GBPUSD Dips Below 1.2500 on Diminished Fed Rate Cut Prospects

The GBP pairs plummeted down on Friday even Friday UK GDP Data printed at 0.10% expanded in February month when compared to 0.20% expanded in January month. This two months expansion shows Second half of recession is swallowed. FED Rate cuts from June month is totally faded by economist view makes US Dollar stronger against GBP. This week GBP CPI data will determine the BoE Policy rate cuts in the upcoming meetings.

In Friday’s London session, the GBP/USD pair slipped below the critical psychological level of 1.2500. This decline in the Cable is attributed to the strength of the US Dollar, which continues to attract demand amid persistent inflationary pressures in the United States. The latest US inflation data for March, which surpassed expectations, has led traders to recalibrate their projections for Federal Reserve (Fed) rate cuts, previously anticipated for the June and July meetings.

GBPUSD is moving in Ascending channel and market has fallen from the higher high area of the channel

Market sentiment has turned pessimistic, with expectations now shifting towards the Fed initiating rate cuts starting from the September meeting. Furthermore, investors now anticipate only two rate cuts this year, compared to initial expectations of six at the beginning of the year.

In the European session, S&P 500 futures experienced some losses, while the US Dollar Index (DXY) climbed to nearly 106.00. This uptick in the DXY reflects hopes that the Fed will delay interest rate reductions relative to other developed economies’ central banks. Meanwhile, 10-year US Treasury yields saw a slight retreat from their four-month high around 4.60%.

Looking ahead, market focus turns to the release of the monthly Retail Sales data for March, scheduled for Friday. This data, representing household spending, is expected to show a slower growth rate of 0.3% compared to the previous reading of 0.6%, potentially alleviating concerns about persistently high inflation.

On the UK front, despite positive factory data and an anticipated rise in the monthly Gross Domestic Product (GDP) for February, the Pound Sterling struggled to attract buyers. UK GDP expanded by the expected 0.1% following a 0.2% increase in January. The evidence of growth in the first two months suggests that the technical recession recorded in the second half of 2023 was relatively mild.

Looking ahead to next week, market participants will closely monitor the release of the GBP Consumer Price Index (CPI) and labor market data, which will significantly impact speculation regarding the Bank of England’s (BoE) potential decision to initiate interest rate reductions. Currently, financial markets are expecting such cuts to begin from August.

GBPUSD Outlook: Pound Falls Amid Rising Geopolitical Tensions, BoE-Fed Differences

The GBP pairs plummeted down on Friday even Friday UK GDP Data printed at 0.10% expanded in February month when compared to 0.20% expanded in January month. This two months expansion shows Second half of recession is swallowed. FED Rate cuts from June month is totally faded by economist view makes US Dollar stronger against GBP. This week GBP CPI data will determine the BoE Policy rate cuts in the upcoming meetings.

Pound Sterling Loses Ground Amidst Renewed Dollar Demand

After a brief recovery earlier in the week, the GBP/USD pair faces renewed selling pressure as demand for the US Dollar surges once again. Factors contributing to the resurgence of the Greenback include expectations surrounding the US Federal Reserve (Fed) policy, geopolitical tensions, and robust economic data.

The US Consumer Price Index (CPI) data for March, released mid-week, exceeded expectations, indicating higher inflationary pressures than anticipated. This has led to a revision in market expectations for a Fed rate cut, with the probability of a June cut decreasing significantly. Additionally, hawkish comments from several Fed policymakers and strong core Producer Price Index (PPI) figures further support the case for delaying any policy changes by the Fed.

Geopolitical tensions, particularly in the Middle East, also contribute to the Dollar’s strength. Reports of potential strikes by Iran or its proxies against Israel have heightened concerns, prompting responses from various countries and escalating tensions in the region.

Meanwhile, in the United Kingdom, Bank of England (BoE) policymaker Megan Greene’s remarks suggest a less dovish stance, citing higher services inflation compared to the US. However, despite some support from this, the Pound remains vulnerable to Dollar strength.

On the economic front, the UK Gross Domestic Product (GDP) and industrial figures for February, though in line with expectations, fail to inspire confidence in the Pound.

Looking ahead, the focus shifts to the UK Consumer Price Index (CPI) data for March, set to be released mid-week. While the UK’s economic calendar is relatively light, market participants will closely monitor speeches from BoE policymakers and key economic indicators from the US for further insights into monetary policy directions and market sentiment.

GBP Falls to 4.5-Month Low, UK GDP Edges Up

The GBP pairs plummeted down on Friday even Friday UK GDP Data printed at 0.10% expanded in February month when compared to 0.20% expanded in January month. This two months expansion shows Second half of recession is swallowed. FED Rate cuts from June month is totally faded by economist view makes US Dollar stronger against GBP. This week GBP CPI data will determine the BoE Policy rate cuts in the upcoming meetings.

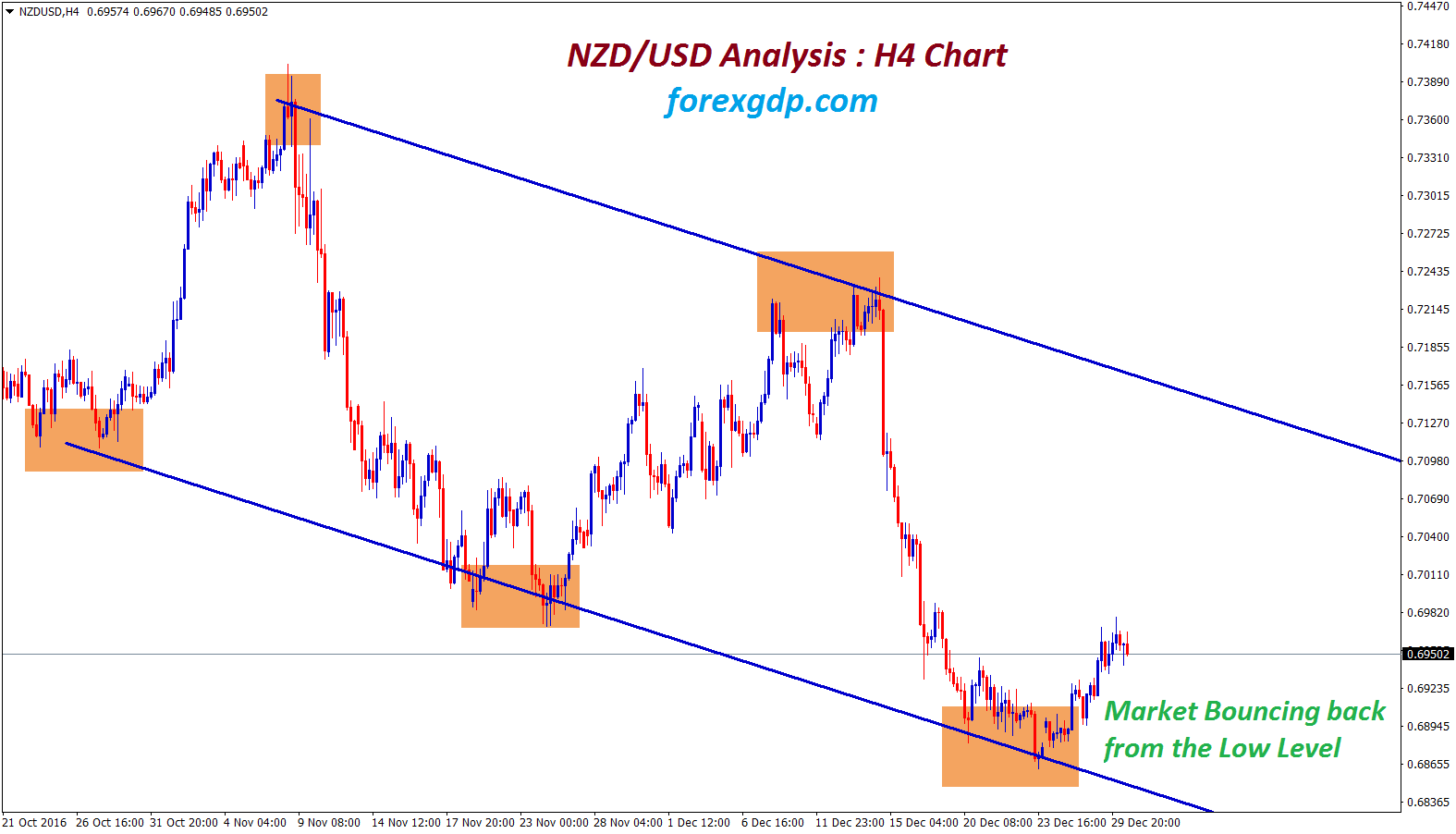

GBPUSD is moving in Descending channel and market has reached lower low area of the channel

The British pound faced downward pressure on Friday, with GBP/USD trading at 1.2594 during the European session, marking a decline of 0.47%. This decline adds to the pound’s weekly losses, which amount to 1.1%. Earlier today, the pound dropped to 1.2489, its lowest level since November 23.

UK GDP Shows Modest Growth

The UK economy recorded a modest growth of 0.1% month-on-month (m/m) in February, marking a second consecutive month of expansion following an upwardly revised 0.3% gain in January. This growth comes after the UK experienced a technical recession in the latter part of 2023 but appears to be on track for a slight expansion in the first quarter of this year.

March saw a notable rebound in the UK manufacturing sector. Manufacturing production surged by 1.2% m/m, a significant improvement from the previous month’s -0.2%, and surpassing market expectations of 0.1%. Industrial production also showed strength, rising by 1.1% m/m, following a 0.3% decline in February and exceeding market forecasts of no change.

However, the UK economy remains fragile despite these positive signs. Services recorded a meager growth of 0.1% m/m in March, while construction output experienced a decline of 1.9%. In comparison to other G-7 economies, the UK continues to lag behind, ranking ahead of only Germany.

Bank of England’s Cautious Approach

The Bank of England (BoE) has maintained its policy rate for five consecutive meetings, and today’s GDP data is unlikely to prompt a change in its cautious stance of keeping rates “higher for longer.” Although inflation dropped to 3.4% in February, it remains well above the BoE’s 2% target. Therefore, the BoE is expected to be hesitant to consider rate cuts until inflation shows further signs of decline.

In the United States, Federal Reserve officials are adopting a hawkish tone regarding rate cuts following robust economic data in March. Nonfarm payrolls exceeded expectations with a gain of 303,000 jobs, while the Consumer Price Index (CPI) continued to accelerate, reaching 3.5%. Fed members John Williams and Susan Collins have indicated that the Fed remains cautious about inflation and sees no immediate need to rush into rate cuts.

ECB Survey: Eurozone Inflation Forecasted at 2.4% This Year

The ECB inflation forecast survey shows no change from the previous polls. Inflation for the Euro zone remained at 2.4% in 2024 and 2.0% in 2025 and 2026. GDP will be expanded by 0.50% in 2024 and 1.4% in 2025 and 1.3% in 2026.Core inflation data will be 2.6% in 2024, 2.1% in 2025 and 2.0% in 2026. ECB Survey shows less inflation towards target of 2% only, So Euro currency plummeted against US Dollar last week.

The European Central Bank (ECB) released the latest results from its Survey of Professional Forecasters (SPF) on Friday, revealing that the inflation projections remain steady compared to the previous round of the survey conducted three months earlier.

EURUSD is moving in Descending channel and market has reached lower high area of the channel

Here are the key highlights from the survey:

- Inflation Forecasts: According to the SPF findings, inflation in the Eurozone is expected to remain at 2.4% for the current year. Looking ahead, the forecast indicates a slight moderation, with inflation projected to reach 2.0% in 2025, 2026, and in the longer term.

- Core Inflation: Core inflation, which excludes volatile food and energy prices, is anticipated to stand at 2.6% in 2024, showing a slight decline to 2.1% in 2025, and stabilizing at 2.0% in 2026.

- Economic Growth Projections: The SPF survey also included forecasts for economic growth. Minimal revisions were made to these projections, with Gross Domestic Product (GDP) expected to expand by 0.5% in the current year. Looking further ahead, GDP growth is forecasted to reach 1.4% next year and in 2026, and then settle at 1.3% thereafter.

Eurozone inflation expected to dip to 2% – ECB survey

The ECB inflation forecast survey shows no change from the previous polls. Inflation for the Euro zone remained at 2.4% in 2024 and 2.0% in 2025 and 2026. GDP will be expanded by 0.50% in 2024 and 1.4% in 2025 and 1.3% in 2026.Core inflation data will be 2.6% in 2024, 2.1% in 2025 and 2.0% in 2026. ECB Survey shows less inflation towards target of 2% only, So Euro currency plummeted against US Dollar last week.

Economists participating in the European Central Bank’s (ECB) Survey of Professional Forecasters (SPF) remain resolute in their outlook for euro zone inflation, projecting it to decline to 2% and maintain that level over the forecast horizon. According to the latest SPF results released on Friday, inflation is expected to stand at 2.4% for the current year and settle at 2.0% in 2025, 2026, and in the longer term, showing no change from the previous poll conducted three months earlier.

Furthermore, revisions to economic growth forecasts were minimal, indicating a subdued outlook. Gross Domestic Product (GDP) is anticipated to expand by 0.5% in the current year, followed by growth of 1.4% in the subsequent year and in 2026. Beyond that, GDP growth is projected to reach 1.3%.

The ECB, while maintaining interest rates at a record high in its recent decision, hinted at the possibility of rate cuts as early as June. This move comes amidst concerns over persistently high inflation in the United States, potentially delaying similar actions by the U.S. Federal Reserve.

The SPF’s findings are based on responses from 61 economists representing European companies and financial institutions. The survey was conducted between March 18 and 21, providing valuable insights into the economic outlook for the euro zone.

EU inflation forecasted to decline from 2.4% in 2024 to 2% in 2025 and 2026: ECB

The ECB inflation forecast survey shows no change from the previous polls. Inflation for the Euro zone remained at 2.4% in 2024 and 2.0% in 2025 and 2026. GDP will be expanded by 0.50% in 2024 and 1.4% in 2025 and 1.3% in 2026.Core inflation data will be 2.6% in 2024, 2.1% in 2025 and 2.0% in 2026. ECB Survey shows less inflation towards target of 2% only, So Euro currency plummeted against US Dollar last week.

EURUSD has broken Descending Triangle in downside

According to the European Central Bank’s (ECB) survey of professional forecasters for the second quarter of this year, headline inflation in the European Union (EU), measured by the harmonised index of consumer prices (HICP), is anticipated to decrease from 2.4 per cent in the current year to 2 per cent in both 2025 and 2026. This projection remained consistent with the previous round of the survey.

The expectations for core HICP inflation, which excludes energy and food, also remained steady from 2024 to 2026, with longer-term expectations unchanged at 2 per cent, as stated in an ECB release.

Economists participating in the survey predicted real gross domestic product (GDP) growth of 0.5 per cent for the current year, followed by expansions of 1.4 per cent in both 2025 and 2026.

Compared to the preceding survey round, expectations for 2024 and 2025 underwent slight downward and upward revisions of 0.1 percentage point, respectively, while projections for 2026 remained unaltered.

In terms of short-term GDP outlook, respondents anticipated a gradual strengthening of economic activity throughout the current year, while longer-term growth expectations held steady at 1.3 per cent.

Forecasts for the unemployment rate saw a minor downward revision across the entire horizon. Although participants expected the unemployment rate to rise to 6.6 per cent in the current year, they projected declines to 6.5 per cent in 2026 and further to 6.4 per cent in the longer term.

CAD Week Ahead: Inflation Data and Rate Cut Speculation Disruption

The Canadian CPI data for the March month is expected to ease and 2.8% printed in February month. BoC is expected to cut the rates in June month meeting due to CPI data is easing month on Month.

USDCAD has broken Ascending channel in upside

Next week, Canada is set to release its Consumer Price Index (CPI) data on Tuesday, drawing significant attention from investors. Despite global concerns about persistent inflationary pressures, the possibility of a rate cut by the Bank of Canada (BoC) in June remains on the table.

")

In February, Canada’s headline CPI rate moderated to 2.8%, with underlying measures showing similar declines. If this downward trend continues in March, it could raise the likelihood of a rate cut in June. Currently, market expectations for a rate cut in June are below 50%, but a further decline in inflation could increase pressure on the Canadian dollar.

Since the beginning of the year, the Canadian dollar has already depreciated by approximately 3.5% against the US dollar. Any indications of a potential divergence in monetary policy between the Federal Reserve and the Bank of Canada could exacerbate these losses further.

CAD Inflation Data Ahead: Rate Cut Bets Disrupted

The Canadian CPI data for the March month is expected to ease and 2.8% printed in February month. BoC is expected to cut the rates in June month meeting due to CPI data is easing month on Month.

USDCAD is moving in box pattern and market has rebounded from the support area of the pattern

Next week, on Tuesday, Canada is set to release its Consumer Price Index (CPI) data, drawing attention to the state of inflation in the country. Despite global concerns over persistent inflation, the Bank of Canada (BoC) is still considering a rate cut in June.

In February, Canada’s headline CPI rate eased to 2.8%, and underlying measures also declined. If this trend continues into March, it could increase the likelihood of a rate cut in June, which currently stands at less than 50%. Such a move would add further pressure on the Canadian dollar.

The Canadian dollar has already depreciated by approximately 3.5% against the US dollar this year. Any indications of a divergence in monetary policy between the Federal Reserve (Fed) and the BoC could exacerbate these losses.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals , 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!