate adjustments will likely intensify. Additionally, upbeat Durable Goods Orders for March, reported by the US Census Bureau, reflect strong demand by households, further shaping market sentiment toward gold prices.

EURUSD – German IFO Biz Climate Index: April at 89.4 vs. Expected 88.9

The German IFO Climate index surged to 89.1 in the April month from 87.9 printed in the March month, 88.9 is expected. Business economic assessment index came at 88.9 in the April month from 88.1 printed in the last month and 88.7 is expected. IFO expectations in the next six months rose to 89.9 in the April month from 87.7 printed in the March month. Overall German data came at higher than expected, but EURUSD moved flat after the data printed.

EURUSD is moving in Descending Triangle and market has reached support area of the pattern

In April, the German IFO Business Climate Index headline figure showed a substantial increase to 89.4, marking a significant improvement from the March level of 87.9. This figure exceeded market expectations, which had anticipated a reading of 88.9.

Furthermore, the Current Economic Assessment Index also saw a notable uptick from 88.1 in March to 88.9 in April, surpassing the forecasted value of 88.7.

Additionally, the IFO Expectations Index, which reflects firms’ outlook for the upcoming six months, demonstrated a strong rise to 89.9 in April, compared to 87.7 in March. This exceeded the anticipated value of 88.9, indicating increased optimism among businesses regarding future economic prospects.

USDJPY – climbs to 155.00 amidst US data, BoJ policy caution

The Senior Ruling party of Japan executive Ochi said currently no interventions in the FX Market, if reading goes to 160-170 range we see prompt action in the FX market by BoJ Officials. This hint gives Yen weakness against counter pairs and no more fear on rising rates from BoJ and interventions from BoJ.

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The USD/JPY pair surges to new heights, reaching 155.00 during Wednesday’s trading session in London. This uptrend is fueled by a boost in the US Dollar’s strength, driven by market uncertainty surrounding the forthcoming release of key economic indicators for the United States. Specifically, investors are awaiting the publication of the Q1 Gross Domestic Product (GDP) data and the core Personal Consumption Expenditure Price Index (PCE) figures for March, scheduled for Thursday and Friday. These data points are expected to significantly shape market expectations regarding the timing of potential interest rate adjustments by the Federal Reserve (Fed).

Market sentiment remains selective, with S&P 500 futures experiencing modest gains during the European session, while risk-associated currencies exhibit weakness against the US Dollar. The US Dollar Index (DXY) sees a slight uptick after encountering buying interest around the 105.70 level.

In Tuesday’s trading, the US Dollar underwent a notable correction following the release of a disappointing US preliminary Purchasing Managers’ Index (PMI) report for April by S&P Global. The report indicated that both the Manufacturing PMI, below the 50.0 threshold indicating contraction, and the Services PMI experienced a sharp decline. This suggests a potential slowdown in the previously robust US economic outlook.

Investors are particularly focused on today’s release of Durable Goods Orders data for March. In February, Durable Goods Orders increased by 1.4%, indicating resilience in long-term product demand. Strong Durable Goods Orders figures suggest persistent inflationary pressures.

Meanwhile, the Japanese Yen weakens amid expectations that the Bank of Japan (BoJ) will refrain from further interest rate hikes this week. The BoJ recently raised interest rates to 0%-0.1% after maintaining an ultra-loose monetary policy for 17 years. However, a Reuters poll suggests that the BoJ is likely to keep its policy unchanged until at least the June meeting, with potential tightening occurring later in the year. Concerns about potential Japanese intervention in the foreign exchange market to support the depreciating Yen intensify, with Senior Japan Ruling Party Executive Ochi indicating that excessive weakening of the Yen towards 160 or 170 against the Dollar could prompt policymakers to consider intervention measures.

USDCAD – Rebounds to 1.3700 Post Weak Canadian Retail Sales

The Canadian Retail sales for the month of February came at -0.10% versus 0.10% expected and -0.30% printed in the January month. This is turn reduces the CPI data in the upcoming months and give positive way for BoC to cut the rates soon in the June month. Slower demand from Consumers in the Canada makes lowering the cost of manufacturing goods at the factory gates.

USDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The USD/CAD pair demonstrated robust buying interest, climbing to the 1.3700 level following the release of weaker-than-anticipated Retail Sales data by Statistics Canada for the month of March. Retail Sales at brick-and-mortar stores contracted at a slower pace of 0.1%, contrasting with the 0.3% decline recorded in February. However, market expectations had projected a 0.1% increase in Retail Sales, making the actual figures disappointing.

Retail Sales serve as a crucial leading indicator of consumer spending, reflecting the demand from households. A decrease in Retail Sales implies subdued demand from consumers, prompting manufacturers to lower prices of goods and services. This downward pressure on consumer prices contributes to a reduction in consumer price inflation, potentially prompting the Bank of Canada (BoC) to initiate interest rate cuts sooner. Currently, financial markets are anticipating interest rate reductions by the BoC to commence as early as the June meeting.

Conversely, the US Dollar faces challenges in reclaiming ground above the immediate resistance level at 105.80. Investors appear to remain cautious in light of the impact of the weak S&P Global preliminary PMI report for April, which was released on Tuesday. The report indicated a dip in the Manufacturing PMI below the 50.0 threshold, alongside a significant decline in the Services PMI to 50.9.

Looking ahead, market focus will shift to the release of key economic data, including the Q1 Gross Domestic Product (GDP) figures and the core Personal Consumption Expenditure Price Index (PCE) data for March, scheduled for Thursday and Friday, respectively. These economic indicators will influence speculations regarding the timing of potential rate cuts by the Federal Reserve (Fed). Presently, market expectations suggest that rate cuts by the Fed may commence from the September meeting.

USDCHF – remains under 0.9150 ahead of US GDP data

The Swiss ZEW Survey expecations reading came at 17.6 in the April month from 11.5 in the Previous month. Middle east tensions calm down makes Swiss Franc lower against counter pairs.

USDCHF is moving in the Box pattern and the market has fallen from the resistance area of the pattern

US Q1 GDP is expected at 2.4% from 3.6% printed in the previous quarter. So US Dollar is moving in the flat against CHF in the market.

During the early European session on Thursday, the USD/CHF pair trades near 0.9145, reflecting a weaker stance. Traders are adopting a cautious approach as they await the release of the US preliminary Gross Domestic Product (GDP) Annualized data for the first quarter (Q1) later in the day. Any developments regarding escalating tensions in the Middle East could potentially boost safe-haven assets like the Swiss Franc (CHF).

The recent stance of the US Federal Reserve (Fed) policymakers, maintaining the current monetary policy, has lent some support to the Greenback in recent weeks. However, uncertainty prevails regarding the timing of any future monetary policy adjustments. The upcoming US GDP growth data for Q1 2024 might provide insights into the performance of the US economy during that period.

Initial estimates suggest that US GDP growth in Q1 is anticipated to be around 2.5% on an annualized basis, compared to the previous reading of 3.4%. A stronger-than-expected GDP figure could lead to speculation that the Fed might delay any potential rate cuts, thereby potentially boosting the US Dollar (USD).

Meanwhile, recent data from the Centre for European Economic Research indicated an improvement in Switzerland’s ZEW Survey Expectations to 17.6 in April from 11.5 in the previous reading. Additionally, ongoing geopolitical tensions in the Middle East may elevate the CHF, considered a traditional safe-haven currency, consequently putting downward pressure on the USD/CHF pair.

USD INDEX – US Durable Goods Orders up 2.6% in March at $283.4B

The US Core Durable goods order rose to 2.6% in the March month and 0.70% printed in the February month. Excluding transportation rose to 0.20% and Excluding defense rose to 2.3%. Transportation equipment’s rose to $6.8 billion and totally $95.9 billion orders came in the March month.

USD Index is moving in an Ascending channel and the market has reached the higher low area of the channel

The US Census Bureau released data on Wednesday indicating that Durable Goods Orders in the United States experienced a notable increase of 2.6%, amounting to $7.3 billion, reaching a total of $283.4 billion for the month of March. This growth follows a revised 0.7% uptick (originally reported at 1.4%) in February.

According to the press release from the US Census Bureau, when excluding transportation, new orders saw a more modest increase of 0.2%. Excluding defense-related orders, there was a more substantial rise of 2.3%. Notably, the surge in orders for transportation equipment, which has seen growth for two consecutive months, led the overall increase, amounting to $6.8 billion or a 7.7% increase, bringing the total to $95.9 billion.

GBPUSD – GBP Recovery Halts on Early BoE Rate Cut Speculation

GBP Composite PMI data for the month of April came at 54.9 from 53.1 in the March month and 53.0 is expected, manufacturing PMI data came at below 50.00 Since January 2024, Services PMI data came at 53.0 in the April month.

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

New Busniess activity increases in the UK makes consumer spending to increase more in the Upcoming days, So BoE may delay rate cuts to August month. UK Policy maker Jonathan Haskel said Labour market is main heart of inflation to increase, if labour market eased then inflation come to our target of 2%.

The Pound Sterling (GBP) finds itself in a sideways trend around the 1.2450 mark versus the US Dollar (USD) during the early American session on Wednesday, following a robust recovery from a five-month low around 1.2300. The GBP/USD pair grapples with directionality as the US Dollar consolidates its position after a notable correction on Tuesday. The US Dollar Index (DXY), gauging the currency’s strength against six key counterparts, endeavors to stabilize near the 105.70 level. Furthermore, uncertainty surrounding the timing of potential rate cuts by the Bank of England (BoE) contributes to the pause in the Pound Sterling’s recovery.

In Tuesday’s trading session, the USD faced downward pressure following the unexpected release of weak preliminary US PMI figures by S&P Global. The Manufacturing PMI slipped below the pivotal 50.0 threshold, indicating a contraction in the sector, while the Services PMI registered a sharp decline to 50.9.

Conversely, the Pound Sterling witnessed a notable upward surge subsequent to the release of a robust preliminary PMI report for the United Kingdom by S&P Global/CIPS. Despite investor expectations of a slight decline to 53.0, the Services PMI surged to 54.9 from its previous reading of 53.1. However, the preliminary Manufacturing PMI unexpectedly dipped below the 50.0 mark, indicating a contraction after being in expansion territory since January. The factory PMI plummeted to 48.7, significantly below both expectations and the prior reading of 50.3.

Moreover, S&P Global/CIPS reported an increase in new business volumes across the private sector in April, marking the strongest growth rate since May 2023. However, this expansion was primarily centered on the service economy, while manufacturers experienced a moderate downturn in order books.

The strong new business volumes signal a positive consumer spending outlook, which could potentially elevate inflationary pressures and allow the Bank of England (BoE) to postpone interest-rate cuts. This scenario presents a favorable backdrop for the Pound Sterling’s performance.

However, the Pound Sterling faces challenges in extending its recovery above the 1.2450 level, as firm expectations for early rate cuts by the BoE counterbalance the impact of the upbeat S&P Global/CIPS PMI report. Traders remain divided between predicting rate cuts by the BoE before or after the Federal Reserve (Fed), with opinions leaning slightly towards August over June. Commentaries from BoE policymakers further complicate the timing of the first interest rate cut. While BoE Deputy Governor Dave Ramsden expresses confidence in inflation returning to the 2% target by May, BoE policymaker Jonathan Haskel expresses concerns about persistent inflation due to tight labor market conditions, emphasizing the centrality of the labor market in inflation dynamics.

AUDUSD – Climbs Further as Q1 Inflation Proves Persistent

The Australian CPI Q1 came at 3.6% versus 3.4% expected and 4.1% printed in the last quarter. This data proved RBA may be do rate cut in February 2025 instead of November 2024. Continuing headwinds for Australian Dollar to move up after the CPI rose to unexpected level last day.

AUDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

AUD/USD experienced a slight retreat from its intraday highs, hovering just below the 0.6500 mark on Wednesday. The currency pair had surged to 0.6530 overnight following the release of Australian inflation data for the first quarter, which proved to be stickier than anticipated. Economists had forecasted a rise in prices by 3.4%, but the actual Consumer Price Index (CPI) data showed a 3.6% increase.

The unexpected resilience in inflation figures suggests that the Reserve Bank of Australia (RBA) may be less inclined to implement interest rate cuts in the near future. This outlook served as a catalyst for the continuation of the AUD/USD recovery, as the expectation of prolonged high interest rates is favorable for the Australian Dollar. Heightened interest rates tend to attract more foreign capital, thus bolstering demand for the AUD.

AUD/USD emerged as the leading performer among major currencies, recording three consecutive days of gains and showcasing the strongest performance within the G10 currency group over a five-day period. Market sentiment indicates that the RBA is likely to be among the last central banks within the G10 to reduce interest rates, providing a supportive backdrop for the Australian Dollar.

Rabobank analysts noted that the stronger-than-expected inflationary pressures in Q1 could prompt the RBA to upwardly revise its inflation forecasts at the upcoming May meeting. Coupled with underwhelming US PMI data from Tuesday, which undermined the notion of US economic exceptionalism, Rabobank anticipates further upward momentum for AUD/USD in the foreseeable future.

TD Securities analysts have revised their prediction for an RBA rate cut, now projecting the first cut to occur in February 2025 rather than November. This shift in expectations aligns with a more hawkish stance from the RBA, although actual action is expected to be deferred.

However, Societe Generale analysts caution that sustained upward movement in AUD/USD may hinge on a decline in US yields. They assert that even with reduced prospects of RBA rate cuts, AUD/USD’s ascent above 0.6500 could be contingent on a retreat in US yields.

NZDUSD – climbs near 0.5950 amid improved risk appetite

The NZ Dollar moved higher against USD after the Iran said no retailiation on Israel now, this comment makes NZ Dollar stronger against counter pairs. The People Bank of China is planning to reduce the medium term rates inorder to boost the consumer spending, China is boosting to import NZ goods to their economy more.

NZDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The NZD/USD pair is on an upward trajectory, hovering around 0.5940 during the Asian trading session on Thursday. The New Zealand Dollar (NZD) is gaining strength as investor sentiment improves. Optimism prevails amidst indications of potential de-escalation in tensions between Iran and Israel, following remarks by an Iranian official suggesting no immediate retaliation against Israeli airstrikes.

Reports from the China Securities Journal indicate plans by the People’s Bank of China (PBoC) to lower the Medium-term Lending Facility (MLF) rate during its upcoming rate setting on May 15. This move is aimed at reducing funding costs, potentially stimulating economic activity in China. Consequently, increased consumer spending in China may bolster demand for New Zealand exports, supporting the NZD.

Meanwhile, the US Dollar Index (DXY), reflecting the USD’s performance against major currencies, experienced a decline after mixed manufacturing data from the US. However, gains in US Treasury yields partially offset the Greenback’s losses.

In the US, the Department of Commerce reported a 2.6% month-over-month (MoM) increase in Durable Goods Orders for March, surpassing both the previous reading of 0.7% and the anticipated 2.5%. However, core goods, excluding transportation, saw a modest 0.2% MoM growth, falling short of the projected 0.3%.

Investor focus now shifts to the release of preliminary Q1 Gross Domestic Product Annualized data for the US on Thursday. Expectations suggest a slowdown in growth, with these figures offering crucial insights into the state of the US economy. The outcome could influence future decisions by the Federal Reserve (Fed).

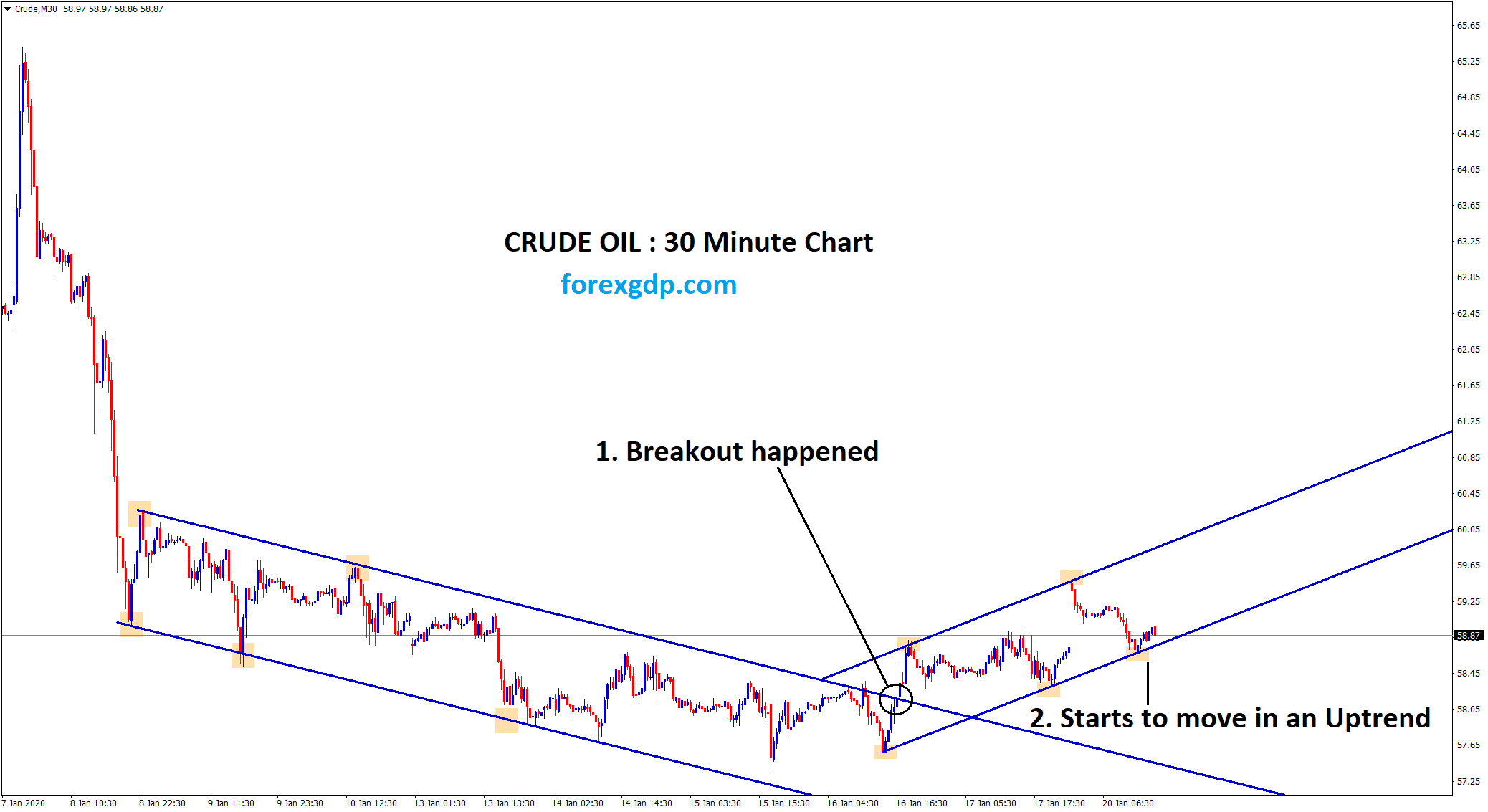

CRUDE OIL – WTI slips under $82.50 amid easing Middle East worries

The Crude Oil prices are moving down against USD after the Middle east conflict lowered, various sanctions against Iran were imposed by US. So Oil supply increases after the sanctions, US Energy commission agency said April 19 ending 6.368 million barrels Decrease from 2.34 Million barrels builit up last week ending. This demand shows boost the Oil prices in the coming weeks.

XTIUSD Crude oil price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Western Texas Intermediate (WTI), the benchmark for US crude oil, is currently trading around $82.45 per barrel on Thursday. The price of oil is experiencing a slight decline as concerns about a potential escalation of tensions in the Middle East ease. Additionally, the recent hawkish stance taken by the Federal Reserve (Fed) is contributing to the strength of the US dollar (USD), which in turn is putting pressure on oil prices.

Recent developments indicating a reduction in tensions between Iran and Israel, along with uninterrupted oil flow from the Middle East despite regional conflicts, have led to a decrease in WTI prices over the past few sessions. However, any signs of renewed geopolitical tensions in the Middle East or the imposition of stricter sanctions on Iran could provide support to oil prices and limit further downside.

Moreover, the growing speculation that the Federal Reserve (Fed) might delay interest rate hikes is bolstering the US dollar, which acts as a deterrent for oil prices. A stronger dollar makes oil more expensive for buyers holding other currencies. Several Fed officials have indicated that interest rate cuts are not imminent as inflation remains higher than anticipated.

On the supply side, data from the Energy Information Administration shows that US commercial crude stockpiles for the week ending April 19 saw a significant decrease of 6.368 million barrels, marking the largest drawdown since mid-January. This drawdown suggests a tightening of supply, which could potentially support oil prices amidst other market factors.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!